Billion-Dollar Market Opportunity: Digital Diabetes Management Shifts from 2C to 2B Amid Over 200 Million Affected Individuals in China

As a new force driving disruptive industrial transformation, digital technology has gradually permeated every sector of healthcare. Chronic disease management, a vital component of the healthcare industry, will see its ecosystem reshaped by digital technologies. Diabetes, being one of the primary conditions in chronic disease management, must align with this digital trend, proactively pursue innovative breakthroughs, and establish a digital ecosystem for diabetes management.

According to data released by the IDF (International Diabetes Federation),In 2018, the number of diagnosed diabetes patients in China reached 114.39 million. When combined with 148.70 million individuals in the prediabetic stage, the total population affected by diabetes exceeded 260 million, making China the country with the largest diabetic population globally. By 2025, the diabetic population is projected to reach 320 million, creating a vast market for diabetes management.

Faced with such a vast market, digital diabetes management companies sprang up like mushrooms between 2015 and 2016, peaking at over 500 firms and creating the phenomenon known as the “Hundred Sugar Wars.” After several years, most of these enterprises have vanished, with fewer than 30 surviving.

What are the current issues with digital management models for diabetes, what is the optimal path forward for digital diabetes management, and what resources are required to support it?

To address the aforementioned questions, VCBeat has conducted research on companies engaged in digital diabetes management and interviewed field experts. By organizing and analyzing the data collected from these surveys and interviews, VCBeat has authored the “Report on Digital Innovation in Diabetes Management,” aiming to identify effective solutions and provide references for the digital transformation of diabetes management, and even chronic disease management as a whole.

Key Takeaways:

1. In 2025, the diabetic population will exceed 300 million, and the market size for diabetes management is expected to reach RMB 135 billion.

2. The business model for digital diabetes management is transitioning from C-end app services to B-end SaaS services.

3. The integrated digital management platform for the entire course of diabetes will consolidate resources from multiple stakeholders—including healthcare institutions, pharmaceutical companies, medical device manufacturers, pharmacies, commercial insurance providers, and health management organizations—to build an ecosystem service system encompassing “medical care + pharmaceuticals + insurance + management.”

4. Medication Therapy Management for Diabetes Is a Critical Area Requiring Breakthroughs in Digital Technology

5. The digital diabetes management industry is still in its growth stage regarding investment and financing, with B2B service providers securing relatively higher funding.

6. Expansion of Digital Diabetes Management from Single-Disease Management to an Integrated, Interconnected Information Platform

Concept

Diabetes is a chronic disease caused by defects in insulin secretion or action, characterized by chronic hyperglycemia accompanied by disorders of carbohydrate, fat, and protein metabolism.Mainly includes type 1 diabetes, type 2 diabetes, gestational diabetes, and specific types of diabetes.。

Digital Management of Diabetes IsRefers to a medical behavior management process in which healthcare institutions or physicians conduct remote interventions for individuals with diabetes (including patients with diabetes and those with prediabetes) using digital diabetes management software and smart hardware, or in which these individuals utilize relevant digital tools for self-management, with the aim of controlling the condition and preventing deterioration.。

(1) Diabetes mellitus patients are defined as individuals presenting with typical diabetic symptoms (polydipsia, polyuria, polyphagia, and unexplained weight loss) and exhibiting either a random venous plasma glucose level ≥11.1 mmol/L, a fasting plasma glucose (FPG) level ≥7.0 mmol/L, or a 2-hour plasma glucose level of 11.1 mmol/L during an oral glucose tolerance test (OGTT).

(2) The prediabetic population refers to individuals with impaired glucose regulation, whose blood glucose levels fall between normal values and the diagnostic thresholds for diabetes, placing them at high risk for developing diabetes.

(3) Digital management of diabetes includes health education, online consultation, real-time blood glucose monitoring, insulin delivery control, intelligent medication management, physician tools, patient education, dietary management, patient communities, and exercise management.

(4) Digital diabetes management software primarily consists of diabetes management apps, while digital diabetes management hardware is mainly dominated by smart glucose meters and smart insulin pumps.

Market Role

The market roles of enterprises providing digital management services for diabetes are mainly divided into two categories,One is to provide an app for online management targeting physicians or individuals with diabetes; the other is to offer SaaS services to healthcare institutions, enabling the development of tiered diagnosis and treatment platforms or diabetes management platforms.。

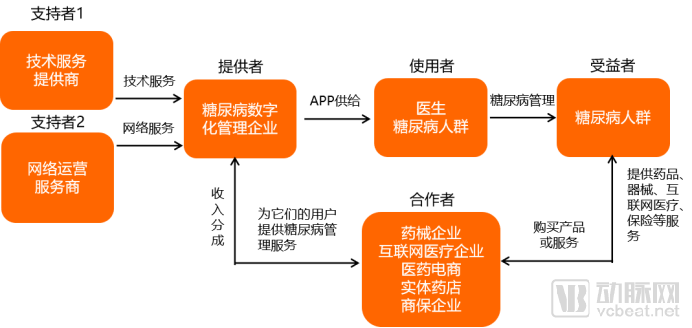

Figure 1: Market Stakeholder Relationship Map for the Digital Diabetes Management Industry

Image source: VCBeat

Image source: VCBeat

(1) Users: Physicians or individuals with diabetes. Physicians utilize the physician-side app for post-consultation management of patients with diabetes, while individuals with diabetes use the patient-side app to access health education materials, log blood glucose levels, engage in online consultations, purchase medications online, and participate in community discussions.

(2) Beneficiaries: The diabetic population, including patients with diabetes and individuals with prediabetes. Whether used by physicians or by the diabetic population themselves, diabetes management apps aim to achieve glycemic control in this group.

(3) Providers: Digital diabetes management companies that provide diabetes management apps to physicians or individuals with diabetes, along with online services such as blood glucose monitoring, disease education, online consultations, medication management, and patient communities.

(4) Supporters: Technical service providers and network operation service providers. The former provides foundational technical support for the development of diabetes management apps, while the latter provides network services to ensure the normal operation of these apps.

(5) Partners: pharmaceutical and medical device companies, internet healthcare providers, pharmaceutical e-commerce platforms, brick-and-mortar pharmacies, commercial insurance companies, etc. Pharmaceutical and medical device companies supply diabetes medications, blood glucose meters, insulin pumps, and other products; internet healthcare providers offer online follow-up consultations and prescription renewals; pharmaceutical e-commerce platforms and brick-and-mortar pharmacies facilitate medication sales; and commercial insurance companies provide diabetes-specific insurance products. These institutions collaborate with digital diabetes management enterprises to deliver a closed-loop service model integrating “medical care + medication + insurance + management” for individuals with diabetes.

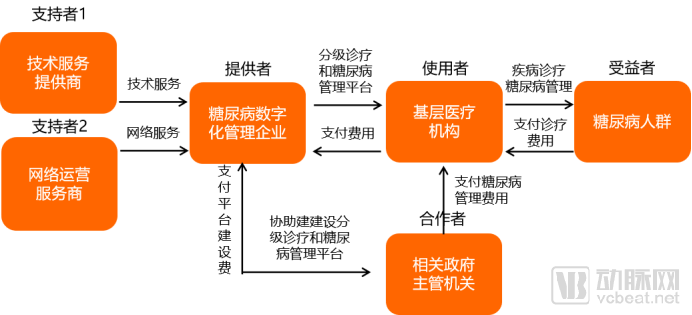

Figure 2. Relationship Map of Market Roles in the Digital Diabetes Management Industry

Image source: VCBeat

Image source: VCBeat

(1) Users: Primary healthcare institutions, which utilize the tiered diagnosis and treatment platform and the diabetes management platform to provide disease diagnosis and treatment as well as diabetes management services for the diabetic population.

(2) Beneficiaries: The diabetic population, including patients with diabetes and individuals with prediabetes. Primary healthcare institutions utilize tiered diagnosis and treatment platforms and diabetes management platforms to provide online consultation services for diabetic patients and achieve blood glucose control in the diabetic population.

(3) Provider: Digital diabetes management companies that build tiered diagnosis and treatment platforms and diabetes management platforms for primary healthcare institutions.

(4) Supporters: Technology service providers and network operation service providers. The former provides fundamental technical support for the development of the tiered diagnosis and treatment platform and the diabetes management platform, while the latter provides network services to ensure the normal operation of the platforms.

(5) Collaborators: Relevant government authorities, including local governments, Health Commissions, Finance Bureaus, and Healthcare Security Administrations. With the support of these government agencies, digital diabetes management enterprises establish tiered diagnosis and treatment platforms and diabetes management platforms for local primary healthcare institutions.

Patient Population

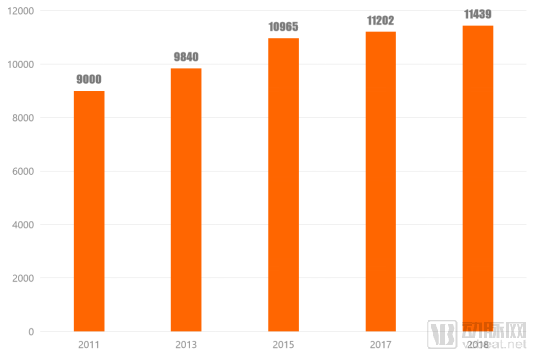

According to data released by the International Diabetes Federation (IDF),In 2018, the number of diagnosed diabetes patients in China reached 114.39 million, accounting for 8.2% of the total population, making it the country with the largest diabetic population globally.。

Figure 3. Number of Diagnosed Diabetes Patients, 2011–2018 (in ten thousands)

Data sources: IDF, China Industry Information Network; chart by VCBeat.

Based on a compound annual growth rate (CAGR) of 3% from 2011 to 2018,In 2025, the number of diagnosed diabetes patients in China will reach 140.69 million. With an additional 182.90 million people in the prediabetes stage, the total diabetic population will amount to 323.59 million.。

Table 1. Number of Individuals with Diagnosed Diabetes and Prediabetes in 2018 and 2025

Image source: VCBeat

Market Size

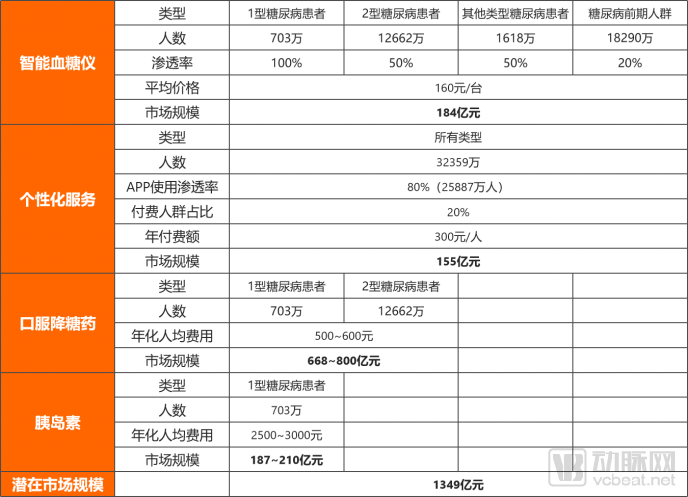

The diabetes market primarily comprises the smart glucose meter market, personalized services market, oral hypoglycemic agents market, and insulin market, with a total potential market size reaching RMB 134.9 billion.. With the application of digital technologies in diabetes management, digital diabetes management can cover the entire diabetes market, and the market size is promising.

Table 2: Estimation of China's Diabetes Market Size in 2025

Image source: VCBeat

From the perspective of the overall composition of the diabetes market, oral hypoglycemic agents and insulin represent two large sub-segments, accounting for 75% of the entire diabetes management market. Therefore, these two segments are currently the key areas where digital technologies should be deeply integrated.. Intelligent blood glucose monitoring technology is relatively mature, with a diverse range of related products; however, in the personalized services market, patients’ willingness to pay remains weak, and further market education will take time.

Oral hypoglycemic agents and insulin are both integral to diabetes treatment. By integrating digital technologies into various stages of diabetes management, products such as smart pillboxes and smart insulin pumps can play a significant role.

The 2017 "Report on Patients' Digital Life" released by Xueqiu showed that,32% of patients do not fully adhere to prescribed medication regimens, a rate that is even higher among diabetic patients, approaching 40%.. By integrating medical instructions, the smart pillbox can remind patients to take their medication on schedule. Furthermore, by scanning drug barcodes via a mobile mini-program, users can receive timely alerts regarding medication inventory levels, expiration dates, and refill needs. Once connected to a smartphone via GPRS, the smart pillbox automatically records medication intake times; the system will trigger an automatic alarm in cases of missed or duplicate doses. Additionally, the smart pillbox can synchronize patient data in real time, aggregating it on a platform (WeChat Official Account) for patients and their families to view at any time.

Figure 4 Product image of the intelligent pillbox for blood glucose management

Image source: Jianzhilu

For patients with type 1 diabetes, insulin is essential. During insulin therapy, patients on conventional regimens require 2–3 injections per day, whereas those on intensive insulin therapy need 3–4 daily injections. It is difficult for patients using traditional syringes to precisely control their daily insulin dosage, which increases the risk of hypoglycemia due to accidental overdose. Smart insulin pumps mimic the physiological function of a healthy pancreas by employing an AI-controlled insulin delivery system that administers insulin via continuous subcutaneous infusion.

Figure 5. Product image of the smart insulin pump

Image source: Medtronic

Smart insulin pumps simulate basal insulin secretion through adjustable, pulsatile subcutaneous infusion. When patients eat, preprandial insulin dosage and infusion patterns can be set based on the type and total amount of food, thereby controlling postprandial blood glucose levels.

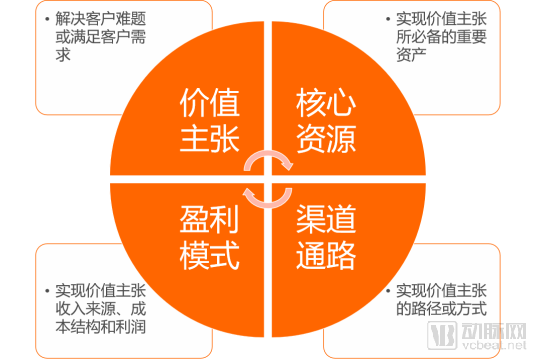

The Four-Element Model of Business Model

The company's business model is determined byAn interdependent system comprising Value Propositions, Key Resources, Channels, and Profit Model。

Figure 6. Four-Element Model of Business Model

Image source: VCBeat

(1) Value Propositions refer to the products or services a company provides to solve customer problems or meet customer needs. It is the starting point for creating a business model and defines the value a company offers to its customers.

(2) Key Resources refer to the essential assets required to deliver products or services to customers, including human resources, physical resources, intellectual property, equipment, and capital. They serve as the foundation of a business model.

(3) Channels refer to the paths and methods by which a company’s products or services reach customers; they constitute the delivery mechanism of the business model.

(4) Profit Model refers to how a company’s products or services generate customer payments, the costs incurred in doing so, and the profits earned by the company; it is the endpoint of the business model.

Therefore, any successful business model must have a strong value proposition that integrates relevant resources to deliver products or services to customers, establishes clear pathways to reach them, and ensures customers are willing to pay, thereby enabling the enterprise to achieve sustainable development.

Analysis of Major Models

Through interviews and research with companies specializing in the digital management of diabetes,The primary business models for the digital management of diabetes include: collaborating with pharmaceutical and medical device companies to serve individual consumers; partnering with pharmaceutical and medical device companies as well as internet healthcare enterprises to serve individual consumers; providing online-to-offline (O2O) services to individual consumers; and cooperating with hospitals or endocrinology departments to serve individual consumers.。

Collaborating with pharmaceutical companies to sell diabetes medications, and partnering with medical device manufacturers to distribute blood glucose meters, test strips, and related products. Digital diabetes management enterprises provide users with services including blood glucose monitoring, medication adherence tracking and reminders, diabetes-related health education, and data recording and analysis. The pharmaceutical and medical device companies are responsible for the sales and distribution of medications and blood glucose meters, sharing a predetermined percentage of the revenue with the digital diabetes management enterprises.

(1) Value Proposition

Help pharmaceutical and medical device companies increase sales of diabetes medications and devices.

(2) Core Resources

Brand, Diabetes Management APP, APP R&D and Operation Talent.

(3) Channels

Collaborate with pharmaceutical and medical device enterprises to provide digital diabetes management services to purchasers of drugs and devices, thereby enhancing consumer satisfaction and increasing repurchase rates.

(4) Profit Model

Revenue is primarily derived from revenue sharing with pharmaceutical and medical device companies, while app development and operations constitute the main costs.

This model can boost sales of pharmaceuticals and medical devices through the services offered by a digital diabetes management platform, converting purchasers of these products into users of diabetes management service providers, thereby reducing customer acquisition difficulty and costs. However, purely online diabetes management services struggle to foster strong user stickiness, which limits revenue potential.。

Tang Doctor partnered with Tasly to sell pharmaceuticals. The Tang Doctor app was integrated with Tasly’s pharmaceutical sales network, enabling Tang Doctor users to purchase medications through Tasly’s distribution channels. Meanwhile, Tasly’s existing user base gained access to the Tang Doctor app to receive related online diabetes management services, thereby driving user growth for Tang Doctor. Profits were shared between Tang Doctor and Tasly according to a predetermined ratio. However, low user stickiness constrained profit growth, ultimately preventing the establishment of a long-term partnership.

To promote the sales of pharmaceuticals and medical devices, companies offer a diabetes management service package for a specified period when patients purchase a certain quantity of medications or a blood glucose meter. Internet healthcare providers deliver services such as online consultations and online follow-up visits with prescription renewals, while digital diabetes management companies provide management services to users. The pharmaceutical and medical device companies pay fees to the digital diabetes management companies based on the duration of the service period.

(1) Value Proposition

Help pharmaceutical and medical device companies increase sales of diabetes medications and devices.

(2) Core Resources

Brand, Diabetes Management App, and Talent for App R&D and Operations.

(3) Channels

Collaborate with pharmaceutical and medical device companies to provide digital diabetes management services to purchasers of drugs and devices, thereby enhancing consumer satisfaction and increasing repurchase rates.

(4) Profit Model

Revenue is primarily derived from revenue sharing with pharmaceutical and medical device companies, while app development and operations constitute the main costs.

This model integrates pharmaceutical and medical device resources with healthcare services, providing users with integrated medication and management services for diabetes, thereby enhancing the user experience. Pharmaceutical and medical device companies increase product sales, while internet healthcare companies and digital diabetes management firms receive service fees from these pharmaceutical and medical device companies. However, initial operational costs are high, and a significant number of patients may churn once the free service period ends.。

For example, in 2017, Eli Lilly, DXY, and Tang Daifu (now deregistered) collaborated on the “Eli Lilly Diabetes Care Excellence Program.” Patients who purchased Eli Lilly’s diabetes medications were eligible to receive complimentary online medical services provided by DXY and blood glucose monitoring services provided by Tang Daifu. Eli Lilly leveraged these services to stimulate medication purchases, while DXY and Tang Daifu gained user traffic by serving Eli Lilly’s patients and received revenue shares from Eli Lilly’s drug sales as stipulated in their agreement. Under this collaboration model, Eli Lilly incurred substantial costs, yet the resulting increase in sales volume fell far short of projections. A significant number of patients discontinued use once the period of complimentary services ended.

Online, the app provides users with services such as blood glucose monitoring, medication monitoring and reminders, diabetes-related health education, and data recording and analysis. Offline, hospitals or clinics are established, and professional physicians and diabetes care managers are employed to provide diagnosis, treatment, and management services to patients.

(1) Value Proposition

Help people with diabetes control their blood sugar and provide timely treatment for abnormal blood glucose levels.

(2) Core Resources

Diabetes management apps, app R&D and operations professionals, physicians, diabetes care managers, and hospital or clinic operations professionals.

(3) Channels

Online diabetes management services are provided to users via a mobile app, while offline diagnosis and treatment services are delivered to patients through hospitals or clinics.

(4) Profit Model

Revenue is primarily derived from diagnosis and treatment fees for diabetic patients, as well as charges for personalized services. Costs mainly include app development and operational expenses, medical staff compensation, and the construction and operating costs of hospitals or clinics.

This model enables the provision of offline services, enhancing patient experience and user stickiness, while physical institutions also serve as customer acquisition channels. However, the construction and maintenance costs of physical institutions are high, resulting in an asset-heavy operational model, and the scope of offline services is limited.。

Diabetes digital management companies provide SaaS services to hospitals or endocrinology departments, including the development of standardized systems for diabetes diagnosis and treatment processes, tiered diagnosis and treatment platforms for diabetes, and diabetes management platforms, while also assisting them in delivering diabetes patient management services. Hospitals pay these digital management companies platform construction and maintenance fees, as well as diabetes management service fees based on per-patient visits or annual contracts.

(1) Value Proposition

Provide SaaS services to hospitals or endocrinology departments, assist physicians in managing patients with diabetes, alleviate physician workload, and improve management efficiency.

(2) Core Resources

Qualifications, government relations, tiered diagnosis and treatment and diabetes management platforms, as well as talent for platform R&D and operations.

(3) Channels

Establish partnerships with hospitals or endocrinology departments by providing them with SaaS services, and assist physicians in managing patients with diabetes.

(4) Profit Model

Revenue is derived from platform construction and maintenance fees paid by hospitals, as well as diabetes management service fees charged on a per-visit or annual basis. Costs primarily consist of investments in platform research and development and operations.

The advantage of this model lies in its ability to alleviate the burden of diabetes patient management for hospitals or endocrinology departments through the use of the system. Digital diabetes management companies acquire user resources by providing SaaS solutions and diabetes management services to hospitals or endocrinology departments, thereby gaining leverage for collaborations with pharmaceutical and medical device manufacturers as well as insurance companies. However, gaining recognition from primary healthcare institutions requires strong qualifications and government relations, and the initial investment in system costs is substantial.。

Different business models are at different stages of digital innovation in diabetes management. In light of the historical background of internet healthcare development, digital innovation in diabetes management can be divided into three stages:

In 2014, the mobile internet was in its ascendant phase and began to explore applications within the healthcare industry. Mobile health apps emerged in large numbers, with applications launched across various medical subsectors. Companies specializing in digital diabetes management invested heavily in marketing to acquire traffic and scale up their operations. They also incentivized physicians to refer patients to their apps through subsidies. Between 2014 and 2016, the number of diabetes management apps peaked at over 500. These companies provided patients with services such as blood glucose monitoring, medication tracking and reminders, diabetes-related health education, and data recording and analysis.However, as the battle for traffic intensifies, customer acquisition becomes increasingly difficult and costly. Moreover, most registered users are unwilling to pay for services such as blood glucose monitoring, medication monitoring or reminders, and health education, making commercial monetization challenging. Meanwhile, these services fail to generate strong user stickiness or deliver a stable stream of users to pharmaceutical and medical device companies, hindering the establishment of long-term partnerships between the two parties.。

To enhance the patient service experience, digital diabetes management companies are optimizing their online diabetes management services and establishing internet hospitals to provide diabetic patients with online follow-up consultations, prescription renewals, and other services. Simultaneously, they are expanding their offline presence by opening hospitals and clinics to deliver in-person diabetes treatment services, thereby strengthening patient loyalty and increasing patients’ willingness to pay.However, internet hospital services struggle to compete with digital healthcare enterprises such as WeDoctor, Haodf, and Chunyu Yisheng. Meanwhile, establishing offline physical medical institutions requires substantial capital investment and offers limited geographic coverage, resulting in a constrained patient volume and hindering scalable expansion.。

The first two stages have always been driven by consumer-side (C-end) demand. In the 3.0 stage, companies specializing in digital diabetes management began to address business-side (B-end) needs by providing Software-as-a-Service (SaaS) solutions to hospitals or endocrinology departments. These solutions include standardized systems for diabetes diagnosis and treatment workflows, tiered diagnosis and treatment platforms for diabetes, and comprehensive diabetes management platforms, with the aim of retaining patients on the platform and building a large-scale, highly engaged patient user base.However, strong technical service capabilities are required to gain recognition from hospitals or endocrinology departments and establish long-term collaborative relationships with them.Currently, digital diabetes management companies such as Zhiyun Health, Kongtang Weishi, Tang Hushi, and Ruikongtang are already actively conducting related business.

From the hospital’s perspective, to comply with health insurance cost-containment requirements, hospitals must reduce expenditures on diabetes medications and complication treatments. Digital diabetes management companies can assist hospitals in managing diabetic patients, thereby lowering the incidence of complications. Furthermore, as diabetes management services are currently not included in the list of billable medical services provided by hospitals, physicians have limited incentives to engage in out-of-hospital diabetes management, creating an opportunity for these enterprises to fill the gap.

From the perspective of the Department of Endocrinology, inpatient glycemic management is critical; notably, patients with abnormal blood glucose levels cannot undergo surgery safely and smoothly. By leveraging a digital diabetes management system, real-time blood glucose data of surgical patients across all departments can be synchronized with the Department of Endocrinology, enabling timely intervention for those with abnormal readings. This underscores the status and importance of the Department of Endocrinology within the hospital. Meanwhile, the implementation of a standardized diabetes diagnosis and treatment system can enhance diagnostic efficiency, extend services to more diabetic patients, and increase departmental revenue.

Figure 7. Evolutionary Path of Digital Innovation in Diabetes Management

Image source: VCBeat

In the 3.0 phase of digital innovation in diabetes management, enterprises face higher demands on their innovation and management capabilities. How to empower hospitals or endocrinology departments, acquire a stable and scalable user base, and integrate other B-side resources—such as pharmaceutical and medical device companies, internet healthcare providers, and pharmaceutical e-commerce platforms—to deliver high-quality, integrated services to C-end users has become a critical challenge for digital diabetes management companies to solve.。

Business Model Innovation

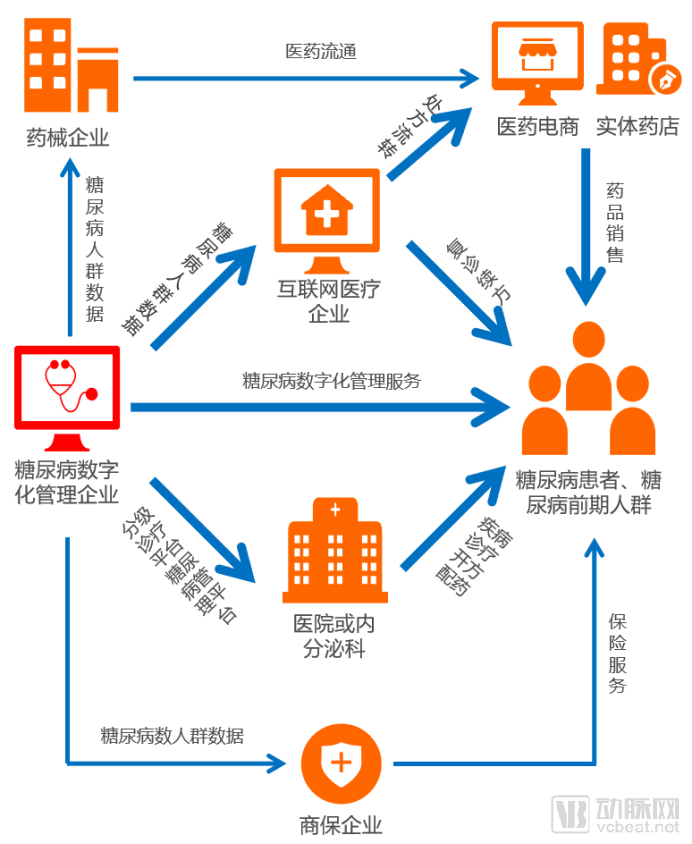

In the future, companies specializing in digital diabetes management must adopt an entire-industry-chain perspective, integrating healthcare service providers such as medical institutions, pharmaceutical and medical device manufacturers, internet healthcare companies, pharmaceutical e-commerce platforms, pharmacies, and commercial insurance enterprises. Centered on the needs of individuals with diabetes, they should provide integrated, full-course-of-care services.

(1) Value Proposition

Help people with diabetes manage their blood glucose levels and provide diabetes-related diagnostic and therapeutic services.

Help B-side partners increase the sales volume of their products or services.

(2) Core Resources

Tiered diagnosis and treatment and diabetes management platform, R&D and operational talent for the platform, industry chain resources, and digital technologies.

(3) Distribution Channels

By partnering with primary healthcare institutions to acquire user groups and provide diabetes management services, we enhance user stickiness through these services. We then leverage the accumulated user base to collaborate with pharmaceutical and medical device companies, internet healthcare providers, and commercial insurance firms, offering diabetic patients services such as medications, blood glucose meters, follow-up consultations, prescription renewals, and insurance coverage. This integrates “medical care + pharmaceuticals + insurance” services, further improving user experience and engagement while boosting sales for B-side partners. On top of meeting users’ basic diabetes management needs, we integrate products or services from B-side institutions based on big data analytics and AI-assisted decision-making to deliver personalized custom services—including precision nutrition, exercise, and sleep management—thereby truly building a comprehensive service ecosystem that expands from basic to personalized offerings.

(4) Profit Model

Revenue is primarily derived from tiered income from B-side partners and service fees charged to C-side users, while costs mainly consist of investments in platform research and development and operations.

Figure 8. Integrated Digital Management Platform for the Full Course of Diabetes

Image source: VCBeat

(1) Connect to hospitals or endocrinology departments via SaaS to build a user base

Leveraging its strengths in the digital management of diabetes, the company establishes standardized systems for diabetes diagnosis and treatment, tiered diagnosis and treatment platforms, and comprehensive diabetes management platforms for hospitals and endocrinology departments. These initiatives provide telemedicine and online diabetes management services to the general public and patients with diabetes. Endocrinology departments utilize the diabetes platform for post-diagnosis patient management, while simultaneously employing the tiered diagnosis and treatment platform to deliver basic medical services to residents, thereby alleviating the administrative burden on primary healthcare institutions. By collaborating with primary healthcare institutions, the company converts their managed patients into users, providing them with diabetes management services and laying a substantial user foundation for future service monetization.

(2) Integrate pharmaceutical and medical device enterprises, primary healthcare institutions, and internet-based healthcare companies to enhance service capabilities.

User needs vary across different stages. In the early stage, users lack understanding of diabetes and require systematic knowledge about the condition as well as risk alerts. Companies should provide scientific education to guide users on how to perceive diabetes and how to control blood glucose through diet and exercise. Meanwhile, by leveraging AI-enabled monitoring devices, companies can provide real-time feedback on users’ blood glucose levels and promptly notify them once the diagnostic criteria for diabetes are met. During this phase, digital diabetes management enterprises must fully utilize their resources to meet user needs.In the medication phase, patients’ primary needs concern which medications to use and how to access them in a more affordable and convenient manner. At this stage, companies need to collaborate with pharmaceutical and medical device manufacturers specializing in diabetes to continuously provide patients with cost-effective and appropriate medications and blood glucose monitoring equipment. This helps patients manage their blood glucose through medication adherence. Additionally, by partnering with internet healthcare providers, companies can offer online follow-up consultations and prescription renewal services, while enabling medication purchases through pharmaceutical e-commerce platforms and pharmacies.

Diabetes is a condition associated with a high risk of complications, encompassing over 100 types, including diabetic nephropathy, diabetic eye disease, diabetic neuropathy, diabetic foot, and diabetic cardiovascular and cerebrovascular diseases. Patients at this stage require timely treatment. Healthcare enterprises need to integrate resources from primary care institutions to provide professional medical services, thereby reducing the life-threatening risks posed by these complications. Meanwhile, by collaborating with commercial insurance companies, tailored insurance products should be developed based on patients’ needs at different disease stages. Through joint efforts to strengthen the management of key patient populations according to individual conditions, the amount of insurance claims can be reduced.

(3) Leverage digital technologies to provide personalized customization services

By providing long-term monitoring of patients’ blood glucose, diet, exercise, medication, and treatment, a substantial volume of user data has been accumulated. Leveraging digital technologies such as the Internet of Things (IoT), artificial intelligence (AI), and big data, companies generate personalized health profiles for each user. Furthermore, individualized nutrition, exercise, and sleep plans are formulated based on users’ health status to help them adopt healthier lifestyles and reduce the risk of progression from prediabetes to diabetes.

Based on the foregoing discussion,We recognize that the design of a digital diabetes management business model must be patient-centric, integrating medical resources across the diabetes industry chain to provide closed-loop services encompassing healthcare, pharmaceuticals, insurance, and health management. An integrated digital platform for whole-course diabetes management can deliver comprehensive, one-stop diabetes care centered on patients, effectively addressing their pain points and delivering tangible value.。

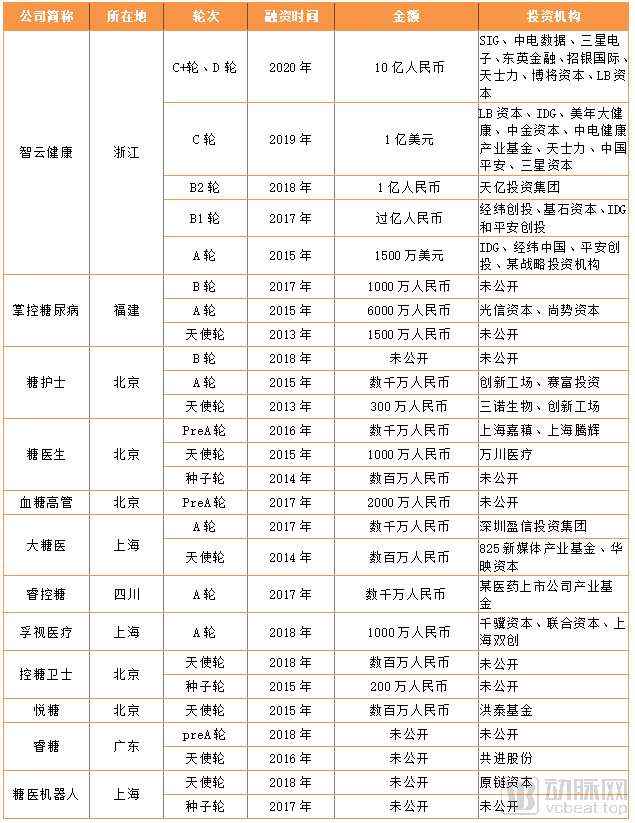

VCBeat has compiled basic information on investment and financing events in the digital diabetes management industry from 2013 to 2020 (as of April 2020).

Table 3. Investment and Financing in the Digital Diabetes Management Industry

Data Source: VCBeat Orange Database

Statistical results show that between 2013 and 2020, a total of 12 companies completed 27 financing rounds, raising a cumulative total of RMB 2.2 billion.

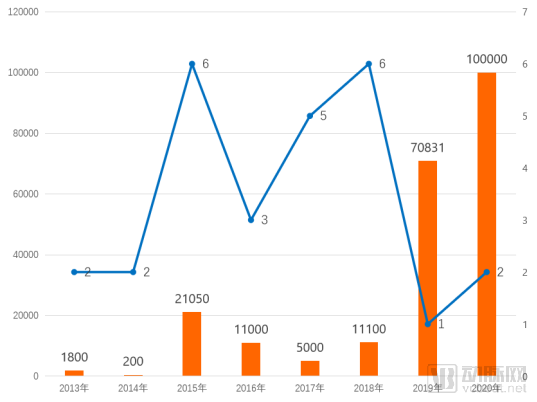

Figure 9. Investment and Financing in the Digital Diabetes Management Industry, 2013–2020 (in ten thousand yuan)

Note: Financing amounts in the millions/tens of millions are calculated as RMB 1 million/10 million. The exchange rate is USD 1 = RMB 7.0831. Data source: VCBeat Orange Database.

We observe that,Financing in the digital diabetes management industry peaked twice, in 2015 and 2018. The 2015 surge was driven by the rise of internet healthcare, which spawned a wave of digital diabetes management companies and attracted capital investment into this emerging sector. In the aftermath, a period of intense competition known as the “Hundred Sugar Wars” led to the collapse of many such enterprises. The survivors demonstrated stronger innovation capabilities, and their business models were gradually validated, thereby bolstering investor confidence and triggering another financing peak in 2018.。

In terms of financing amount, the high figures in 2019 and 2020 were driven by a single company, Zhiyun Health, which secured substantial funding (USD 100 million in Series C in 2019, and a combined RMB 1 billion in Series C+ and Series D in 2020). Excluding this exceptional case, the peak in financing occurred in 2015, consistent with the broader investment boom in the internet healthcare sector.

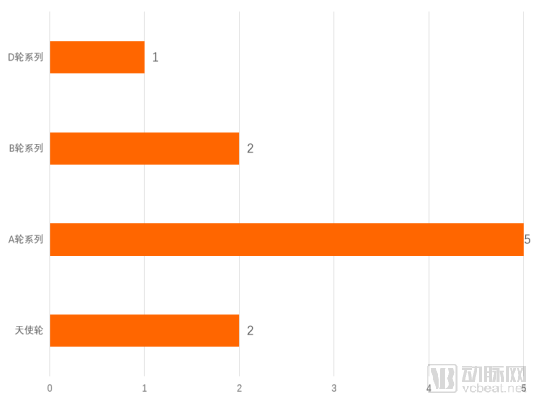

Figure 10 Distribution of the Latest Financing Rounds in the Digital Diabetes Management Industry

Data Source: VCBeat Orange Database

Based on the distribution of the latest financing rounds among enterprises, Series A financings are the most numerous, with a total of seven financing events occurring prior to Series A. Series A financing serves as a watershed moment in the industry’s development stage. The fact that the majority of companies within the sector are at Series A or earlier stages indicates that the industry’s business model is still in an exploratory phase, with product or service systems undergoing continuous refinement and awaiting market validation.It is evident that digital diabetes management remains in its early stages; enterprises capable of establishing new business models and achieving strong sales of their products or services will be prioritized by investors.。

Zhiyun Health has completed its Series D financing round, emerging as a leader in the digital diabetes management industry. The company has established a core system that acquires customers within hospitals and guides consumer (C-end) users toward out-of-hospital conversion. By linking the hospital (H-end) and doctor (D-end) segments to secure physician resources, and connecting the consumer (C-end) and doctor (D-end) segments to enhance interactions between patients and physicians—thereby boosting overall engagement—the company ultimately achieves a closed-loop business model integrating “medical care” and “pharmaceuticals” through its pharmaceutical e-commerce platform.

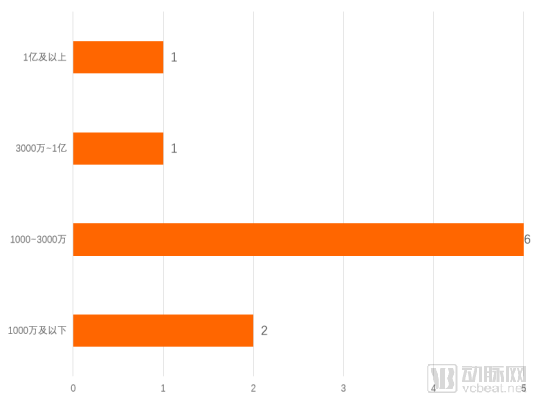

Figure 11 Distribution of Cumulative Financing Amount in the Digital Diabetes Management Industry (RMB)

Data Source: Arterial Orange Database

In terms of cumulative financing amounts for companies that have secured funding, eight companies each raised less than RMB 30 million., which once again demonstrates that the digital management of diabetes is still in its early stages of development, with capital maintaining a cautious investment stance. Enterprises should seize this opportunity to innovate their business models, provide more valuable products or services to users, and secure greater investment.。

Capital attention will shift from “enterprises that leverage their own resources to serve B-side clients” to “enterprises that leverage B-side resources to serve C-end users.”: From the perspective of the current mainstream business models of digital diabetes management companies, they primarily rely on self-developed digital diabetes management platforms to assist pharmaceutical companies, medical device manufacturers, online pharmacies, and brick-and-mortar drugstores in providing diabetic patient education, blood glucose monitoring, dietary management, exercise management, and medication management. This enables these entities to offer additional online diabetes management services alongside the sale of drugs and devices, thereby improving repurchase rates, boosting sales for pharmaceutical and device companies, and generating corresponding revenue shares.Fundamentally, digital diabetes management companies serve a B2B role and exhibit strong dependence on other institutions.。

Personalized health management is a key direction for the future development of medical services. As digital diabetes management companies accumulate an increasingly large user base, patient needs are evolving beyond basic services such as health education and blood glucose monitoring. In particular, individuals with prediabetes have a strong demand for comprehensive health management, driving the need for personalized services including precision nutrition, personal fitness coaching, health screenings, and specialist consultations.. To deliver personalized user services, digital diabetes management companies need to integrate B-side resources such as dietary nutrition institutions, exercise management organizations, testing and inspection agencies, and hospitals or clinics to meet user needs. As previously mentioned, individuals with prediabetes constitute the primary market for diabetes management; providing services to this population will create greater profit margins for enterprises and gain recognition from capital investors.

The above covers the first four chapters of the report. The complete framework is as follows. Scan the QR code to access the mini-program and read the full report for free:

Report Contents:

I. Industry Definition: Digital Management Covers Patients with Diabetes and Individuals with Prediabetes

II. Market Potential: The potential market size is expected to reach RMB 135 billion in 2025

III. Business Model: Transition from Consumer-Facing APP Services to B-End SaaS Services

IV. Capital Enthusiasm: The Industry Is Still in Its Growth Stage, with B2B Service Enterprises Securing Significant Financing

V. Policies and Guidelines: Integrated Information Platforms Will Be the Future Direction for the Digital Management of Diabetes

VI. Typical Case: Addressing Pain Points in Diabetes Management and Enhancing Service Capabilities Through Model Innovation

References:

1. “Special Report on the Diabetes Industry Chain: Sweet Chain Ties, Perfect Ecosystem,” Changjiang Securities

2. “Diabetes + Internet” Through the Lens of User Research: An In-Depth Industry Report on Diabetes within the Internet-Based Chronic Disease Management Sector, 36Kr Research Institute

3. “Research on the Application of Artificial Intelligence in Diabetes Diagnosis,” Xue Xiang

4. “Years of Diabetes Management: Why Are Patients Still Reluctant to Pay?” Ba Dian Jian Wen

Special thanks to Guo Gaoxing, Founder and CEO of Zhangkong Diabetes; Li Chengzhi, Founder and CEO of Tang Hushi (Sugar Nurse); Wu Jingyu, CEO of Datangyi; Liu Hongdou, Founder and CEO of Ruikongtang; and the Founder of Kongtang Weishi.He Daoxin,Director of Operations, Zhizhong MedicalZhang Xunjie’s strong support for this study.