Decoding the Health Management Landscape: Over 100 Investments in 3 Years, SoftBank and IDG Lead the Charge as Three Key Segments Attract Billions

According to data from the National Bureau of Statistics, China’s total annual number of clinical visits reached 8.42 billion in 2018, setting a new record. This figure serves as a wake-up call, highlighting the urgent need to shift disease prevention efforts upstream and accelerate the development of personal health management and related industries.

Since the emergence and dissemination of medical concepts related to health management at the beginning of this century, health management in China has been in a state of exploration and development. In 2014, the inaugural year of internet healthcare ushered in by mobile internet technology, health management also witnessed an upward trajectory, with various innovative models emerging in rapid succession.

Since the introduction of policies such as the “Healthy China 2030” Planning Outline, the Healthy China Action, and the 13th Five-Year Plan for Health Promotion and Work, the status of health management within the healthcare sector has been significantly elevated. The paradigm shift from treating diseases to preventing them has gradually taken root, propelling the health management industry into a phase of rapid development and quickly narrowing market gaps. Driven by three major trends—population aging, changes in disease patterns, and technological advancements—health management is emerging as a vast blue ocean for innovation and entrepreneurship.

(Note: Calculation of amounts—undisclosed financing amounts are counted as 0; disclosures of “tens of millions of yuan” are counted as RMB 10 million; USD amounts are converted to RMB at the current exchange rate.)

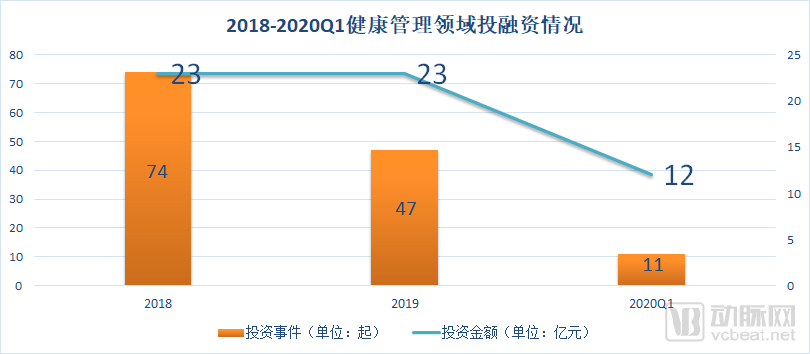

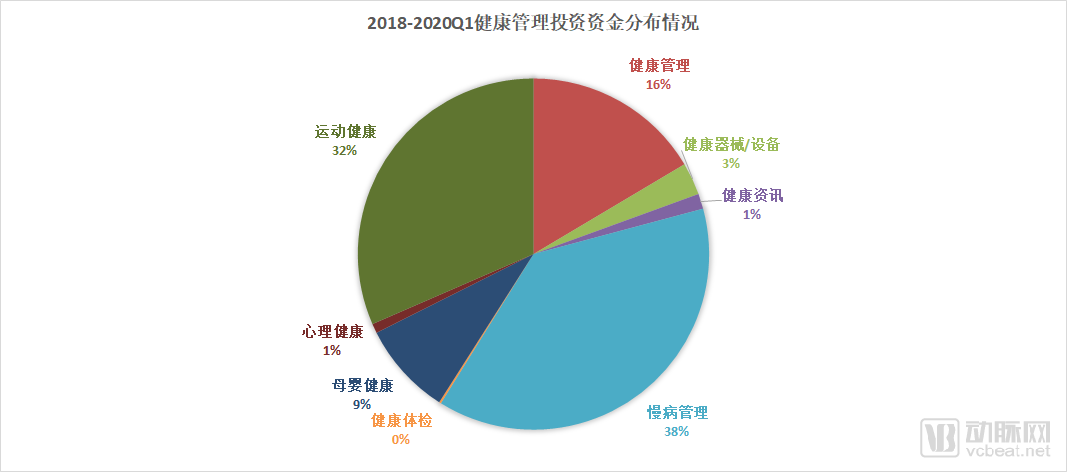

From 2018 to the first quarter of 2020, a total of 132 primary market financing and investment events occurred in the health management sector, with capital inflows amounting to approximately RMB 5.9 billion. The three sub-sectors most favored by investors were chronic disease management, fitness and wellness, and health management. (Note: In a broad sense, health management refers to non-medical approaches aimed at helping individuals achieve optimal physical and mental well-being. In a narrow sense, it involves the direct provision of managed health services through various means to promote and maintain users’ health, with corporate business models primarily built around delivering such managed health services directly to consumers.)

VCBeat, through analysis of relevant data and interviews with industry experts, aims to outline the true market landscape and future development trends of health management.

Health management employs non-medical approaches to help individuals achieve optimal physical and mental well-being. According to data released by Kaiser Permanente in the United States, medical care accounts for only 10%–20% of the factors influencing health, while living environment, lifestyle, and other determinants constitute 80%–90%.

In China, the tendency to prioritize treatment over prevention has long been the most pervasive issue within the healthcare ecosystem. The health management industry has remained in a prolonged exploratory phase, “crossing the river by feeling the stones,” without identifying an effective path for development. Within the public hospital-dominated healthcare service system, health management was initially almost exclusively confined to the physical examination departments of public hospitals.

The turning point came in 2014. As healthcare system reforms deepened, market barriers were gradually dismantled, and industrial upgrading advanced in depth. Driven directly by new technologies, new concepts, and new policies, health management entered a fast track of development. According to data from an Analysys report,The market size of the health management industry was 221.6 billion yuan in that year, and it is projected to double to 501 billion yuan over the next five years.

In October 2016, the Central Committee of the Communist Party of China and the State Council issued the “Outline of the ‘Healthy China 2030’ Plan,” which explicitly proposed integrating health into all policies and aiming for China’s major health indicators to reach the level of high-income countries by 2030. In the following years, health management was frequently highlighted as macro-level policies such as the “Medium- and Long-Term Plan for the Prevention and Control of Chronic Diseases in China (2017–2025)” issued by the State Council, and meso- and micro-level policy adjustments such as the revised “Measures for the Administration of Health Insurance” by the China Banking and Insurance Regulatory Commission (CBIRC), were implemented. These policies emphasized and affirmed the development of the health management industry, outlining specific pathways, including the provision that “up to 20% of health insurance premiums may be allocated to health management services.”

According to the "China Family Health Big Data Report," less than one-quarter of the population has a solid grasp of basic health knowledge and concepts, and fewer than one-fifth maintain healthy lifestyles or possess essential health skills. However, 93% agree that "health management should cover every member of the family," and 81.8% express a preference for "health intervention services aimed at improving their own unhealthy lifestyles and habits." These figures indicate that health awareness among Chinese residents is gradually rising, with increasing emphasis placed on the concept of health management. At the same time, they also highlight thatThe health literacy level of Chinese residents remains low, representing a market in urgent need of solutions.

Technologically, with the advancement of IoT, artificial intelligence, and big data, alongside the widespread adoption of wearable devices and home monitoring equipment, solutions have emerged to improve lifestyles by leveraging smart networked devices to monitor user health data and intervene in and guide user health. From the perspective of venture capitalists (VCs), the maturity of technology and products often solidifies the logic of being “standardizable, replicable, scalable, and quantifiable,” revealing a “long and wide” market track.

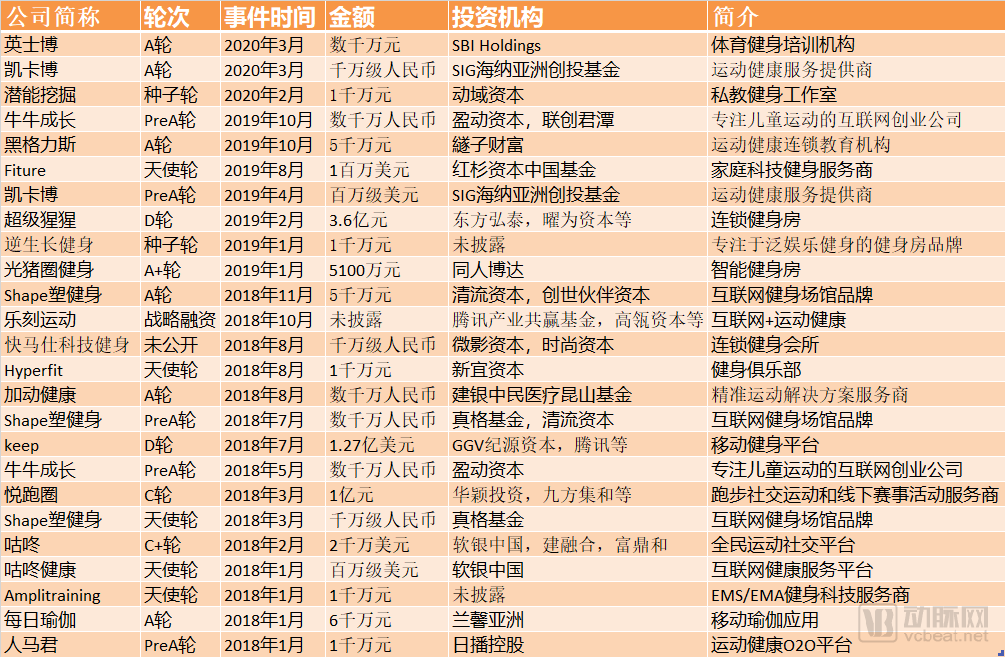

Consequently, a host of investors armed with business cards and capital began scouting for deals in the market. Hillhouse Capital invested in LeKeep Fitness; Sequoia Capital backed Fiture (which specializes in home-based tech-enabled fitness services); Northern Light Venture Capital invested in YiXinLi (One Psychology); SoftBank invested in Mommy Knows; Pacific Insurance and others invested in Miao Health……

As the key drivers—capital, demand, policy, and technology—come into view, the narrative of health management begins to unfold. The stage is set, the audience is seated, the curtain rises, and the actors make their entrance one by one.

Note: This article is based on investment and financing data in the health management industry from 2018 to the first quarter of 2020, as monitored by the VCBeat Orange Database. It adopts the perspective of grounded theory, whereby researchers autonomously construct analytical paradigms from the data, rather than employing a priori classification methods.

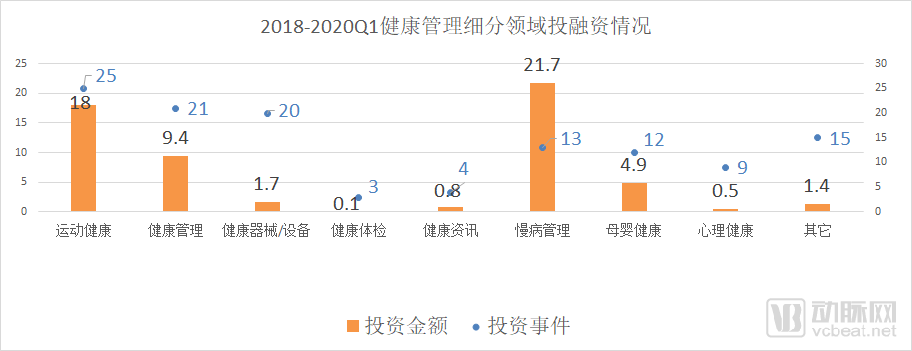

As shown in the figure above, chronic disease management, exercise and health, and health management platforms are the three sub-sectors attracting the most capital attention, with investment amounts of RMB 2.17 billion, RMB 1.8 billion, and RMB 940 million, respectively. The combined financing volume of these three sectors accounts for more than 80% of the broad-concept health management industry.

The substantial capital inflows into these three subsectors are driven by the maturation of innovative enterprises’ businesses and products, which has led to later-stage investment rounds and frequent large-scale financing. For instance, in April 2019, the health management platform Miao Jiankang announced a C-round financing of RMB 500 million. Within the past three years, Zhiyun Health (formerly Zhangshang Tangyi), a player in chronic disease management, secured four rounds of financing, with its latest D-round raising RMB 1 billion, bringing its cumulative total to over RMB 1.8 billion. In the fitness and health sector, Keep announced in July 2018 that it had raised USD 127 million in D-round financing from investors including GGV Capital and Tencent.

Chronic Disease Management

In 2015, diabetes management apps emerged in the market, attracting significant capital investment and sparking what the industry dubbed the “Hundred Sugar Wars.” Today, however, only five companies specializing in diabetes management have secured funding over the past three years, with Zhiyun Health, formerly known as Palm Sugar Doctor, emerging as the leading enterprise.

Kuang Ming is the founder of Zhiyun Health. Prior to establishing Zhiyun Health, Kuang Ming worked at renowned companies such as Intel and Johnson & Johnson Medical. In 2014, Kuang Ming conceived a vision: “to build an enduring century-old enterprise in the broader health sector, starting with services and big data management in the field of diabetes.”

Thus, Kuang Ming, who had been earning an annual salary of one million yuan and enjoying a respectable lifestyle, changed his life trajectory by resigning to join the ranks of entrepreneurs and founding “Zhangshang Tangyi” (Pocket Diabetes Doctor). At the end of 2014, Kuang Ming and his team launched a diabetes health management service platform that leverages intelligent algorithms to enable patients with diabetes to accurately record blood glucose levels, assess complications, and access knowledge on blood sugar control anytime and anywhere.

In addition to diabetes management, other notable players have emerged in the chronic disease management sector, such as Xiaolu Medical Clinic and Akang Health. Xiaolu Medical Clinic is a traditional Chinese medicine (TCM) telemedicine platform that operates a TCM wellness app targeted at individuals with chronic conditions and urban populations experiencing suboptimal health. Akang Health manages businesses including prescription medications for chronic diseases.

Sports and Health

Over the past three years, there have been 25 financing and investment events in the sports and health sector, with the total investment amount reaching RMB 1.8 billion. In terms of investment institutions, it is evident that top-tier capital firms such as Sequoia Capital, Hillhouse Capital, and Tencent have already invested in this field.

However, judging from the current core businesses of enterprises in this sector, the landscape is characterized by “exercise without health,” meaning that major players primarily focus on users’ fitness and exercise activities, while rarely engaging in direct monitoring and intervention of their health behaviors. In the future, if companies in this field can expand from fitness and exercise into the more direct realm of exercise-based health management, they will break through their current growth ceilings and bottlenecks.

The company with the largest financing scale in this field is Keep, founded by Wang Ning, a post-90s entrepreneur. The inception of Keep stemmed from Wang’s breakup upon graduating from university, which led him to take up running and subsequently inspired him to develop a mobile fitness application. In the summer of 2014, the first prototype of Keep was created in a café near the Yonghe Temple in Beijing. Since then, backed by investments from Tencent, GGV Capital, and other investors, Keep has gradually evolved from a single-purpose tool into a comprehensive sports application integrating fitness, social networking, diet management, running, cycling, and e-commerce.

Health Checkup

Over the past three years, only three financing deals occurred in the primary market, with Xiaoniao Health, Zhikang Technology, and Aoya Medical securing early-stage investments.

But in the secondary market, the narrative surrounding this sector is compelling enough.

In 2006, Yu Rong, who was previously primarily the Chairman of Shanghai Tianyi Investment Group, crossed over into the health checkup sector and established Meinian Onehealth. Subsequently, through a series of capital operations, including a back-door listing and mergers and acquisitions, Meinian Onehealth became the enterprise ranking first in core operational data within the health checkup market. Even Ciming Health Checkup, which had once held the industry’s top position, was acquired by Meinian Onehealth.

On the evening of October 27, 2019, an announcement by Meinian Onehealth Healthcare signaled the entry of another industry giant. According to the disclosure, Alibaba Network and its acting-in-concert party, Hangzhou Xintou, collectively acquired a 10.82% stake in Meinian Health, becoming the company’s second-largest shareholder. Meanwhile, Shanghai Qijun acquired a 5.34% stake in Meinian Health; the entity is managed by Yunfeng Capital and maintains close ties with Jack Ma. Alibaba’s total investment amounted to RMB 7.265 billion. Previously, Alibaba’s Taobao, together with other investors including Suning.com (in which Alibaba holds a stake), privatized all shares of iKang Guobin, another major player in the health checkup industry, in a transaction valued at USD 1.5 billion.

The combined investment of approximately RMB 18 billion across two rounds firmly established Alibaba’s absolute dominance in the health checkup sector.

In an interview, Yu Rong stated that Meinian Onehealth, as China’s largest entry point for health services and big data platform, possesses nearly limitless potential for industrial expansion and influence. Essentially functioning more like a big data company, it produces, develops, utilizes, and enhances data to create new value for customers’ life and health. “Professional screening – high-risk stratification – individualized prevention – precision treatment forms the foundational logic of our business development,” said Yu Rong.

Health Management

Here, this paper adopts a narrow definition of health management, referring to the direct provision of health management services that employ various measures to promote user health, with its business model built upon managed health services for users.

Over the past three years, a total of 21 investment and financing events occurred in this field, with capital inflows amounting to approximately RMB 940 million.

Health management embodies integrated medical technologies; its development is driven not by a single industry, but by the synergistic efforts of multiple sectors. Currently, leveraging technologies such as the Internet of Things (IoT) and big data, health has ceased to be the exclusive domain of healthcare enterprises. With diverse approaches being explored for the advancement of health management, a coordinated multi-industry development pattern is gradually taking shape in the market.

As a series of health management applications and service providers have emerged, the practical application of industrial synergy is continuously deepening. Major corporations such as Apple, Alibaba, and Google have also entered the health management sector to varying degrees. Leveraging their competitive advantages across multiple industries, they are gradually implementing comprehensive technological solutions for health management services, thereby highlighting the unique strengths of their respective products.

In the domestic market, an analysis of the core businesses of the companies shown in the chart above reveals that health management enterprises employ diverse operational models. These include UHoojia, which leverages big data to drive patient management and help users achieve smart in-hospital nursing and mobile out-of-hospital care; Miaojiankang and Dongya Health, which operate as comprehensive health management platforms; and Binghan Technology, which focuses on the sleep sector.

Currently, the company with the largest financing scale in the health management sector is Miao Health, whose CEO is Kong Fei.

In 2012, Kong Fei, then president of a well-known gaming company, came across a medical-grade mobile health terminal device developed by an Israeli company. Over the next year or two, Kong conducted trend analyses through overseas visits, hospital surveys, and experience summaries, leading him to conclude that health management represented a significant trend and a major opportunity. Consequently, Kong embarked on his entrepreneurial journey and founded Miao Health in 2014.

Miao Health has currently developed seven major business groups, including the Miao Health APP, Miao Bao, Miao Yi, Miao Yao, and the Canada Health Management Center (China). By leveraging high-frequency health management as an entry point, it has established a closed-loop model integrating “healthcare with medical services, pharmaceuticals, and insurance.” The platform has accumulated over 80 million users and secured nearly RMB 1 billion in financing.

Summary

Among the subsectors of broad-spectrum health management, the four areas introduced above are relatively mature. In the realm of health devices and equipment, the focus is primarily on leveraging Internet of Things (IoT) technology to develop wearable devices, such as those from Fanmi Technology and Wanyu. Wearable devices have now become mass-market products, occupying an indispensable position in the health management industry chain.

In the field of health information, there have been four financing and investment events in the past three years, with Baike Mingyi Wang, Bama Ying, and Momself receiving investments; currently, the market size in this sector is relatively small. In the maternal and child health sector, there have been 16 financing and investment events, with significant funding amounts going to Cui Yutao’s Parenting Academy, Mami Zhidao, and Yihe Health.

In other areas, business models are diverse; for example, YiBai Technology focuses on medical live streaming, while ZhiYu Information specializes in the digitalization of elderly care services. The business models of companies in these sectors are largely still in the exploratory phase.

The industry’s relatively rapid growth in recent years has led to a broad consensus: without health management, China will face immense pressure on its healthcare and elderly care systems in the future.

This means that the industry’s development prospects are exceptionally clear, and health management will play an increasingly vital role in the future evolution of the entire healthcare industry.

However, at present, the entire industry still faces many pain points. Gu Shufeng, COO of Miao Health, shared his insights on the industry’s pain points, bottlenecks, and opportunities in an interview with VCBeat:

The demand for health management has always been present; however, the health management industry has historically lacked effective and targeted interventions. A paradox exists between individualized, personalized health management and the law of large numbers underpinning big data analytics. For instance, while the law of large numbers indicates that long-term high-sugar diets lead to diabetes, this statistical generalization may fail when applied to individuals due to significant variations in constitutional makeup and living environments. Rather than relying on single-dimensional statistical laws, multi-dimensional comprehensive data analysis is required. By integrating individual-level big data—such as family disease history, comprehensive dietary structure, exercise patterns, and psychological stress—it becomes possible to conduct precise disease risk assessments for individual users. Furthermore, dynamic and continuous tracking and analysis are necessary to account for future changes in users’ lifestyles. Therefore, current one-on-one precision health management solutions must involve ongoing tracking, analysis, and feedback to deliver customized, personalized health promotion outcomes, while also requiring validation through evidence-based medical results.

Secondly, although China’s health management industry is experiencing rapid growth, it remains in its early stages of development. The sector has historically lacked unified standards, with many companies still exploring and refining their business models. Consequently, no fully mature brands or dominant market leaders have yet emerged. As a participant in this industry, Miao Health is continuously striving to promote the development of the health management sector and establish itself as a leading service brand.

“Finally, there is the issue of industry payers. Currently, the potential market size is enormous, and the actual market size is also growing. ‘The willingness of insurance institutions at all levels to pay continues to strengthen. Meanwhile, with the vigorous development of Healthy Cities by governments at all levels, an increasing number of enterprises are providing employees with health benefits beyond physical examinations and supplementary medical coverage, including health management services, commercial insurance, and pharmaceuticals. This aligns with Miao Health’s ongoing iteration of health management service-oriented products designed to meet user needs across markets such as the insurance industry, Healthy Cities, and corporate clients,’ said Gu Shufeng.”

Pain Points and Opportunities Coexist. Driven by key factors such as technology, policy, and capital, health management is currently at a moment rich with opportunities. The future development of the industry may follow the path outlined below:

I. Verticalization and Specialization. In the vast health management industry, it is difficult for any single enterprise to achieve a monopoly across every niche segment. Therefore, verticalization and segmentation are inevitable trends in the industry’s future evolution. For innovative enterprises, it is essential to identify their areas of competitive advantage and build substantial professional barriers. By strengthening and expanding their presence within these specific domains, they can position themselves to thrive under the spotlight of future healthcare advancements.

II. Refining Solutions to Precisely Meet User NeedsCurrently, it is difficult to identify any product within any niche segment of the health management industry that has achieved a perfect 100% satisfaction rating from a large-scale user base. Many products on the market only partially address specific user needs to varying degrees. Enterprises must continuously optimize and refine their solutions to deliver genuine user value and ensure a superior user experience. While many companies readily claim to have acquired tens of millions or even hundreds of millions of users, a critical question remains: Do their products truly deliver user value commensurate with these figures?

III. Identifying Commercial Value. Once you have genuinely created user value, it is time to pursue commercial value. Given the current state of the industry, although health management faces challenges such as unclear payers and low willingness to pay, with effective solutions in place, governments, insurance institutions, and users will all be willing to pay for truly high-quality health management solutions.

In the brief history of the internet, there is a prevailing logic: companies that fail to create value for users may achieve commercial success, but it will be short-lived.