The Next Frontier in CRO: Integrated Real-World Evidence Solutions

In August 1998, the State Drug Administration (SDA) was officially established. Following its establishment, in order to strengthen drug supervision and administration and promote law-based administration, the SDA reformulated and promulgated a series of regulatory frameworks, including the Measures for the Approval of New Drugs and the Good Clinical Practice (GCP) for Drug Clinical Trials, which were aligned with international standards while taking into account China’s national conditions.

The introduction of Good Clinical Practice (GCP) regulations spurred the emergence of China’s first wave of clinical Contract Research Organizations (CROs), such as Beijing Huisite (later known as Keweis), Eagles, Guangzhou Boji, and Beijing Qihuang. After 2000, a larger number of clinical CROs emerged, including Beijing Wanquan, Tigermed, Dimeisi, Rundo, Hanboruiqiang, Shenyang Yiling, Beijing Chuntian, Bonasia, Haijinge, Shanghai Yongzheng, Fangen Pharmaceutical, Noxell, Bonoway, Saidesheng, Kelin Likang, and Bestar. Benefiting from favorable clinical trial policies, the growth of the domestic pharmaceutical market, and the influx of foreign pharmaceutical companies into China, Tigermed was listed on the Shenzhen Stock Exchange in 2012.

In 2015, the former China Food and Drug Administration (CFDA) launched the “July 22” initiative for self-inspection and verification of clinical drug data. This move not only addressed the backlog in review and approval processes but also reshaped the landscape of clinical trials in China, leading to the downfall of a number of contract research organizations (CROs). Subsequently, the “Opinions of the General Office of the State Council on Carrying Out Quality and Efficacy Consistency Evaluation for Generic Drugs,” issued on March 5, 2016, spurred the emergence of a new wave of CROs primarily focused on bioequivalence (BE) studies. With the promulgation of the “Opinions on Reforming the Review and Approval System for Drugs and Medical Devices” on August 18, 2015, and the “Implementation Opinions on Deepening the Reform of the Review and Approval System to Encourage Innovation in Drugs and Medical Devices” on October 8, 2017, along with the implementation of a series of supporting policies, there was a significant acceleration in the return of biomedical talent to China and a surge in domestic enterprises’ enthusiasm for new drug research and development. The issuance of a batch of clinical trial approvals for new drugs greatly promoted the development of clinical-focused CROs and the emergence of new clinical-stage CRO companies.

Amid this wave of policy dividends, we are pleased to witness the growth of enterprises. In 2019, Tigermed reported revenues of RMB 2.8 billion and net profit of RMB 842 million, and plans to apply for a listing on the Main Board of the Hong Kong Stock Exchange. It will become the third leading Chinese “A+H” pharmaceutical R&D outsourcing service provider, following WuXi AppTec and Pharmaron, and remains the only CRO primarily focused on clinical services.

Unfortunately, since 2015, clinical CROs have secured a wave of investment driven by favorable policies, accelerating their development and expansion. However, in recent years, the sharp rise in labor costs and intense market competition have suddenly given rise to crises, with the COVID-19 pandemic further exacerbating the challenges faced by traditional clinical CROs. As of April 2020, no second Chinese clinical CRO had been listed on mainstream exchanges such as the Shanghai Stock Exchange, Shenzhen Stock Exchange, or Hong Kong Stock Exchange.

Is the IPO Dream for China’s Clinical-Stage CROs Still Far Off?

According to statistical data from the “China Pharmaceutical R&D Outsourcing (CRO) Industry Market Outlook and Investment Strategic Planning Analysis Report” released by Qianzhan Industry Research Institute, the sales revenue of China’s CRO industry market is expected to exceed RMB 100 billion in 2021. The compound annual growth rate (CAGR) over the five-year period (2019–2023) is approximately 19.86%, with forecasts indicating that the sales revenue of China’s CRO industry market will reach RMB 168 billion in 2023. In a market worth hundreds of billions of yuan, several CRO companies primarily engaged in CMO and safety assessment services have already gone public; it is implausible that only one CRO company focused on clinical trials would be listed.

Given the human resource service nature of traditional clinical CROs, factors such as high labor costs, uncontrollability in clinical trial operations, intense competition, and fragmented business scales have compelled these enterprises to break through their existing models, integrate new technologies, explore new service domains, and create new sources of high profit. The field of real-world evidence (RWE) is poised to become a new growth engine for CRO businesses—a potential multi-billion-dollar market on the verge of explosive growth. This sector will undoubtedly give rise to the next clinical CRO listed on the main board, with capital infusion providing it with immense potential for expansion and boundary-breaking innovation.

What Is Real-World Evidence? Why Is It Becoming the Next Growth Frontier for CRO Services? The author will analyze this rapidly expanding market from the perspectives of policy dividends, new opportunities in traditional business lines, emerging market opportunities, and expansion potential.

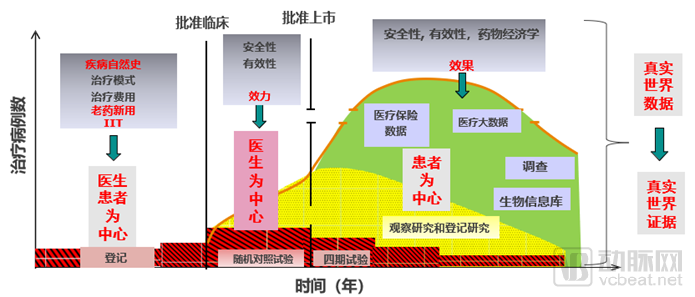

Real-world evidence refers to the relevant evidence generated from data on drug usage patterns, potential benefits, and safety obtained from sources other than traditional clinical trials. Real-world evidence is generated throughout and serves the entire product lifecycle, preceding product development and supporting the product throughout its lifespan. In particular, regulatory authorities in various countries are introducing a series of policies to support the use of real-world evidence in product development, review, and regulation, thereby accelerating market approval.

Integrated Real-World Evidence (RWE) solutions encompass not only traditional Phase IV clinical studies but, encouraged by policy, are also being applied to product review and market approval, thereby substituting for certain aspects of traditional randomized controlled trials. Furthermore, these solutions support pre-approval clinical research and post-marketing continuous safety and effectiveness studies, playing a significant role in academic research after product launch (as shown in Figure 1).

Figure 1. Real-World Evidence Across the Product’s Full Life Cycle

Window of Policy Dividends

In December 2016, the United States enacted the 21st Century Cures Act, encouraging the FDA to conduct research and use real-world evidence to support regulatory decisions for drugs and other medical products, thereby accelerating the development of pharmaceuticals. Driven by this legislation, the FDA successively issued the following documents between 2017 and 2019: “Use of Real-World Evidence to Support Regulatory Decision-Making for Medical Devices,” “Guidance on the Use of Electronic Health Record Data in Clinical Investigations,” “Framework for FDA’s Real-World Evidence Program,” and “Submitting Drug and Biologics Information to the FDA Using Real-World Data and Real-World Evidence.”

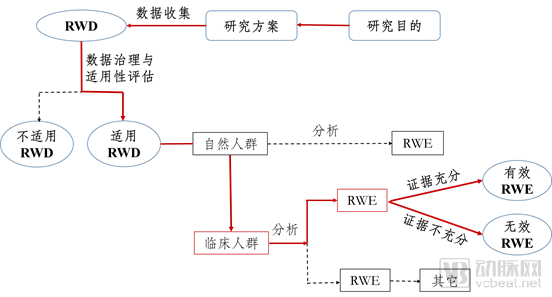

The National Medical Products Administration (NMPA) of China also issued corresponding requests for comments and, on January 7, 2020, released Document No. 1 of 2020, titled “Guiding Principles for Using Real-World Evidence to Support Drug Development and Review (Trial Implementation).” This document clarifies the definitions related to real-world studies, the sources and applicability of real-world data, the basic design of real-world studies, and the evaluation of real-world evidence, thereby providing guidance on leveraging real-world evidence to assess drug efficacy and safety. Real-world evidence can be used to support regulatory decision-making for drugs, including providing evidence of efficacy and safety for new drug registration and marketing approval, supporting changes to the labeling of marketed drugs, and fulfilling post-marketing requirements or re-evaluation. As shown in Figure 2:

Figure 2 is from the "Guiding Principles for Supporting Drug Development and Review with Real-World Evidence (Trial Implementation)"

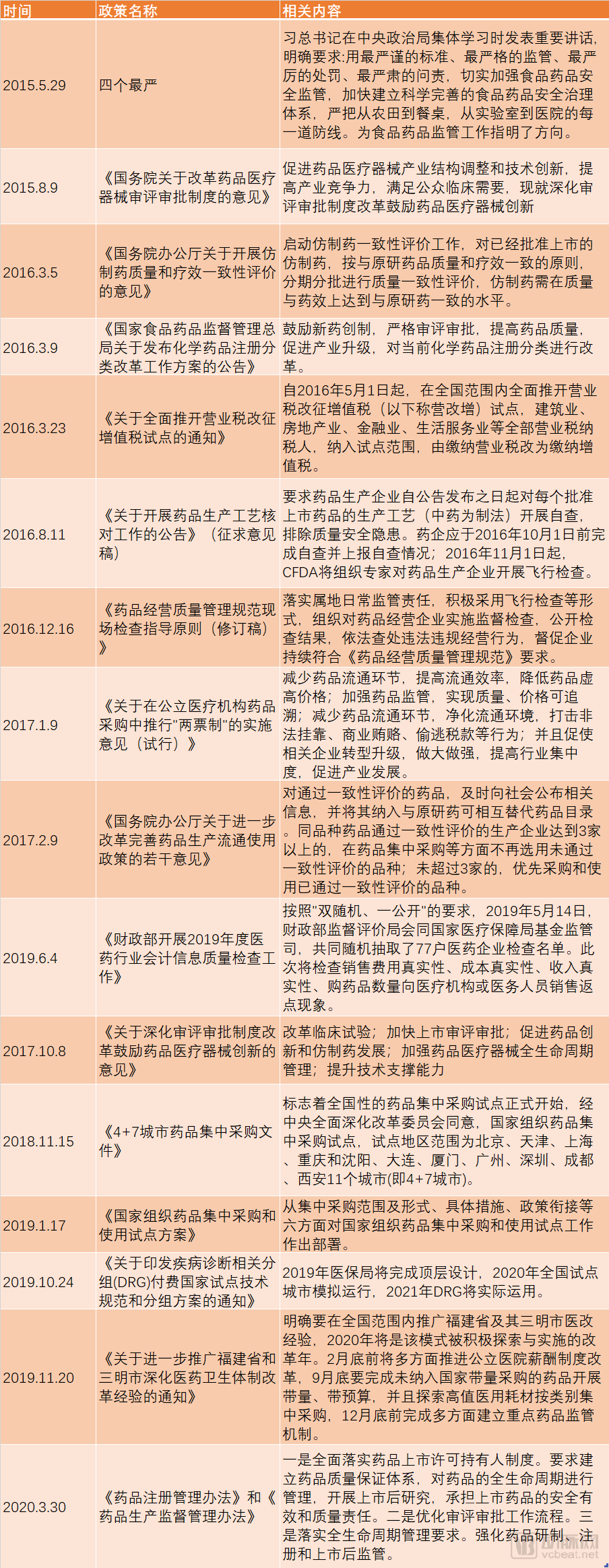

Amid the continuous introduction of policies in China’s pharmaceutical R&D sector, the landscape of drug marketing has also undergone significant changes. The 2016 wave of unannounced GMP/GSP inspections led to the closure of a large number of small-scale manufacturing enterprises. The consistency evaluation for generic drugs has further optimized the competitive structure of the pharmaceutical industry, leading to greater resource concentration. Reforms in the drug approval process have accelerated the clinical development and market launch of innovative drugs in China. These developments will further drive the integration of resources among domestic pharmaceutical companies, promote a combination of generic production and innovation, and ultimately enable Chinese-originated drugs to enter the global market.

The “Sanming Model,” the Two-Invoice System, the VAT reform, the “4+7” volume-based procurement program, the Ministry of Finance’s joint “penetrative” financial audits of pharmaceutical companies with the National Healthcare Security Administration, and the DRG pilot programs will fundamentally transform the traditional “kickback-driven sales model.” The industry will shift toward patient-centric academic marketing that focuses on product attributes, highlights unique product advantages, meets clinical needs, and better serves patients and physicians. This transformation in pharmaceutical marketing will spur a substantial increase in academic research, particularly post-launch studies for innovative drugs. Relevant policies are summarized in Table 1:

Table 1 Summary of Policies in Pharmaceutical R&D and Marketing

New Opportunities for Traditional Businesses

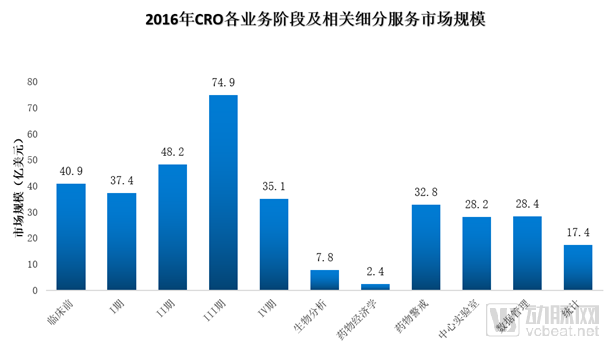

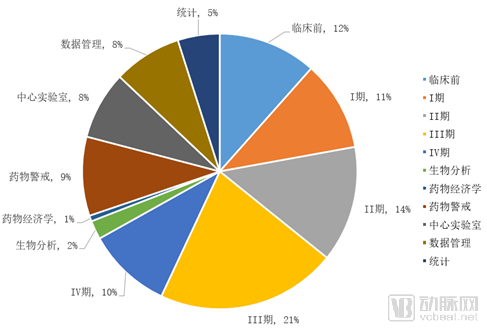

The core business of traditional clinical CROs is Phase I–IV studies. According to 2016 reports from Frost & Sullivan and China Merchants Securities, the market sizes for Phase I–IV clinical trials were USD 3.74 billion, USD 4.82 billion, USD 7.49 billion, and USD 3.51 billion, respectively, with corresponding market shares of 11%, 14%, 21%, and 10% (as shown in Figures 3 and 4).

Based on this ratio, the estimated size of China’s traditional Phase IV clinical trial market is approximately RMB 2.6 billion. Phase IV studies are characterized by large sample sizes, multicenter and multiregional designs, and long durations. Prior to the “July 22” regulatory crackdown, Phase IV studies—particularly those sponsored by foreign pharmaceutical companies—were a key competitive focus for traditional clinical CROs, with gross profit margins estimated at around 25%–35%.

Since the “July 22” policy change, the sharp rise in labor costs, the surge in the number of domestically developed innovative drugs, cost-cutting measures by foreign pharmaceutical companies, and extremely low gross profit margins have shifted Phase IV studies from the traditional domain of clinical CROs to a key focus area for big data companies and next-generation CROs. However, at present, only companies offering integrated real-world evidence (RWE) solutions can effectively manage these traditional Phase IV projects and achieve satisfactory profitability. Such companies require both strong clinical project operational capabilities and adaptive information technology systems. Therefore, traditional clinical CROs need to strengthen their IT and systematic capabilities to address project operational costs. Meanwhile, big data companies and next-generation CROs must enhance their clinical project operational capabilities to ensure project quality and timelines while controlling costs.

Figure 3 Market Size of CRO Services by Business Phase and Related Sub-segments, 2016

Figure 4. Market Share of CRO Services by Business Stage and Related Sub-segments, 2016

New Market Opportunities

As previously mentioned, the introduction of policies in the fields of drug research and development and marketing will create three new areas for real-world studies:

1. Real-World Studies for Product Registration

Real-world evidence can, in certain circumstances, serve as an alternative to traditional randomized controlled trial (RCT) studies for pre-market clinical development and post-marketing re-evaluation. The specific circumstances are as follows:

I. To provide evidence of efficacy and safety for the registration and marketing of new drugs: Based on the characteristics of different diseases, accessibility of treatment options, target populations, therapeutic outcomes, and other factors related to clinical research, real-world studies can be conducted to obtain information on drug effectiveness and safety, thereby providing supportive evidence for the registration and marketing approval of new drugs, such as those for rare diseases.

II. Providing Evidence for Label Changes of Marketed Drugs: When randomized controlled trials (RCTs) are infeasible or suboptimal, it may be more feasible and reasonable to use real-world evidence generated from pragmatic clinical trials (PCTs) or observational studies to support new indications, such as in the field of pediatric medications.

III. Summary of Human Use Experience and Clinical Development for Empirical Formulas from Renowned Senior TCM Practitioners and Preparations Produced by Medical Institutions: For the clinical development of drugs with existing human use experience, such as empirical formulas from renowned senior Traditional Chinese Medicine (TCM) practitioners and preparations produced by medical institutions, new pathways for clinical development may be explored by combining real-world studies with randomized clinical trials, provided that the prescription is fixed and the production process is largely established.

2. Real-World Studies of Innovative Drugs Post-Market Launch

Post-marketing studies are typically conducted extensively for innovative drugs after their launch to provide further clinical evidence and academic materials. The research costs usually account for approximately 10% of annual sales, gradually decreasing over time based on the drug's market presence.

For example, Pfizer’s Lipitor underwent at least one hundred post-marketing clinical studies after its launch. A substantial body of real-world evidence has demonstrated its superiority over other medications, generating extensive marketing materials, delivering high academic value, providing guidance for clinical practice, enhancing product competitiveness, driving substantial sales revenue, and prolonging the period of peak sales performance.

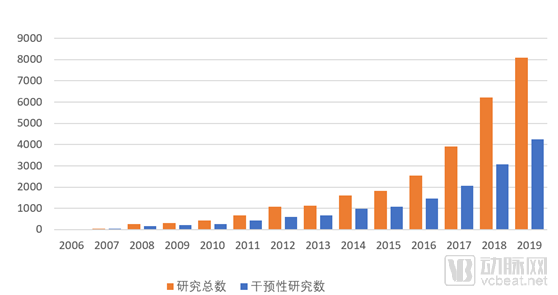

As shown by the number of non-Phase I–III studies registered with the Chinese Clinical Trial Registry and ClinicalTrials.gov (Figures 5 and 6), the volume of real-world studies in China continues to grow steadily. This trend is driven by two factors: on one hand, innovative drugs from Chinese pharmaceutical companies have been successively launched, while new drugs from multinational pharmaceutical companies are being accelerated onto the Chinese market; on the other hand, pharmaceutical marketing in China is shifting from kickback-driven sales to academic promotion, transitioning from market-driven to medically driven approaches. Consequently, pharmaceutical companies will conduct a substantial number of real-world studies in the future.

Figure 5. Number of projects registered at the Chinese Clinical Trial Registry (2006–2019) (excluding Phase I–III trials)

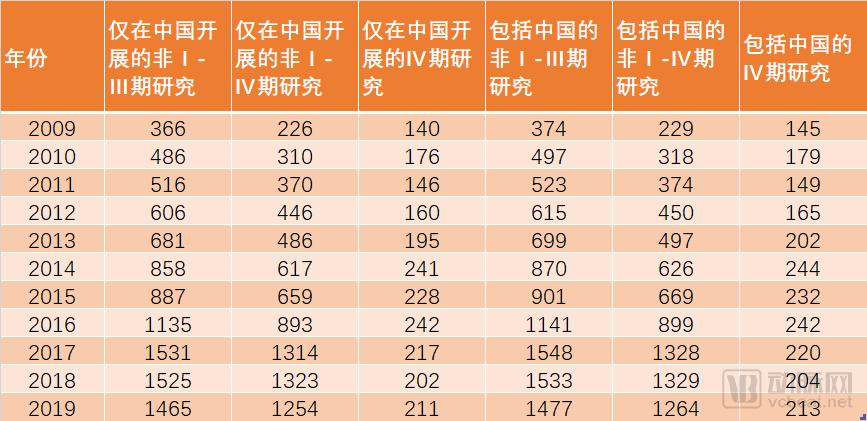

Table 2 ClinicalTrial Registration Involving Phase IV and Non-Phase I–IV Studies Conducted in China

3. Academic Research Based on Real-World Evidence

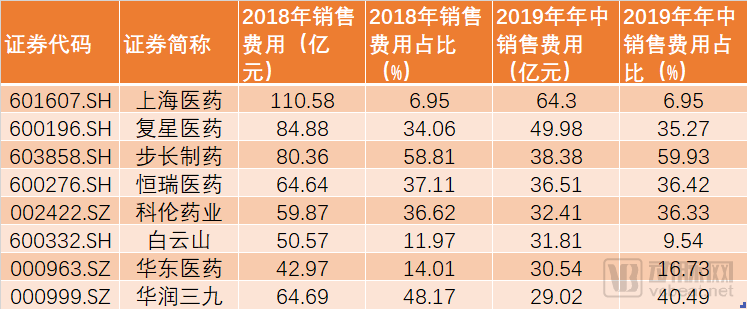

Sales expenses of Chinese pharmaceutical companies have remained persistently high (as shown in Table 3). Corporate expenses include sales expenses, administrative expenses, research and development (R&D) expenses, and financial expenses, with advertising and marketing-related expenditures included in sales expenses. In addition, sales expenses also cover market development and academic promotion fees, business entertainment expenses, and compensation for sales personnel, although the statistical methodologies vary among different listed companies.

In August 2018, Ren Zeping’s team published a report titled “Unveiling the Mystery of Abnormally High Sales Expenses in Chinese Pharmaceutical Companies.” The report stated that a 2014 survey identified six primary channels for sales expenditures by pharmaceutical companies in China: fees for influencing bidding agencies, fees for influencing hospital officials, kickbacks to physicians, commissions for medical representatives, costs associated with tax evasion and money laundering (through invoice fraud), and payments for prescription data collection (“tongfang”). Among these, expenditures on influencing bidding agencies, influencing hospital officials, and physician kickbacks corresponded respectively to the bidding phase, hospital procurement phase, and prescription sales phase, representing three rounds of benefit redistribution. Notably, physician kickbacks accounted for more than half of total sales expenses.

Table 3 Sales Expenses of Listed Pharmaceutical Companies

Under the “4+7” centralized volume-based procurement policy, shortlisted products will undoubtedly see a significant reduction in sales expenses. However, the pharmaceutical market still includes varieties not yet included in centralized procurement, such as adjuvant medications and traditional Chinese medicines. Amidst the transformation of sales models and stringent crackdowns on kickback-driven sales, previously allocated sales expenditures will shift from being sales-centric to focusing on product services that benefit patients. This transition will spur extensive academic research to further demonstrate the clinical value of respective products, which is precisely where real-world data and its evidence can play a pivotal role.

Expansion Space

On May 3, 2016, Quintiles, the world’s largest CRO, merged with IMS Health, a strategic consulting firm serving the pharmaceutical and healthcare industries, to form IQVIA. The merger created a cross-disciplinary company that integrates global information and technology services with traditional global outsourcing capabilities. Once a company in China develops integrated solutions based on real-world evidence, it will inevitably possess both of these service capabilities. Only such companies can break through the ceiling of traditional outsourcing services, thereby unlocking immense market potential.

Author: Xie Shengrong

Master of Pharmacology from China Pharmaceutical University, Bachelor of Clinical Medicine, and Chairperson of the Nanjing Ginkgo Biloba Rare Disease Family Care Center. Possesses 12 years of experience in clinical trial management and operations, having worked at both domestic and foreign CROs including Foresee Pharmaceuticals, PPD, and INC Research. Managed multiple Phase I–IV clinical studies and successfully completed pivotal Phase III trials for two new drugs.

Since 2015, we have focused on real-world studies. In 2017, we took the lead among CROs by establishing a dedicated Real-World Study Department, which now comprises 80 professionals. The department specializes in undertaking real-world studies for both domestic and foreign enterprises during the Phase III to Phase IV stages, key monitoring programs with 3,000 cases, investigator-initiated trials (IITs), academic research, epidemiological studies, as well as health economics and pharmacoeconomics research.