Quest Diagnostics: From Apartment Bathtub to Wall Street – A 15-Year, $9B+ M&A Journey Transforming Diagnostic Testing

Quest Diagnostics

Diagnostic Testing Service Provider

LabCorp

Medical Diagnostic Service Provider

On May 25, VCBeat released“270 Third-Party Medical Testing Labs Enter the Individual Nucleic Acid Testing Market: Can Consumer-Facing Business Become a New Growth Engine?”An analysis of the expansion strategies of domestic third-party clinical laboratory companies in the consumer market in the post-pandemic era.

It is widely believed in the industry that third-party testing institutions’ entry into the consumer market amid the pandemic marks an industry watershed, which may stimulate the previously sluggish domestic third-party testing sector and usher in greater development in the future.

In fact, after years of development, the third-party clinical laboratory industry in the United States has become highly mature and played a significant role during the COVID-19 pandemic. According to the latest quarterly reports from the two largest third-party testing giants in the U.S., Quest Diagnostics (hereinafter referred to as "Quest") can currently perform more than 50,000 nucleic acid tests for SARS-CoV-2 and 150,000 blood antibody tests per day; LabCorp can perform 55,000–65,000 nucleic acid tests and over 50,000 blood antibody tests daily.

VCBeat (WeChat ID: Vcbeat) has also provided a detailed analysis of the development history of Quest Diagnostics, a leading player in the global third-party clinical laboratory industry, which may help us better understand the future trajectory of this sector.

Quest has a rather long history; its predecessor, Metropolitan Pathology Laboratory (MetPath), was established in 1967 by Paul A. Brown, who was then a pathology resident at NewYork-Presbyterian Hospital.

As a pathologist, Brown witnessed firsthand the chaotic state of the testing industry at the time and aspired to establish a company that could provide high-quality laboratory testing capabilities to the surrounding areas. To this end, he borrowed $500 from his godfather to found MetPath.

Quest’s predecessor, MetPath, was originally founded in this apartment (image from Quest’s official website)

Many famous American companies were founded in garages, and garage culture represents the entrepreneurial spirit prevalent in American society. However, unlike those on the spacious West Coast, MetPath, which started in crowded New York, was not established in a garage but in an ordinary apartment in Washington Heights, northern Manhattan. Due to the cramped space, Brown had to use the bathtub in the apartment as the workspace for slide testing.

After a period of development, MetPath gradually gained recognition. In 1982, the renowned Corning Glass (a traditional company whose name may sound somewhat unfashionable, but which later rose to prominence in the internet era with its well-known “Gorilla” scratch-resistant glass) acquired MetPath and renamed it Corning Clinical Laboratories, making it a key component of its healthcare business.

Corning expanded its laboratory testing business through hundreds of mergers and acquisitions. In particular, between 1991 and 1995, the revenue of Corning Clinical Laboratories tripled. Coupled with the competitive landscape at the time, the spin-off of Corning Clinical Laboratories was put on the agenda.

Development of the U.S. Clinical Laboratory Testing Market at That Time

Independent clinical laboratories in the United States emerged in the 1930s. Due to the large number of private practices in the U.S., many of these facilities lacked sufficient capital to procure large-scale instrumentation for testing their limited sample volumes. Consequently, hospital laboratories began offering outsourced testing services to these private practices.

Independent third-party medical testing laboratories first emerged in the 1960s. As a nascent industry, the early third-party testing market lacked adequate regulation and quality assurance, resulting in significant variability in service quality. This environment paved the way for the establishment of MetPath, the predecessor of Quest Diagnostics.

Notably, just two years after the founding of MetPath, a testing laboratory named Biomedical Laboratories was established. It later evolved into LabCorp, which would become Quest Diagnostics’ primary competitor.

Since the 1960s, total healthcare expenditure in the United States has exhibited an explosive upward trend. In 1980, total healthcare spending reached $247.2 billion, nearly ten times the $26.9 billion recorded in 1960. Its share of U.S. GDP for that year also rose from 5.1% to 8.9%.

To alleviate the financial burden on healthcare, the U.S. government and commercial health insurance providers have successively revised health insurance policies since the 1980s, reducing medical subsidies to hospitals.

In 1984, the U.S. Congress mandated that laboratory testing services be covered under Medicare Part B (Medical Insurance Supplementary to Hospital Insurance) and periodically reduced the Medicare budget caps. This legislation served as a catalyst for the development of the third-party laboratory industry.

Driven by cost considerations, some hospitals began outsourcing laboratory services to independent clinical laboratories with lower operating costs, ushering in the first phase of rapid growth for these independent entities. By the late 1980s, the market share of third-party testing institutions had expanded to approximately 20% of the overall testing market, on par with that of private clinics. Meanwhile, the market share of hospital laboratories, which once held an absolute dominant position, declined to around 60%.

To address the long-standing deficiencies in laboratory testing and service quality, the U.S. Congress enacted the Clinical Laboratory Improvement Amendments of 1988 (CLIA '88), initiating strict regulation of physician office laboratories and independent medical laboratories. The legislation mandates that clinical laboratories obtain certification to ensure that their testing services are consistent, accurate, reliable, and timely.

This legislation spurred renewed rapid growth in independent clinical laboratories that held advantages in quality and efficiency. By the mid-1990s, the market share of private clinic-based testing had declined to 8%, while the market share of third-party testing providers rose to approximately 35% of the overall testing market.

Despite their competitive advantages in cost and scale, third-party clinical laboratories face significant challenges in capturing market share from hospital-based laboratories due to various factors, such as insurance reimbursement rates and institutional protectionism. Consequently, this market share ratio has remained largely unchanged to date.

According to estimates, the U.S. medical testing market reached $30 billion in 1995 and was experiencing rapid growth. Based on a 40% share outside hospital laboratories, third-party testing institutions still had a $12 billion market opportunity, representing significant potential.

Meanwhile, although laboratory testing expenditures account for only 4% of total healthcare spending in the United States, they influence more than 70% of diagnostic decisions, underscoring their pivotal role.

Spin-off from Corning and Independent Listing

In the mid-1990s, the third-party clinical laboratory industry faced intensifying competition, leading to a significant decline in revenue and profitability. This was driven by strict government regulations and accounting audits, mounting pressure to reduce healthcare costs amid rising medical expenditures, and a market condition of oversupply.

To navigate the intensely competitive landscape at the time, while rapidly achieving economies of scale and maintaining focus and flexibility, Corning Glass decided to spin off its healthcare business as an independent publicly traded company. To ensure the new entity’s financial health, Corning even forgave more than $700 million in debt attributable to the laboratory testing business.

In early 1996, Quest was listed on the New York Stock Exchange, comprising two business segments of Corning’s healthcare operations: Corning Clinical Laboratories and Corning Nichols Institute. Another segment under Corning, Corning Pharmaceutical Services, was spun off independently under the name Covance and has since grown into a globally renowned CRO company.

Interestingly, Covance was acquired by LabCorp, Quest’s biggest competitor, in 2015—a case of “brothers born of the same root, why rush to torment each other?”

The name "Quest" represented the company’s vision at the time: Quality, Integrity, Innovation, Accountability, Collaboration, and Leadership.

Since its inception, Quest has established three clear strategic visions: to provide high-quality, cost-effective laboratory testing and services; to become the preferred partner for large healthcare purchasers, such as regional health organizations; and to emerge as an innovative leader in the pathology testing, information, and services industry.

Although specific details have been adjusted over time, Quest’s corporate vision and goals have remained largely unchanged over the years—a practice well worth learning from for Chinese enterprises.

It is worth noting that the Nichols Institute, which was integrated into Quest Diagnostics, enjoys a prestigious reputation in the field of pathological testing and has been central to ensuring Quest’s subsequent leadership in innovation.

Dr. Albert Nichols founded the Nichols Institute in 1971. It has long been a leader in innovation in laboratory testing, translating numerous academic achievements in laboratory diagnostics into commercial successes. Among its most renowned contributions are the widely recognized method for measuring free thyroxine and novel assays for monitoring the efficacy of HIV treatment.

Guided by its clear vision for development, Quest established several strategic initiatives following its independent public listing. These strategies subsequently permeated the entire course of Quest’s growth.

First, enhance service quality by introducing Six Sigma quality control;

Second, rapidly expand scale to achieve economies of scale;

Third, enhance profitability and reduce costs;

Fourth, collaborate with large healthcare purchasers to maximize coverage of the insured population.

Implementing Six Sigma to Enhance Service Quality

In 1998, Quest launched the “Our Quality Journey” initiative, aiming to achieve industry-leading quality standards by the end of 2002.

First, Quest aimed to reduce the voluntary employee turnover rate from 16% at that time to 10% by 2000, and further down to 7% by the end of 2002. According to internal statistics, Quest incurred annual costs of up to $60 million due to voluntary turnover, stemming from recruitment, training, and reduced operational efficiency.

Second, to enhance customer satisfaction, it is necessary to elevate the quality of medical services to Six Sigma levels. At that time, the prevalent testing accuracy rate in the diagnostic industry was approximately 90%. Quest Diagnostics planned to increase this to 99.99966%, meaning only 3.4 errors per one million tests.

Third, establish minimum growth requirements. Quest plans to double its operating profit by the end of 2002.

Six Sigma implementation was rigorously executed thereafter. In 2000, the number of Six Sigma Black Belts reached 135, a threefold increase. By 2002, nearly all members of the senior management team had become Six Sigma Green Belts.

Meanwhile, in 2002, two clinical laboratories and their testing facilities under Quest Diagnostics obtained ISO 9001 certification, while five additional laboratories achieved ISO 9002 certification.

Strict quality requirements have also laid a solid foundation for its subsequent acquisition of competitive advantages.

Expand and Enhance Scale Advantages

In 1996, Quest Diagnostics processed over 60 million orders from more than 75,000 clients annually, operating 17 regional laboratories and 14 branch offices across the United States. Nichols Institute was positioned as a premium brand in the market, leveraging ultra-sensitive gene sequencing, cell scanning, and biochemical technologies to provide complex immunoassays, cytogenetic, and molecular diagnostic tests to nearly one-third of hospitals nationwide.

By 1999, Quest had achieved significant growth, becoming the market leader in the U.S. third-party clinical laboratory industry with an 8% market share. Quest operated 1,400 convenient patient service centers and maintained a fleet of 3,000 specialized specimen transport vehicles across the United States. It performed 400,000 tests each business day and served 100,000 individuals in the top 50 metropolitan areas nationwide.

Meanwhile, Quest has also begun its overseas expansion, establishing offices in London (UK), Mexico City (Mexico), and São Paulo (Brazil).

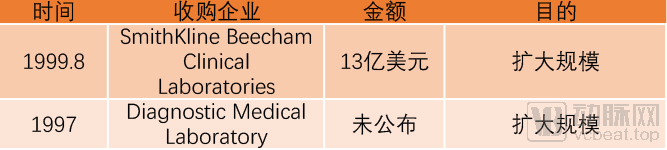

In 1997 and 1999, Quest acquired Diagnostic Medical Laboratory and SmithKline Beecham Clinical Laboratories, respectively. The latter acquisition, in particular, amounted to $1.3 billion, a substantial sum at the time.

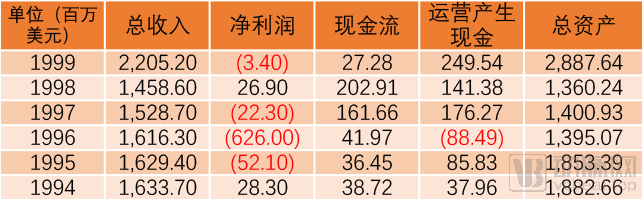

Unit: Million USD

We can discern the impact of these two acquisitions from Quest’s annual reports at the time: In 1996, Quest’s total revenue, cash flow from operations, and total assets were $1.616 billion, -$88 million, and $1.395 billion, respectively; by 1999, these three metrics had reached $2.205 billion, $250 million, and $2.888 billion, respectively. Quest rapidly expanded its scale, and the advantages of scale began to emerge.

Enhancing Profitability

In the mid-1990s, market competition in the third-party clinical laboratory industry was intense. To secure orders, price wars became the preferred competitive strategy for most third-party testing companies, significantly impacting the profitability of this emerging sector.

Quest found that, due to rapid market expansion and intense competition, the primary metric used by the industry to evaluate sales department performance was the number of new customers acquired. The sales department paid little attention to whether contracts were profitable. After establishing advantages in quality and scale, Quest began addressing this issue. It revised the sales department’s performance metrics to include contract profitability as a key consideration.

First, Quest assessed its current order status. In regions where contract prices were significantly below cost, Quest leveraged the reputation built through high-quality services to renegotiate pricing with customers, or adjusted payment models by shifting from fixed monthly payments to fee-for-service arrangements. These measures enhanced the company’s profitability while remaining acceptable to customers.

Secondly, in 1997, Quest Diagnostics conducted a review of the profitability of its laboratory network. It improved laboratory profitability by reducing the scale of loss-making laboratories, merging them with other facilities, or integrating them into laboratory collaborative alliances. Following these adjustments, nearly all laboratories returned to profitability.

Furthermore, given that most customers were confined to local markets at the time, Quest began exploring alternative revenue streams, aiming to achieve nationwide sales in China without establishing branch offices. The adoption of information technology and database utilization was also prioritized on the agenda.

In fact, the company had already established its database division as early as 1994, which later became the Quest Informatics business. This venture enabled healthcare management organizations to leverage Quest’s accumulated laboratory database to better manage patients’ health status and disease risks. In the initial phase, Quest primarily generated revenue by providing these organizations with rapid access interfaces to its database.

Finally, Quest Diagnostics also expands its partnerships with hospital laboratories by leveraging its expertise to provide outsourced management services, or by helping hospitals integrate their laboratory operations to enhance profitability and further strengthen relationships with these institutions.

Two competing nonprofit hospitals in western Pennsylvania once attempted to merge their laboratories to reduce costs, but ultimately failed. The predecessor of Quest Diagnostics has been providing them with outsourced management services since 1986.

With the assistance of Quest, the laboratories of the two hospitals established distinct divisions of labor. The shared laboratory was designated for inpatient testing, while the other was established as an independent commercial laboratory to provide outpatient testing services.

Following the spin-off, the laboratory’s overall operational efficiency and service quality improved significantly, while costs declined. At that time, the minimum cost for laboratory testing at emergency care hospitals across 571 urban areas in the United States was $571, whereas in the Pennsylvania region, it was only $343.

With such cases in hand, more hospitals began to outsource services to Quest Diagnostics. In 1996, 17 hospitals in Pennsylvania joined the laboratory consortium. Additionally, within California and Iowa, 25 hospital laboratories formed consortia with assistance from Quest Diagnostics.

In this way, Quest Diagnostics established strong collaborative relationships with many hospitals, which later facilitated its acquisition of their laboratory businesses. However, some consortia, having learned from Quest Diagnostics’ experience, instead became its competitors.

Strengthen Collaboration with Large-Scale Healthcare Service Purchasers

Since its inception, key accounts have been Quest’s most significant source of revenue. According to the 1996 annual report, orders from monthly subscription-based users accounted for approximately 35–40% of the company’s total order volume, making it a veritable cash cow.

To underscore its commitment to key accounts, Quest Diagnostics reorganized its sales and marketing departments into two divisions: one dedicated to traditional clients, and the other focused on expanding into high-growth emerging sectors, such as large-scale networks and regional healthcare service providers.

In 1998, Quest entered into partnerships with Johns Hopkins Medicine and Sutter Health, a move widely regarded as a significant breakthrough in securing major clients during the company’s early years. Subsequently, Quest established a long-term collaboration with Oxford Health Plans, which served 1.75 million members, and signed a ten-year exclusive service agreement with Premier Inc., a leading group purchasing organization for healthcare providers.

In addition to direct services, Quest has another strategic move for collaborating with key accounts—establishing joint ventures. As a result, contracts with these key clients are naturally held under the joint venture entities.

For example, Quest Diagnostics formed a joint venture with Samaritan Health System, the largest healthcare provider in Arizona, to establish Sonora Quest Laboratories. In 1998, Quest Diagnostics also established joint ventures with UPMC Health System and Unity Health, both of which are major local healthcare providers.

Through the implementation of a series of measures, Quest rapidly scaled up and became the leader in the third-party clinical laboratory industry at that time. As the industry entered a period of prosperity, Quest also experienced more than a decade of rapid growth.

Since the turn of the millennium, independent laboratories such as Quest Diagnostics have gradually consolidated, achieving economies of scale. To ensure compliance, these companies have exercised considerable caution in designing every aspect of their operations, strictly adhering to governmental regulatory requirements. These measures have collectively reduced industry risks.

More importantly, the influence of health management groups reversed the downward trend in testing fees. These factors enabled the third-party clinical laboratory industry to gradually recover starting in 1999, ushering in a decade-long period of rapid growth.

At the time, Quest Diagnostics believed that the market size of the clinical laboratory industry would grow by at least 5% annually, with long-term growth potentially reaching 7%. This projection was primarily based on several considerations.

First, the overall population distribution and aging trend in the United States have led payers to favor early disease screening and prevention as a means of reducing total healthcare expenditures.

Second, advances in genomics and proteomics have facilitated the development of novel genetic testing methods and technologies; the resulting cost reductions from technological progress have further enhanced test accessibility.

Third, the demand for testing and monitoring of infectious diseases, such as HIV and hepatitis C, has risen significantly.

Fourth, technological advancements and cost reductions have increased the accessibility of testing.

Fifth, years of market education have heightened consumers’ awareness of diagnostic testing, leading to a certain willingness to pay even in the absence of insurance coverage.

Based on these considerations, in addition to adhering to its previous strategy, Quest Diagnostics has shifted its growth focus toward advanced testing technologies such as genetic testing, anatomic pathology, and targeted regional acquisitions. Meanwhile, the company has fully leveraged the empowering potential of digitalization.

Activating the "Acquisition Maniac" Mode and Diversified Operations

During this phase, Quest completed several highly significant acquisitions, the impact of which continues to this day.

First, the acquisition of MedPlus was completed in November 2001, securing the core capabilities required for informatization. MedPlus’s ChartMAXX electronic medical record (EMR) system was vigorously promoted across hospitals and clinics. Subsequently, MedPlus also developed eMaxx for internet connectivity.

Seizing this opportunity, Quest began integrating its internal information systems in 2002. At that time, the internet was still in its infancy, and many previously acquired laboratories operated locally with a wide variety of disparate IT systems. As the company expanded, this fragmented approach could no longer meet operational needs.

With the rapid development of the Internet, Care360, which evolved from eMaxx, has gradually become a key competitive advantage for Quest. Physicians can fully digitize ordering, result retrieval, medication prescribing, and online sharing of medical data through this system. This has significantly reduced error rates in these processes and improved efficiency.

It is precisely because of these advantages that the adoption rate of Care360 has increased year by year. In 2006, more than 100,000 physicians used Care360. Five years later, in 2011, this figure doubled, with the number of physicians using the service reaching 200,000; that year, 32 million prescriptions were issued through Care360.

In 2009, shortly after the rise of mobile internet, Quest Diagnostics launched Care360 Mobile for use on the iPhone. In 2010, Care360 obtained ONC-ATCB 2011/12 certification from the Office of the National Coordinator Health Information Technology Certification Body (ONC-ATCB), becoming a comprehensive EHR product.

Between 2006 and 2007, Quest Diagnostics successively acquired Enterix, Focus Diagnostics, HemoCue, and AmeriPath. Through these acquisitions, Quest Diagnostics strengthened its portfolio in early cancer screening, infectious disease testing, point-of-care testing technologies, and anatomic pathology services.

In particular, the $2 billion acquisition of AmeriPath drove Quest Diagnostics’ revenue in the anatomical pathology segment to surge to $2.5 billion in 2007, accounting for 35% of its total revenue. In 2002, this segment generated only $1 billion in revenue.

It is precisely these acquisitions that have given Quest the confidence to embark on its next move: adjusting its revenue structure to achieve greater diversification.

Expand Revenue Diversification

Quest’s ambition to expand revenue diversification was not a fleeting idea, but rather stemmed from the development of the U.S. clinical laboratory market. Compared with the situation more than a decade earlier, the landscape of the U.S. laboratory market had undergone certain changes by 2005. Hospital-affiliated laboratories continued to dominate, accounting for 60% of the market share.

However, changes have occurred in the fields of third-party laboratories and clinic-affiliated laboratories. Third-party laboratories have essentially captured the market share previously held by clinic-affiliated laboratories, accounting for 33% of the entire clinical testing industry.

However, as before, it remains extremely difficult to capture market share from hospital-affiliated laboratories. This will have a certain impact on Quest’s sustainable revenue. Therefore, Quest has also proposed increasing the proportion of revenue derived from non-testing businesses.

Starting in 2001, Quest Diagnostics began to focus on drug abuse testing and clinical trial testing. In that year, it provided laboratory services to 19–20 leading pharmaceutical companies and signed 830 new drug support agreements. Among these, GlaxoSmithKline has consistently been Quest Diagnostics’ largest client in clinical drug trials, accounting for 40–50% of this business over the long term.

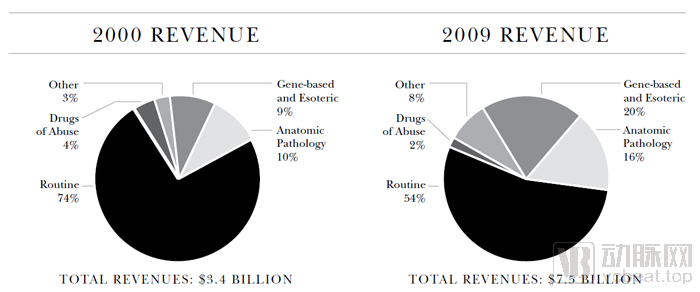

According to the 2005 annual report, laboratory testing services accounted for 95% of the company’s revenue; clinical drug trials rose to 3%, and health insurance risk assessment contributed less than 1%. Quest aims to increase the share of non-testing businesses to 8% of total revenue within a few years.

Based on the revenue breakdown disclosed in 2009, Quest indeed achieved its goal of increasing the proportion of non-testing businesses to 8%.

Comparison of Quest’s Revenue Structure (Image from Quest Annual Report)

Meanwhile, Quest also proposed an internationalization strategy. In 2007, 3% of Quest’s revenue came from overseas. Quest entered the Indian market in 2007 to meet its plan of having international revenue account for 10% within five years.

Due to India’s relatively open regulatory environment for drug clinical trials, Quest’s primary operations in the country focus on conducting clinical trials for multinational pharmaceutical companies, while also incorporating health insurance risk assessment and high-end testing services. Consequently, the establishment of this presence can increase the proportion of non-testing revenue in its overall income.

Technological Innovation

Through continuous R&D, external collaborations, and acquisitions, Quest has been innovating its products to continually enhance their appeal to users.

As early as 2002, Quest Diagnostics entered into a strategic partnership with Roche, becoming the first third-party laboratory to introduce Roche’s novel testing technologies, such as the electrochemiluminescence NT-proBNP assay used to aid in the diagnosis of congestive heart failure.

Subsequently, Quest partnered with Celera Diagnostics and Correlogic Systems to enter the promising fields of early screening for cardiovascular disease and blood testing for ovarian cancer.

Essentially, Quest Diagnostics introduces new testing technologies every year. The aim is to continuously enhance the customer experience and alleviate patient anxiety and discomfort.

For example, Quest Diagnostics’ Leumeta test, introduced in 2007 and based on plasma detection, can reduce the pain associated with bone marrow biopsies for patients with leukemia and lymphoma. The ImmunoCAP allergy blood test can avoid the itching caused by asthma allergen testing.

Meanwhile, Quest has also set the benchmark for the diagnostic testing industry. For instance, in 2008, Quest obtained exclusive licensing from Fujirebio for a serum HE4-based test, which was the first FDA-approved screening test for early detection of ovarian cancer in two decades.

In response to the H1N1 pandemic that began in 2009, Quest Diagnostics pioneered the development of an H1N1 viral test and, in collaboration with Vermillion, developed OVA1, the first FDA-approved early screening test for malignant ovarian masses.

In 2007, the Blueprint for Wellness risk assessment program, originally part of Quest’s employee healthcare benefits package, successfully attracted many major clients. Prominent organizations such as Domino’s Pizza, one of the most well-known fast-food chains in the United States; the Houston Independent School District; and Turner Construction Company, a renowned construction firm, all became clients of this program.

Quest Diagnostics has also kept pace with the internet and mobile internet trends, partnering with Google to launch Google Health. This application enables users to easily and conveniently manage their test results and order certain restricted tests under their own names.

In addition to Google, Quest has partnered with Keas and Microsoft to launch Keas and Microsoft HealthVault services. It also introduced the TestMinder service, which sends email reminders to patients who require frequent testing, as well as apps such as Gazelle, which allows users to view test results and manage their health conditions on their mobile phones.

In addition to these measures, Quest Diagnostics set a target in 2007 to reduce its operating costs by $500 million. Consistent with the successful implementation of its previous initiatives, this goal was exceeded ahead of schedule in 2009, demonstrating the company’s impressive execution capabilities.

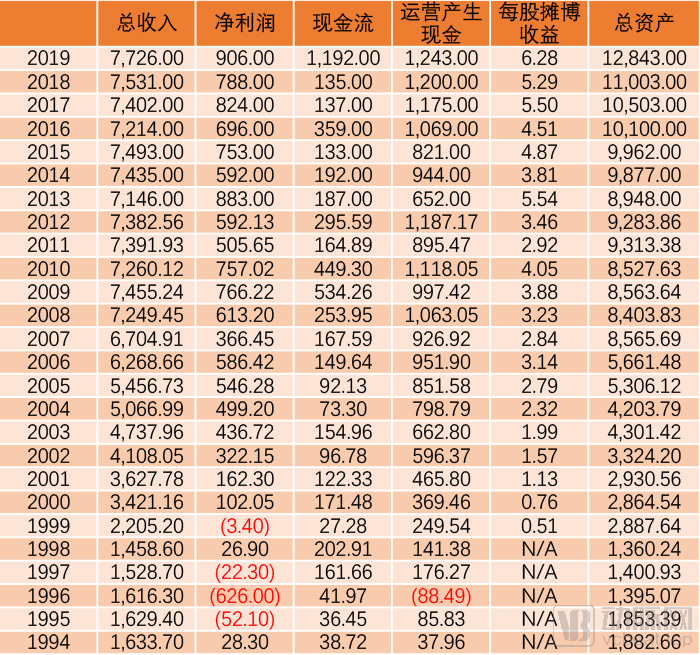

Unit: USD million (diluted earnings per share in USD)

During this golden decade, Quest Diagnostics delivered exceptional financial performance. In 2000, its total revenue, net income, and diluted earnings per share were $3.421 billion, $102 million, and $0.76, respectively. By 2009, these figures had reached $7.455 billion, $766 million, and $3.88, representing increases of 2.18-fold, 7.51-fold, and 5.12-fold, respectively.

Quest has become the undisputed leader in the third-party clinical laboratory industry with a 15% market share, growing into a behemoth that operates more than 2,000 patient service centers, maintains a fleet of over 3,500 dedicated transport vehicles, and owns 25 aircraft.

Such impressive performance makes it no surprise that Quest could proudly declare on its 10th anniversary in 2006 that an initial investment of $10,000 in Quest’s stock at the time of its IPO in 1996 would have been worth $145,000 by the end of 2006.

Of course, in addition to Quest’s own efforts, its strong performance during this period was also largely attributable to the overall prosperity of the industry. In fact, in 2006, Quest lost its contract with UnitedHealthcare, which served 12 million patients and accounted for as much as 7% of its total revenue.

However, the cash flow generated from operations in 2007 declined only slightly, dropping from $952 million in the previous year to $927 million, before resuming rapid growth. This prosperity appears to have clouded Quest’s judgment, sowing the seeds of future trouble.

At the start of 2010, Quest Diagnostics faced significant challenges. In 2010, the U.S. Food and Drug Administration (FDA) announced its decision to exercise regulatory authority over the clinical laboratory testing industry and planned to issue guidance on its regulatory approach to the sector.

The FDA has proposed adopting a risk-based regulatory approach, with particular focus on test items that have a wide distribution range and pose a higher risk of harm. This has had a significant impact on the third-party clinical laboratory industry.

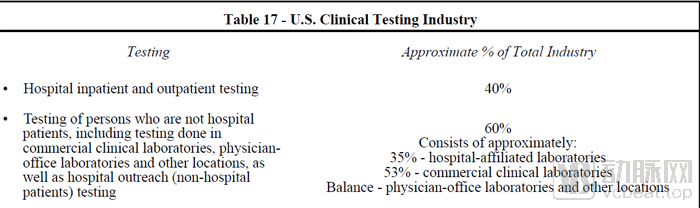

Meanwhile, after years of expansion, the market space for the third-party testing industry has gradually become saturated and stabilized. Due to various factors, third-party testing institutions have still been unable to capture market share from hospital-affiliated laboratories. Compared to ten years ago, the shares of hospital-affiliated laboratories, third-party testing institutions, and clinic laboratories have remained virtually unchanged.

This awkward predicament even led Quest to devise an alternative calculation method in its annual report, dividing the laboratory testing industry into in-hospital and out-of-hospital testing. However, it takes only a few seconds to realize that this is merely a semantic game.

Quest Diagnostics changed its methodology for estimating market share in its annual reports during the 2010s (Image source: Quest Diagnostics Annual Report)

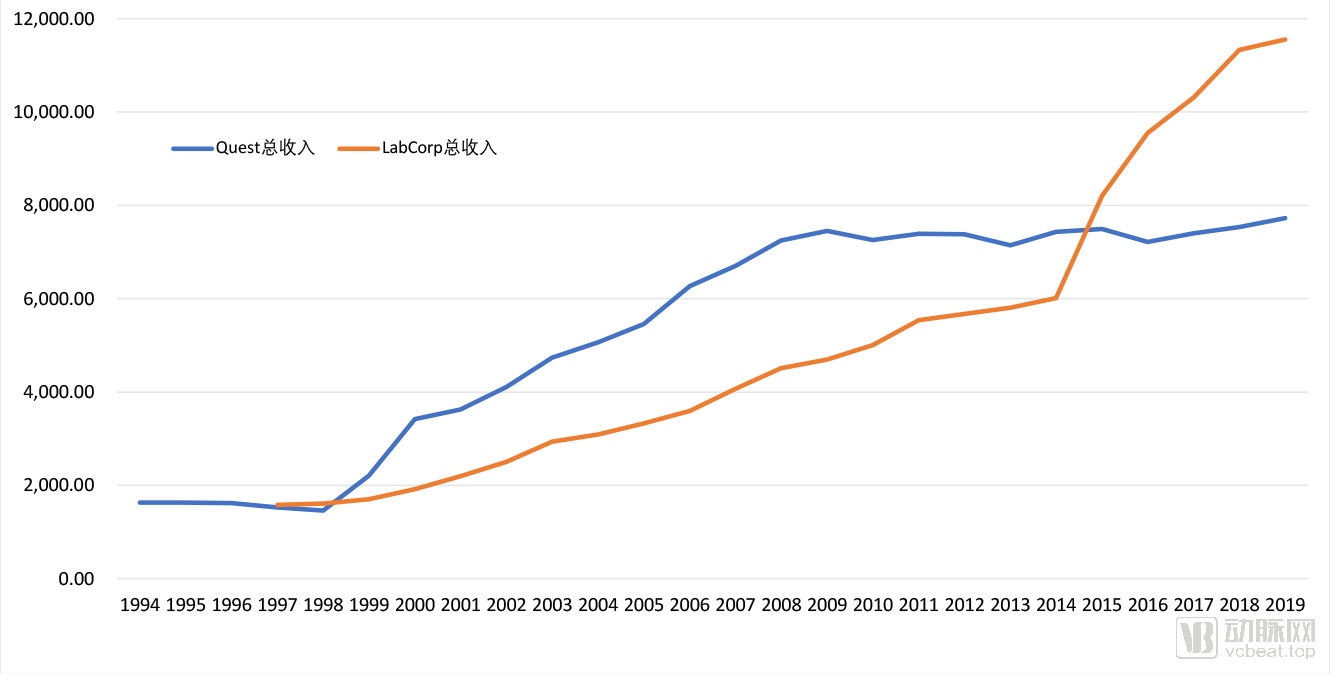

After reaching a revenue peak of $7.455 billion in 2009, Quest’s performance hovered around this level in the subsequent years. The ceiling effect became evident. In 2015, its largest competitor, LabCorp, surpassed Quest in revenue for the first time after completing its acquisition of Covance.

Comparison of Total Annual Revenue of the Two Major Laboratory Testing Giants (Unit: Million USD)

Quest Diagnostics revisited its strategy in 2012. First, it reviewed the criteria users employ when selecting third-party clinical laboratories.

These criteria include: service capability and quality; accuracy, speed, and consistency of test results; pricing; insurance coverage; variety and volume of tests offered; number, convenience, and geographic location of testing centers; reputation among physicians; information technology solutions; staff qualifications; and the ability to develop new tests.

Based on these factors, Quest Diagnostics has proposed the strategic goal of “Renewed Growth”: 1. Refocus on diagnostic information services; 2. Drive operational excellence; 3. Restore growth; 4. Streamline organizational structure to promote growth and efficiency; 5. Implement disciplined capital allocation and pursue value-accretive acquisitions through strategic alliances.

In fact, in terms of specific measures, Quest took two actions: first, subtraction, and then addition.

Step 1: Streamline Costs

First, streamline the organization and reduce costs. In 2013, Quest Diagnostics eliminated three layers of management hierarchy at once, cutting 400 to 600 managerial positions.

In 2012, Quest Diagnostics announced a plan to continuously reduce operating expenses, targeting a $500 million cost reduction in 2014 compared to 2011 levels. By 2014, the company had actually reduced its operating expenses by $700 million.

Subsequently, Quest planned to reduce costs by $600 million in 2017, bringing the total cost reductions since 2011 to $1.3 billion.

As part of its divestiture strategy, Quest sold its OralDNA saliva testing business, HemoCue, and Enterix’s test manufacturing operations consecutively in 2012–2013, generating approximately $800 million in proceeds.

Quest Diagnostics has once again consolidated its laboratory and diagnostic information services and implemented a franchising model, aiming to reduce costs while delivering premium services without compromising its scale advantages.

Of course, Quest Diagnostics has not franchised all of its testing services. Its focus is concentrated on cardiovascular, metabolic, and endocrine disorders; routine health screenings; infectious diseases and immunology; neurology; oncology; prescription drug monitoring and toxicology; sports medicine; and gynecology and reproductive health.

Step 2: The Buying Spree Mode Is On

The first step in addition is to initiate an aggressive acquisition mode. In 2016, Quest Diagnostics even proposed strategically accretive acquisitions as one of the means to achieve annual growth of 1–2%.

Compared to the previous decade-plus, the number of acquisitions by Quest during this period has been staggering. However, the deal sizes have not reached the multi-billion-dollar magnitudes seen in the past.

The acquisitions of Athena Diagnostics ($740 million) and Celera Corporation ($344 million) in 2011, as well as the acquisition of Solstas Lab Partner Group ($572 million) in 2014, were among the most significant deals during this period.

These acquisitions enabled Quest to secure several key major clients, including IBM Watson Health, Optum (a subsidiary of UnitedHealth Group), Safeway, AncestryDNA, Walmart, Cleveland Clinic, McKesson Special Health, U.S. Oncology Network and Texas Oncology, and Montefiore Health System (a renowned academic medical center in the New York metropolitan area).

Notably, by first securing an order from this subsidiary, Quest successfully regained the long-term contract with UnitedHealthcare in 2018.

Quest also restructured its IT architecture, and MyQuest, the application upgraded from Care360, had 87 million registered users by 2019.

Through collaborations with enterprises, universities, and institutions such as Genomic Vision, the University of California, the CDC, and the NIH, Quest Diagnostics has also introduced a variety of new testing technologies.

In 2012, the STRATIFY JCV Antibody ELISA test received FDA Breakthrough Device designation. It was the first FDA-approved assay for detecting antibodies against the JC polyomavirus, used to assess the risk of developing progressive multifocal leukoencephalopathy (PML), a severe rare disease.

All of this enabled Quest to return to growth. In 2019, Quest delivered an impressive financial report: total revenue reached $7.726 billion, while net profit of $906 million, cash flow of $1.192 billion, and operating cash flow of $1.243 billion all hit record highs.

In terms of revenue structure, Quest has also refocused on its testing business, which accounts for 96% of the total. Based on this proportion, the annual revenue generated by the testing business should be approximately $7.417 billion.

Based on the data disclosed in LabCorp’s 2019 annual report (total revenue of $11.555 billion, with 60% attributable to laboratory testing services), the revenue generated from its testing business amounted to $6.933 billion. Thus, Quest Diagnostics remains the undisputed leader in the third-party laboratory testing market.

Unit: million USD (diluted earnings per share in USD)

Currently, Quest operates a fleet of 4,000 specialized transport vehicles and 23 aircraft. The company employs over 600 individuals with doctoral or master’s degrees, holds more than 1,000 patents, and has over 500 patent applications pending. Quest also maintains more than 7,000 patient service locations, including 2,275 company-owned patient service centers. It performs 175 million tests annually, covering approximately 90% of the insured population in the United States.

In 2019, pursuant to the Protecting Access to Medicare Act (PAMA), the Centers for Medicare & Medicaid Services (CMS) issued a revised fee schedule for clinical laboratory testing services provided under Medicare in 2018. In 2018 and 2019, CMS reduced reimbursement rates for clinical laboratory tests and plans to further reduce them by approximately 10–20% over the next 20 years.

PAMA calls for further revisions to the Medicare Clinical Laboratory Fee Schedule after 2020, based on future market rate surveys, and plans to cap annual reimbursement reductions at 15% from 2021 to 2023.

It is widely believed in the industry that PAMA will have an overall negative impact on the clinical laboratory testing sector. However, the scope of PAMA’s impact certainly includes hospital-affiliated laboratories as well. This presents an opportunity for Quest Diagnostics.

On the other hand, hospital-affiliated laboratories have historically been able to secure higher reimbursement rates from commercial insurance providers, which remains one of the primary reasons why third-party testing institutions have been unable to capture their market share.

However, this situation is changing, driven by the expansion of service networks by third-party clinical laboratory providers and their collaborations with commercial health insurers. Currently, there is a trend among commercial health insurers to shift their focus toward these lower-cost third-party laboratories.

If managed properly, third-party testing providers such as Quest Diagnostics can leverage their industry-leading, high-quality, and cost-effective laboratory services to capture greater market share from hospital-affiliated laboratories, thereby reshaping the current market landscape.