Will the $9B-Backed Fitness Sector—Led by Keep—Become the Next Big Health Traffic Gateway?

Many past events are difficult to hypothesize about.

For instance, in 2014, Wang Ning, a student at Beijing Information Science and Technology University, stumbled upon the business opportunity in fitness while “healing” from a breakup through weight loss during his graduation season. Without this experience, would Keep, which has since completed seven rounds of financing totaling over RMB 1.8 billion, exist as it does today?

Like Wang Ning, hundreds of other entrepreneurs, including Shen Bo and Liang Feng, have entered the sports and fitness startup sector through various circumstances—or, more accurately, have joined a game driven by capital and policy support. According to statistics from the VCBeat Orange Database,Over the past seven years, there have been 151 financing and investment events in the primary market of the sports and fitness sector. More than a hundred startups have secured funding, with 147 investment institutions—including Hillhouse Capital, Sequoia Capital, and Tencent—collectively investing over RMB 6 billion.

Keep, founded by Wang Ning; Codoon, founded by Shen Bo; and Joyrun, founded by Liang Feng, have currently surged to the forefront of the industry. For other players in this sector, however, securing financing has become increasingly difficult over the past two years. As the tailwinds fade, this finite game appears poised to crown its winners.

The essence of this game is that, in a consumer society constructed by the symbolic order, people are compelled to move continuously from one commodity to another, with “sports,” “fitness,” and “beauty” being the categories currently on display in the shop window.

In 2011, as public attention was focused on the “Hundred Groupons War” in the group-buying sector, headlines were repeatedly dominated by news of successive funding rounds for companies such as Meituan, Dianping, and Lagou. Outside the spotlight, a sports social platform named Codoon quietly secured RMB 22 million in angel investment from Shanda Group. Its development philosophy was to “disrupt traditional sports through the Internet.” This was a substantial sum; measured against prevailing price levels at the time, it could have purchased more than ten residential properties in Beijing or Shenzhen.

Since Shanda’s investment in Codoon, the sports and fitness sector remained quiet for several years before finally entering its period of explosive growth.

In 2014, with the initial public offerings of internet companies such as JD.com, Alibaba, and Sina Weibo, people’s entrepreneurial passion was ignited.

In October of that year, the State Council issued the “Several Opinions on Accelerating the Development of the Sports Industry and Promoting Sports Consumption,” which set a target to achieve “500 million sports participants and a sports industry output value of RMB 5 trillion” by 2025.

Beyond policy guidance, the O2O model is also breaking down barriers and gaining widespread popularity across major industries.TV hosts will no longer pronounce O2O as “O-two-O,” and executives of some traditional enterprises will no longer start their speeches by saying “zero-two-zero.”

Online-to-Offline (O2O): Bridging the online and offline worlds by comprehensively integrating all industries, it has become the most popular approach in the wave of mass entrepreneurship and innovation.

The entrepreneurial fever has also spread to the sports and fitness sector.

In the traditional fitness and exercise sector, the predominant model consists of large-scale gyms that charge members annual fees. The industry as a whole remains quite traditional, creating an urgent need for the introduction of new technologies and innovative concepts.

In 2014, 16 companies secured financing, including Keep, founded by Wang Ning, who had gone through a breakup during his graduation season. He raised RMB 3 million from Zehou Capital.

Of the 16 companies that secured financing, it is more accurate to describe them as 15 apps rather than 16 distinct enterprises. Apart from Qingcheng Technology, which focuses on digitalizing the fitness industry, the other 15 are all consumer-facing apps.

In terms of market entry models, some focus on sports venue reservations, others on pedometers, and still others on offline events and competitions; the remainder are all engaged in mobile fitness.

In addition to Keep, other industry leaders such as Joyrun and Codoon Sports also secured financing in 2014. Codoon Sports raised $30 million from SIG China and SoftBank China, while Joyrun received an investment in the millions of RMB from Qihoo 360.

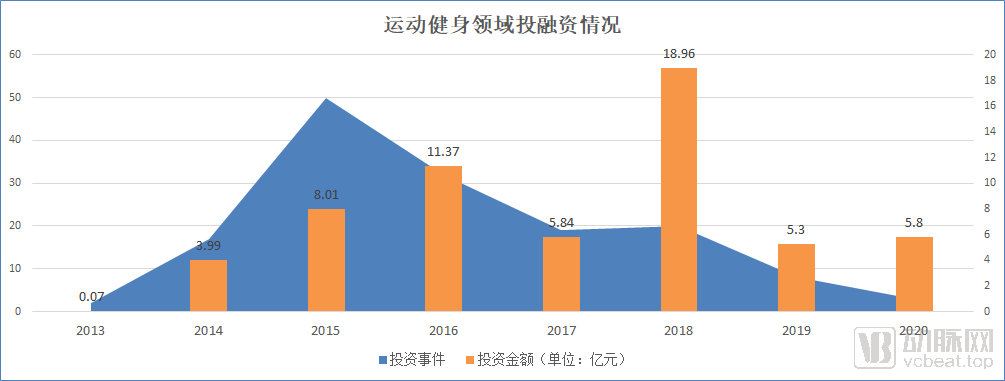

By 2015, this sector had become a hotbed of investment activity. There were 50 financing and investment deals, with nearly 40 companies raising approximately RMB 801 million. Companies such as Keep, Quan Cheng Re Lian, and Jian Mei Le secured two or more rounds of funding that year.

(Note: In the financial statistics, financing amounts denominated in US dollars are converted into RMB at the current exchange rate. Financing rounds with no disclosed amount are counted as 0. When only the order of magnitude is disclosed, “several million” is counted as 1 million, “tens of millions” as 10 million, and “hundreds of millions” as 100 million. Please note that, based on this calculation method, the actual total financing amount in the industry will be greater than or equal to the figures presented in this article.)

Subsequently, the fervor in this field has continued. In 2016, there were 32 deals totaling RMB 1.137 billion; in 2018, 20 deals totaling RMB 1.896 billion; and in 2020 (data as of May 19), 3 deals totaling RMB 580 million.

After years of development, looking back at this industry, we can clearly identify several key milestones.

Prior to 2014, the entire industry was in an exploratory phase. During this period, the number of mobile apps was limited, yet the market held immense potential. On the demand side, users had limited awareness of fitness and lacked strong demand. In terms of financing, investment scales were small, and capital was scarce. Regarding product development, app functionalities were basic and required further expansion.

From 2014 to 2019, the industry entered a period of explosive growth. During this time, mobile applications emerged in rapid succession, leading to intense competition. On the demand side, rising health and fitness awareness drove a surge in the user base. In terms of capital investment, substantial funds flowed into the market, fueling fierce competition among investors. Regarding product development, functional modules were expanded and continuously refined.

By 2019, the industry had entered its maturity phase. During this period, leading companies emerged, capturing significant market shares as the market approached saturation. On the demand side, fitness awareness became deeply ingrained among consumers, driving steady growth in demand. In terms of financing, the investment boom cooled down, with capital increasingly concentrating on top-tier players, making it more difficult for newly established enterprises to secure funding. Regarding products, functionalities were continuously optimized, and numerous new business models emerged.

Over the past two years, financing events in the industry have declined sharply, with only a few startups securing funding as capital has concentrated among top-tier players. This indicates that the industry has entered a mature phase of steady growth, shifting to a saturated market where leading players will face a decisive showdown.

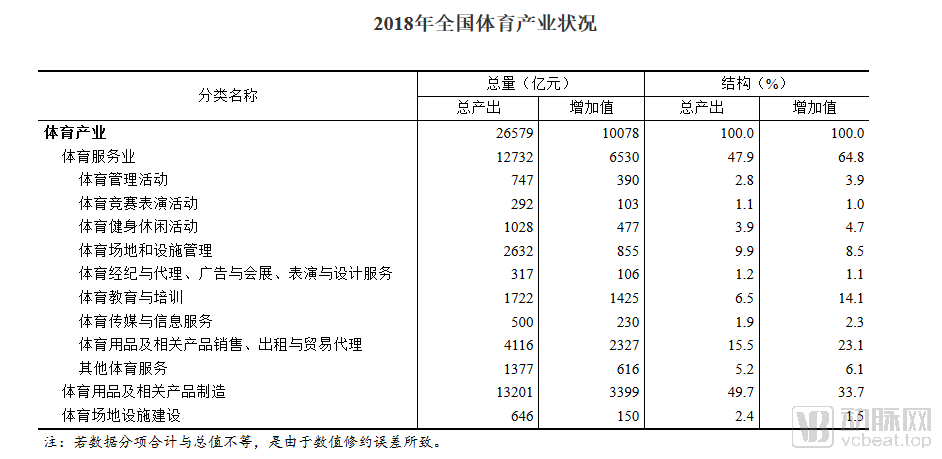

In 2014, when the fitness and exercise sector began to gain momentum, the market size (total output) of China’s sports industry stood at RMB 1.3575 trillion. By 2018 (with data disclosed in January 2020), the scale of China’s sports industry had reached RMB 2.6579 trillion, nearly doubling its market size within five years.

(Page source: Screenshot from the National Bureau of Statistics website)

The number of people who regularly participate in physical exercise is expected to reach 440 million by 2020.

Benefiting from the industry’s rapid growth, its “disruptors” have also grown substantially.On May 19, 2020, Keep secured $80 million in its Series E funding round, with its valuation entering the unicorn ranks.

In the broader fitness industry, well-funded and powerful players can currently be divided into two major categories. One category consists of online-focused players whose core business revolves around internet-based tools and products, represented by Keep, Joyrun, and Codoon. The other category comprises offline-focused players primarily engaged in physical operations, exemplified by LeFit, Supermonkey, and Liking Fit. Today, with technology clusters represented by mobile internet having become industry infrastructure, both types of players have successfully integrated online and offline operations. Nevertheless, their development paths and current business focuses remain markedly different.

Comparison of Strengths Between Two Types of Players

As can be seen from the chart, these players have reached the late stages of financing, with cumulative funding amounts ranging from hundreds of millions to over a billion yuan. The investment institutions behind them are almost exclusively star-studded capital firms.

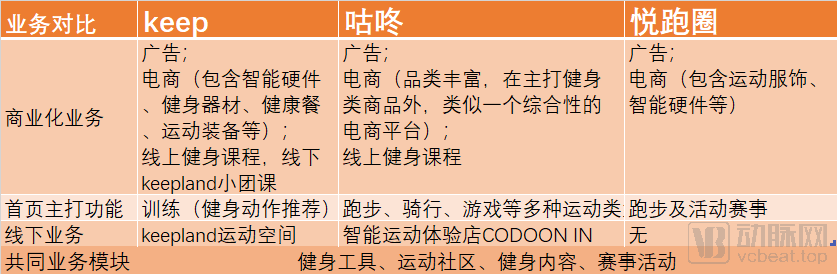

In terms of business model, Online-type players started as internet-based fitness tools and gradually evolved into comprehensive sports and fitness platforms covering workout tutorials, e-commerce, events and competitions, and offline venues.

(Source: Author’s product observations of three apps)

As can be seen from the chart above, the three companies are highly similar in their core businesses but differ slightly in product positioning. Keep focuses more on providing users with comprehensive fitness courses. While Codoon and Joyrun have similar core businesses, they still exhibit differences, primarily in their target user groups. Codoon targets users who enjoy various types of sports, aiming to provide an intelligent sports platform offering diverse workout options for the general public. In contrast, Joyrun targets running enthusiasts, striving to create a professional app dedicated to running.

For Offline-type players, the business primarily focuses on offline physical operations, based on the upgrading, iteration, and intelligent transformation of traditional gyms.

Supermonkey, which specializes in "showcase-style" gyms in key cities, is located in commercial hubs in city centers. It focuses on user experience at both physical and psychological levels. Currently, it has entered nine cities and operates on a pay-per-session reservation model for users.

Leke Fitness has entered eight cities across China, with over 450 stores. Most of its locations are situated in residential communities, near shopping malls and supermarkets, and around office buildings, operating on a 24-hour basis. The company plans to open 5,000 stores nationwide within the next three years.

Likingfit operates 24-hour smart gyms, adopting a business model that combines an online fitness app with offline internet-enabled smart gym facilities. Targeting white-collar workers and young users as its primary demographic, it provides on-demand fitness services to users at any time.

In summary, judging from the development logic of the two types of players currently, more efficient connectivity between online and offline channels has become a major trend. The ultimate winners are likely to be those who can integrate all scenarios and truly achieve a closed-loop business model.

In recent years, capital injection has played an indispensable role in the rapid expansion of the sports and fitness industry.

(Number of Transactions by Institutions in the Sports and Fitness Sector)

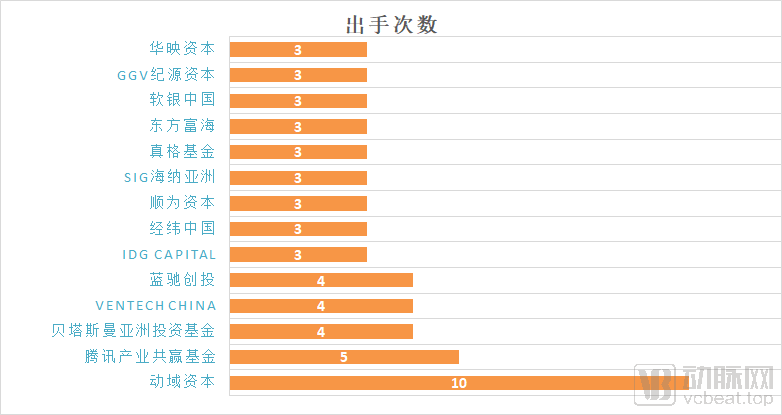

As shown in the chart above, major star venture capital firms have flocked to this sector, with SoftBank China, Matrix Partners China, and Tencent each making three or more investments. As financing rounds progress to later stages, these institutions are likely to make larger-scale investments, going “all in” to bet on the few ultimate winners.

Taking the development of Peloton, a unicorn in the U.S. sports and fitness sector, as an example. Prior to Peloton’s rise, the United States already had a highly mature fitness market, dominated by three primary models: traditional large-scale gyms, boutique fitness studios, and O2O (online-to-offline) gyms.

Among these players, Peloton has emerged as a standout by implementing refined operations in the fitness industry. The Peloton platform offers a vast library of professional video content across various disciplines, such as yoga, running, and indoor cycling. Users can subscribe via monthly or annual fees to access on-demand workouts from home. This model has gained significant popularity among younger demographics, allowing them to exercise on stationary bikes or treadmills without leaving home. The equipment connects directly to live-streamed classes, enabling real-time interaction with celebrity instructors, which saves time and money while enhancing workout efficiency. The emergence of the Peloton model serves as an optimal complement to the traditional fitness landscape, which has historically been dominated by brick-and-mortar gyms.

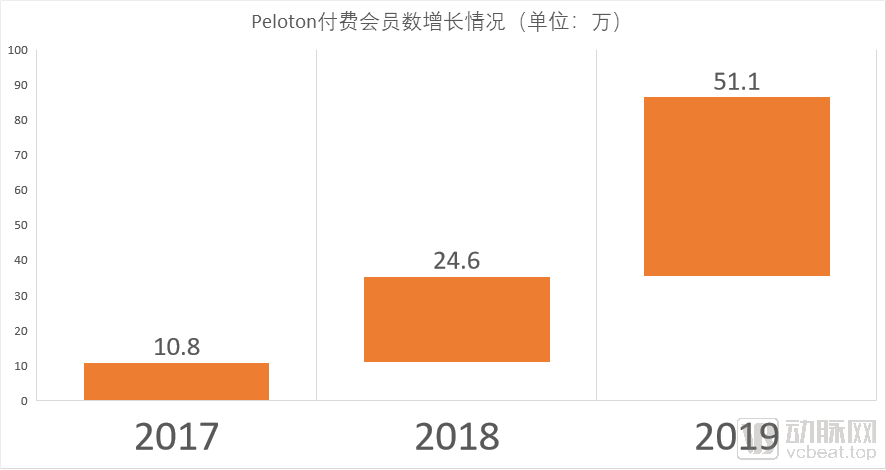

(Data source: Peloton IPO filing)

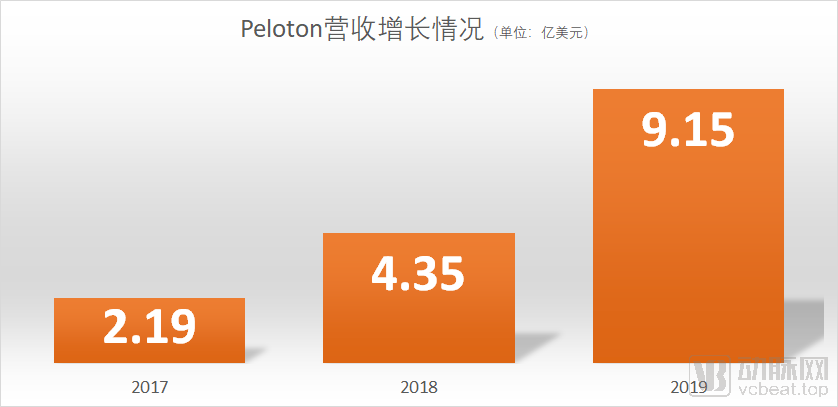

(Data source: Peloton IPO filing)

Revenue and paid membership figures indicate that Peloton has maintained steady growth over the past three years, with a compound annual growth rate (CAGR) exceeding 100%.In September 2019, Peloton went public on the Nasdaq. As of the market close on May 21, its latest market capitalization stood at $12.8 billion, propelling it into the ranks of super unicorns.

Peloton’s success has been driven by two core strategic pillars: its technology and its operating model.

Technologically, Peloton is a pioneer in driving fitness through mobile internet technology, creating immersive experiences that users love by integrating the physical and digital worlds. It has rapidly expanded its market through data-driven marketing and education-based approaches, building cumulative word-of-mouth among its user base. According to its prospectus, the number of users of its mobile fitness products increased from 35,135 as of June 30, 2016, to 511,202 as of June 30, 2019, representing a compound annual growth rate of approximately 144.1%.

In terms of its operating model, Peloton runs a vertically integrated, precision-targeted community that is difficult to replicate, alongside an addictive fitness experience for users. To meet the comprehensive needs of its members, Peloton cultivates a highly targeted community with strong engagement; loyal users continuously drive organic growth through word-of-mouth, expanding the community’s reach. Peloton’s commercial activities are deeply embedded within this user-centric community ecosystem. As the fitness community undergoes continuous fission, growth, and expansion, Peloton’s business has seen steady and significant success.

Peloton cannot be easily replicated in China. Nevertheless, Peloton offers a broad insight: China’s fitness market has substantial room for improvement across online and offline channels, as well as in fitness scenarios, particularly in the development of business models.

According to China’s “Healthy China 2020” Strategic Research Report, 83.8% of Chinese residents aged 18 and above never engage in physical exercise, while only 11.9% exercise regularly (defined as exercising more than three times per week, with each session lasting at least 10 minutes). This indicates substantial growth potential in the sports and fitness sector. With core demand and consumer awareness in place, coupled with a high industry ceiling, the sports and fitness field is poised for promising future prospects.

Even though the market has entered a mature phase, with incumbent players becoming the main force in the market, the industry will continue to grow, and the user base will further expand.

However, based on existing business models, current market players are all constrained by certain bottlenecks. Take Keep as an example: according to media reports, Keep’s revenue was projected to reach RMB 1 billion in 2019, with income from its sports product category accounting for more than half of the total revenue.

If these sports and fitness platforms with massive traffic open up their boundaries, expanding from sports and fitness to sports health and then to overall wellness, they will quickly break through current bottlenecks and raise the ceiling for future growth.

The basis for this argument lies in the fact that the user profiles of these sports and fitness platforms align closely and precisely with the target users of internet medical health platforms.

The user profile of the former consists of individuals who are proficient in using internet tools and aspire to pursue sports, fitness, and a healthy lifestyle, while the latter aims to cultivate and serve a group of people within the innovative medical service network.

(Source: Keep 2020 Brand White Paper)

The distance from fitness and general wellness to niche sectors within the broader health industry—such as health insurance, internet healthcare, and health management—is remarkably short. With hundreds of millions of users currently at their disposal, aren’t sports and fitness platforms precisely the user base that innovative medical services and payment models are most eager to reach and most likely to acquire? Aren’t these platforms the most promising entry point for traffic in the broader health sector, both in the present and in the future?

Based on the varying nature of traffic, healthcare traffic entry points can be categorized into the following four types: general-purpose traffic entry points represented by super apps, such as Alipay, WeChat, and Meituan; search-based entry points represented by search engines, such as Baidu and Sogou; content-driven entry points represented by vertical healthcare platforms, such as Chunyu Doctor; and scenario-based long-tail medical demand entry points facilitated through cross-industry collaborations, such as pharmacies and health examination centers.

Currently, competition for traffic entry points is concentrated on general traffic portals, search engines, and content platforms. These mature markets are fiercely competitive, resulting in high customer acquisition costs per user. In contrast, cross-industry scenario-based entry points remain a blue ocean market, with only a small fraction of healthcare needs within these scenarios having been tapped.

Last year, the Alibaba Group identified health checkup providers as a key traffic entry point, investing RMB 7.265 billion to become the second-largest shareholder in Meinian Onehealth Healthcare Holdings Co., Ltd., and spending $1.5 billion to fully privatize iKang Guobin, another major player in the health checkup industry.

In the context of sports and fitness, users have clear and strong demands for health-related services. This sector naturally aligns with downstream areas such as health management and light consultations. Moreover, traffic on sports and fitness platforms has reached hundreds of millions, demonstrating a significant traffic effect.

Fitness platforms such as Codoon and Keep command hundreds of millions of users. If they can expand from fitness and exercise into healthcare, becoming a traffic gateway for the broader health industry, their growth prospects would be exceptionally promising. In terms of revenue, selling sports equipment is not in the same league as selling pharmaceuticals, insurance, or medical services. Should these fitness platforms cross over into areas such as online mutual aid, health insurance, health management, and internet-based healthcare, their business operations could experience exponential growth.

In fact, some players have made such attempts.

In June 2019, Keep made an initial foray into the pharmaceutical sector by partnering with Voltaren, a topical analgesic used to alleviate pain associated with muscle and soft-tissue injuries—such as sprains, strains, bruises, and overuse injuries—as well as lower back pain and joint pain. Media reports at the time indicated that the collaboration was quite successful.

However, there have been no further updates from Keep in the healthcare sector since then.

In a recent news report, Keep founder Wang Ning revealed, “Keep is benchmarking itself against Nike.”