Fudan Zhangjiang Biopharmaceutical Advances Toward STAR Market Listing with Focus on Photodynamic Therapies

On April 27, the Listing Committee of the STAR Market approved the A-share issuance and listing of Shanghai Fudan-Zhangjiang Bio-Pharmaceutical (1349.HK) on the STAR Market. Following this successful approval, Fudan-Zhangjiang will become a dual-listed “A+H” company. In recent years, Fudan-Zhangjiang has garnered favor in the capital markets for two main reasons: first, the endorsement from its largest shareholder, Shanghai Pharmaceuticals; second, as a growth-oriented enterprise in the field of photodynamic therapy drug development, it is more sought after by investors than value-oriented companies.

Historical Stock Price Chart of Fudan-Zhangjiang | Image Source: Tonghuashun

Shanghai Fudan-Zhangjiang Bio-Pharmaceutical has experienced two bull market runs. The first occurred after a period of consolidation from 2010 to 2013, when its stock price surged from RMB 2 to RMB 12 in 2015, fueled by the “leveraged bull market,” representing a six-fold increase over slightly more than two years. The second took place in 2018, when the stock entered a year-long consolidation phase, followed by a two-fold rally in the first four months of 2019.

So, with Shanghai Fudan-Zhangjiang Bio-Pharmaceutical’s imminent listing on the STAR Market, can it once again deliver better returns to investors?

Shanghai Fudan-Zhangjiang Bio-Pharmaceutical was established in 1996 through joint investments by Fudan University, Shanghai Pudong New Area Economic and Trade State-owned Assets Management Co., Ltd., and Shanghai Zhangjiang High-Tech Development Promotion Center, among others. In 2002, the company listed on the Growth Enterprise Market of the Hong Kong Stock Exchange, and in 2013, it transferred its listing to the Main Board of the Hong Kong Stock Exchange.

Fudan-Zhangjiang has been dedicated to the research and development of novel drugs, such as photodynamic therapy agents. Currently, it has three independently developed and marketed products: topical aminolevulinic acid hydrochloride powder for external use (brand name: Aila), based on its photodynamic technology platform; long-circulating doxorubicin hydrochloride liposome injection (brand name: Libo Duo), an anti-tumor drug based on its nanotechnology platform; and hemoporfin for injection (brand name: Fumeida).

Currently, Shanghai Fudan-Zhangjiang Bio-Pharmaceutical holds equity stakes in six subsidiaries, engaging in businesses such as the research and development, and sales of innovative drugs and medical devices.

In 2007, the Company’s first subsidiary, Taizhou Fudan-Zhangjiang, was established, serving as a key production base for its innovative drugs. Additionally, regarding Demed Clinic Alliance, a nationwide dermatology and aesthetic clinic chain invested in and established in 2015, Shanghai Fudan-Zhangjiang Bio-Pharmaceutical announced in February 2019 its plan to sell a 30.04% equity interest in the entity to Rongke Rongtuo Health Data Industry Equity Investment Partnership (Limited Partnership) for RMB 16.52 million.

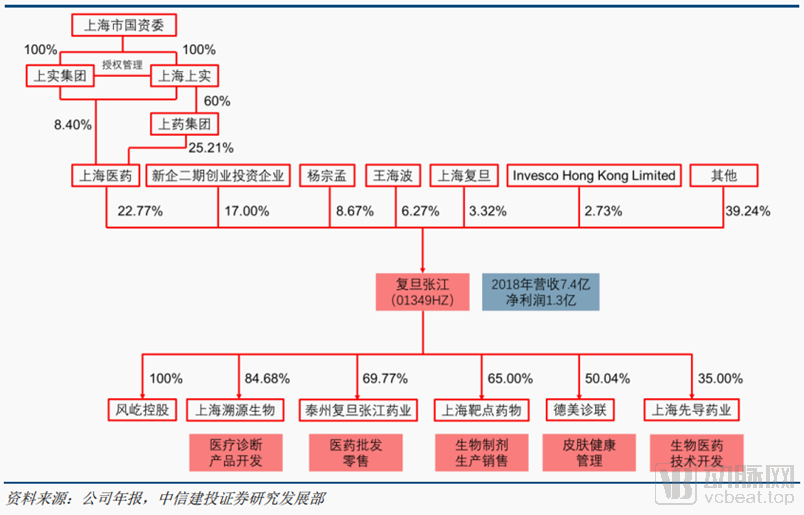

Here, it is essential to highlight the shareholding structure of Shanghai Fudan-Zhangjiang Bio-Pharmaceutical. The actual controller behind the company is the Shanghai State-owned Assets Supervision and Administration Commission (Shanghai SASAC). Currently, the major shareholders include Shanghai Pharmaceuticals (22.77%), New Enterprise Phase II Fund (17.00%), Yang Zongmeng (8.67%), and Wang Haibo (6.27%).

As can be seen from the shareholding structure diagram, no single shareholder of Shanghai Fudan-Zhangjiang Bio-Pharmaceutical holds more than 30% of the company’s total share capital. There is no controlling or actual control relationship among the company’s shareholders, nor is there any common controlling shareholder or actual controller.

Following Shanghai Fudan-Zhangjiang Bio-Pharmaceutical’s listing on the STAR Market through a share issuance, the equity stakes of existing shareholders will be further diluted. This means that no single shareholder will hold more than 30% of the company’s total share capital, thereby precluding any decisive influence over corporate decision-making.

To this end, the Company also discloses in its prospectus that there is a risk that the absence of an actual controller may lead to instability in corporate governance or reduced decision-making efficiency, thereby causing the Company to miss business development opportunities and resulting in fluctuations in its production, operations, and operating performance.

However, this does not mean that Shanghai Fudan-Zhangjiang Bio-Pharmaceutical lacks investment value. In recent years, the number of A-share listed companies without actual controllers has gradually increased, with typical examples including Vanke, Yunnan Baiyao, and Gree Electric Appliances, which came under the control of Hillhouse Capital in 2019. Conversely, investors may even benefit from aggressive equity stakes taken by major shareholders or from high dividend payouts.

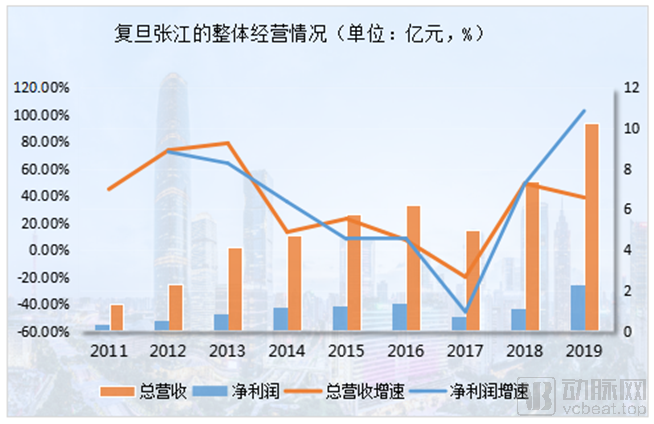

Based on operational performance since 2011, the development of Shanghai Fudan-Zhangjiang Bio-Pharmaceutical can be broadly divided into three stages:

Phase I: Rapid Growth Period. Performance growth from 2011 to 2016 was highly stable. Total operating revenue increased from RMB 134 million in 2011 to RMB 622 million in 2016, while net profit rose from RMB 31 million to RMB 139 million. The compound annual growth rates (CAGR) for total revenue and net profit over this six-year period were 29.16% and 28.41%, respectively.

Phase II: Period of Slowing Performance. In 2017, impacted by the “Two-Invoice System” policy, distributors of the core product Libaoduo were unable to fully comply with exclusive distribution agreements, leading to a decline in sales. Total annual revenue amounted to only RMB 498 million, representing a year-on-year decrease of 19.97%, while net profit stood at merely RMB 75.28 million, marking a significant year-on-year drop of 45.72%.

Phase III: Recovery and Growth Phase. Fortunately, in 2018, the company decided to terminate the exclusive general distribution agreement and reestablished a new sales and promotion team for oncology drugs, resulting in an 85% year-on-year increase in Libaoduo’s sales revenue, with its share of total revenue reaching 36%.

In 2019, Shanghai Fudan-Zhangjiang Bio-Pharmaceutical delivered impressive financial results, with total annual revenue reaching RMB 1.029 billion, a year-on-year increase of 38.75%, and net profit amounting to RMB 227 million, a year-on-year surge of 102.76%, marking its best performance since going public.

Shanghai Fudan-Zhangjiang Bio-Pharmaceutical’s Performance Since 2011 Source: Company Financial Reports

Behind the performance growth of Shanghai Fudan-Zhangjiang Bio-Pharmaceutical lies, on one hand, the support from its four major R&D platforms, including the photodynamic technology platform, nanotechnology platform, genetic engineering technology platform, and oral solid dosage form technology platform; on the other hand, it is highly dependent on three core products.

AiLa is the world’s first photodynamic therapy drug for the treatment of condyloma acuminatum, filling a long-standing gap in effective therapies for lesions in special anatomical sites (intraurethral, intrarectal, and cervical areas). According to data from Menet, AiLa holds a 60% market share in China. Since its launch in 2007, cumulative sales have reached 4.173 million units, with total revenue exceeding RMB 2.323 billion.

Libaoduo is the first domestic generic version of Doxil, the world’s first anticancer liposomal drug, and is indicated for the treatment of various cancers, including breast cancer, ovarian cancer, and multiple myeloma. Since its market launch in 2009, it has achieved cumulative sales of 612,000 vials, with total sales revenue exceeding RMB 2.157 billion.

Fumedah is the world’s first photodynamic therapy drug specifically indicated for port-wine stains, classified as a Class 1.1 chemical drug. The FDA has recognized it as the first drug to be submitted for approval for the treatment of port-wine stains. Since its market launch in 2017, cumulative sales have reached 45,200 units, with total revenue exceeding RMB 169 million.

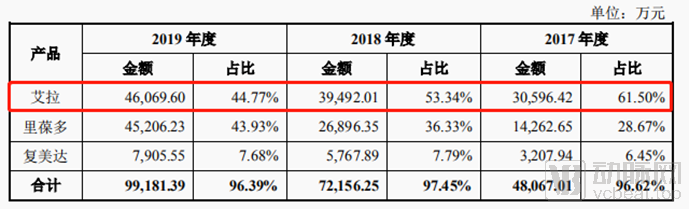

Sales Performance of Core Products Source: Prospectus

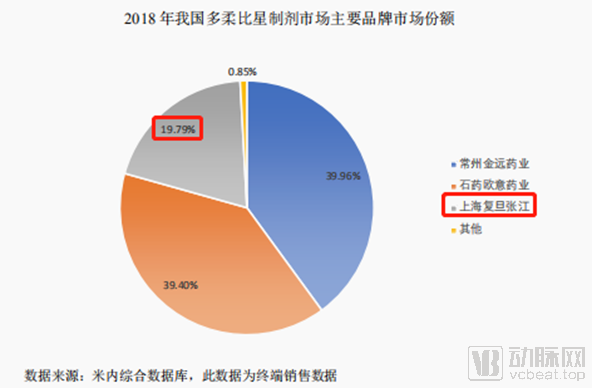

In terms of product structure, Aila’s revenue share from 2017 to 2019 was 61.5%, 53.34%, and 44.77% respectively, showing a continuous downward trend; conversely, Libo Duo’s revenue share has steadily increased over the past three years, but it faces market competition from CSPC Ouyi’s Duomeisu and Changzhou Jinyuan Pharmaceutical’s Lixing; meanwhile, the new product Fumeida has not yet achieved rapid volume growth.

As these three drugs account for 96% of the company’s revenue, its gross profit margin and net profit margin have remained stable at 91% and 20%, respectively, over the years.

However, the company’s product portfolio is relatively narrow, and its revenue model is highly concentrated. Although short-term performance growth is significant, a decline in sales of any single product would have a substantial impact on overall results.

In the first quarter of 2020, due to the impact of the COVID-19 pandemic, the end-user consumption of the company’s main products was significantly affected, declining by more than 50% year-on-year. If no new products are introduced in a timely manner to fill the gap, the company’s future performance will not be effectively guaranteed.

For pharmaceutical R&D companies to achieve stable performance growth, sustained investment in research and development is indispensable.

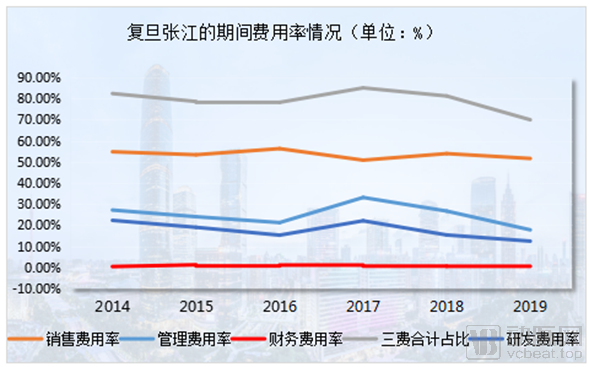

However, Shanghai Fudan-Zhangjiang Bio-Pharmaceutical’s R&D investment performance has been mediocre over the past four years. From 2016 to 2019, the company’s R&D expenditures were RMB 112 million, RMB 112 million, RMB 109 million, and RMB 130 million, respectively, with R&D expense ratios of 17.51%, 21.99%, 14.65%, and 12.68%, respectively. R&D expenses did not increase in line with total revenue; instead, they exhibited a continuous downward trend.

Expenditure Profile of Fudan-ZhangjiangSource: Company Financial Reports

The primary reason lies in the company’s persistently high selling expense ratio. Since 2014, Shanghai Fudan-Zhangjiang Bio-Pharmaceutical’s selling expense ratio has remained at approximately 50%, significantly exceeding the industry average of 44%. Moreover, total selling expenses over the past four years amounted to RMB 1.525 billion, which is 3.32 times the RMB 463 million spent on research and development during the same period.

Undoubtedly, the disproportionately high proportion of sales expenses in revenue has constrained the company’s investment in research and development, leading to weak development capabilities and a lack of competitive new products.

Moreover, the company’s asset-liability ratio has been rising steadily for years. The debt ratios from 2017 to 2019 were 22.06%, 35.06%, and 40.37%, respectively, reflecting a very rapid growth rate. In addition, its accounts receivable turnover ratio is below the average level of comparable listed companies.

Therefore, a strategy that can effectively address these “hidden concerns” is to achieve a listing on the STAR Market as soon as possible.

As disclosed by Shanghai Fudan-Zhangjiang Bio-Pharmaceutical, the proposed public offering will consist of no more than 120 million shares, representing not less than 11.51% of the company’s total share capital upon completion of the issuance. The fundraising target is RMB 650 million, of which RMB 230 million will be allocated to the “Hemoporfin U.S. Registration Project,” RMB 240 million to the “Sustainable Development Project for Innovative Biopharmaceutical R&D,” and RMB 180 million to the “Acquisition of Minority Interests in Taizhou Fudan-Zhangjiang Project.”

On July 17, 2019, Fudan-Zhangjiang had already completed the acquisition of 100% equity interest in Taizhou Fudan-Zhangjiang ahead of schedule. Consequently, the company is poised to reallocate its use of funds and increase investment in new drug research and development projects.

Undoubtedly, the company’s long-term competitiveness hinges on the successful R&D of new products and their subsequent industrialization and commercialization.

To this end, Shanghai Fudan-Zhangjiang Bio-Pharmaceutical has been actively expanding the indications of AiLa for glioma, acne, and cervical diseases associated with HPV infection in recent years. Meanwhile, Liboduo and Fumeida are also undergoing registration in the United States, with prospects for future expansion into overseas markets.

Although the company terminated the development of three drug candidates in 2019, it still has 11 products in preclinical research and clinical trial stages. Predominantly innovative drugs, these candidates cover multiple therapeutic areas, including oncology, hepatobiliary diseases, and autoimmune disorders. If successfully launched, they will create new revenue and profit streams for the company.

Based on the foregoing analysis, it is evident that despite Shanghai Fudan-Zhangjiang Bio-Pharmaceutical’s historically strong financial performance, its operations are heavily reliant on a limited portfolio of products. Coupled with elevated selling expenses, modest R&D investment, and a rising debt-to-asset ratio, these factors have placed considerable operational pressure on management. This fundamentally explains the company’s mediocre stock price performance in recent years.

However, from a valuation perspective, as of the market close on May 12, Shanghai Fudan-Zhangjiang Bio-Pharmaceutical had a total market capitalization of RMB 4.467 billion, net profit of RMB 227 million, and a price-to-earnings (P/E) ratio of 19.7x, which is at a historically low level. Compared with its A-share peers Betta Pharmaceuticals (178x) and Kanghong Pharmaceutical (43.3x) during the same period, the company is undoubtedly more undervalued.

From the perspective of return on equity (ROE): an ROE of 10%-15% indicates an average company, 15%-20% signifies an outstanding company, and 20%-30% denotes an excellent company.

Shanghai Fudan-Zhangjiang Bio-Pharmaceutical maintained a stable ROE of 17% from 2013 to 2016. After a sharp decline in 2017 due to the impact of the “Two-Invoice System” policy, the ROE surged to 24.41%, highlighting the company’s growing potential and investment value.

Source: Company Financial Report

Overall, Shanghai Fudan-Zhangjiang Bio-Pharmaceutical is indeed a fast-growing enterprise. However, when investing in growth stocks, “market timing” is crucial. As for whether it is currently an appropriate time to enter, one must still observe the impact of the pandemic, the company’s performance growth, and conduct more in-depth research and tracking of product development progress to achieve precise investment decisions.