Where Did the Up to 50% Price Reduction from China's Three-Stage High-Value Medical Consumables Reform Ultimately Flow?

The video of the volume-based procurement negotiations between AstraZeneca and the National Healthcare Security Administration in 2019 remains vivid in memory. Within less than half a year, policies on medical consumables have come thick and fast, and pioneers in reform zones have entered the deep-water zone.

“With pharmaceuticals leading the way, reforms in medical consumables have progressed even faster,” an entrepreneur with years of experience in the consumables supply chain told VCBeat. “The ultimate goal of consumables policies is very clear, yet the objectives at each stage are somewhat ambiguous. It is like building blocks: sub-modules with diverse functions are assembled together to create something entirely new.”

There are three primary reasons for the policy focus on medical consumables. First, this is a vast market; in 2018, its size exceeded RMB 170 billion. Given the substantial daily usage by physicians, it is essential to ensure both reliable quality and reasonable pricing. Second, expenditures in this sector are closely tied to the national medical insurance fund; controlling high-value medical consumables is therefore critical to managing medical insurance costs. Third, the high gross margins in the medical consumables industry have attracted a large workforce, particularly among distributors. Data from 2015 shows that the total number of pharmaceutical and medical device distributors reached 2.8 million, compared to only 3 million physicians in the same year. The excessive number of distributors has driven up the prices of drugs and medical devices without generating corresponding real value.

Among medical consumables, high-value consumables—which accounted for 62.50% of the market with a size of approximately RMB 106 billion (2018 data)—have become the focal point of policy attention. This category covers a broader range of products, features continuous innovation, and is often associated with precision surgeries, thereby necessitating stricter regulatory oversight.

So, amid the wave of reforms, how will the entire high-value consumables supply chain change? And where should the participants go from here? To address these questions, VCBeat interviewed multiple consumables manufacturers and distributors, attempting to review the high-value consumables reforms in various provinces and cities in recent years and identify the future development direction of this market.

In early 2017, the State Council’s Office of Healthcare Reform, in conjunction with the National Health and Family Planning Commission and seven other departments, jointly issued a notice requiring medical institutions to take the lead in implementing the “two-invoice system” for drug procurement, aiming to reduce artificially inflated drug prices and alleviate the medication burden on the public.

This policy was met with widespread skepticism at its launch, and reality has proven the skeptics right: through tactics such as inflated pricing and hospital-pharma collusion, pharmaceutical companies and hospitals have been able to easily circumvent the revenue losses imposed on drug manufacturers by the Two-Invoice System.

"Xiang Zhuang performs the sword dance, but his intention is to assassinate Liu Bang."

In the aftermath, distributors were the most heavily impacted by this policy, particularly national-level distributors lacking direct ties to end-user hospitals, who were quickly forced out of the market amid these regulatory adjustments.

The Expansion Path of High-Value Consumables Policy Is Similar to That of Pharmaceuticals. After Witnessing the Substantial Achievements in the Pharmaceutical Sector, the Promotion of High-Value Consumables Has Swept Through Like Autumn Wind Clearing Fallen Leaves, Leaving Everyone in This Wave Feeling Insecure. Before Half of 2020 Had Passed, Numerous New Policies Had Already Emerged.

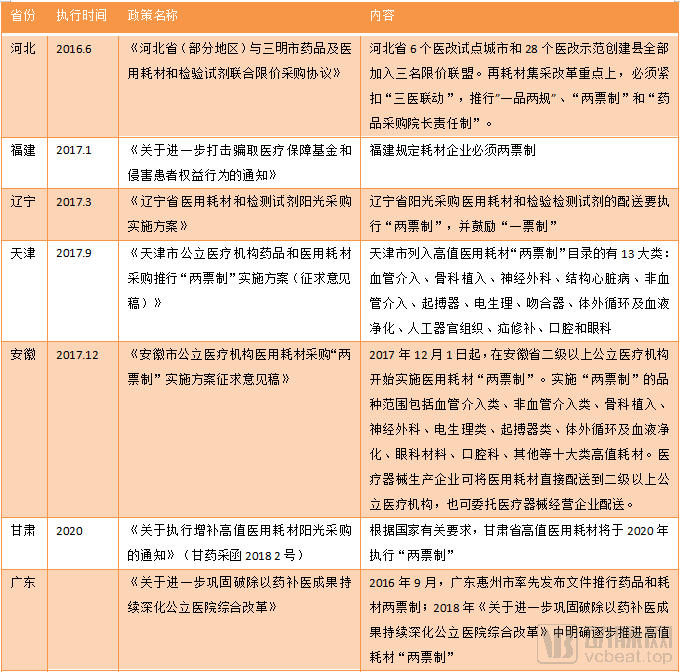

As of October 2019, a total of 25 provinces and municipalities had implemented the “Two-Invoice System” for medical consumables. Among them, 12 provinces—Inner Mongolia, Liaoning, Shaanxi, Anhui, Hubei, Jiangxi, Guizhou, Guangdong, Fujian, Hainan, Qinghai, and Tibet—had fully enforced the Two-Invoice System for medical consumables; six provinces, including Heilongjiang, Hebei, Shanxi, Henan, and Jiangsu, had implemented the system in selected pilot cities; seven provinces, namely Hunan, Guangxi, Zhejiang, Sichuan, Gansu, Ningxia, and Shandong, had issued relevant policy documents; only six provinces and municipalities—Beijing, Shanghai, Chongqing, Shandong, Jilin, and Xinjiang—had not implemented the Two-Invoice System.

Implementation of the Two-Invoice System in Selected Regions

For pharmaceutical and medical device distribution companies, revenue typically stems from product price differentials and manufacturer rebates. Under the Two-Invoice System, distributors positioned in the middle of the supply chain can neither capture product price differentials nor benefit from manufacturer rebates. However, distributors with established hospital and physician resources have been minimally affected; their only change is that their upstream suppliers have shifted from other distributors to pharmaceutical and medical device manufacturers.

Market restructuring means more opportunities. To seize more resources and enhance their competitiveness, downstream distributors have begun to explore ways to expand their value-added services in circulation. A Sichuan-based distributor handling TAVR products in Southwest China told VCBeat that they are striving to continuously optimize their distribution network, reduce logistics costs, and cultivate a team of sales professionals with specialized knowledge. These professionals help train hospital physicians on relevant products and undertake maintenance tasks for certain medical devices.

These distributors’ precautionary measures are not without merit. In the past, issues in circulation were often diluted across lengthy distribution chains. However, the “Two-Invoice System,” by tightening control over these chains, has caused such problems to accumulate entirely in the hands of pharmaceutical and medical device manufacturers and hospitals. Under these circumstances, distributors capable of resolving more issues for manufacturers and hospitals have a greater likelihood of survival.

Overall, the Two-Invoice System has not resolved the pricing issues of high-value medical consumables, nor has it eliminated the diverse promotional and bribery practices. Nevertheless, it has undoubtedly cleaned up the gray areas in distribution, making the entire supply chain for medical consumables more transparent.

On July 16, 2019, the Anhui Provincial Healthcare Security Administration, Health Commission, Department of Finance, and Drug Administration jointly issued the “Implementation Plan for Centralized Volume-Based Procurement and Negotiated Pricing (Pilot) of High-Value Medical Consumables in Provincial Public Medical Institutions in Anhui Province,” marking the commencement of volume-based procurement for high-value medical consumables. In the initial round of volume-based procurement, only orthopedic implants (spinal) and ophthalmic products (intraocular lenses) were included, with procurement volumes required to account for 70% and 90%, respectively, of the total purchases of high-value medical consumables by provincial public medical institutions in 2018.

Subsequently, provinces and municipalities such as Liaoning, Jiangsu, Shanxi, and Gansu launched volume-based procurement (VBP) of medical consumables in multiple cities. Meanwhile, Sanming City and its collaborative regions, the Beijing-Tianjin-Hebei region, and a coalition comprising Heilongjiang, Jilin, Liaoning, Inner Mongolia, Shanxi, and Shandong adopted an alliance model to procure consumables at uniform prices, thereby preventing price disparities across different regions. An increasing number of regions and a broader range of medical consumables have been incorporated into the scope of volume-based procurement.

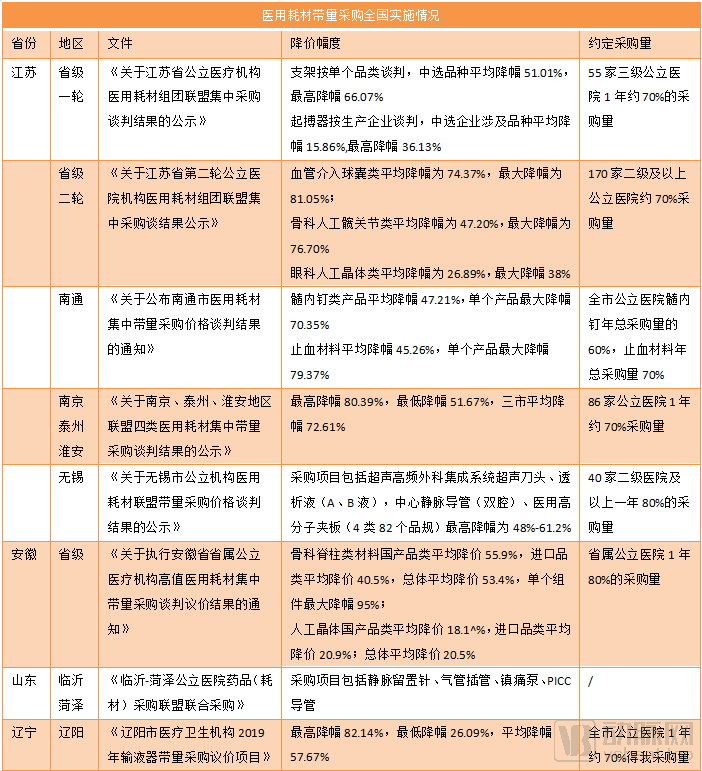

The impact of volume-based procurement is highly evident. In the race to secure near-monopolistic sales rights, numerous companies have been compelled to trade price for volume, ultimately driving the unit price of medical consumables down to an extremely low range.

Taking orthopedic spinal materials procured in Anhui Province as an example, the average price reduction for domestically produced categories was 55.9%, while that for imported categories was 40.5%, with the maximum price reduction for a single component reaching 95%. In Nantong City, Jiangsu Province, the average price reduction for hemostatic materials was 47.21%, with the maximum price reduction for a single product at 70.35%; the average price reduction for hemostatic materials was 45.26%, with the maximum price reduction for a single product at 79.37%.

Data source: WeChat Official Account “Medical Device Distributors Alliance”

In addition to the items listed in the table, volume-based procurement negotiations are also underway in Shanxi Province, the Beijing-Tianjin-Hebei region, and the provinces of Heilongjiang, Jilin, Liaoning, Inner Mongolia, Shanxi, and Shandong.

In addition to high-value consumables manufacturers being forced to bid at low prices, the operating margins of distribution enterprises have been further squeezed. Large medical device distribution companies possess greater survival advantages in an increasingly competitive environment.

The “Announcement of Winning Bidders for the Centralized Distribution Supplier Selection and Medical Consumables Supply Chain Extension Services [SPD] Project at Jinan Fourth People’s Hospital,” released in October 2019, serves as a prime example. In this tender for centralized distribution and SPD services, the winning bidders were subsidiaries of major medical distribution enterprises, including China Medical Device, Sinopharm Medical Device, Weigao, Shouhang, Shanghai Pharmaceuticals, and Ruikang.

Upon closer examination, the Fourth People’s Hospital of Jinan has imposed stringent requirements on the warehousing hardware facilities of distribution enterprises. Specifically, a warehouse with a total area of ≥10,000 m² earns 3 points, and a cold storage area of ≥750 m² earns another 3 points. Furthermore, to achieve full marks in the “product variety” category, bidders for medical consumables must offer no fewer than 4,000 distinct items.

Furthermore, the announcement disclosed the historical bid-winning records of the successful enterprises. These companies have previously secured centralized distribution rights for medical consumables at numerous Grade II Class A and Grade III Class A hospitals, with service contracts spanning five years and distribution volumes amounting to hundreds of millions of yuan.

It has become a trend for large-scale distribution enterprises to serve as service providers. Under the volume-based procurement (VBP) policy, the traditional role of “distribution” no longer exists; hospitals now prioritize only the supply chain capabilities of these distributors. In this context, small and medium-sized distributors face even greater survival challenges.

The ultimate target of volume-based procurement remains pharmaceutical and medical device manufacturers. Under these policies, the total market value of high-value consumables has shrunk rapidly. Most companies that failed to win bids have lost nearly their entire business in affected regions, leading to increased industry concentration. Furthermore, while companies could previously circumvent regulations through inflated invoicing under the “Two-Invoice System,” such tactics have now largely become ineffective—ultimately, prices for medical consumables have indeed come down.

In addition to the aforementioned changes, the volume-based procurement policy for medical consumables has given rise to new models during its implementation. The “One-Invoice System” is one such example.

Due to the significant price reductions following negotiations, some products no longer have room for rebates. As a result, most distribution companies have refused to engage in loss-making transactions and have relinquished their distribution rights. Meanwhile, many medical device and pharmaceutical companies have long opted for self-distribution. This means that there is effectively only one invoice during the product’s circulation process.

The national government supports the promotion of the single-invoice system and has issued corresponding policies to back it. Currently, 11 provinces and municipalities, including Fujian, Zhejiang, Hubei, Shanxi, Shaanxi, Tianjin, and Shandong, have explicitly encouraged the implementation of the single-invoice system.

However, the single-invoice system also brings many problems. After volume-based procurement, the amount to be settled between medical institutions and enterprises has increased significantly, while hospitals often delay payments for several months or even a year, which constitutes a substantial loss for medical device manufacturers.

In 2019, supporting policies for volume-based procurement were rolled out in quick succession. In Jiangsu Province, where these reforms have been most extensively implemented, the General Office of the Jiangsu Provincial Commission for Discipline Inspection of the Communist Party of China, the General Office of the Jiangsu Provincial Supervisory Commission, the Jiangsu Provincial Healthcare Security Administration, and the Jiangsu Provincial Health Commission jointly issued the Notice on Promoting Sunshine Procurement of High-Value Medical Consumables Across the Province. This notice imposed restrictions on payment timelines for medical and health institutions, requiring hospitals to transfer payments to the designated settlement account within 30 days after completion of delivery and acceptance. In the same year, Liaoning Province also established a prepayment revolving fund system for the basic medical insurance fund. The prepayment amount was set at no less than 30% of the procurement value in principle, and was to be disbursed in advance before the implementation of volume-based procurement results for medical consumables and in vitro diagnostic reagents.

Meanwhile, this document from Jiangsu Province also requires that all procurement expenses of public medical institutions across the province be settled through the provincial platform, so as to guide and promote online procurement via unified settlement, thereby achieving the integration of business flow, information flow, and fund flow on the provincial platform, referred to as the “integration of three flows.”

Through the new “integration of three flows” procurement platform, consumables manufacturers can receive payments directly from medical institutions and then pay logistics fees to commercial distributors. This facilitates a functional shift from “tender-based procurement services” to “service-oriented tender procurement,” while also streamlining the processes for issuing consumables procurement orders and making payments. However, the role of commercial distributors in this model will be significantly diminished, further compressing their profit margins.

Platform-based procurement entails price linkage. In accordance with the nationally unified classification and coding system for medical consumables covered by medical insurance, establishing mechanisms for sharing high-value medical consumable price information across departments and between provinces to facilitate coordinated procurement pricing is one of the key functions of such platforms, enabling healthcare institutions to procure high-value medical consumables at relatively reasonable lower prices.

Only at this stage has the policy impact of volume-based procurement been nearly fully realized. The national health insurance system directly imposes price caps on high-value medical consumables during the procurement phase, and bypasses hospitals in the settlement phase by having the healthcare security authorities settle payments directly with suppliers. All transaction information falls under the oversight of the National Healthcare Security Administration, making the entire pharmaceutical and medical device sales process more open and transparent.

Therefore, in addition to reducing the prices of pharmaceuticals and medical devices, the newly established National Healthcare Security Administration (NHSA) has consolidated the powers of “procurement, payment, and supervision” through the “integration of three flows.” Only by resolving information asymmetry in the circulation of pharmaceuticals and medical devices can the NHSA effectively proceed with its next strategic move.

In retrospect, the Two-Invoice System eliminated distributors from the pharmaceutical and medical device supply chain, and Volume-Based Procurement forced manufacturers to make significant concessions. However, neither policy has fully impacted hospitals and physicians. In fact, these measures have failed to eliminate physicians’ incentives to overuse consumables.

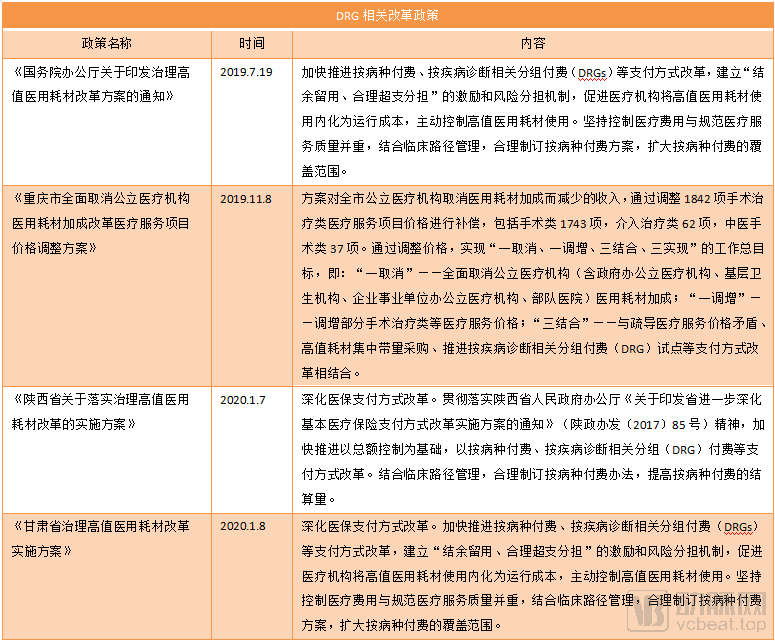

However, these two policies undoubtedly eliminate redundancies in the distribution of pharmaceuticals and medical devices, rendering the entire supply chain from production to usage controllable. In this context, DRG has become a decisive tool for regulating the behavior of physicians and hospitals.

Prior to the adoption of DRG for cost containment, this approach had long been utilized to evaluate efficiency across hospitals. By comparing the cost consumption index and time consumption index for the same disease across different hospitals, we can readily identify institutions with anomalous values and promptly pinpoint underlying issues. This implies that precise requirements are imposed on the use of high-value medical consumables for every surgical procedure.

Historically, the management and distribution models for medical consumables in most hospitals have been extensive, resulting in significant waste. If there is evidence of consumable misuse, Diagnosis-Related Groups (DRG) will identify unusual patterns in physicians' practices based on consumable utilization data.

Meanwhile, DRG signifies a reform of physician incentive mechanisms. By adopting bundled payment models, it internalizes the costs of pharmaceuticals and medical consumables into hospitals’ operational expenses. Under this incentive structure, physicians have no justification for the indiscriminate use of medical supplies; instead, cost-consciousness becomes the prudent approach.

Up to DRG, the ultimate beneficiaries have become evident.Following the major reforms of the Two-Invoice System, Volume-Based Procurement (VBP), and Diagnosis-Related Groups (DRG), pharmaceutical and medical device manufacturers, distributors, as well as physicians and hospitals, have all faced increasing constraints.At this point, the Healthcare Security Administration, whose interests align with those of patients and which ultimately aims to “control healthcare costs,” emerged as the final winner.

Data sourced from Artery Orange

Payment Model Reforms in High-Value Consumables Reform Plans Across Multiple Regions Cite DRG as One of the Directions

Overall, under ideal conditions, a series of policy measures will systematically address issues in China’s high-value medical consumables market, including price disorder, imperfect procurement mechanisms, the inability to make year-on-year price comparisons, inadequate invoice management, outstanding loans owed by public hospitals, and information asymmetry in procurement. Ultimately, this will gradually achieve national healthcare cost containment.

The entire reform process appears to have unfolded in three major steps: from the Two-Invoice System to Volume-Based Procurement (VBP), and then to Diagnosis-Related Groups (DRGs). In practice, however, policies for medical consumables are often implemented at the provincial or municipal level, with varying paces and degrees of participation across different regions. It is difficult for any single region to fully implement a given policy in isolation. Places such as Jiangsu Province, Nanjing City, and Sanming City in Fujian Province have taken the lead, largely following the pathway described above. Meanwhile, many other cities are advancing these reforms concurrently, or have already begun preparing for DRG pilots even before fully achieving volume-based procurement.

Therefore, assuming that the pathway following the sequence of “single-invoice system – volume-based procurement – DRG” is feasible, the focus of subsequent policy implementation will tend toward addressing the gaps within the existing structure.

Without coding, it is difficult to define quality standards and ensure the effectiveness of subsequent diagnosis and treatment.Therefore, the primary issue to be addressed in this field is the lack of standardized coding for high-value medical consumables.. In March 2019, the National Healthcare Security Administration convened a symposium to discuss this issue. Although the coding for numerous medical consumables was completed in 2020, the overall initiative remains ongoing.

Secondly,How to Establish a Consistency Evaluation for High-Value Medical Consumables Is a More Profound Issue. The high-value consumables market in 2020 presented an excellent opportunity for import substitution, as regional procurement platforms continued to prioritize “low price” in the absence of an established evaluation mechanism. This meant that high-priced, high-quality imported consumables would face a dilemma of greater-than-expected price reductions and loss of market share.

Many high-value interventional consumables remain in patients’ bodies for years. If procurement prioritizes “low price” alone without evaluating quality, this will harm patients. Furthermore, such incentive mechanisms are one-sided: while they encourage companies to develop lower-cost products with equivalent functionality, they also stifle innovation that commands a premium.

Furthermore, a unified standard for medical insurance reimbursement of medical consumables has not yet been established; to date, only a few cities have launched relevant pilot programs. Taking Tianjin as an example, the city previously implemented benchmark price management for disposable medical consumables, with medical insurance coverage based on these benchmark prices. Under this model, hospitals could increase their revenue by negotiating greater discounts from suppliers. This was merely an initial attempt; in the future, medical insurance reimbursement for medical consumables may be managed in accordance with the framework used for pharmaceutical reimbursement.

Finally, let us discuss Diagnosis-Related Groups (DRGs). Without the “Two-Invoice System” (or even the “One-Invoice System”) and volume-based procurement clearing obstacles for incentive mechanisms, physicians might waver between cost containment and excessive utilization, while pharmaceutical and medical device companies could still dominate usage patterns through kickback-driven sales. However, even with these two preceding policy supports, the National Healthcare Security Administration (NHSA) would struggle to fully leverage DRGs to reduce operational costs before the DRG coding framework matures. It will take some time before the system matures and is implemented to apply DRGs to the field of high-value consumables.

Although policy directions may appear fragmented, they are in fact clear. As benchmark city policies yield results, distributors and medical device companies must rethink their positioning and development strategies under cost-containment pressures.

For small and medium-sized distributors, this combination of policy measures has left them with virtually no room to maneuver. After losing the consumable products covered by volume-based procurement (VBP), they have been forced to pivot to other consumables not yet subject to such policies. However, the ultimate outcome of VBP for high-value medical consumables may be that all consumables are sold through the platform of the National Healthcare Security Administration (NHSA). By then, the rebates and price differentials that previously existed will disappear, making digitalized logistics and back-end services the only viable path forward.

For large domestic medical consumables manufacturers, the current focus of innovation lies in delivering high-quality products at low prices. At this juncture, companies must either capture over 70% of the product categories within their respective regions or exit those categories altogether. In the long run, however, manufacturers still need to pursue a “qualitative leap” in their products.

For manufacturers of high-value consumables with record-high prices, although policies have little direct impact on their revenues and expenditures, the products they develop must ultimately undergo regulatory approval for market launch. Therefore, these companies must give greater consideration to the strengths and weaknesses of competing products, striving to create innovative and differentiated offerings to avoid falling into the trap of “approval marking the beginning of failure.”

In 2020, the sounds of industry reshuffling were incessant. Amidst the turbulent changes, only those who clearly understood the policies could emerge as the ultimate winners.