Orthopedic Sports Medicine: The Fastest-Growing Segment in Orthopedics with Domestic Penetration Below 2%

When the 11th ISAKOS (International Society of Arthroscopy, Knee Surgery and Orthopaedic Sports Medicine) Congress was held in Shanghai, Yao Ming, as a specially invited representative of the Conference Chair, delivered an English speech at the meeting. It may seem somewhat surprising to see Yao Ming appear at a conference for professional medical exchanges, but in reality, athletes are the group most closely associated with sports medicine.

With population aging and the promotion of nationwide fitness, an increasingly broad segment of the population is benefiting from orthopedic sports medicine. On Zhihu, there is a story about a physician who, after seeing numerous friends posting about their exercise and fitness routines on social media, began to rigorously train in arthroscopic surgery. He anticipated that a large number of people would face sports-related injuries in the future, making sports medicine surgery a high-potential field within orthopedics.

In fact, the trend predicted by this physician has already been corroborated in clinical practice. According to incomplete statistics from the Orthopaedic Branch of the Chinese Medical Association, more than 110,000 arthroscopic surgeries were performed in China in 2009. Currently, industry experts estimate that the annual number of arthroscopic surgeries performed in China now exceeds 600,000.

The growth of the past decade is merely the beginning for sports medicine. Currently, 60–70% of sports medicine surgeries in China are still concentrated in Grade A tertiary hospitals. In the coming years, specialized sports medicine departments will become more widespread across additional hospitals and cities, and the field will continue to maintain a trajectory of rapid growth. Sports medicine has already become the fastest-growing subsector within orthopedics.

In addition to high growth, another major characteristic of the sports medicine niche market is import monopoly; in 2017, the market share of domestically produced products in China’s sports medicine market was less than 2%.

The high growth potential and the vast market for domestic substitution have fueled significant optimism regarding sports medicine, with the field poised to evolve into a high-growth niche comparable to hand surgery, joint replacement surgery, and spinal surgery. Startups in the sports medicine sector have also attracted strong interest from investment firms, with nearly all having completed at least one round of financing in recent years.

What Factors Will Drive Growth in Orthopedic Sports Medicine? How Can Domestic Startups Break Through the Import-Dominated Market? VCBeat (WeChat ID: vcbeat) has surveyed companies in China’s orthopedic sports medicine sector and interviewed industry insiders.

Orthopedic Sports Medicine is a subspecialty of orthopedics and sports medicine.The goal of sports medicine is to achieve maximal functional restoration with minimal trauma. Sports medicine products are primarily used to treat soft tissues between bones., such as injuries to the Achilles tendon, ligaments, menisci, tendons, and cartilage; meniscal and cruciate ligament injuries; tendinopathy; skeletal muscle injuries; cartilage and osteochondral injuries; joint instability; and glenoid labrum injuries.

Reviewing the historical evolution of orthopedics, the emergence of gunshot wounds after World War II spurred rapid development in the trauma subspecialty; in the 1950s, joints became a prominent focus within orthopedics, with many companies driving product innovation in joint replacement; from the 1970s to the 1980s, spinal surgery experienced vigorous growth; and sports medicine truly emerged as a distinct field within orthopedics in the 1980s.

The development of orthopedics in China, in the true sense, began in 1996. Sports medicine is a specialty independent of orthopedics abroad. It encompasses the four R’s: reconstruction, regeneration, repair, and rehabilitation. Only when all four stages are rigorously completed can it be considered sports medicine in the strictest sense.

In China, sports medicine initially focused primarily on arthroscopic surgery and was classified as a fourth-level discipline under the hierarchy of Clinical Medicine → Surgery → Orthopedics. Currently, driven by the nationwide fitness boom, the National Health Commission has mandated that every Grade A tertiary hospital establish a dedicated sports medicine specialty, elevating sports medicine to the status of a second-level discipline.

At the current stage, the primary indications for sports medicine in China are mainlyAll-Arthroscopic or Arthroscopy-Assisted Minimally Invasive Surgery, the morphological repair and functional reconstruction of soft tissues such as ligaments, joint capsules, and fasciae lag behind international standards in terms of overall development.

From the perspective of sports medicine product classification, sports medicine products can be subdivided into three major categories: body reconstruction products (fracture and ligament repair products, arthroscopic equipment, implants, prostheses, orthoses), body support and recovery products (braces and supports, physical therapy equipment, compression garments), and accessories.

Medical device products in orthopedic sports medicine primarily include arthroscopy systems (including main scope systems and motorized shaver systems), reconstruction systems (interference screws, suture-button titanium plates), and repair devices (meniscus repair systems, artificial ligaments, etc.).

Classification of Medical Devices in the Field of Sports Medicine

High-Value Sports Consumables: A Complex Product Landscape, its technical barriers are higher than those of general orthopedic medical devices.Due to the relatively short history of sports medicine development in China, a large number of overseas sports medicine products have not truly entered the Chinese market.

In recent years, the global orthopedics market has experienced a slowdown in growth. According to projections in the EvaluateMedTech World Preview 2018–2024 report, diagnostic imaging and orthopedics will be the slowest-growing segments within the medical device industry, with a compound annual growth rate of only 3.7% from 2017 to 2024. Although the orthopedics market has moved past its period of high growth, sports medicine remains the fastest-growing subsector within orthopedics.

The rapid growth of the sports medicine market is directly reflected in the changes in two key indicators: the number of arthroscopic surgeries performed nationwide and the number of sports medicine physicians in China.

In terms of surgical procedures, arthroscopic surgeries account for more than half of the domestic sports medicine market in China. Currently, market growth in sports medicine is primarily driven by the increase in arthroscopic procedures. According to IQVIA statistics, there are approximately 8,000 arthroscopes in use in China, with an annual growth rate of 20%. Data from Millennium indicates that in 2018, approximately 6 million arthroscopic procedures were performed in the United States, compared to only 850,000 in China. Arthroscopic minimally invasive surgery features small incisions and minimal trauma; it is now a consensus in sports medicine that such procedures should be conducted using arthroscopy.

Initially, the arthroscope was designed solely as a device for visualization and diagnosis. However, with technological advancements, arthroscopy has evolved from a diagnostic tool into a surgical procedure.

As a diagnostic tool, arthroscopy can confirm certain conditions, such as synovial plica syndrome. Furthermore, it enables the performance of procedures that were previously difficult to accomplish via open surgery, such as partial meniscectomy and debridement of osteochondral lesions of the talus in the ankle. The instruments and equipment required for this procedure include the main arthroscopic unit, an arthroscopic power system, and a radiofrequency ablation system. The preference for minimally invasive surgical techniques has driven growth in the arthroscopy market.

In terms of surgical volume, Peking University Third Hospital, a leading institution in orthopedics, has 68 inpatient beds in its Institute of Sports Medicine. The department handles over 70,000 outpatient visits annually and performs more than 4,500 surgeries per year, with this number increasing year by year. Notably, the annual number of anterior cruciate ligament (ACL) reconstruction surgeries alone has exceeded 1,400 cases, ranking first in China.

At some hospitals that have only recently launched sports medicine services, although the surgical volume is lower than that of large hospitals, the growth rate is rapid. Taking the First Division Hospital of Xinjiang as an example, the hospital opened a specialized outpatient clinic for minimally invasive sports medicine in 2018. Despite this late start, arthroscopic surgeries exceeded 400 cases within the first year of the clinic’s operation. The total volume of sports medicine diagnoses and treatments has surpassed 4,000 cases.

“Looking at the change in the number of physicians, one practitioner stated, ‘Five years ago, there were likely fewer than 1,000 doctors in China performing sports medicine surgeries, whereas today there are at least three to four thousand. The most direct manifestation of this growth is the enthusiasm among physicians at sports medicine academic conferences; even for subspecialties such as hip arthroscopy, a single conference can attract more than 1,000 attendees.’”

Zhang Zhiling, Partner at Zhenghe Huitong Medical, stated: “If we were to summarize the future potential of sports medicine in one sentence, the current stage of its development is akin to that of traditional orthopedics in the year 2000.”

According to incomplete statistics from the Orthopaedic Branch of the Chinese Medical Association, more than 110,000 arthroscopic surgeries were performed in China in 2009. Currently, there is no precise figure for the number of arthroscopic surgeries conducted domestically. Through its research, VCBeat learned from industry insiders that approximately 600,000 to 700,000 arthroscopic surgeries were performed in China between 2018 and 2019. Regarding terminal market share, one industry insider stated bluntly that the sports medicine terminal market share is approximately RMB 1.2 billion to RMB 1.3 billion. This figure is smaller than the market shares reported by many market research firms (according to Millennium’s statistics, the size of China’s sports medicine market was RMB 2.12 billion in 2018, projected to grow to RMB 3.91 billion by 2021, with a compound annual growth rate of 22.63%), but it more accurately reflects the true market size. Although the current market share is not substantial, sports medicine still has significant room for growth given the existing growth rate.

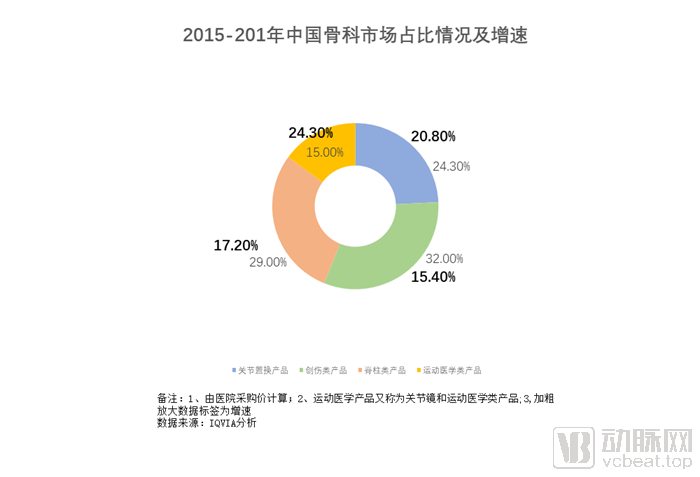

According to data from the “Panoramic Report on China’s Orthopedic Device Market” released by IQVIA, sports medicine accounted for 17% of the overall orthopedic market in the United States from 2015 to 2017, with a growth rate of only 6.5%. In contrast, sports medicine represented 15% of China’s orthopedic market, with a growth rate of 24.3%.

A detailed examination of the drivers fueling the growth of China’s sports medicine market reveals that, from a macro-environmental perspective, the momentum stems from population aging and the rising incidence of sports-related injuries. The increasing prevalence of musculoskeletal disorders (such as osteoarthritis and rheumatoid arthritis), driven by rapid population aging, has directly contributed to the growth in arthroscopic procedures. According to the State Council’s “National Fitness Plan (2016–2020),” China’s physically active population was projected to reach 435 million by 2020. Assuming an estimated sports injury rate of 50% among regular exercisers, approximately 220 million people in China would have sustained sports-related injuries by that time.

In addition to aging and sports injuries driving the growth of sports medicine, the increase in orthopedic sports medicine physicians is an indispensable pillar for the growth of this segment.

An industry insider stated in an interview that orthopedic surgeons previously rarely chose to specialize in sports medicine, with most preferring to focus on areas such as the spine and joints. Procedures in sports medicine, such as those for rotator cuff tears, meniscal tears, or joint wear, demand a high degree of surgical precision. However, as orthopedic surgeons’ understanding of sports medicine has deepened and companies have continued their market education efforts, the number of orthopedic surgeons specializing in sports medicine is growing rapidly.

Sports medicine in China is currently in a phase of rapid catch-up. Hospitals that have established independent sports medicine departments are typically those with strong traditional orthopedics programs, such as Peking University Third Hospital, Beijing Jishuitan Hospital, Shanghai Sixth People’s Hospital, and Huashan Hospital Affiliated to Fudan University. In most other hospitals, sports medicine remains a subspecialty within the department of orthopedics. Although these institutions maintain considerable strength in traditional orthopedics, the overall development of sports medicine in China still lags behind international standards.

To cite a simple example, many well-known athletes often need to travel abroad for treatment after sports injuries. However, apart from the lag in sports medicine surgery compared to foreign countries, China has an even larger gap with foreign countries in professional rehabilitation.

A major driver of the rapid growth of sports medicine in China is the increasing number of physicians capable of performing sports medicine surgeries. This rise in the number of sports medicine specialists is also inseparable from market education efforts by sports medicine companies. Hospitals that were among the first to establish sports medicine departments invariably had strong orthopedics divisions, and it was likewise traditional orthopedic giants that pioneered the Chinese sports medicine market.

In terms of market share, imported products hold a significant portion of the domestic orthopedic sports medicine market. Orthopedic sports medicine is also the subsector within orthopedics with the lowest rate of domestic production in China.

Among orthopedic medical devices, trauma devices have the highest localization rate, exceeding 80%, while joint replacement devices are close to 55%, and spinal devices stand at approximately 60%. However, in 2017, the domestic market share for sports medicine products was less than 2%. Currently, the sports medicine sector is dominated by foreign companies, including Smith & Nephew, Johnson & Johnson, Arthrex, and Conmed.

Global orthopedic medical device giants strategically entered the sports medicine sector early on through acquisitions, establishing complete sports medicine industry chains, which clearly underscores their significant emphasis on the sports medicine market.

In 2003, Johnson & Johnson partnered with Mitek, a sports medicine manufacturer, to expand its orthopedics portfolio. Mitek was the world’s first company to offer suture anchors (used for fixing tendons and ligaments to bone). Since then, Johnson & Johnson’s orthopedics division has covered trauma, spine, joints, sports medicine, and neurosurgery. In the field of sports medicine implants, Johnson & Johnson’s Mitek brand is currently a market leader, with annual shipments in China valued at RMB 200–300 million.

In 2015, DePuy Synthes acquired Olive Medical, gaining its visualization systems, extending DePuy’s product portfolio, and propelling DePuy into the arthroscopic visualization market to provide therapeutic services for patients suffering from pain or injuries in the shoulder, knee, hip, and small joints. In 2014, Smith & Nephew acquired ArthroCare Corp., a U.S. manufacturer of sports medicine products, for $1.7 billion in cash to strengthen its sports medicine business.

Zimmer Biomet, one of the global leaders in orthopedics, acquired the Cayenne sports medicine product line in 2016. In early 2019, Stryker acquired the Israeli company OrthoSpace to strengthen its sports medicine surgical portfolio. OrthoSpace has launched its flagship product, InSpace™, through technological innovation. This product is indicated for the treatment of patients with difficult-to-treat rotator cuff tears.

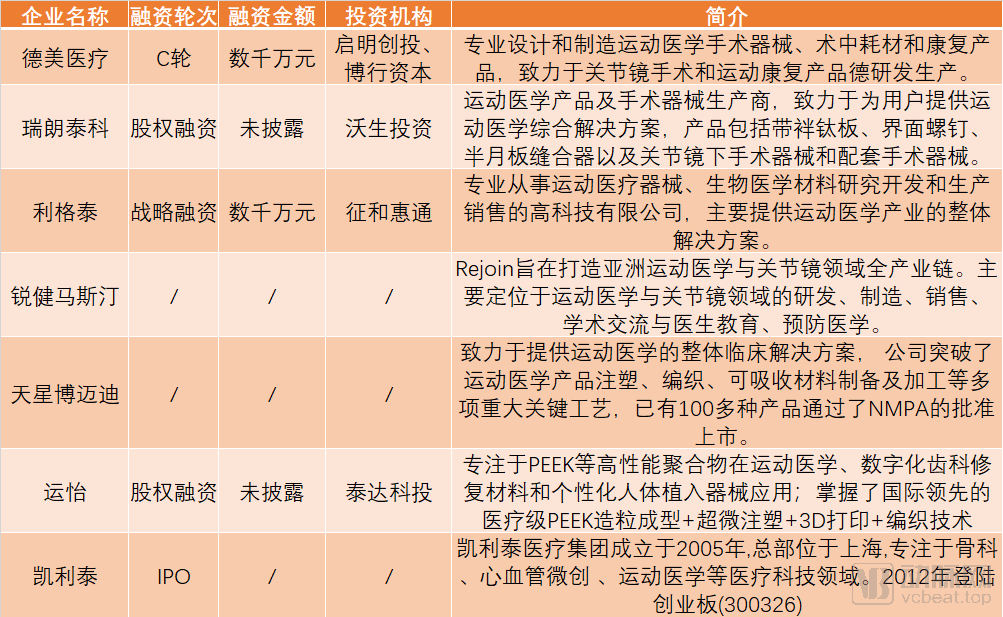

Wherever import monopolies exist, domestic brands are on the rise. Throughout the development of the medical device industry, domestic substitution has remained the central theme, and sports medicine is no exception. In this emerging market for sports medicine, a cohort of startups is beginning to take root.

Few domestic companies have ventured into the emerging field of sports medicine. Currently, some listed companies in China are making strategic layouts, including Kanghui Medical, Double Medical, and Weigao Group. Additionally, a number of startups are beginning to emerge.

Overview of Domestic Sports Medicine Startups (Note: Data compiled from public sources. For any inaccuracies or unlisted companies, please contact VCBeat for further discussion.)

The advantages of domestically produced products can be divided into two aspects: first, lower costs; second, the ability to develop products that better align with the operational habits of Chinese physicians and the anatomical structures of the Chinese population.

In terms of cost reduction, the price of an imported arthroscopy system can reach RMB 3–4 million, whereas domestically produced equipment can bring the price down to approximately RMB 1 million. This price reduction lowers procurement costs for hospitals, making domestic products more affordable for a greater number of healthcare institutions.

Based on the current strategic plans of startups, many aspire to become providers of comprehensive solutions in the field of sports medicine. However, at this stage, no domestic company in China has yet emerged with the capability to deliver such end-to-end solutions.

The primary reason is the high barrier to entry in the field of sports medicine. Strictly speaking, although many companies involved in sports medicine in China are traditional orthopedic firms, sports medicine devices have a higher threshold than general orthopedic devices. The two main characteristics of sports medicine are addressing soft tissue issues and facilitating minimally invasive surgeries; thus, most products differ from conventional orthopedic medical devices.The development of sports medicine cannot follow the path some orthopedic companies envision—simply investing in equipment and imitating products. It is not enough to merely have capital to establish production lines; a profound understanding of the sports medicine field is essential.

Take sports medicine manufacturing facilities as an example. There are significant differences between sports medicine and orthopedic manufacturing facilities. Sports medicine production requires addressing challenges such as injection molding and weaving of soft tissues, whereas the core strength of many Chinese orthopedic companies lies primarily in mechanical machining, which has limited application in the field of sports medicine.

An industry insider stated, “Currently, a significant number of companies in China are still focused on the clinical application of metal anchors in their sports medicine R&D. In reality, the use of metal anchors in sports medicine surgeries is zero in the United States, and they are not the highest-volume single product in China either. This indicates that some domestic companies lack a deep understanding of sports medicine. Product design in this field requires a holistic understanding of sports medicine, rather than focusing on individual products. For any product, considerations should include: the direction of development in sports medicine; clinical needs; how to achieve precise surgical control and shorten the learning curve for physicians; and how to better serve patients.”

Furthermore, due to the immaturity of China's sports medicine industry chain, it remains challenging to produce comprehensive solutions.China has completed its industrialization process in a relatively short period, yet certain fine-processing capabilities remain insufficient. For instance, while the country produces a substantial volume of steel for infrastructure development, domestic production capacity for medical-grade metallic materials and biomedical materials remains relatively weak.

In addition to the challenges in product research and development, marketing obstacles are equally formidable. In the early days, when imported brands such as Smith & Nephew entered the then-untapped Chinese sports medicine market, their primary focus was on educating the market within Tier 1 cities’ Grade A tertiary hospitals. The remaining untapped market for domestic sports medicine brands now lies in Tier 2 and Tier 3 cities, as well as a larger number of Grade B secondary hospitals, which means that market expansion will be even more challenging.

From one perspective, domestic sports medicine companies currently exhibit significant product homogenization, with most players concentrated in similar market segments. As these products achieve large-scale commercial launch, the sports medicine market may face genuine competition in the future.

Overall, domestic companies in China are still in the early stages of development. Their products have not yet entered the phase of large-scale sales validation, and as all players remain in these nascent stages, it is difficult to determine which product is superior.

Undoubtedly, in the still-immature field of orthopedic sports medicine in China, domestic startups have many shortcomings, whether in processing capabilities or product integrity. The process of establishing local sports medicine brands is lengthy. However, as more people pay attention to this market, the domestic sports medicine market will gradually grow stronger.