CDSS Goes Commercial: How Health IT Companies Are Tapping into a Billion-Dollar Market

Clinical Decision Support Systems (CDSS) are not a new concept. During the rise of personal computers, forward-thinking individuals recognized the value of computer-aided diagnosis and attempted to construct a virtual “doctor” through programming, euphemistically termed an “expert system.”

However, simple one-to-one data mapping at that time could not address complex medical issues. As the saying goes, traditional Chinese medicine diagnosis relies on “inspection, auscultation and olfaction, inquiry, and palpation,” requiring physicians to gather information through multiple sensory channels and apply logical reasoning to arrive at effective conclusions. Relying solely on patients’ chief complaints without comprehensively evaluating factors such as age, physical condition, and medical history renders such a “diagnosis” little more than a matter of chance.

Over the past 50 years, expert systems have undergone multiple iterations, evolving from initial query-based systems with single functions and independent relationships into integrated components of clinical systems. In terms of knowledge management, the previously fixed, hard-coded knowledge bases have transformed. The definition of Clinical Decision Support Systems (CDSS) has become broader, emphasizing the use of clinical data by physicians to improve healthcare quality. During this process, knowledge representation has trended toward standardization, and knowledge sharing has become configurable.

Current CDSS development should focus on three key aspects: first, data-driven approaches that effectively leverage health data generated during medical processes to uncover underlying logic and patterns; second, configurability, enabling content and workflow customization based on configurable knowledge bases; and third, specialization, developing CDSS tailored to refined clinical scenarios by leveraging personalized data from different hospitals and departments.

If the first two directions determined the precision of CDSS development, then the third direction—specialization—has broadened the market’s scope. It is precisely for this reason that numerous players are flocking into this space.

Over the past few years, numerous listed companies and startups have entered this space, including unicorns such as LinkDoc Technology and Jiahua Health, internet giants like Tencent and Baidu, as well as highly competitive emerging enterprises such as Huimei Technology and Senyi Intelligence.

In November 2018, Tencent secured a key special project on “Research and Development of Digital Diagnostic and Therapeutic Equipment,” developing the AI-Assisted Clinical Decision Support System (AIACDSS) and becoming the first internet giant to enter this field.

Just four months ago, Baidu quietly took a controlling stake in Beijing Kangfuzi Technology Co., Ltd. and consolidated its healthcare-related businesses under its current entity, Lingyi Zhihui. As of the time of acquisition, the latter had been deeply engaged in the field of Clinical Decision Support Systems (CDSS) for nearly four years, with its related products deployed in dozens of primary healthcare institutions.

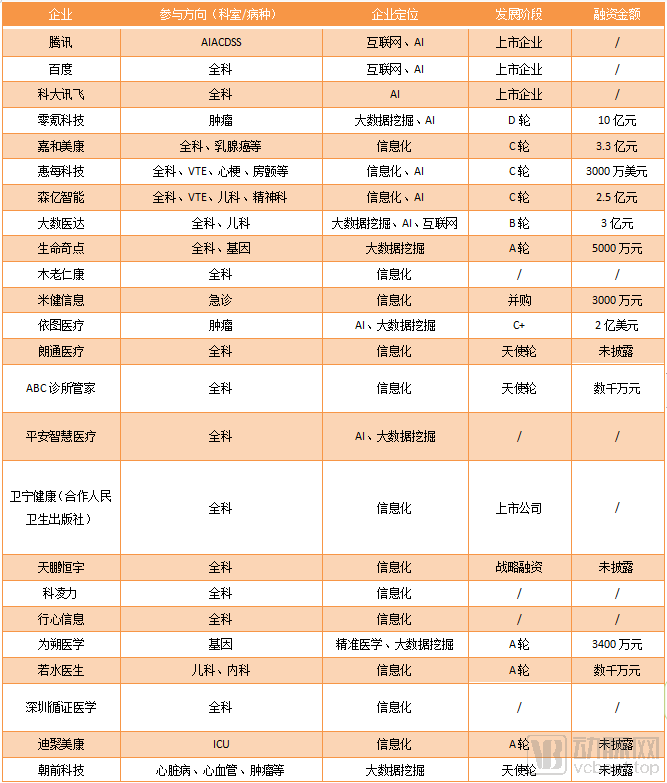

By scanning relevant sectors, VCBeat identified 30 companies with independent Clinical Decision Support System (CDSS) businesses or projects (many listed health IT companies and information platform providers offer related technologies and services but have not established standalone products; these were excluded from the statistics). In terms of scale, most companies are pre-Series B, and fewer than one-third are publicly listed.

Healthcare Companies with Independent CDSS Businesses (Incomplete Statistics)

Data sourced from the VBInsight database and Qichacha.

Due to the high fragmentation of the healthcare IT market, the share of startups remains underestimated, particularly for vendors whose operations are confined to local regions and thus difficult to capture in statistics. Nevertheless, traces of these uncounted enterprises can still be found in healthcare IT product procurement projects listed on the China Bidding and Procurement Network.

From a business perspective, developing general practice versions of Clinical Decision Support Systems (CDSS) to serve primary care remains the preferred choice for many companies. A total of 18 enterprises have set this as their R&D target, while another 13 have begun developing specialty-specific CDSS. Currently, more mature products include those for Venous Thromboembolism (VTE), myocardial infarction, and pediatrics.

Differences in development pathways, R&D logic, and market size between general practice Clinical Decision Support Systems (CDSS) and specialty-specific CDSS are undoubtedly the primary drivers behind the divergence in corporate strategies. Given equivalent investment, a general practice CDSS can be rapidly deployed to new regions following successful pilot implementation. In contrast, expanding a specialty-specific CDSS into new clinical settings requires fresh analysis of physicians’ workflow habits, clinical pathways, and data characteristics specific to those settings. This implies that companies must expend significantly greater effort to develop products that gain physician acceptance. Consequently, publicly listed companies with data advantages, such as Tencent, Baidu, and iFlytek, are more inclined to construct knowledge graphs to address primary care challenges rather than focusing on specialized clinical solutions for department-specific issues.

Notably, companies that leverage genetic data to supplement clinical data and thereby enhance physicians’ decision-making have begun to emerge over the past two years. In VCBeat’s 2018 statistics on the CDSS sector, no such CDSS-focused companies were identified; however, the current round of statistics has revealed three relevant enterprises: Life Singularity, Weishuo Medicine, and Angikangr.

An analysis of the historical business positioning of these enterprises reveals that most CDSS offerings evolved from their foundational health informatics services. This indicates that prior to developing CDSS, they had already accumulated in-hospital informatics experience with systems such as electronic medical records (EMR), hospital information technology (HIT) infrastructure, and specialty-specific information management platforms. Statistical data show that as many as nine companies possess advanced capabilities in AI and big data mining. In particular, for startups before Series B financing, their entry into the CDSS market was not driven by the intent to create a standalone CDSS product; rather, they started with AI-assisted imaging diagnosis and gradually expanded upstream and downstream across the patient care journey.

Overall, compared with VCBeat’s 2018 statistics, companies that offered CDSS as a standalone product at that time continue to deepen their R&D efforts, while more companies have entered the field in the past two years, indirectly highlighting the market’s potential.

Lingyi Zhihui, a subsidiary of Baidu, is a typical example. The company has developed along two main paths: first, it has entered the smart healthcare industry system by focusing on intelligent medical care, intelligent management, and intelligent patient services; second, it has brought inclusive medical services to primary care institutions with Clinical Decision Support Systems (CDSS) as the core—CDSS has become one of Baidu’s core products in its healthcare sector.

The influx of numerous enterprises has intensified competition within the clinical decision support system (CDSS) industry; however, when it comes to specific application scenarios, we still need to examine the development challenges of CDSS in a fragmented manner.

As the ultimate dream of expert system designers in its early days, general practice CDSS has been implemented in numerous hospitals, with its business model beginning to take shape.

Specifically, its functions are primarily directed toward two areas: first, simulating multidisciplinary team (MDT) discussions to provide reference opinions for specialists in large hospitals, thereby preventing blind spots in expert decision-making; and second, being deployed in primary care hospitals to enhance the diagnostic capabilities of grassroots medical institutions.

Lin Yueyu, Chief Architect of AI at Dashu Yida, once cited a case in which a patient experiencing intestinal discomfort sought specialist care at a top-tier (Grade 3A) hospital in Beijing. Despite undergoing numerous tests and multiple rounds of expert consultations, the underlying cause remained elusive. It was only when an intern doctoral candidate from a non-gastroenterology specialty reviewed the case that the true issue—an immune system disorder—was identified.

This is precisely the role of a Clinical Decision Support System (CDSS): “Specialists are often confined to their routine knowledge, potentially overlooking certain considerations. In such cases, physicians require a knowledge base that enumerates various potential causes for a patient’s symptoms, helping experts recall relevant information and serving a function similar to multidisciplinary consultation. This will reduce the likelihood of specialists missing other diagnoses.”

Currently, the primary role of general practice Clinical Decision Support Systems (CDSS) remains at the primary care level. With AI assistance, both the accuracy and speed of information matching in these systems have improved significantly. Taking the application of Lingyi Zhihui at the Mafang Community Health Service Center in Pinggu District, Beijing, as an example, the system reduced the time for initial patient consultation to approximately 3 minutes. Including the generation and printing of medical records, the entire process takes roughly 5 minutes. Compared to routine consultations, CDSS-assisted visits are more detailed and time-consuming in terms of direct interaction; however, when considering the end-to-end workflow, the total time spent per patient is substantially reduced.

Overall, within the framework of tiered diagnosis and treatment, an ideal general practice-oriented Clinical Decision Support System (CDSS) can provide primary care settings with standardized, efficient, and accurate diagnostic tools. It assists physicians in determining whether patient referrals are necessary, thereby extending equitable access to high-quality medical resources concentrated in tertiary centers to every grassroots healthcare region through a replicable model.

In contrast, specialty CDSS requires not only extensive knowledge bases for data support but, more critically, a deep understanding of the clinical diagnostic pathways for target diseases. As Zhang Qi, CEO of Huimei Technology, puts it, “The development of specialty CDSS is primarily a clinical issue, and secondarily a technical one.”

Specifically, Zhang Qi summarized the core issues into two points: “Initially, we focused entirely on the clinical treatment process of patients, including changes in their condition, medication data, laboratory and imaging tests, and nursing care data. However, even with this approach, the data obtained remained incomplete. To develop a robust Clinical Decision Support System (CDSS), we also need to integrate patients’ past medical histories and post-discharge follow-up information, thereby synthesizing data from the entire diagnosis and treatment workflow to truly achieve a ‘real’ understanding of the patient.”

This is one of the reasons why companies are reluctant to venture into specialty-specific Clinical Decision Support Systems (CDSS). To achieve optimal outcomes, enterprises must navigate an extensive workflow that involves interfacing with dozens of disparate health information systems. “Different business systems have different interfaces, data standards, and processing protocols; therefore, the entire process of data collection, standardization, and recognition is highly complex.”

The second challenge lies in the variability of parameters. Unlike general practice, specialists often encounter patients with severe conditions, sometimes even life-threatening ones, when providing specialized care. “In such scenarios, clinical decision support systems (CDSS) must handle a vast number of variables. Establishing high-quality data annotations and precise models to analyze patient conditions requires substantial effort.”

However, it is precisely because of the potential for complex and variable clinical scenarios that tertiary hospitals have a subjective demand for specialized Clinical Decision Support Systems (CDSS). The head of data products at Senyi Intelligence stated, “In addition to meeting the requirements for electronic medical record (EMR) grading, hospitals expect us to assist in medical administration by performing quality control on certain medical record data. Furthermore, CDSS can help hospitals establish standardized clinical workflows and structured clinical data. When combined with a reliable clinical knowledge base, this facilitates the accumulation of data assets. Many physicians value this aspect, hoping to leverage these accumulated resources for subsequent data analysis and scientific research.”

Of course, the development of specialty Clinical Decision Support Systems (CDSS) is still in its early stages. Given the current data reserves, few enterprises have access to sufficient patient oncology data covering the entire care journey. Empowered by AI, CDSS requires robust data support to function effectively, which implies that there are numerous opportunities for specialty CDSS in the field of oncology, representing a vast blue ocean market.

Having understood physicians’ needs and the challenges involved in building Clinical Decision Support Systems (CDSS), what does an effective CDSS look like in practice? How can such a product be maintained and innovated? Let us examine three mature products as case studies.

Dashu Yida: How Can an AI-Powered General Practice CDSS Based on Electronic Medical Records Break Through?

In the general practice version of CDSS, data is like soil, while information processing technology serves as fertilizer; both are indispensable for cultivating an excellent general practice CDSS.

Since its establishment in 2015, Dashu Yida has spent nearly five years refining its capabilities in the Clinical Decision Support System (CDSS) domain, accumulating a vast amount of standardized patient data. Building on this data foundation, the company has constructed an effective knowledge graph that integrates extensive patient data with medical knowledge into a neuron-like knowledge network using AI. This represents one of the most significant advantages distinguishing its CDSS from competitors.

Sheng Luwei, Regional General Manager of Dashu Yida, told VCBeat: “Symptoms and conditions often have a many-to-one relationship. For instance, fever is associated with a wide range of diseases, so we must delve into deeper underlying logic. A CDSS that merely lists all possible conditions corresponding to a symptom such as cough, without further analysis, holds little value.”

“Through big data analysis based on knowledge graphs, we can prioritize conditions by severity and urgency, account for interconnections among different diseases, and comprehensively generate a reasonable probability estimate. During this process, clearly implausible diseases are excluded, ensuring that the results are clinically actionable for physicians.”

Currently, the Dashu Yida Multi-dimensional CDSS (Clinical Decision Support System) features multiple functionalities, including intelligent electronic medical record documentation, diagnostic assistance, treatment recommendations, intelligent connotation-based quality control, and medical knowledge queries, making it a typical general-practice-oriented CDSS. In terms of implementation, the system was first piloted in 55 impoverished villages in Yangshan County, Qingyuan City, Guangdong Province, and has since been fully rolled out across 2,277 provincial-level impoverished villages in 15 prefecture-level cities in Guangdong Province.

Huimei Technology's In-Hospital Intelligent VTE Prevention and Control

Venous thromboembolism (VTE) is not a disease specific to any single medical specialty. Patients who are postoperative, have suffered trauma, have advanced-stage cancer, are in a coma, or are bedridden for prolonged periods are all at risk of developing VTE. However, assessing a patient’s risk of VTE is not straightforward. Beyond relying on physicians’ clinical experience, more authoritative approaches involve using individualized VTE risk assessment models, such as the Caprini Risk Assessment Scale and the Padua Prediction Score, to analyze and evaluate patients. Nevertheless, because VTE assessment is time-consuming, physicians must strike a balance between their primary clinical duties and VTE screening and prevention efforts—a challenge that further strains hospitals’ already limited resources.

Huimei Technology leverages artificial intelligence to address this challenge by implementing intelligent tracking, scoring, and monitoring of patients. Numerous difficulties must be overcome in this process. “To enable computers to determine whether a patient has experienced a cerebral infarction within the past month—a key risk factor for venous thromboembolism (VTE)—the system must not only help machines understand the temporal constraints of the event (i.e., focusing on recent occurrences within a specified one-month window, while excluding events from three or six months prior), but also assess the patient’s disease status, including grading and classification. This often requires synthesizing information from medical history, MRI reports, and other sources to reach a conclusion. Traditional information systems are incapable of handling such complex tasks,” explained Zhang Qi to VCBeat.

To address these challenges, Huimei leverages natural language processing (NLP) technology to achieve semantic understanding of medical record data, structuring and standardizing descriptive natural language. Furthermore, deep learning algorithms integrate personalized medical record data into a rule base, and, in conjunction with clinical guidelines and various assessment scales, construct a VTE knowledge graph. This approach enhances the accuracy of the final machine learning model while simultaneously resolving the two major difficulties faced by physicians: "difficulty in data entry" and "difficulty in data analysis."

Furthermore, AI-based clinical decision support capabilities can assist healthcare professionals in conducting automated assessments and issuing alerts to prevent the ordering of contraindicated medications based on patient-specific contraindications. By shifting quality control checkpoints upstream through AI-driven quality assurance, this approach effectively addresses the challenge of managing the intrinsic quality of venous thromboembolism (VTE) care provided by physicians.

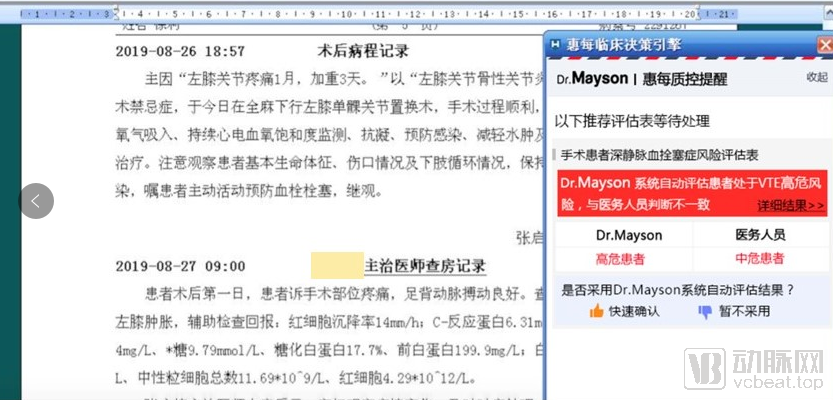

Meanwhile, Huimei regularly communicates with physicians to address the specific requirements of individual hospitals, thereby enhancing the “intelligence” of its system through clinical application. For instance, Huimei holds regular meetings with departments such as the Medical Affairs Department at China-Japan Friendship Hospital to discuss feedback and suggestions on system usage. During the initial launch of the VTE (Venous Thromboembolism) system, clinical staff reported that the original alert mechanism did not allow physicians to promptly and clearly assess the severity of CDSS (Clinical Decision Support System) alerts. In response, Huimei optimized the system by introducing color-coded alerts, enabling doctors and nurses to gain a preliminary understanding of risk levels before confirming patient conditions. This detailed improvement has further enhanced the effectiveness of the hospital’s VTE prevention and control system.

Senyi Intelligence: Hemorrhage Assessment and Database Governance

Senyi Intelligence, which started with Chinese medical natural language processing technology, has also made various attempts in CDSS. Currently, it has created relatively mature products in areas such as VTE, perioperative care, cardiology, and pediatrics. According to Senyi Intelligence, to develop specialized CDSS systems effectively, it is essential to thoroughly understand the clinical decision-making pathways, identify pain points within these processes, and address them using data and knowledge.

Lu Xiang stated, “Taking bleeding assessment as an example, when using scales for evaluation, the clinical definition of bleeding encompasses data from three aspects: history of prior bleeding, bleeding diathesis, and hematologic disorders. In clinical practice, there may be more than 50 definitions related to these three aspects. Some of these definitions are derived from laboratory indicators, some from medical record texts, and others from diagnostic histories. Relying solely on physicians and nurses to analyze such a large number of indicators not only entails a heavy workload but also fails to guarantee accurate results. However, by employing natural language processing and data standardization, among other techniques, we can rapidly provide accurate bleeding assessments.”

Furthermore, with the advancement of clinical medicine and the transformation of hospital operations in recent years, there is a growing need for a configurable medical knowledge base. In this regard, Senyi Intelligence ensures the validity of its knowledge base through continuous updates.

“The first step is knowledge comprehension. At the outset, we engage in continuous communication with clinicians and discuss the final medical decision-making content with relevant Key Opinion Leaders (KOLs). Only after confirming that the ultimate medical understanding of this knowledge is sound do we translate it into computer language for the second step: testing.”

“The second step involves testing based on the medical content converted into the decision engine to ensure the accuracy of the computer code. Upon completion of this step, we will immediately proceed to the third step: end-to-end testing, which is conducted in the hospital’s backend system using real patient cases. Only after completing these steps can we guarantee the reliability of the knowledge base.”

When discussing the market and business model of CDSS, we need to make estimates from three perspectives: general practice, grading, and specialization.

First, let us examine the market for CDSS solutions designed to meet EMR grading requirements. In light of current policy realities, hospitals are required to deploy CDSS only when pursuing an Electronic Medical Record (EMR) system certification at Level 4 or above. However, the CDSS requirements for Level 4 EMR certification are limited to basic drug compatibility checks. Starting from Level 5, additional functionalities are mandated, including alerts for laboratory and imaging tests as well as diagnostic recommendations. Based on current pricing trends, the tender prices for CDSS solutions supporting Level 4 and Level 5 EMR certifications generally range from RMB 400,000 to 500,000. For Level 6, the tender price is approximately RMB 800,000, while for Level 7, it ranges from RMB 1.2 million to 1.5 million.

However, as indicated by policy, only tertiary hospitals (Grade III Class A) currently face mandatory requirements to procure rated versions of Clinical Decision Support Systems (CDSS). Broadly speaking, in 2019, more than 7,000 hospitals across China applied for electronic medical record (EMR) grading. This implies that the market is not particularly large, with an annual scale of approximately RMB 8 billion.

The market for general practice is relatively larger. If limited to knowledge base query functions, the bidding price for a single product ranges from RMB 300,000 to 500,000. However, healthcare institutions typically require additional features such as assisted diagnosis, medication recommendations, and supporting hardware products. Consequently, the average revenue per customer (ARPU) for a single institution amounts to approximately RMB 1 million.

According to Sheng Luwei, Regional General Manager of Dashu Yida, Jiangsu Province has more than 90 districts and counties. Assuming an average project procurement value of RMB 1 million per district or county, this translates into a market worth RMB 100 million. However, in certain core cities, the density of primary healthcare institutions will be significantly higher than that in ordinary cities.

Furthermore, private healthcare chains, in an effort to standardize clinical workflows and enhance operational efficiency through big data, are also adopting general practice-oriented CDSS solutions. For instance, Lü Yisheng Community Chain Clinics has procured the CDSS product from Huimei Technology. Consequently, the total estimated market size for general practice CDSS is projected to exceed RMB 10 billion.

Specialty CDSS products are slightly more expensive than general practice products. According to bidding data compiled by VCBeat, their prices range from RMB 500,000 to RMB 3 million. However, the market size depends on the extent to which companies can develop application scenarios. If a single VTE product could be deployed in every hospital, the market for this specific specialty CDSS scenario would approach that of rating-oriented CDSS systems.

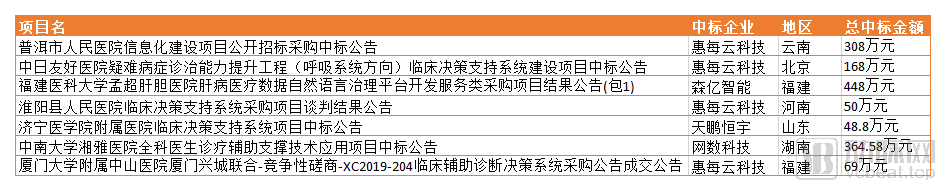

Partial CDSS Tender Data, Sourced from the VCBeat Orange Database

Examining the business model further, whether for general practice or specialty Clinical Decision Support Systems (CDSS), the current approach still follows the traditional Health Information Technology (HIT) sales path: selling to hospitals on a per-project, one-time basis, while charging an annual service fee in subsequent years.

However, given the iterative nature of knowledge bases, CDSS vendors will continuously update their products and make ongoing investments in the future. From this perspective, the SaaS model may be more suitable for CDSS vendors. Furthermore, annual subscription fees provide hospitals with a safeguard against the uncertainties associated with emerging technologies. Therefore, in terms of business models, the payment structure for CDSS is likely to shift from project-based fees to service-based subscriptions in the future. If this transition proves successful, the market size is expected to expand further.

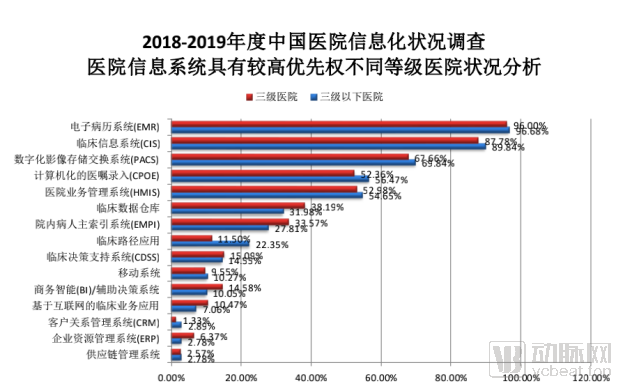

Finally, it is important to address the issue of payment. For specialty Clinical Decision Support Systems (CDSS), hospitals have a demand to purchase such systems to enhance control over the quality of clinical diagnosis and treatment; therefore, hospitals will serve as the payers for specialty CDSS. The "Survey on Informatization Status of Chinese Hospitals," released by CHIMA in 2019, revealed the attitudes of hospital information departments toward CDSS through sampling surveys. The results indicated that CDSS ranked high in priority across both tertiary grade A hospitals and hospitals below the tertiary level.

However, for the general practice version of CDSS, primary healthcare institutions may lack the direct incentive to pay for such a product that does not directly generate revenue.

Nevertheless, the state is determined to enhance the diagnostic and treatment capabilities of primary healthcare institutions. For many public primary care facilities, procurement conducted by district- and county-level Health Commissions has become one of the primary payment models for General Practice Clinical Decision Support Systems (GP-CDSS). Furthermore, this model is also extending benefits to private medical institutions; in certain coastal cities, private healthcare providers can likewise avail themselves of this advantage.

From a market-wide perspective, the technologies underlying general practice CDSS and grading-oriented CDSS have matured and established viable business models. In contrast, specialty-specific CDSS remains a variable. The ability to implement quality control across certain clinical pathways in hospitals does not necessarily translate into success in more complex fields such as oncology. Moreover, in the exploration of new future markets, these solutions may encounter scenarios where they are not applicable or where data collection proves difficult. This situation presents both risks and opportunities.