Two Years Since NHSA's Establishment: Transforming China's Healthcare System

Today marks the second anniversary of the establishment of the National Healthcare Security Administration.

Two years ago today, the National Healthcare Security Administration (NHSA) officially commenced operations at its headquarters on Yuetaan Beixiao Street in Xicheng District, Beijing. Over the subsequent two years, a series of policies—including healthcare fund supervision, volume-based procurement, adjustments to the national drug reimbursement list, and DRG-based payment reforms—were researched, formulated, and launched from this location, bringing about profound changes to the medical and health industry. As the regulatory authority, the NHSA has emerged as the most prominent innovator within the sector, injecting new growth and imaginative possibilities into the future of healthcare.

VCBeat, through its analysis of 50 major policies and interviews with industry experts, has identified the following reform trajectory pursued by the National Healthcare Security Administration:After strengthening regulatory oversight to ensure the financial sustainability of the basic medical insurance fund, the National Healthcare Security Administration will leverage its role as a payer to drive transformation in healthcare service delivery models. In the future, alongside the establishment of a multi-tiered medical payment system, an innovative healthcare service system will also be developed.

Beyond the pathway, the broader logic lies in:Policy and the power it embodies are not merely coercive or prohibitive; they are also productive. They generate new discourses, new genres, and new objects, and they constitute new practices and new ecologies.

As early as 2014, a report jointly released by Huazhong University of Science and Technology and the People's Publishing House predicted that by 2024, “the basic medical insurance fund would face a severe deficit of RMB 735.3 billion.”

This prediction is well-founded, as the substantial annual increase in healthcare expenditure has become a growing concern for the public.

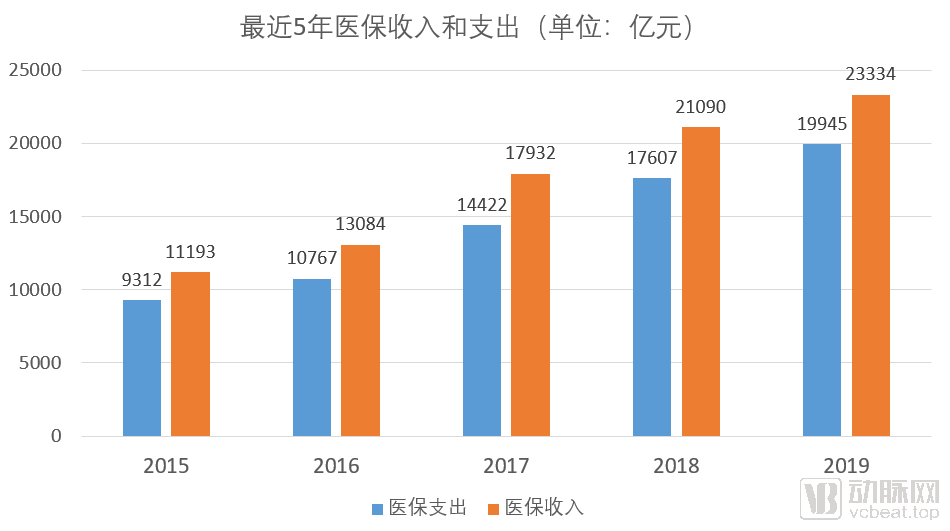

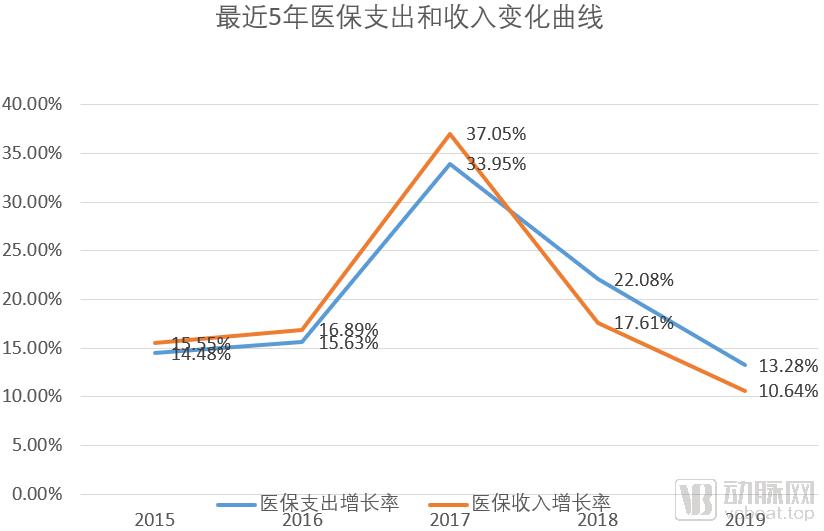

In 2014, the basic medical insurance fund recorded revenues of RMB 968.7 billion and expenditures of RMB 813.4 billion, with mounting financial pressure in the subsequent years. By 2018, the growth rate of medical insurance expenditures reached 22.08%, while the growth rate of revenues stood at 17.61%.The two curves intersected, with the growth rate of medical insurance expenditures surpassing that of medical insurance revenues for the first time.

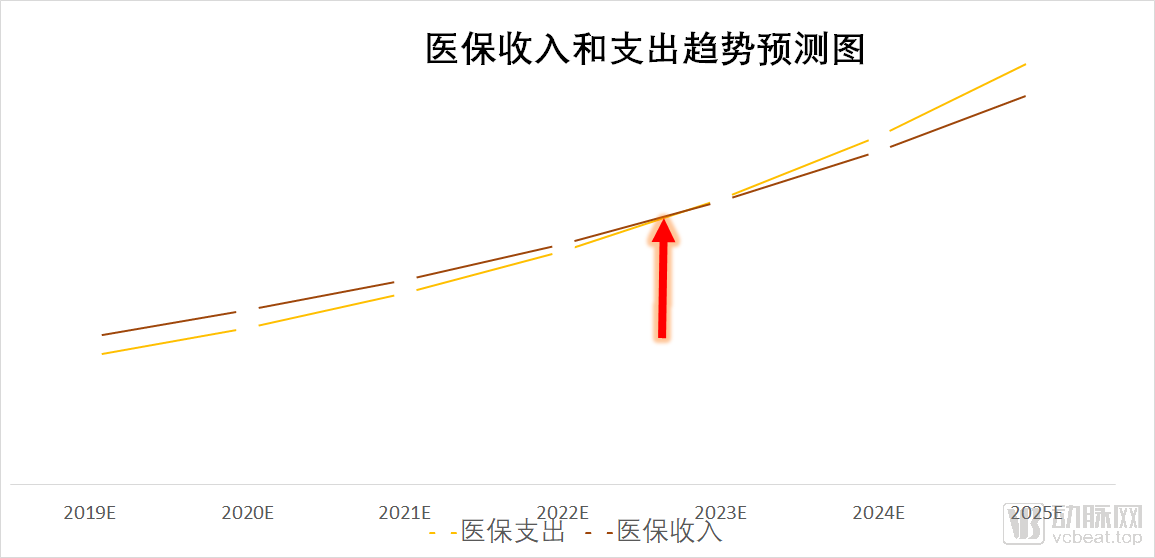

If the 2018 health insurance data (revenue and expenditure figures, revenue growth rate, and expenditure growth rate) are used as constants to calculate future growth trends,Consequently, in 2023, medical insurance expenditures will surpass revenues, marking the onset of a deficit in the operation of medical insurance funds.

Healthcare is vital to the national economy and people’s livelihood, and it bears on the public’s aspiration for a better life. No one wishes to see the two curves cross and then diverge in opposite directions, nor does anyone want such a situation to arise.

Under the previous system, oversight of medical insurance funds was fragmented across four departments. The Ministry of Human Resources and Social Security managed medical insurance for urban employees and urban residents; the National Health and Family Planning Commission administered the New Rural Cooperative Medical Scheme; the Ministry of Civil Affairs oversaw medical assistance programs; and the National Development and Reform Commission regulated medical service and drug pricing. To achieve truly unified management, these functions must be consolidated under a newly established administrative body. Such integration would not only ensure more effective management and regulation of medical insurance funds but also leverage the position of a super-payer to drive industry-wide reforms and other strategic initiatives.

Only by centralizing power can we truly accomplish major undertakings.

Additionally,As healthcare reform enters its deep-water zone, a more powerful fulcrum and focal point must be identified to achieve deeper-level reforms.

Against this backdrop, the National Healthcare Security Administration was established. In March 2018, a major institutional reform of the State Council was launched, introducing top-level design; in May, the National Healthcare Security Administration was officially inaugurated.

The Newly Established National Healthcare Security Administration: What Will It Do?

In early July 2018, the film “Dying to Survive” was released. It garnered enthusiastic public response, with discussions on issues such as exorbitant drug prices trending on social media hot searches and making headlines. Seizing this opportunity shaped by public opinion, the National Healthcare Security Administration (in conjunction with the National Health Commission) issued its first major policy since its establishment: the “Notice on Launching Provincial-Level Special Centralized Procurement of Anti-Cancer Drugs.”

Of course, it may simply be a response to public opinion, or perhaps the two are entirely unrelated.This world is often just like this: things are interconnected yet separate, making it difficult to clearly articulate the relationship between two matters.

Starting with the centralized procurement of anticancer drugs, the National Healthcare Security Administration has launched a comprehensive wave of reforms.

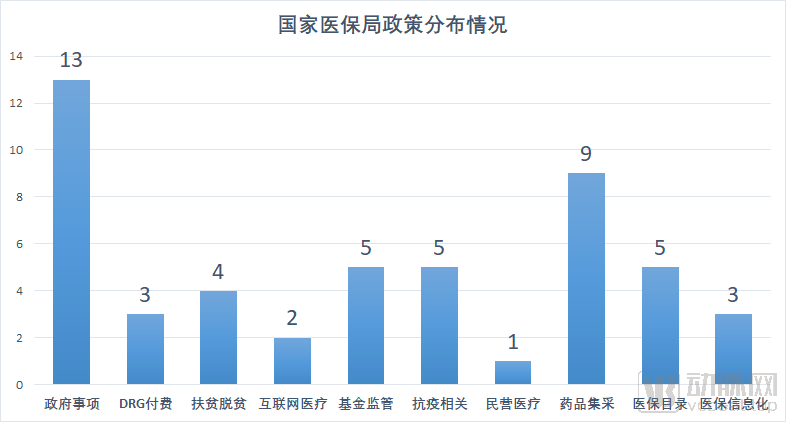

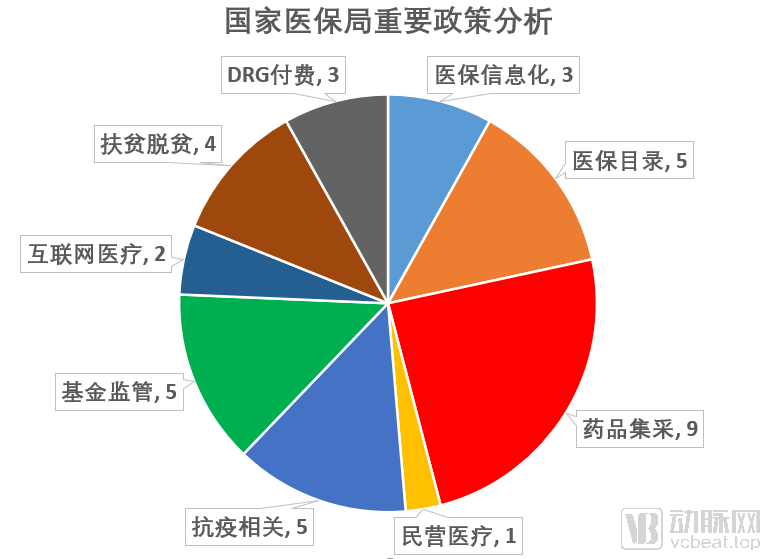

According to the public data published under the “Government Documents” section on the official website of the National Healthcare Security Administration, VCBeat has drawn numerous insights through statistical analysis and classification:

(Note 1: Since its establishment, the “Government Documents” public notice board on the official website of the National Healthcare Security Administration has posted a total of 54 documents. Four of these were issued by other regulatory authorities and are therefore excluded from this statistical analysis. Key policies will be listed and discussed separately in the text. Note 2: Some policies often span multiple domains; the classification results presented in this article may not fully align with the specific scope of each policy. Readers are advised to take note of this.)

In the two years since its official establishment, the National Healthcare Security Administration (NHSA), either independently or in conjunction with other departments, has issued a total of 50 policy documents. Thirteen of these pertain to governmental affairs and work notices, such as the “Notice on Strengthening the Conduct of the Medical Security System” and the “List of Administrative Law Enforcement Matters of the National Healthcare Security Administration (2020 Edition).”

Beyond administrative matters and work notifications, the other 37 major policies have brought profound impacts and significant transformations to the industry.

Drug Centralized Procurement

There are nine policies regarding centralized drug procurement. The purpose of centralized drug procurement is to explore and improve the mechanism for centralized drug purchasing and a market-led drug pricing mechanism, reduce the public’s burden of medication costs, standardize drug distribution order, and enhance medication safety for the public. The National Healthcare Security Administration holds comprehensive authority over payment, supervision, and pricing. Through the “4+7” pilot program, it aims to explore mechanisms for drug price formation.

Judging from the current situation, the effects of the series of policies on centralized drug procurement are significant. Among the initial 31 pilot varieties, 25 were selected. The average price reduction for the selected drugs was 52%, with a maximum reduction of 96%, compared to the lowest procurement prices for the same drugs in the pilot cities in 2017.

According to data from the "2019 Statistical Bulletin on the Development of Medical Security Undertakings" (hereinafter referred to as the "Statistical Bulletin") released by the National Healthcare Security Administration, the preliminary total value of online procurement orders through provincial drug centralized procurement platforms across all 31 provinces (autonomous regions and municipalities) in China reached RMB 991.3 billion by the end of 2019. Of this amount, orders for Western medicines (chemical drugs and biological products) totaled RMB 811.5 billion, while orders for proprietary Chinese medicines amounted to RMB 179.8 billion. The value of orders for drugs covered by basic medical insurance accounted for RMB 832.7 billion, representing 84% of the total online procurement volume.

By the end of 2019, the 25 selected drugs in the pilot regions for the “4+7” centralized volume-based drug procurement program had achieved an average of 183% of their contracted purchase volumes, with the procurement volume of selected drugs accounting for 78% of the total procurement volume for drugs with the same generic names. Following the nationwide expansion of the pilot program, all 25 generic drug varieties were successfully included in the expanded procurement, with prices decreasing by an average of 59%, representing a further 25% reduction on top of the “4+7” pilot prices.

Adjustment of the National Reimbursement Drug List

Closely linked to centralized drug procurement is the adjustment of the National Reimbursement Drug List (NRDL), which involves five policy measures. The NRDL governs 80% of the sales market in public hospitals. For pharmaceutical companies, failure to secure inclusion in the NRDL means losing the market expansion advantages conferred by reimbursement coverage, thereby plunging them into fierce market competition. For consumers, the inclusion of more life-saving and emergency medications in the NRDL will help reduce out-of-pocket expenses.

On August 20, 2019, the National Healthcare Security Administration (NHSA) issued a notice on printing and distributing the “National Basic Medical Insurance, Work-Related Injury Insurance, and Maternity Insurance Drug Catalog,” triggering an earthquake in the industry. This major adjustment to the drug catalog marked the first comprehensive revision since the establishment of the NHSA, as well as a thorough review of the existing catalog entries since the first edition was released in 2000. It came only two years after the previous major overhaul of the medical insurance drug catalog.

Based on the five policies concerning adjustments to the National Reimbursement Drug List (NRDL), the National Healthcare Security Administration aims to normalize the dynamic adjustment of the NRDL, thereby optimizing existing medical resources and maximizing the efficacy of the national healthcare insurance fund.

According to preliminary statistical data, the 2019 edition of the National Reimbursement Drug List (NRDL) included a total of 2,709 Western medicines and Chinese proprietary medicines, comprising 1,370 Western medicines and 1,339 Chinese proprietary medicines. Additionally, 892 types of Chinese herbal decoction pieces with national standards were also included.

Supervision of Medical Insurance Funds

There are also five policies regarding the supervision of medical insurance funds. Supervising these funds is a top priority for the National Healthcare Security Administration (NHSA); how can people’s life-saving money be illegally defrauded or wasted? To this end, through concerted efforts, the NHSA has established a high-pressure stance nationwide against fraud and deception in medical insurance claims. This has led to the implementation of a series of working mechanisms, including clarifying responsibilities, streamlining channels for reporting complaints, and ensuring that identified issues are handled strictly, severely, and promptly. Currently, promotional materials combating medical insurance fraud can be seen in hospitals, communities, and various other public spaces.

According to preliminary statistical data, in 2019, medical insurance departments at all levels conducted on-site inspections of 815,000 designated medical and pharmaceutical institutions. A total of 264,000 institutions found in violation of laws, regulations, or contractual agreements were penalized; among these, 6,730 had their medical insurance agreements terminated, 6,638 received administrative penalties, and 357 cases were referred to judicial authorities. Across various regions, 33,100 insured individuals involved in illegal or non-compliant activities were processed; settlement services were suspended for 6,595 individuals, and 1,183 cases were referred to judicial authorities. Throughout the year, a total of RMB 11.556 billion in funds was recovered.

Throughout the year, the National Healthcare Security Administration organized 69 inspection teams to conduct nationwide unannounced inspections, covering 30 provinces and 149 medical and pharmaceutical institutions, with a total of RMB 2.226 billion identified as suspected illegal and non-compliant funds.

Poverty Alleviation and Eradication

“Building a moderately prosperous society in all respects” is by no means an empty slogan. The National Healthcare Security Administration has introduced four policies specifically focused on poverty alleviation and eradication.

Following the release of the Three-Year Action Plan for Poverty Alleviation through Medical Security (2018–2020) in 2018, additional policies were issued in 2019, including the Guiding Opinions on Resolutely Fulfilling the Critical Tasks of Poverty Alleviation through Medical Security. These documents stipulated that ensuring full coverage of the impoverished population under basic medical insurance, critical illness insurance, and medical assistance programs constitutes a mandatory baseline target.

In poverty alleviation and eradication efforts, further strengthen the comprehensive safeguard function of the triple-tier system. Fully establish a unified basic medical insurance system for urban and rural residents, stabilize expectations for inpatient benefits, and improve outpatient pooling arrangements. Universally enhance the coverage level of critical illness insurance, continue to implement preferential policies for impoverished populations—including a 50% reduction in deductibles and a 5-percentage-point increase in reimbursement rates—and completely eliminate annual payment caps for registered impoverished individuals. Direct medical assistance funds toward deeply impoverished areas to further strengthen the safety-net protection capacity of medical assistance.

According to preliminary statistical data, by the end of 2019, the total number of enrollees in basic medical insurance across all categories reached 1.35436 billion, with coverage consistently maintained at over 95%.

Internet Healthcare

Although only two policies have been issued in the field of internet healthcare, each policy’s introduction has ushered in a new era for the industry.

It is widely believed in the industry that the lack of integration with medical insurance payment systems will largely become the biggest obstacle to the development of the internet healthcare sector.

For innovative medical service models such as internet-based healthcare, which involve complex regulatory issues, the National Healthcare Security Administration has adopted a strategy of steadily advancing reforms, progressing from initial breakthroughs to broader implementation.

On August 30, 2019, the National Healthcare Security Administration issued the "Guiding Opinions on Improving Pricing and Medical Insurance Payment Policies for 'Internet+' Medical Services." The policy stipulates that fair pricing and payment policies shall be implemented for both online and offline medical services. "Internet+" medical services provided by designated medical institutions, which are identical in content to offline medical services covered by medical insurance payment and adhere to the corresponding charging standards of public medical institutions, shall be included in the scope of medical insurance payment and reimbursed in accordance with regulations after completing the requisite filing procedures.

During the pandemic, internet healthcare demonstrated significant value. Major platforms and physical hospitals successively launched online fever clinics, later expanding online consultation services to other departments. These initiatives first helped alleviate public panic related to the epidemic, then guided patients to seek medical care online, thereby avoiding cross-infection risks associated with in-person hospital visits. Additionally, they ensured continuity of care for chronic disease patients, including follow-up consultations and medication management.

On March 2, 2020, the National Healthcare Security Administration and the National Health Commission jointly issued the “Guiding Opinions on Promoting ‘Internet+’ Medical Insurance Services During the Prevention and Control of the COVID-19 Pandemic,” further advancing the inclusion of internet-based diagnosis and treatment services into medical insurance reimbursement.

The policies cover a wide range of areas, each exerting a profound impact on the industry; therefore, a detailed analysis of each will not be provided here.In the following section, this article will draw on an interview with Dr. Liu Zhichen, a senior strategic expert in the broader health sector, to explore issues such as the reform logic of the National Healthcare Security Administration and the evolving trends of China’s future healthcare payment system.

As the financial pressure on the medical insurance fund intensifies, the National Healthcare Security Administration has implemented a series of measures to ensure the stable and sustainable operation of medical insurance funds. The majority of the 50 policies mentioned above were formulated around these management objectives.

Dr. Liu Zhichen believes that, based on the policy logic since its establishment, the National Healthcare Security Administration’s primary measures or first-phase tasks are “cost containment” and “revenue expansion.” “Cost containment” refers to reducing expenditures from the medical insurance fund, while “revenue expansion” aims to establish a multi-tiered medical security system, thereby “expanding the scope of coverage provided by the medical insurance fund through social forces.”

In terms of cost containment and expenditure control, there are two primary levels. The first focuses on fund supervision to eliminate fraudulent activities involving medical insurance funds. In June 2019, the National Healthcare Security Administration officially issued the “Notice on Launching the ‘Two Pilots and One Demonstration’ Initiative for Medical Insurance Fund Supervision,” along with a list of pilot cities. It has actively explored innovative approaches to fund supervision, including the establishment of a credit system for fund regulation and the implementation of intelligent monitoring systems for medical insurance, aiming to achieve refined oversight of medical insurance funds and the goal of cost containment.This segment’s contribution to overall costs has been increasing year by year.

In 2018, a total of RMB 1.008 billion in medical insurance funds was recovered; in 2019, the full-year recovery amounted to RMB 11.556 billion. It is evident that efforts to combat medical insurance fraud will continue to intensify in the future.However, the recovery of fraudulently obtained medical insurance funds contributes minimally to cost containment, given the nearly RMB 2 trillion in annual medical insurance fund expenditures.

The most significant contribution to cost containment lies at the second level: adjusting the payment mechanisms of medical insurance funds and establishing a composite payment system reform to drive the transformation of healthcare service models, thereby achieving more substantial goals in cost control and expenditure reduction. This is primarily manifested in two aspects. First, regarding the control of inpatient expenses, the focus is on driving changes in payment methods with Diagnosis-Related Groups (DRG) as the core. This approach compels medical institutions and physicians to shift away from previous fee-for-service practices that often led to over-treatment, moving instead toward standardized, clinically pathway-guided care focused on cost management. By establishing positive incentive mechanisms, medical institutions and physicians are empowered to autonomously achieve the goal of controlling the growth of inpatient costs.

Second, in light of the weaknesses in China’s public health system exposed by the current epidemic, the state will gradually strengthen the role of primary healthcare institutions in health management and promote the establishment of an integrated healthcare service system. From the perspective of payment mechanisms, the National Healthcare Security Administration will actively drive reforms such as bundled payments for medical consortia and county-level medical communities. By integrating medical care with health security and emphasizing preventive measures prior to clinical diagnosis and treatment, these payment incentives will facilitate a transition from a traditional treatment-centric model to a prevention-oriented healthcare service model.

Under the previous fee-for-service payment system, excessive medical treatment was prevalent, as doctors and healthcare institutions could only achieve revenue growth by ordering more procedures and tests. Meanwhile, the traditional health insurance reimbursement model primarily focused on inpatient care; for instance, many conditions treated in outpatient settings were not covered, forcing patients to seek hospitalization solely for reimbursement purposes, which also led to a waste of medical resources. Additionally, there were issues with prescriptions written during hospital stays. Since the practice of subsidizing healthcare providers through drug sales had not been completely eradicated, physicians lacked the incentive to control medical costs.

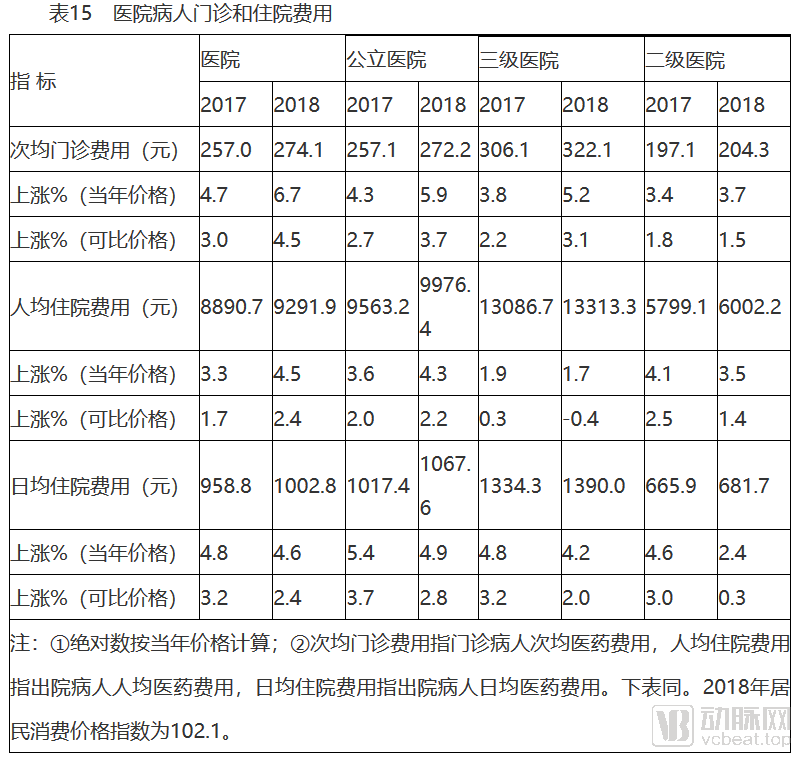

The above is the Statistical Bulletin on the Development of China’s Health and Wellness Undertakings in 2018 (the 2019 edition has not yet been officially released). From this, we can see that inpatient expenses are several times higher than outpatient expenses, which also constitute the largest portion of medical insurance fund expenditures. Effective control over these costs will significantly reduce expenditures from the medical insurance fund.

Policies such as DRG-based payment, fund supervision, and volume-based procurement introduced by the National Healthcare Security Administration adhere to the logic of “cost containment.”

However, Dr. Liu Zhichen believes that “in the design of future payment mechanisms by the National Healthcare Security Administration, further institutional frameworks are needed to truly align payment reform with incentives for healthcare institutions and physicians, thereby fostering their proactive participation in the transformation of healthcare service delivery models through the establishment of positive incentive mechanisms.”

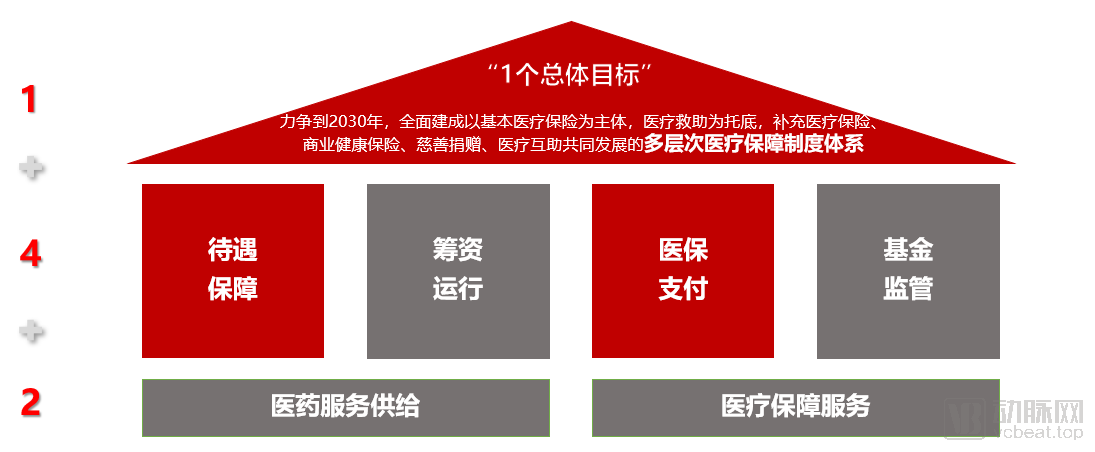

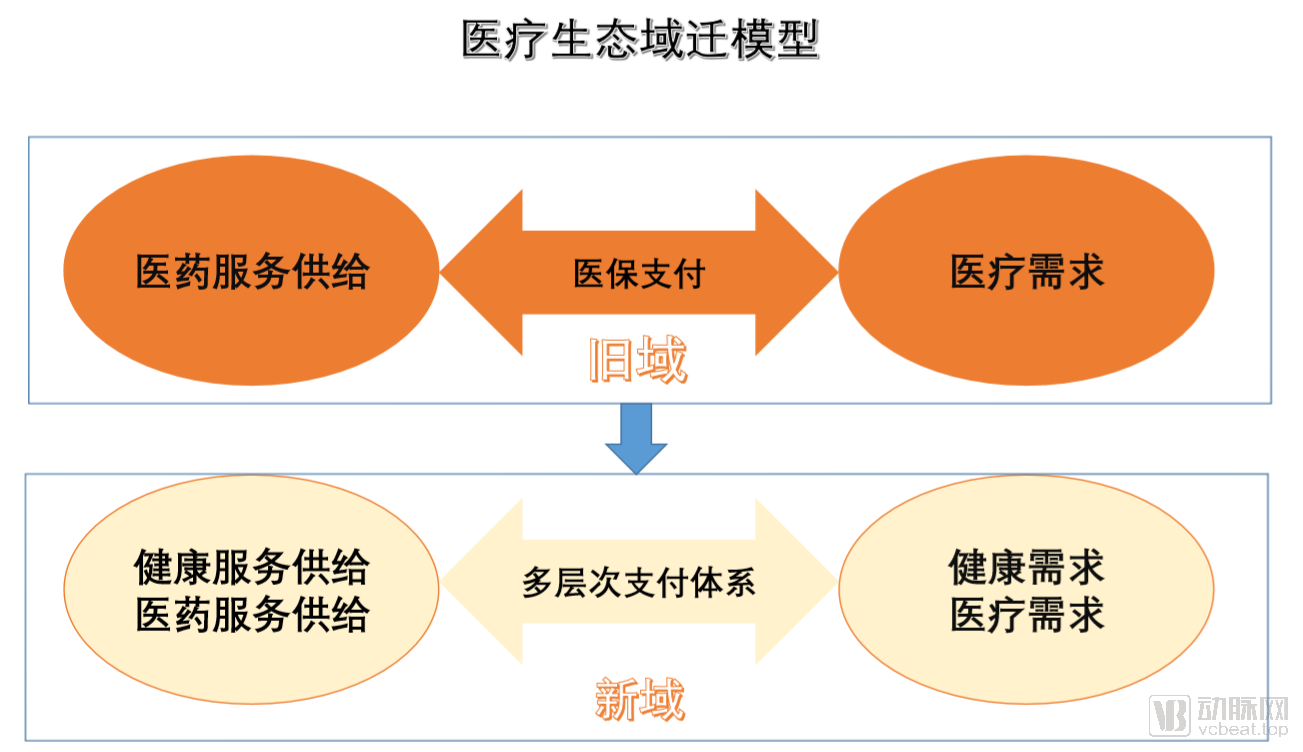

On the revenue side, regulators, including the National Healthcare Security Administration, have introduced top-level designs."To establish a multi-tiered healthcare security system in which basic medical insurance serves as the mainstay, medical assistance provides a safety net, and supplementary medical insurance, commercial health insurance, charitable donations, and mutual medical aid develop in concert."

On March 5, 2020, the “Opinions on Deepening the Reform of the Medical Security System,” issued by the Central Committee of the Communist Party of China and the State Council, sparked significant repercussions. Many industry insiders have hailed this policy as a programmatic document that will set the tone for China’s healthcare reform over the next decade. The policy proposes an overall reform framework of “1+4+2.”

(Source: Provided by Dr. Liu Zhichen)

Starting from this roadmap, we can see the policy logic of “open source.”

"In the multi-tiered medical security system, basic medical insurance serves as the mainstay, while commercial health insurance is expected to become the largest payer of supplementary medical insurance within the 'multi-tiered security system' in the future."

Over the past one to two years, regulators have introduced multiple policies to vigorously promote the development of commercial health insurance. From the “New Regulations on Health Insurance” to the “Opinions on the Development of Commercial Insurance in the Social Services Sector,” these policies have provided encouragement and support for the growth of commercial health insurance.

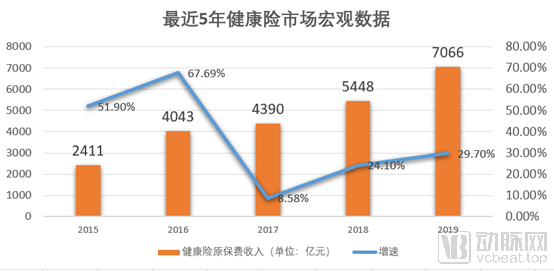

Benefiting from supportive policies and a surge in demand, commercial health insurance has entered a phase of rapid development, with the compound annual growth rate (CAGR) of its market size exceeding 30% over the past five years. Based on this growth trajectory, the market size of health insurance is projected to approach the trillion-yuan mark in 2020.

Currently, commercial health insurance claims account for less than 4% of total healthcare expenditure, indicating substantial growth potential for the health insurance sector in the future.

Driven by the dual engines of expanding revenue sources and controlling costs, the operational trajectories of health insurance payments and revenues will ultimately be reversed.

Once the initiatives to increase revenue and reduce expenditures have been implemented with relative success, the National Healthcare Security Administration’s next phase of work may involve leveraging its role as a “super-payer” to drive a transformation in healthcare service delivery models, thereby inducing structural shifts and domain migration across the entire healthcare ecosystem. In retrospect, several years from now, the reform of healthcare payment mechanisms will undoubtedly be credited as a pivotal factor in the overall success of China’s healthcare reforms.

In the short to medium term, the following areas will undergo significant changes, which may also present opportunities for industrial innovation.

First is internet healthcare. Since the outbreak of the pandemic this year, the trend toward online medical services has been very pronounced, ushering in significant development opportunities for internet healthcare. In Liu Zhichen’s view,Internet healthcare this year differs from our previous understanding. In the past, internet healthcare primarily referred to third-party platforms such as Ping An Good Doctor, WeDoctor, and Chunyu Doctor. However, the current wave of internet healthcare is driven more by the government and public hospitals, focusing on the digital transformation of traditional medical services. In the future, online services will be directly integrated with medical insurance coverage.

However, the full integration of internet-based healthcare with medical insurance still faces a series of regulatory challenges. How should online services be priced? How should payments be processed? How can it be determined whether a consultation is an initial visit or a follow-up? How should online services be regulated? And how can the quality of online services be evaluated? These issues urgently need to be addressed.

Next is medical big data.Managing personal health data across the entire lifecycle is a major trend in healthcare, but the lack of open and integrated medical data hinders many initiatives. For instance, without access to comprehensive individual medical records, health insurance companies struggle with actuarial calculations, risk control, and product development. This has led to a concentration of commercial health insurance products in critical illness coverage (such as million-yuan medical insurance) and high-end health plans, resulting in a certain degree of disconnection with basic medical insurance. However, severe and critical illnesses are merely statistical outliers under the law of large numbers; common and chronic diseases represent the norm in healthcare.

Liu Zhichen believes that future issues regarding medical data should move toward a “separation of three powers,” namely, clearly defining the producers, regulators, and users of medical data, so that all participants in the industry ecosystem can assume their proper roles.

Finally, health management.Health management utilizes non-medical approaches to help individuals achieve a state of comprehensive physical and mental well-being. According to data released by Kaiser Permanente in the United States, medical care accounts for only 10%–20% of the factors influencing health, whereas living environment, lifestyle, and other determinants constitute 80%–90%.

From the perspective of top-level design by regulators, including the National Healthcare Security Administration, multiple policies have clearly advanced the concept and implementation of health management. For instance, the recently issued “Notice on Regulating Health Management Services Provided by Insurance Companies (Draft for Comment)” formulated by the China Banking and Insurance Regulatory Commission explicitly outlines the content and scope of health management services that insurers are permitted to offer.

Although not yet officially released, it has already revealed the future direction of industry development. Whether through the future coordination of national medical insurance funds and public health funds with greater emphasis on primary care, or through commercial health insurance supporting the provision of health management services, it is evident that, with the successive introduction of national policies, a health security mechanism shifting its focus from disease treatment to individual health and prevention is gradually taking shape and being put into practice.