Post-Tianzhihang IPO: Emerging Fields for the Next Surgical Robotics Unicorns

Author: Daotong Investment

VCBeat Note: On June 3, the China Securities Regulatory Commission (CSRC) announced its approval of the registration for the initial public offering (IPO) of Beijing Tinavi Medical Technologies Co., Ltd. (hereinafter referred to as “Tinavi”) on the STAR Market. Tinavi specializes in the research and development, manufacturing, sales, and services of orthopedic surgical navigation and positioning robots. It is the first company to obtain a Class III medical device registration certificate for orthopedic surgical robots issued by the China Food and Drug Administration (CFDA).

Tinavi Medical Technologies’ listing has further bolstered domestic capital markets’ confidence in surgical robots. Surgeries performed with robotic assistance offer greater precision, reduced blood loss, and faster patient recovery. Although Intuitive Surgical has long dominated the global surgical robot market, the competitive landscape continues to see new entrants. Industry giants such as Medtronic, Johnson & Johnson, and Stryker have all entered the field, while a wave of startups has emerged in China.

What new trends will emerge in the medical robotics industry, and which sectors are poised to produce dark horses? VCBeat (WeChat ID: vcbeat) has compiled and edited the “Research Report on the Surgical Robotics Industry” by DaoTong Investment. DaoTong Investment focuses on early-stage investments in the healthcare sector. In early 2017, it invested in Hangzhou Shuchuang, a surgical robotics company with backgrounds from Intuitive Surgical. Over the past few years, Shuchuang has achieved a series of R&D milestones, completed multiple subsequent funding rounds, and secured hundred-million-yuan-level financing from Sinopharm China International Capital Corporation and Zheshang Venture Capital at the end of 2019. Through deep involvement in and companionship with Shuchuang’s growth, DaoTong has also closely observed the industry’s development and changes over recent years. The following is a summary of the key points:

Core Views:

1.The development of the medical robotics industry is an inevitable trend.Against the backdrop of global population aging and a severe future shortage of healthcare professionals, intelligent medical robots will become the most critical solution to address the imbalance between supply and demand. Over the past four years, China’s medical robot market has grown more than tenfold.

2. The medical robotics market is the second-largest robotics market globally, with the surgical robotics segment accounting for the largest share within it. Surgical robots represent the next generation of surgical techniques, offering patients less trauma and shorter postoperative recovery times.

3. The “equipment + consumables + services” model for surgical robots can form a self-sustaining commercial loop, with consumables accounting for more than 50% of the surgical robot market share.

4. From a technical perspective: Surgical robots have entered the natural orifice stage, including vascular intervention and bronchoscopic surgical robots, with future expansion potential to the urethra, anus, and other areas; from a product form perspective: miniaturization and specialization are the development trends of surgical robots.

5. For surgical robotics companies: Developing the equipment is merely the first step in a long journey. From supporting consumables, regulatory compliance and patents, to training and the accumulation of clinical cases, a successful robotics company must continuously build an ecosystem around its devices.

From an industry perspective, the development of the medical robotics sector is an inevitable trend. Against the backdrop of global population aging and a severe future shortage of healthcare professionals, intelligent medical robots represent the most critical solution to addressing the imbalance between supply and demand.

From the current perspective, three major factors are driving the demand for medical robots. The first is population aging. In 2015, the global population aged 60 and above was approximately 901 million, and it is projected to reach 1.4 billion by 2030. In China, the population aged 60 and above will reach 248 million in 2020, accounting for 17% of the total population. Over the next two decades, China will enter a period of rapid aging, with the proportion of people aged 60 and above expected to exceed 20% by 2040.

Second is the scarcity of medical resources. According to a WHO report, there will be a global shortage of approximately 12.9 million healthcare workers by 2035. Statistics from the Chinese Nursing Association indicate that China currently faces a shortfall of at least one million nurses. A study by the China Academy of Social Management projects that by 2020, the number of semi-disabled elderly individuals in China would reach 68.52–75.90 million, while the disabled elderly population would reach 5.99–6.74 million. The demand for elderly care assistants was estimated at 6.57–7.31 million positions, yet only slightly over 50,000 certified caregivers were available at that time.

Third, there is growing demand for high-quality healthcare. Medical robots offer advantages in minimally invasive procedures, including reduced bleeding, greater precision, and faster recovery. As public perceptions shift and disposable income rises, medical robots will gain wider acceptance. According to Trading Economics forecasts, China’s per capita disposable income was projected to reach $6,606 by 2020.

Surgical Robots Are the Next Generation of Surgical Techniques

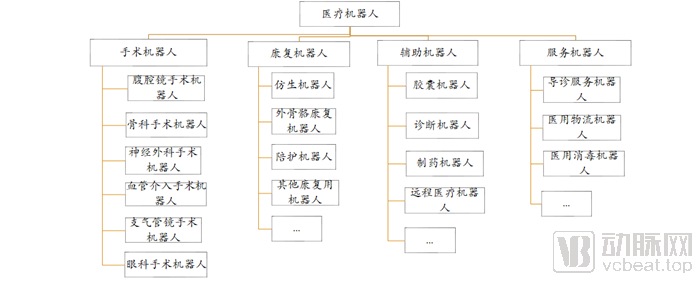

According to the International Federation of Robotics (IFR) standards, medical robots can be categorized into four major types: surgical robots, rehabilitation robots, assistive robots, and service robots. According to forecasts by Boston Consulting Group, the global medical robot market is projected to reach $11.4 billion in 2020, making it the second-largest robotics market. China’s medical robot market grew more than tenfold over the four-year period from 2016 to 2020; however, its current overall market size remains only one-tenth of the global total.

Among these, surgical robots will account for the largest market share, with consumables comprising more than 50% of the surgical robot market.

Surgical robots represent the next generation of surgical practice. Driven by technological advancements, they enable shorter learning curves for surgeons and more standardized surgical outcomes, while simultaneously minimizing patient trauma and accelerating postoperative recovery. The business model integrating robotic equipment, consumables, and services can form a self-sustaining commercial loop, which explains why major medical device giants are willing to pay premium prices to acquire robotics-related targets.

Surgical robots can be classified by procedure type into: laparoscopic surgical robots (urology, gynecology, general surgery, etc.), orthopedic surgical robots (spine, joint, etc.), neurosurgical robots, vascular interventional surgical robots, bronchoscopic surgical robots, and ophthalmic surgical robots, among others.

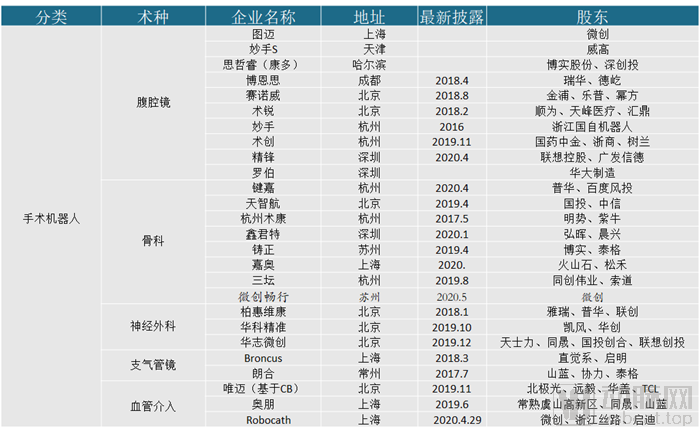

Domestically Produced Surgical Robot Project

From the perspective of the domestic market, China has moved past the early stage of market education, and the clinical community has fully recognized the value of surgical robots. Currently, what various medical departments lack are effective, stable, and cost-effective solutions.

From a technical perspective: Surgical robots have entered the stage of natural orifice procedures, including vascular intervention and bronchoscopic surgical robots, which fall within the scope of natural orifice applications. In the future, this could extend to the urethra, anus, and other areas.In terms of product form: miniaturization and specialization are the development trends of surgical robots.

Starting a business in the field of surgical robotics places exceptionally high demands on the founding team’s technical reserves, fundraising capabilities, regulatory and patent application expertise, and familiarity with global supply chains. From R&D prototyping and clinical trials to production and sales, failure at any stage could render substantial prior capital investments futile. For early-stage startups, establishing a robust global patent portfolio can help mitigate these risks to a certain extent.

It also serves as a reminder to all entrepreneurs in this field: developing the device is merely the first step in a long and arduous journey. From supporting consumables, regulatory compliance, and patents to training and the accumulation of clinical case studies, a successful robotics company must continuously build an ecosystem around its device.

As a leading medical investment institution in China, DaoTong Investment remains bullish on the substantial growth potential of surgical robots and looks forward to supporting more outstanding entrepreneurs in this field.

Industry Leader Case Study:

Intuitive Surgical:Intuitive Surgical’s da Vinci surgical robot system holds a near-monopoly in the field of laparoscopic surgical robots, with a market capitalization reaching $60 billion. In 2019, Intuitive Surgical’s business revenue reached $4.4 billion, a 22% increase from 2018. Of this, 72% was recurring revenue, including accessories and consumables, services, and leasing, while the remaining $1.3 billion came from equipment sales.

In 2019, the global volume of surgeries performed using the da Vinci Surgical System reached 1.229 million, representing an 18% increase from 2018, with the cumulative number of procedures reaching 7.2 million. In 2019, 1,119 da Vinci surgical robot systems were sold, a 21% increase compared to 2018. As of December 31, 2019, a total of 5,582 da Vinci systems had been installed worldwide.

2018 Data from China: 84 hospitals installed 102 da Vinci Surgical Robot Systems, with a cumulative total of 120,000 procedures performed. The da Vinci Surgical Robot System is classified as a Class B large-scale medical equipment, requiring hospitals to obtain configuration approval from the provincial health commission. According to the "Notice on the Planning of Large-Scale Medical Equipment for 2018-2020" issued by the National Health Commission, the national planned allocation of surgical robots was set to reach 197 units by the end of 2020.

Laparoscopic Surgical Robot:

Cambridge Medical Robotics:

A representative startup in the emerging field of laparoscopic surgical robots, founded in 2014, obtained CE certification in March 2019 and completed its first batch of 30 surgical procedures in May of the same year. It is currently in the process of seeking FDA approval. In September 2019, the company closed its Series C financing round, raising $240 million, marking the largest private equity financing deal in the European medical technology sector to date.

Hangzhou Shuchuang Robotics Co., Ltd.:Established in November 2016 and headquartered in Hangzhou, China, the company operates a 40,000-square-foot production and assembly facility in Vizag, Andhra Pradesh, India, where it benefits from special tariff preferential policies granted by the Indian government. It also maintains a 4,300-square-foot R&D center in San Jose, USA. Currently, the company is conducting exploratory cadaveric clinical studies in India, with plans to subsequently launch global multicenter clinical trials. The founder, a cardiac surgeon, participated in the early clinical trials of the da Vinci Surgical System, has performed over 1,400 cardiac surgical procedures using the da Vinci system, and has trained more than 350 robotic surgery teams, pioneering numerous cardiac surgical procedures worldwide. Since its inception, the company has secured multiple rounds of financing; in late 2019, it completed a Series B financing round worth hundreds of millions of yuan, led by Sinopharm Capital and Zheshang Venture Capital.

Representative Companies in Sub-sectors – Orthopedic and Neurosurgical Surgical Robots:

Medtech ROSA: Founded in France in 2002, the ROSA robotic neurosurgical navigation system received FDA approval in 2009, and its spinal surgery navigation system was approved by the FDA in 2016. In 2016, the ROSA system was adopted by more than 20 hospitals across Europe and the United States. That same year, Zimmer Biomet (a global leader in orthopedic implants, with $7.09 billion in sales in 2018) acquired a 59% equity stake in the company for $132 million in cash. In March 2019, the ROSA system cleared the US FDA 510(k) process, enabling its application in brain, knee, and spinal procedures. It is the world’s only surgical robotic navigation and positioning system approved for use across all three anatomical regions.

Mazor Robotics: Founded in Israel in 2000, it is applied in spinal surgery and neurosurgery. Its first device received FDA approval in 2011. As of December 2019, 200 units had been sold worldwide, with over 40,000 procedures performed. In 2019, it was acquired by Medtronic for $1.64 billion in cash; prior to this, Medtronic already held an 11% equity stake in the company.

Mako Rio: Founded in the United States in 2004, it is applied in orthopedics, including joints and hip bones. In 2013, it was acquired by Stryker, a global orthopedic giant, for $1.68 billion. As of 2018, Mako had installed 642 units globally, with 523 units in the United States.

Beijing Tinavi Medical Technologies Co., Ltd.“Tirobot Tiangji” received the Class III medical device registration certificate issued by the CFDA in November 2016, becoming the first company in China to industrialize orthopedic robots. By the end of 2019, the company’s products had been used in a cumulative total of 5,371 surgeries, covering more than 20 provinces, municipalities directly under the central government, and autonomous regions, and were applied in over 74 Grade A tertiary hospitals, specialized orthopedic hospitals, and other medical institutions.

Huazhi Minimally Invasive Medical Technology(Beijing) Co., Ltd.: Its controlled subsidiary, Tianjin Huazhi Computer Application Co., Ltd., received approval for its “frameless stereotactic instrument” in 2008 and has secured investments from Tasly, Tongsheng, SDIC Chuanghe, and Legend Capital.

Beijing Baihui Weikang Technology Co., Ltd.: In April 2018, the “Neurosurgical Navigation and Positioning System” received regulatory approval; the company secured investments from Yari Capital, ZhenFund, Puhua Capital, and others.

Huake Jingzhun (Beijing) Medical Technology Co., Ltd.: In December 2018, its “Neurosurgical Navigation and Positioning System” received regulatory approval. This system stems from a collaborative R&D project spanning over a decade between Tsinghua University and the neurosurgery departments of several Grade 3A hospitals. The company has secured investments from Kaifeng Capital, Huachuang Capital, and others.

Representative Companies in the Sub-sector - Bronchoscopy Surgical Robots:

Auris Monarch: Founded in 2007, it received FDA approval in March 2018. In February 2019, Ethicon, a wholly-owned subsidiary of Johnson & Johnson, announced the acquisition of Auris Health for $3.4 billion in cash, with an additional $2.35 billion payable upon the achievement of certain milestones. Meanwhile, Fred Moll, founder of Auris, will serve as the head of Ethicon’s surgical robotics division. Auris also owns the Mallegan peripheral vascular robot, developed by Hansen Medical, which it had previously acquired.

Intuitive Surgical Lon:In 2018, Intuitive Surgical made a strategic investment of $15 million in Broncus, and the two parties officially became strategic partners. Intuitive Surgical was granted exclusive global rights to use Broncus’s whole-lung navigation technology for the development of its robotic systems for the diagnosis and treatment of pulmonary diseases. Broncus is a company focused on the research, development, and manufacturing of technologies for the diagnosis and treatment of lung diseases. It primarily develops, produces, and sells precise, minimally invasive interventional diagnostic and therapeutic products for lung conditions such as lung cancer and chronic obstructive pulmonary disease (COPD), based on an augmented reality whole-lung navigation technology platform. The company has obtained more than 73 patents worldwide.

In 2019, Intuitive Surgical’s Ion endoluminal system, a robotic bronchoscope for lung cancer biopsy, received FDA approval.

Representative Companies in the Niche Sector - Vascular Interventional Surgical Robots

Corindus Vascular Robotics, Inc. (AMEX: CVRS): Founded in 2011, the company was formerly known as Your Internet Defender Inc. (“YIDI”). After undergoing multiple restructurings and acquisitions, it adopted its current name in 2014 and is headquartered in Massachusetts, USA. Its CorPath GRX system received FDA 510(k) clearance in October 2017, with the first commercial installation completed by the end of 2017. As of the end of 2018, 52 systems had been installed worldwide. In August 2019, Siemens Healthineers reached an acquisition agreement with Corindus Vascular Robotics. Under the terms of the agreement, Siemens Healthineers acquired all fully diluted shares of Corindus for $4.28 per share in cash, for a total transaction value of $1.1 billion.

The Corindus CorPath GRX coronary intervention surgical robot can effectively reduce the radiation exposure received by physicians during each interventional procedure by more than 95%. For patients, its precise operation and preoperative planning can effectively reduce their radiation exposure by 20%.

Corindus CorPath GRX, which began with coronary interventions, completed its first robot-assisted neurointerventional procedure in Toronto on November 5, 2019.

Representative Companies in Sub-sectors - Ophthalmic Surgical Robots:

Preceyes Bv: In June 2018, surgery was performed on 12 patients with macular holes, jointly conducted by the Oxford Eye Hospital, affiliated with the University of Oxford, UK, and Preceyes B.V. from Eindhoven, the Netherlands.

Vitreoretinal surgery primarily faces three challenges: 1. Precision requirements: The ideal surgical operation precision is required to be 10 micrometers (the diameter of a human hair is approximately 80 micrometers, and the amplitude of a surgeon's hand tremor is generally 100 micrometers);

2. Subtle tactile feedback during surgery: The force exerted by ophthalmic surgical instruments on the retina is less than 15 millinewtons (1 N = 1000 mN; the gravitational force of an egg is approximately 0.5 N);

3. Limited Visual Feedback During Surgery: Surgical procedures take place within the eyeball, requiring fiber-optic illumination. Due to the transparency of the retina, the surgical field is poorly visualized. The procedure necessitates multiple instruments and involves a complex workflow, typically performed by the lead surgeon with assistance from several assistant surgeons.

Experimental results showed that both procedures achieved a 100% success rate, with no significant difference in efficacy. However, robot-assisted surgery currently requires longer operative time, with an average total duration of 55 minutes, compared to an average of 31 minutes for manual surgery.