Prospectus of Artificial Joint Industry Research Report: Market Overview and Product Portfolio

WinX Capital

Investment Institutions in the Greater Health Field

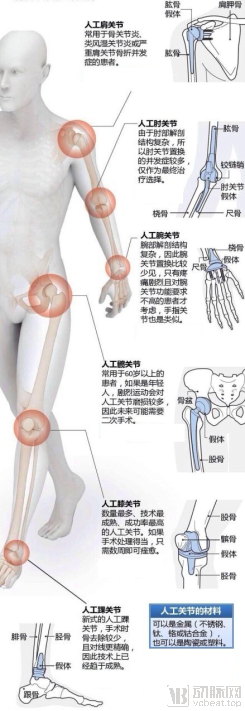

With the accelerating aging of the global population, degenerative osteoarthropathy in the elderly has become a common and frequently occurring disease. Once structural changes occur in the joints due to various causes, pharmacological therapy alone can only partially alleviate pain symptoms and is difficult to improve joint function. In contrast, artificial joint replacement can achieve the goals of pain relief, joint stabilization, deformity correction, and improvement of joint function. To date, prostheses have been developed for the knee, hip, elbow, shoulder, finger, and toe joints.

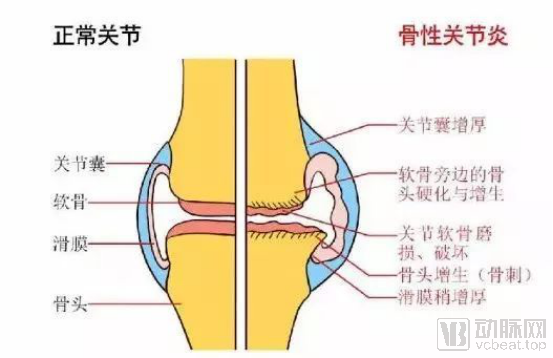

Osteoarthritis is a degenerative disorder characterized by the degradation and damage of articular cartilage, along with reactive hyperplasia at the joint margins and subchondral bone. It is caused by multiple factors, including aging, obesity, mechanical wear and tear, trauma, congenital joint abnormalities, and joint deformities. Also known as osteoarthrosis, degenerative arthritis, senile arthritis, or hypertrophic arthritis, its clinical manifestations include joint redness, swelling, warmth, pain, functional impairment, and deformity. In severe cases, it can lead to joint disability and adversely affect patients' quality of life. Osteoarthritis was projected to become the fourth leading cause of disability by 2020, imposing a substantial economic burden on patients, families, and society.

Osteoarthritis is primarily characterized by degenerative changes in articular cartilage and secondary bone hyperplasia. It is more common in middle-aged and elderly individuals, with a higher prevalence in women than in men. The condition predominantly affects weight-bearing joints, such as the knees, hips, spine, and finger joints. In China, there are over 100 million patients with arthritis, and this number continues to rise. Statistics show that 50% of individuals aged 50 and older suffer from osteoarthritis, while the prevalence reaches 80% among those aged 75 and above.

Artificial joint replacement is a highly mature and effective surgical procedure for treating end-stage severe osteoarthritis and advanced knee diseases. It includes total hip arthroplasty (THA), total knee arthroplasty (TKA), unicompartmental knee arthroplasty (UKA), and patellofemoral joint arthroplasty (PFJ), with the specific approach determined by the location of the lesion, the degree of lower limb alignment deformity, and the surgeon’s experience.

Artificial joint replacement utilizes prostheses made from materials such as metals, ultra-high-molecular-weight polyethylene, and ceramics. These artificial joint implants are manufactured according to the morphology, structure, and function of human joints and are surgically implanted into the body to replace the function of diseased joints, thereby alleviating joint pain and restoring joint function. Procedures include total shoulder arthroplasty, total elbow arthroplasty, total wrist arthroplasty, total hip arthroplasty, total knee arthroplasty, and total ankle arthroplasty. Currently, knee and hip replacements are the two most common types of artificial joint replacement surgeries, with ten-year success rates exceeding 90%. Moreover, more than 80% of patients can use their implants normally for over 20 years, often for the remainder of their lives. In addition, joint replacements for the shoulder, elbow, and ankle are continuously advancing, yielding favorable medium- and long-term outcomes.

Total Hip Arthroplasty (THA) is one of the most common joint replacement procedures. Due to the high frequency of use, the human hip joint is more susceptible to degenerative changes compared to other joints. The primary indications for hip arthroplasty are:

1. Fractures: including intertrochanteric femoral fractures, femoral neck fractures, femoral head fractures, and even some acetabular fractures;

2. Osteoarthritis: Including osteoarthritis caused by various factors, and patients' pain;

3. Bone tumors: including bone tumors of the femoral head, neck, greater trochanter, or the acetabular side near the hip joint.

Additionally, factors such as alcohol consumption, use of hormonal medications, and trauma can lead to avascular necrosis of the femoral head (a type of osteoarthritis). When hip disease progresses to a stage characterized by severe symptoms and loss of function, total hip arthroplasty is required. This procedure involves surgically implanting a femoral stem into the proximal femur; the stem features a metallic ball that serves as the artificial femoral head. An acetabular cup is securely fixed into the acetabulum, and the metallic ball is articulated within the liner of the acetabular cup, thereby replacing the degenerated or necrotic femoral head structure and restoring hip joint function.

Total Knee Arthroplasty (TKA) is the primary method for treating severe knee disorders, alleviating knee pain, and reconstructing knee function. The main indications for knee arthroplasty are:

1. Osteoarthritis: Including degenerative knee osteoarthritis (OA), rheumatoid arthritis (RA), ankylosing spondylitis (AS), and other knee joint lesions caused by non-infectious arthritis; degenerative knee osteoarthritis accounts for 70–80% of total knee arthroplasty cases;

2. Post-traumatic osteoarthritis: Osteoarthritis following severe trauma involving the articular surface, such as cases with significantly impaired function due to failure to restore the articular surface after comminuted plateau fractures, and secondary osteoarthritis resulting from meniscal injury or resection; also includes cases of extensive osteochondral necrosis or other lesions of the knee joint that cannot be repaired by conventional surgical methods.

3. Cases where satisfactory reconstruction of joint function cannot be achieved after resection of tumors involving the knee joint surface. For example, in patients with bone tumors of the distal femur or proximal tibia who are candidates for limb-salvage surgery, artificial knee joint replacement using specialized prostheses may be performed following en bloc resection of the tumor-bearing segment.

Artificial joint replacement remains a mature and effective treatment for end-stage osteoarthritis. With advancements in prosthetic design, surgical techniques, and perioperative management, patient satisfaction following artificial joint replacement has continued to rise.

The incidence of orthopedic diseases is highly correlated with age. As individuals grow older, the probability of developing orthopedic conditions such as fractures, scoliosis, spondylosis, arthritis, and joint tumors increases significantly. Furthermore, with rising life expectancy, the elderly population will continue to expand, leading to sustained growth in the high-risk demographic for orthopedic diseases. This trend is also driving a continuous increase in demand for advanced orthopedic treatments, thereby propelling the ongoing development of the orthopedic industry.

2.1 Global

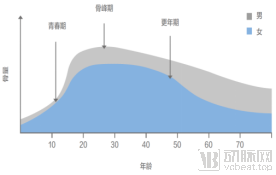

As people age, bone mass in the human body initially increases and then continuously declines; severe reduction in bone mass can lead to osteoporosis.

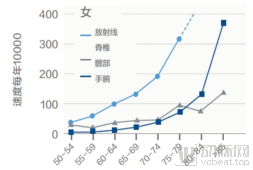

In men, peak bone mineral density is typically reached around the age of 20–30, followed by a gradual decline with advancing age. In women, bone mass decreases significantly after menopause. Osteoporosis is a disease characterized by reduced bone mass, deterioration of bone tissue microarchitecture, increased bone fragility, and compromised mechanical properties, which predisposes individuals to fractures. Data from the International Osteoporosis Foundation indicate that the incidence of fragility fractures in the elderly rises sharply with age.

The Relationship Between Human Bone Mass and Age: Fragility Fractures Increase Sharply with Age

Data source: International Osteoporosis Foundation, Southwest Securities

Osteoporosis makes the elderly highly susceptible to fractures after falls, particularly in the hip and knee joints.

Osteoarthritis is also a degenerative disease and is common among the elderly over the age of 65, with degenerative osteoarthritis being closely associated with age. Among individuals over 60 years old, more than 80% show radiographic signs of osteoarthritis in the knee joint, and 50% suffer from pain.

According to WHO statistics, the incidence of osteoarthritis (OA) among individuals aged 50 and older is 50%, with the knee being the most commonly affected site. Taking the highly developed United States as an example, data from the 2018 JBJS article “Projected Volume of Primary Total Joint Arthroplasty in the U.S. 2014 to 2030” indicate that there were 370,000 primary hip arthroplasties and 580,000 primary knee arthroplasties performed in the United States in 2014, totaling 950,000 primary joint replacements. The ratio of hip to knee arthroplasties was 1:1.57.

The number of joint replacement procedures in the United States continues to grow. In 2018, hip and knee replacement surgeries exceeded 1.7 million cases, with primary knee replacements accounting for 54.4% and primary hip replacements for 32.7%, resulting in a hip-to-knee ratio of 1:1.66. Based on the 90,000 cases recorded in 2014, the five-year compound annual growth rate (CAGR) was 12.34%.

According to an article by Jasvinder A. Singh published in J Rheumatol in 2019, the number of primary total hip arthroplasties (THA) and total knee arthroplasties (TKA) from 2020 to 2040 was projected based on the U.S. National Inpatient Sample (NIS) data from 2000–2014 and census data. The projected annual numbers of THA procedures in the United States (with 95% prediction intervals) for 2020, 2025, 2030, and 2040 were estimated to be 498,000, 652,000, 850,000, and 1,429,000, respectively. For primary TKA, the projected annual volumes for 2020, 2025, 2030, and 2040 were 1,065,000, 1,272,000, 1,921,000, and 3,416,000, respectively. Thus, the total number of joint replacement procedures in the United States is projected to reach 1.563 million, 1.924 million, 2.771 million, and 4.845 million in 2020, 2025, 2030, and 2040, respectively.

2.2 China

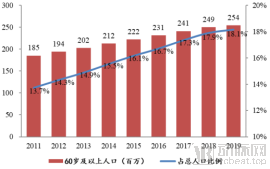

China is undergoing rapid population aging. Based on statistics for the population aged 60 and above, there were approximately 254 million people in this age group in China in 2019. Furthermore, the prevalence of osteoporosis increases with advancing age.

Significant Trend of Population Aging in China: The Relationship Between Osteoporosis and Age

Data Source: National Bureau of Statistics, Southwest Securities

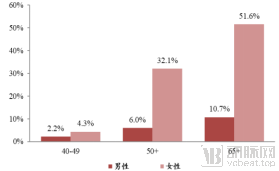

According to the results of China’s first epidemiological survey on osteoporosis, released by the National Health Commission in 2018, the prevalence of osteoporosis among individuals aged 40–49 years was 3.2%, with 2.2% in men and 4.3% in women. Among those aged 65 years and older, the prevalence reached as high as 32.0%, including 10.7% in men and 51.6% in women. Data published by the Chinese Center for Disease Control and Prevention indicate that China has the largest number of osteoporosis patients worldwide, reaching 160 million in 2016. The number of individuals with osteoporosis and low bone mass in China is projected to increase to 280 million by 2020.

Osteoporosis is a major cause of fractures in the elderly. Among individuals aged 50 and older with osteoporosis, the annual incidence of hip fractures is approximately 0.99%. Based on an estimated population of 280 million, this translates to roughly 2.7717 million hip fracture cases per year.

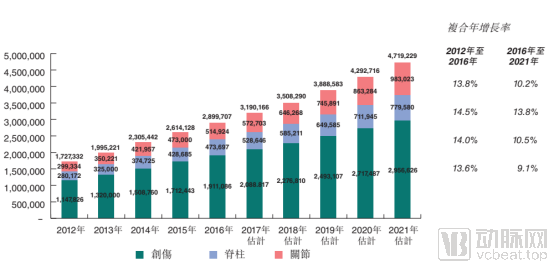

Data from the China Health and Retirement Longitudinal Study (CHARLS) indicate that the prevalence of symptomatic knee osteoarthritis (KOA) in China is 81%, affecting approximately 113.4 million individuals. Osteoarthritis (OA) can lead to joint pain, deformity, and functional impairment, thereby increasing the incidence of cardiovascular risk and all-cause mortality. In particular, symptomatic KOA can nearly double all-cause mortality. With the advancing aging of China’s population, the prevalence of OA is gradually rising, imposing a substantial economic and social burden. Therefore, effective prevention and treatment of OA have become a critical societal issue requiring urgent attention in China.

According to statistics from Archives and the NIH, one in eight Americans over the age of 60 suffers from osteoarthritis, with 25% requiring hip replacement and 9–13% requiring knee replacement. China is currently experiencing population aging; according to data from the National Working Commission on Aging, the population aged 60 and above has reached 240 million, including 100 million arthritis patients and 4 million patients with rheumatoid arthritis. Patients with rheumatoid arthritis generally require joint replacement in the later stages of the disease. By analogy with the United States, it is estimated that approximately 7.5 million patients in China require hip replacement, and 3.9 million require knee replacement.

In addition to the hip and knee joints, the shoulder, elbow, and ankle joints are also seeing increased incidence. The prevalence of arthritis among recreational runners is 3.5%, whereas it is three times higher in sedentary individuals, at 10.2%. Office workers and computer users are most prone to injuries in the wrists, elbows, and shoulders, while drivers are most susceptible to damage in the knees and ankles.

Benefiting from market demand, the number of orthopedic hospitals and the number of outpatient visits to orthopedic departments in China have been increasing in recent years. The number of orthopedic hospitals rose from 464 in 2012 to 617 in 2017, while the number of orthopedic hospital visits increased from 11.54 million in 2012 to 14.39 million in 2017. The compound annual growth rate (CAGR) of orthopedic patient visits was 4%, with the growth rate reaching 10% in 2017.

Number of Orthopedic Hospitals in China, 2012–2017; Number of Patient Visits to Orthopedic Hospitals in China, 2012–2017

Data source: China Health Statistics Yearbook, Huatai Securities

Based on IMS data estimates, the number of joint replacement procedures in China reached 400,000 in 2014, with hip replacements accounting for 60%. According to Frost & Sullivan research, the number of joint replacement procedures in China was 514,000 in 2016, representing a compound annual growth rate (CAGR) of 13.8% from 2012 to 2016.

Data Source: Frost & Sullivan; AK Medical Holdings Prospectus

According to Weiyi Orthopedics data, there were 588,100 joint replacement cases in China in 2018, including 396,500 hip replacements and 191,600 knee replacements.

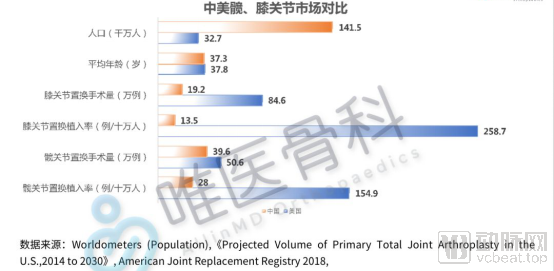

In terms of penetration rates, the United States records 285.7 knee implantations per 100,000 people, whereas China has only 13.5. For hip implantations, the rate is 154.9 per 100,000 people in the U.S., compared to just 28 in China, indicating a low penetration rate for joint replacements in China. Based on U.S. penetration rates, it is estimated that approximately 7.5 million patients in China require hip replacement surgery, and 3.9 million require knee replacement surgery. However, the total number of joint replacement procedures performed in China in 2018 was only 588,100, suggesting significant room for future growth.

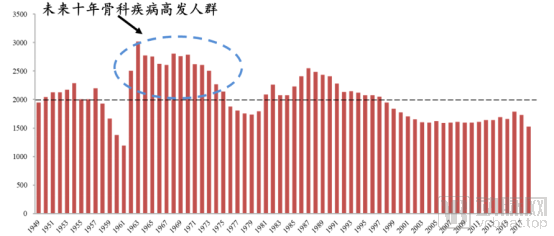

Looking at demographic trends over the next decade, since the founding of the People's Republic of China in 1949, two baby booms began in 1962 and 1981, respectively. The first wave, born in 1962, entered the age group of 55 and above in 2017 and is now approaching the age of 60 and above. Consequently, the high-risk population for orthopedic diseases is expected to maintain a high growth trend for the next ten years.

The First Baby Boom Since the Founding of the People's Republic of China Is Approaching the Age of 60 and Above

Data sources: National Bureau of Statistics, Southwest Securities

Orthopedic diseases are typical age-related conditions, with the majority strongly correlated to advancing age; individuals aged 60 and above represent a high-risk demographic. Currently, China’s joint replacement penetration rate remains low, with a potential market size exceeding ten million cases. In contrast, only 588,100 procedures were performed in 2018, indicating substantial room for growth. Structurally, hip replacements dominate in China, with a hip-to-knee replacement ratio of 2.06:1, whereas the ratio in the United States is 1:1.66. This suggests that many knee patients in China have not yet undergone artificial joint replacement, pointing to significant future growth potential for the artificial knee market. Regarding the patient population, based on post-founding baby boom trends, China’s first baby-boom cohort will enter the age group of 60 and above starting in 2021, leading to sustained high growth in the high-risk population for orthopedic diseases.

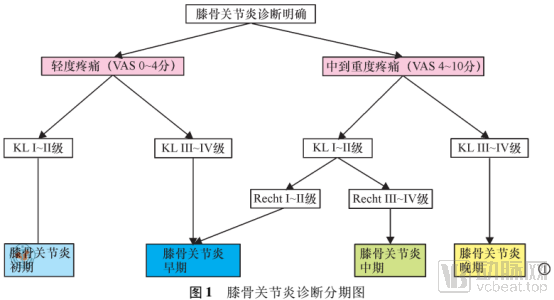

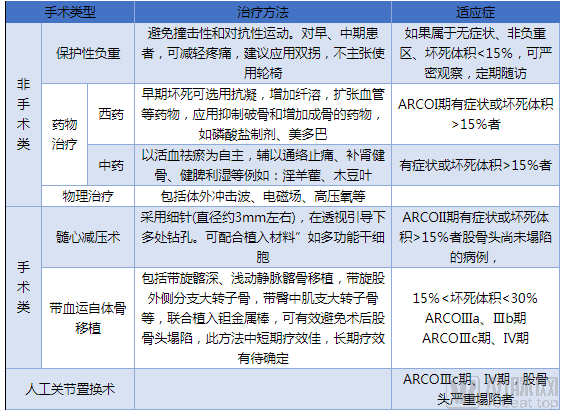

3.1 Staging of Osteoarthritis

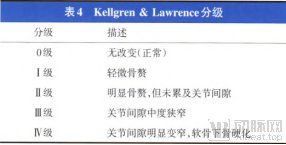

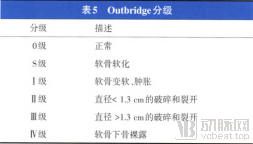

For the treatment of osteoarthritis, staging is required as a first step. Currently, there are multiple methods for the clinical staging of osteoarthritis (OA), including a four-stage classification based on clinical features, the Kellgren & Lawrence grading system based on radiographic changes, and the Outerbridge grading system based on arthroscopic findings of articular cartilage damage. The Kellgren & Lawrence and Outerbridge grading systems are shown in the table below:

Data source: "Guidelines for the Diagnosis and Treatment of Osteoarthritis (2018 Edition)"

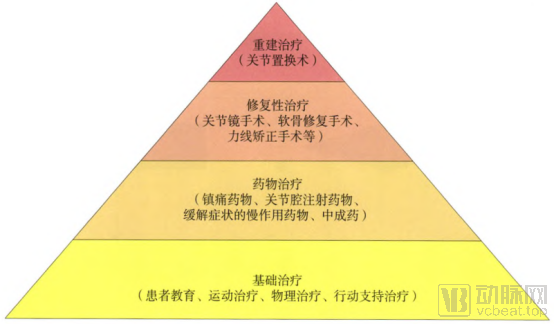

Based on an accurate assessment of the patient’s condition, the treatment of osteoarthritis should strictly adhere to indications and follow a stepwise treatment approach, namely:

Step 1: Non-surgical basic treatment, including patient education, behavioral support, physical therapy, and Chinese and Western medications;

Step 2 Minimally Invasive Knee-Preservation Surgery, Including Arthroscopy, Osteotomy, and Cartilage Repair;

Step 3: Artificial joint replacement surgery, including patellofemoral joint arthroplasty, unicompartmental knee arthroplasty, and total knee arthroplasty.

Stages III and IV represent the end-stage of osteoarthritis, for which joint reconstruction (i.e., artificial joint replacement) should be considered.

Data source: "Guidelines for the Diagnosis and Treatment of Osteoarthritis (2018 Edition)"

3.2 Artificial Joint Replacement

After decades of development, significant progress has been made in prosthetic design, surgical techniques, and rapid recovery protocols for artificial joints. In China’s tertiary hospitals, routine hip and knee replacement surgeries are now typically completed within approximately one hour. These procedures do not require the placement of drainage tubes. By combining multimodal analgesia with enhanced recovery after surgery (ERAS) management, patients can ambulate with crutches as early as one day postoperatively and be discharged within four to five days. As sutures do not need to be removed, patients can return to normal daily life and engage in various activities, with surgical scars being barely noticeable to others. This approach has become a highly successful surgical intervention and is regarded as the gold standard for treating end-stage joint diseases.

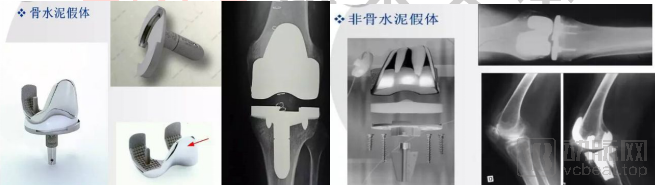

Artificial joint replacement is categorized into hip replacement and knee replacement. The basic surgical procedures for hip replacement include hemiarthroplasty and total hip arthroplasty (THA). The basic surgical procedures for knee replacement include patellofemoral arthroplasty (PFA), unicompartmental knee arthroplasty (UKA), and total knee arthroplasty (TKA).

Specifically, depending on the extent and scope of joint damage, types of artificial joint replacement are classified as follows:

1. Total Joint Arthroplasty

Refers to the replacement of the corresponding articular bone surfaces on both sides of a damaged joint with joint prostheses. Prosthetic designs vary, with different types tailored to specific joints. A total joint prosthesis consists of two hemi-joint components made from different materials, based on the joint's anatomy; examples include total hip arthroplasty, total shoulder arthroplasty, and hinged knee prostheses (where the articulating components are separated by the prosthesis to reduce wear).

2. Joint Surface Replacement

Surface replacement arthroplasty is a type of total joint replacement. It is primarily indicated for cases involving destruction of the articular bone and cartilage, where there is no significant defect or damage to the subchondral bone stock and the periarticular ligaments remain intact. In this procedure, the resurfaced convex side consists of a metallic prosthesis, while the concave side is made of plastic (i.e., metal-on-polyethylene bearing surface). Examples include dual-cup hip arthroplasty, track-guided knee arthroplasty, and ankle surface replacement arthroplasty.

3. Hemiarthroplasty

It is commonly used for bone injury or destruction on one side of a joint. Only the damaged part of the joint is replaced with an artificial prosthesis. Artificial joints can be divided into joint components and intramedullary stems (usually made of metal materials). For example, artificial femoral heads, artificial humeral heads, and knee joints where only the tibial articular surface is replaced are all referred to as hemi-joint surface replacement.

Detailed Analysis of the Hip and Knee Joints

3.2.1 Hip Replacement

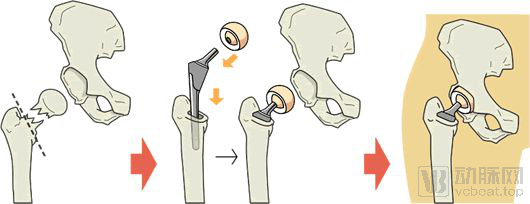

Schematic diagram of hip replacement:

Hip arthroplasty is categorized into total hip arthroplasty, hemiarthroplasty, and tumor prosthetic replacement.

Total hip arthroplasty (THA) can be categorized into conventional total hip replacement and hip resurfacing arthroplasty. Conventional total hip replacement, as illustrated in the schematic diagram, involves replacing the damaged natural femoral head and acetabulum with a metallic femoral stem, femoral head, liner, and acetabular cup. Hip resurfacing arthroplasty still presents numerous challenges and is not widely used in China. Schematic diagrams of conventional total hip replacement and hip resurfacing arthroplasty are shown below:

Standard Total Hip Arthroplasty; Surface Replacement Total Hip Arthroplasty

Hemiarthroplasty, in contrast to total hip arthroplasty systems, involves replacing only half of the joint—typically the femoral stem and head—without resurfacing the acetabular side. Strictly speaking, hemiarthroplasty is referred to as artificial femoral head replacement, which entails replacing only the femoral head. This procedure is relatively straightforward, associated with favorable postoperative hip functional recovery and a lower risk of dislocation. However, wear may occur between the acetabular cartilage and the metallic femoral head during movement after surgery. Therefore, this procedure is primarily indicated for elderly patients with low activity levels, normal body weight, and minimal severe wear of the acetabular cartilage. It is most commonly performed in elderly patients with femoral neck fractures, with the main goals being pain relief and improvement in mobility.

Hemiarthroplasty systems are further classified into bipolar and unipolar hemiarthroplasty. Unipolar hemiarthroplasty consists of a femoral stem connected to a single prosthetic head, whereas bipolar hemiarthroplasty adds an inner liner and an outer prosthetic head to the unipolar design. Compared with unipolar hemiarthroplasty, bipolar hemiarthroplasty can effectively reduce the incidence of joint pain. Schematic diagrams of both types are shown below:

Unipolar Hemiarthroplasty System, Bipolar Hemiarthroplasty System

In addition to total hip arthroplasty and hemiarthroplasty, there are also tumor-specific and custom hip joint systems, as well as revision hip arthroplasty.

Since the majority of hip replacements are performed as conventional total hip arthroplasty, this section will use conventional total hip arthroplasty as an example to examine the current status and trends in hip replacement.

Total hip arthroplasty prostheses primarily consist of four components: the acetabular cup, acetabular liner, femoral head, and femoral stem. The acetabular cup and femoral stem interface with and are fixed to the host bone, while the femoral head and acetabular liner constitute the frictional bearing surface of the hip joint. Based on the fixation method between the acetabular cup/femoral stem and the host bone, prostheses are classified as cemented or cementless (biological fixation). Depending on the materials used for the bearing surface, options include metal, black ceramic, and ceramic femoral heads, as well as metal, ultra-high-molecular-weight polyethylene (UHMWPE), highly cross-linked UHMWPE, and ceramic acetabular liners, resulting in a wide variety of material combinations.

3.2.1.1 Classification of Fixation Modes: From Cemented Fixation to Biological Fixation

From the historical development of artificial joints, the fixation mode of femoral prostheses (femoral stems) has evolved from the initial press-fit type to Charnley’s cemented type, and then to biologic fixation. Biologic fixation is associated with lower long-term complication rates and loosening rates.

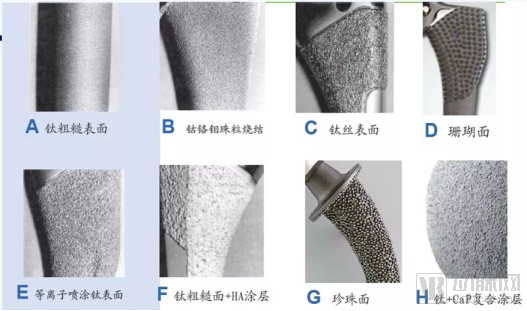

The components of the hip joint that require fixation include the femoral stem and the acetabulum. Femoral stems are categorized into cemented and uncemented (biological) types. Schematic diagrams of both are shown below:

Porous coating, HA coating, porous + HA, press-fit, cemented

Cemented femoral stems are smooth-surfaced femoral stems. After the femoral stem is implanted into the femur, bone cement with self-curing properties is added to fill the gaps between the bone and the implant or within the bone cavity. The chemical name of bone cement is polymethyl methacrylate (PMMA), also known as acrylic bone cement. It was first applied by Charnley in 1958 for fixing the femoral component of hip prostheses.

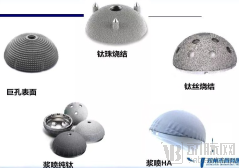

Biological femoral stems encompass a variety of coating types, including bead-blasted surfaces, coral-like surfaces, aluminum oxide-blasted surfaces, titanium mesh surfaces, titanium plasma-sprayed surfaces, and hydroxyapatite (HA)-coated surfaces.

Currently, the mainstream coating type is hydroxyapatite (HA). Hydroxyapatite is similar to the mineral phase of human bone, biocompatible, non-resorbable, non-toxic, does not induce inflammatory or allergic reactions, and is osteoconductive. The typical coating thickness is 150 μm.

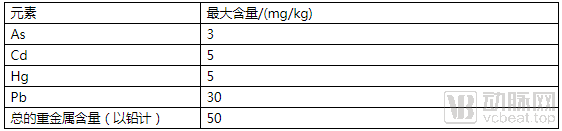

Currently, the Center for Drug Evaluation (CDE) under China’s National Medical Products Administration (NMPA) has established certain technical requirements for hydroxyapatite (HA) coatings, including a Ca/P ratio ranging from 1.67 to 1.76. The maximum allowable limits for heavy metal elements are shown in the table below.

Limit Content of Heavy Metal Elements in Calcium Phosphate Coatings

a. In the crystalline phase, the content of hydroxyapatite crystalline phase shall be no less than 50%, and the maximum allowable content of α-TCP, β-TCP, TTCP, and CaO crystalline phases is 5%; the crystallinity of hydroxyapatite shall be no less than 45%. The number of coating layers, pore size range, and roughness shall be clearly specified. Requirements for coating thickness, porosity, mean intercept length, and coating interface gradient shall be defined, and evaluation criteria shall be established in accordance with the methods specified in ASTM F1854.

Compared with cemented femoral stems, uncemented (biological) femoral stems require less bone resection, involve fewer surgical steps, and are less time-sensitive (as bone cement requires time to harden). They are also easier to remove intact during revision surgery. Therefore, current clinical practice recommends prioritizing uncemented fixation for relatively younger patients. Cemented prostheses are reserved for a small subset of patients, such as those with severe osteoporosis.

Femoral stem fixation is further categorized into proximal fixation, distal fixation, and full-segment stability, with the specific choice tailored to the individual case type.

Other mainstream designs of femoral stems currently include:

1. Dual-taper design provides three-dimensional stability;

2. The quadrilateral cross-section provides axial and rotational stability;

3. Proximal horizontal groove microstructure prevents subsidence, increases the contact area between the prosthesis and bone by 15%, and conforms to the biomechanics of proximal stress transmission;

4. Distal vertical groove microstructure effectively resists rotational torque, reduces intramedullary canal occupancy, and lowers the incidence of thigh pain;

5. Optimized neck design with a rectangular profile, increasing the head-to-neck ratio and range of motion while reducing the risk of impingement between the neck and the acetabular cup or liner. 130° neck-shaft angle, 12/14 taper.

6. Complete sizing: Neck length varies proportionally, offset increases uniformly, with no skipped sizes;

7. Sagittal plane varus tip: Better conforms to the oval-shaped medullary cavity characteristics of Chinese patients, reducing the potential risk of thigh pain.

Dual-tapered design with horizontal slots and vertical groove microstructures on the rectangular neck

In addition to the fixation of the femoral stem, the acetabular cup also requires fixation. Fixation of the acetabular cup is categorized into cemented fixation and biological (cementless) fixation.

Cemented Acetabular Fixation vs. Cementless Acetabular Fixation

Based on existing research findings, cemented prostheses offer superior short-term stability; however, in the long term, particularly for younger or more active patients, they are associated with higher rates of complications and loosening. For patients under 70 years of age, the revision rate for cemented prostheses is 1–2 times that of uncemented prostheses, and the loosening rate is 2–4 times higher; whereas revision rates are similar for patients over 70 years of age. In patients aged 55–64 years, the 15-year survival rate of uncemented prostheses is 80%, which is higher than the 71% observed with cemented prostheses. In patients aged 65–74 years, the 15-year survival rate of uncemented prostheses is 94%, surpassing the 85% rate for cemented prostheses. For patients older than 75 years, the 10-year survival rates for both types exceed 90%, with no significant difference between them.

3.2.1.2 Friction Interfaces: Metal-on-Polyethylene and Ceramic-on-Polyethylene Are the Mainstream

As the most critical joint in the body, the hip joint plays a vital role in transmitting stress from the trunk to the limbs; therefore, the selection of the friction interface for the hip joint is of paramount importance. Ideal bearing surface materials should possess the following characteristics: a low coefficient of friction, minimal generation of wear debris, mild tissue response to wear debris, resistance to third-body wear, and allowance for adequate fluid film lubrication.

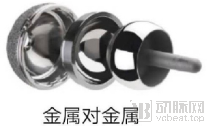

The lower the coefficient of friction at the bearing surface, the less wear occurs in the materials, and the longer the theoretical survival time of the prosthesis. Currently, the most commonly used materials, ranked by increasing coefficient of friction (acetabular cup against femoral head), are as follows: ceramic-on-ceramic < highly cross-linked polyethylene-on-ceramic < highly cross-linked polyethylene-on-metal < metal-on-metal. Among ceramic materials, the ranking is polished ceramic < black diamond-like carbon (DLC) ceramic < yellow zirconia-toughened alumina (ZTA) ceramic. Naturally, a lower coefficient of friction corresponds to a higher price. However, a lower coefficient of friction is not always better; there are other evaluation criteria for different bearing surface material combinations.

Over the past two decades, the emergence of second-generation metallic materials, highly cross-linked polyethylene, and novel bioceramics has significantly enhanced the overall therapeutic outcomes in joint surgery. Currently available bearing surfaces can be categorized into two main types: the first type is "hard-on-soft" combinations, involving metal or ceramic articulating against polyethylene; the second type is "hard-on-hard" combinations, where identical hard materials articulate with each other, including ceramic-on-ceramic and metal-on-metal.

1. Hard vs. Soft

Hard-on-soft bearings include metal-on-polyethylene, ceramic-on-polyethylene, and Oxinium (oxidized zirconium-niobium alloy) on polyethylene.

In hard-on-soft bearings, the soft component is primarily made of polyethylene. The development of polyethylene has undergone four stages. Early conventional polyethylene exhibited high wear rates, and frictional contact easily generated particles, leading to osteolysis and subsequent prosthetic loosening. Consequently, the industry developed metal-on-metal and ceramic-on-ceramic head-liner structures.

In the late 1970s, highly cross-linked polyethylene (HXLPE) emerged. Compared with conventional ultra-high-molecular-weight polyethylene, HXLPE exhibits superior wear characteristics and has become a commonly used bearing surface material in hip arthroplasty. Cross-linking enhances resistance to adhesive wear and corrosive wear, with higher degrees of cross-linking yielding better wear resistance. The wear rate of HXLPE is reduced by 60%–90% compared with that of conventional polyethylene, with liner wear rates of approximately 0.01 mm per year; its advantages are evident, and clinical studies support this view. However, cross-linking adversely affects toughness, ductility, and resistance to fatigue crack initiation. Furthermore, free radicals generated during the cross-linking process can lead to oxidative degradation.

Second-generation HXLPE incorporates numerous advanced technologies. Sequential multi-cycle radiation annealing effectively maintains optimal crystallite size and mechanical properties, reducing free radicals and oxidation without the need for remelting.

Third-generation HXLPE with antioxidant vitamin E added during production improves wear characteristics at the material's oxidation level, and its wear particle-induced osteolytic response is significantly less than that of traditional highly cross-linked polyethylene particles without vitamin E.

A hip simulation study demonstrated that the wear rate of highly cross-linked polyethylene stabilized with vitamin E was 4–10 times lower than that of conventional ultra-high-molecular-weight polyethylene. Its ultimate strength, yield strength, ductility, and fatigue resistance were significantly superior to those of remelted highly cross-linked polyethylene. Polyethylene has now advanced to covalently cross-linked polyethylene (CoXPE).

Currently, the primary hard-on-soft friction interfaces in clinical practice are metal-on-highly cross-linked polyethylene (MoXPE) and ceramic-on-highly cross-linked polyethylene (CoXPE).

Metal-on-highly cross-linked polyethylene (CoXPE) is a time-tested, classic bearing combination that was widely used prior to the advent of ceramic materials. Its primary advantages include lower cost and greater flexibility in sizing and positioning of the metal femoral head. The main drawback is a higher wear rate—approximately twice that of ceramic-on-highly cross-linked polyethylene—resulting in a relatively shorter service life. However, significant improvements in materials and manufacturing processes for currently used metal femoral heads and polyethylene liners have substantially reduced wear rates, making this option a cost-effective and reliable choice.

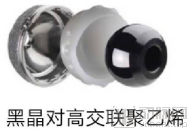

Ceramic-on-highly cross-linked polyethylene (CoXPE) offers the advantages of being less prone to squeaking and fracture, a lower risk of dislocation, and a relatively moderate price. The surface smoothness of ceramic femoral heads is significantly superior to that of metal femoral heads. Compared with metal-on-highly cross-linked polyethylene bearings, ceramic-on-highly cross-linked polyethylene bearings can reduce volumetric wear rates by approximately 50%. Black crystal (a zirconium-niobium alloy with a ceramicized surface) combines the excellent surface properties of ceramics while avoiding the risk of ceramic fracture; thus, the combination of black crystal and highly cross-linked polyethylene is also a favorable option for load-bearing articulations. Its main drawback is inferior wear resistance compared with ceramic-on-ceramic bearings.

To date, there have been no large-scale case reports in the literature regarding revision surgeries necessitated by osteolysis secondary to wear at highly cross-linked polyethylene (HXLPE) bearing surfaces; failures have primarily been attributed to mechanical fracture of the HXLPE liners. Given that HXLPE exhibits reduced resistance to rough surface counterfaces and third-body wear compared to conventional polyethylene, further long-term follow-up is required to evaluate the late-stage clinical outcomes of metal-, ceramic-, or oxidized zirconium-on-HXLPE bearing combinations.

Summary: The wear rate of highly cross-linked polyethylene is currently far superior to that of conventional polyethylene used in the past, making it a favorable option for middle-aged and elderly patients.

2. Hard-on-Hard

Hard-on-hard bearings include metal-on-metal (cobalt-chromium alloy), ceramic-on-ceramic (conventional ceramics, yellow ceramics, and pink ceramics), and black crystal-on-black crystal.

Ceramic-on-ceramic (CoC) bearing surfaces have been in clinical use for over 40 years. CoC bearing surfaces offer numerous advantages, including: (1) high hardness and excellent wear resistance; (2) good hydrophilicity, which improves the wettability of the prosthetic surface, maintains lubrication at the ceramic interface, and reduces adhesive wear; and (3) biological inertness, as ceramic wear particles exhibit stable biological characteristics and significantly reduced inflammatory potential. The low wear rate and stable biological properties greatly reduce the incidence of osteolysis associated with CoC prostheses. However, high brittleness is an inherent drawback of ceramic materials, making prosthetic fracture a serious complication of CoC implants. The fracture rate of third-generation ceramic (high-purity alumina) liners is 0.032%, and that of ceramic heads is 0.021%. Fourth-generation ceramics (matrix composites), also known as Delta ceramics, are composite ceramics formed by adding a certain amount of zirconia and other materials to an alumina matrix. Compared to the previous generation, Delta ceramics demonstrate significant improvements in strength and toughness. This allows for the manufacture of thin-walled ceramic liners, facilitating the use of large-diameter femoral heads. Additionally, the thickness of the femoral head can be reduced, enabling the incorporation of a metal adapter sleeve within the femoral head. This resolves the issue of being unable to use a CoC bearing surface during revision surgery when retaining the femoral stem. The fracture rate of Delta ceramic femoral heads is 0.002%, approximately one-tenth that of the previous generation. However, the fracture rate of Delta ceramic liners remains at 0.028%, showing no significant reduction.

A potential issue with ceramic-on-ceramic (CoC) bearing surfaces is squeaking. Meta-analyses of international literature indicate that the average incidence of joint squeaking after total hip arthroplasty (THA) with CoC bearings is 2.4% (range: 0.7%–20%). This squeaking typically has a late onset, is often persistent, does not resolve spontaneously, and may require revision surgery to replace the bearing material for resolution. There have also been a few case reports in China. West China Hospital observed an incidence of joint squeaking of approximately 1% following CoC THA, mostly occurring during hip flexion. Moreover, the sensation of squeaking gradually disappeared in the vast majority of patients within 3–6 months postoperatively, which differs from findings reported in international literature. Increased friction due to inadequate fluid-film lubrication is considered the fundamental cause of squeaking. Factors such as improper prosthetic implantation angles leading to increased edge loading, third-body particle interposition, and subluxation can all contribute to this condition. Additionally, excessive body mass index (BMI) and certain specific prosthetic designs are also causes of squeaking. Despite these drawbacks, ceramic materials offer significant advantages, including excellent tribological performance, minimal tissue reaction to wear debris, and the ability to use large-diameter femoral heads to enhance stability. Furthermore, the advent of Delta ceramics has significantly reduced the probability of ceramic fracture. Consequently, the use of CoC bearing surfaces in China has been increasing year by year. However, THA with CoC bearing surfaces demands high technical skill from surgeons and requires precise prosthetic component positioning. Surgeons should pay sufficient attention to potential complications. Overall, ceramic-on-ceramic bearings can be considered the optimal choice for hip arthroplasty in young and middle-aged patients.

Metal-on-metal (MoM) bearing surface prostheses were first introduced more than 40 years ago. However, due to issues with material compatibility and manufacturing techniques, they were abandoned because of high rates of complications such as loosening, dislocation, and metal ion contamination. With advancements in new materials, design, manufacturing processes, and implantation techniques, the coefficient of friction between metal-on-metal bearing surfaces has been significantly reduced. Furthermore, since wear does not generate polyethylene particles, the incidence of osteolysis is markedly decreased. The use of large-diameter femoral head MoM prostheses can also significantly reduce dislocation rates and improve patients' hip range of motion. These advantages led to a surge in the popularity of MoM bearing surface prostheses in countries such as the United States over a decade ago. In China, some large hospitals have gradually conducted surface replacement and large-diameter femoral head MoM total hip arthroplasty (THA) on a relatively large scale for young patients, achieving favorable clinical outcomes.

However, as follow-up durations have extended, certain issues associated with metal-on-metal (MoM) prostheses have gradually garnered attention. Data from the Australian Orthopaedic Association National Joint Replacement Registry indicate that the 5-year revision rate for MoM bearing surface total hip arthroplasty (THA) prostheses is 96%, and the 10-year revision rate is 15.5%. Meanwhile, data from the UK National Joint Registry suggest that the 5- and 9-year revision rates for MoM bearing surface THA prostheses are 7.7% and 17.7%, respectively, with clinical outcomes based on revision rates being significantly inferior to those of other bearing surface combinations. Data from the New Zealand Joint Registry show that the revision rate for MoM prostheses with a femoral head diameter ≤28 mm is significantly lower than that of ceramic-on-ceramic, ceramic-on-polyethylene, and metal-on-polyethylene combinations, whereas the clinical outcomes for MoM prostheses with a femoral head diameter ≥36 mm are unsatisfactory. Similarly, further stratified analysis of data from the Australian registry indicates that the 5- and 10-year revision rates for MoM prostheses with a femoral head diameter ≤28 mm are 3.7% and 5.7%, respectively, outperforming traditional polyethylene bearings. Therefore, femoral head diameter has a clear impact on the revision rate of MoM prostheses. In addition to femoral head diameter, design flaws in MoM prostheses (such as low-profile non-hemispherical acetabular cup designs and excessively large or small tolerance ranges) and suboptimal intraoperative implantation angles also increase the risk of revision. The withdrawal of Johnson & Johnson’s ASR metal-on-metal prosthesis from the market in 2010 significantly impacted the use of MoM bearing surface hip implants. Other potential risks associated with MoM include local soft tissue reactions, periprosthetic osteonecrosis, and potential metal ion toxicity. The mechanism by which MoM induces local soft tissue reactions remains incompletely understood. Some researchers have proposed hypotheses based on analyses of inflammatory pseudotumors, suggesting that it is not the metal ions themselves but rather abundant nanosized metal wear particles that cause local soft tissue reactions. These wear particles are phagocytosed by macrophages; within the acidic environment of the phagosomes, cobalt ions dissolve extensively. Upon macrophage apoptosis, a large amount of intracellular cobalt ions is released, forming a "cobalt ion wave" with local concentrations far exceeding those in serum or synovial fluid. This leads to extensive necrosis of surrounding fibroblasts, resulting in soft tissue reactions such as inflammatory pseudotumors. Due to these issues associated with MoM prostheses, their usage proportion has declined significantly year by year both domestically and internationally.

According to sampling statistics from 105,000 total hip arthroplasty (THA) procedures performed at 174 U.S. hospitals between 2001 and 2012, modular acetabular cups accounted for 99% of cases in 2012, and 93% of THAs utilized cementless fixation. In 2012, 59% of THAs employed metal-on-highly cross-linked polyethylene bearings. Meanwhile, the proportion of ceramic-on-polyethylene/highly cross-linked polyethylene bearings continued to rise, increasing from 6% in 2001 to 38% in 2012. The use of ceramic-on-ceramic bearings declined from 11% in 2004 to 1% in 2012, while metal-on-metal bearings dropped from 31% in 2007 to 1% in 2012. These shifts reflect issues identified and prioritized by orthopedic surgeons in clinical practice. Although China currently lacks comprehensive statistical data on the utilization rates of bearing surface materials, the general trend indicates that ceramic-on-ceramic or ceramic-on-highly cross-linked polyethylene combinations are gaining increasing recognition and preference among physicians for younger or more active patients.

Generally, ceramic-on-ceramic artificial joints are the most expensive, followed by ceramic-on-highly-crosslinked-polyethylene implants, while metal-on-polyethylene artificial joints are the least expensive.

Summary: Based on hip joint utilization trends in the United States from 2001 to 2012, the trend for total hip arthroplasty implants favored cementless fixation. The predominant bearing surface remained metal-on-highly cross-linked polyethylene, accounting for nearly 60%, followed by ceramic-on-highly cross-linked polyethylene, which increased from 6% to 38%. The use of ceramic-on-ceramic and metal-on-metal bearings declined, with metal-on-metal usage dropping significantly from 31% to 1%. Current clinical consensus suggests that ceramic-on-ceramic or ceramic-on-polyethylene bearings may be more suitable for younger patients, whereas metal-on-polyethylene bearings are appropriate for elderly patients, such as those over 70 years of age.

3.2.2 Knee Arthroplasty

The knee prosthesis consists of the following three components:

1. Femoral prosthesis: Resurfaces the distal end of the femur. The femoral prosthesis is composed of metal alloys;

2. Patellar Prosthesis: It may feature a monobloc design composed of highly cross-linked polyethylene. Alternatively, it may adopt a two-component modular design consisting of a metal tray and a highly cross-linked polyethylene insert. The insert is either fixed or mobile on the metal tray. The femoral prosthesis articulates with the tibial component;

3. Tibial Prosthesis: It can be designed as a single component or a two-component system. The single-component design is made of plastic, while the two-component design consists of a metal tray fixed to the bone and a plastic insert. The plastic insert provides a smooth surface on which the femoral component articulates.

The plastic insert is typically attached to the tibial tray. A schematic diagram of knee arthroplasty is shown below:

Normal Joint, Damaged Joint, Post-Artificial Joint Replacement

Knee joint prostheses are classified according to different dimensions as follows:

1. Knee prostheses can be classified according to the implantation site into unicompartmental knee arthroplasty (UKA, single-compartment prosthesis), bicompartmental prostheses (excluding patellofemoral joint replacement), and total knee arthroplasty (tricompartmental prosthesis).

Total Knee Arthroplasty Prosthesis, Unicompartmental Knee Prosthesis

Unicompartmental Knee Arthroplasty (UKA) implants are classified as non-constrained prostheses. For isolated medial or lateral compartment pathology, unicompartmental knee replacement is theoretically indicated. A successful UKA procedure maximally preserves joint tissue architecture and kinematic function, while preserving options for subsequent total knee arthroplasty (TKA). Compared with total knee prostheses, UKA has garnered significant attention due to its minimally invasive nature, facilitation of rapid recovery, and favorable functional outcomes and patient satisfaction.

Unicompartmental knee prostheses are categorized into mobile-bearing and fixed-bearing designs. In mobile-bearing systems, the ultra-highly cross-linked polyethylene insert can slide anteroposteriorly; a representative example is the Zimmer Biomet Oxford® Unicompartmental Knee System. In fixed-bearing systems, the ultra-highly cross-linked polyethylene insert is secured and cannot slide anteroposteriorly; representative examples include the Zimmer Biomet ZUK Unicompartmental Knee Prosthesis and the LINK® Sled Unicompartmental Knee Prosthesis. Relevant images are shown below:

2. Based on the fixation method, prostheses can also be classified into cemented and uncemented types.

For artificial hip joints, cementless prostheses are the mainstream, offering superior long-term fixation; cemented prostheses are reserved for a small subset of patients, such as those with severe osteoporosis.

For artificial knee joints, cemented prostheses have gained widespread acceptance due to their favorable long-term follow-up outcomes. In total knee arthroplasty, the role of bone cement extends beyond merely fixing the prosthesis; its more critical function is to enhance the load-bearing capacity of the bone bed, particularly on the tibial side. Cemented prostheses remain the mainstream choice.

3. Based on the degree of mechanical constraint provided in the prosthesis design, prostheses can be classified into non-constrained, semi-constrained, highly constrained, and fully constrained (hinged) prostheses.

(1) Non-constrained prostheses: Non-constrained total knee prostheses are represented by posterior cruciate-retaining (CR) designs. The preserved posterior cruciate ligament (PCL) maintains posterior stability after implantation, thereby allowing the tibial articular surface to adopt a low-constraint design with greater curvature to achieve a larger range of motion; the designed range of motion for such joints is 0–130°. These prostheses require minimal bone resection during surgery, do not necessitate intercondylar osteotomy, and facilitate maintenance of the normal joint line position. The design prioritizes joint mobility, resulting in less mechanical constraint inherent to the prosthesis itself. CR prostheses have specific surgical indications, including cases where the PCL is neither lax nor contracted, and where there is no severe knee deformity or flexion contracture. They are contraindicated in certain conditions, such as rheumatoid arthritis, old tuberculous arthritis, PCL deficiency, injury, or insufficiency, as their use in these scenarios may predispose patients to posterior knee dislocation. Postoperative stability relies more heavily on the integrity of the ligamentous structures that stabilize the knee and the balance of the surrounding soft tissues. For younger patients with intact stabilizing structures, this type of cruciate-retaining prosthesis may be selected, with the expectation of achieving a greater range of motion.

(2) Semi-constrained prostheses: Posterior-stabilized (PS) knee prostheses are representative of semi-constrained designs. They substitute for the function of the posterior cruciate ligament (PCL) through a central tibial post and a corresponding femoral intercondylar box. The advantages of PS prostheses include: ① PCL resection facilitates easier balancing of extension and flexion gaps; ② Knee flexion can be increased by slightly enlarging the flexion gap, with a designed range of motion of 0–145°; ③ Good anteroposterior stability of the prosthesis. PS prostheses are suitable for patients with severe knee flexion deformities and valgus deformities, as well as those with compromised extensor mechanisms, such as patellectomy or patellar tendon injury. Potential disadvantages of PS prostheses include: ① High congruence transmits more stress through the prosthesis, thereby increasing shear stress at the prosthesis-bone interface and resulting in a higher loosening rate compared to cruciate-retaining (CR) designs; ② Greater bone resection during implantation increases the difficulty of revision surgery. Due to their broad surgical indications and relatively low technical difficulty, PS prostheses are currently the most widely used knee implants in clinical practice.

(3) Highly constrained knee prostheses: Such prostheses, including CCK and TC3, feature a taller tibial post and a more congruent femoral component design to address knee instability, thereby providing enhanced mediolateral and posterior stability. They are primarily indicated for primary total knee arthroplasty cases with collateral ligament insufficiency, significant bone defects, or severe deformities, as well as for revision surgeries following failure of primary arthroplasty performed with non-constrained or semi-constrained prostheses.

(4) Fully constrained knee prostheses: Fully constrained prostheses are represented by hinged knee designs. The hinge mechanism of such prostheses provides sufficient mechanical stability, making them suitable for use after tumor resection of the knee joint and in revision total knee arthroplasty cases with loss of knee stability. Early hinged knee prostheses had a 5-year failure rate exceeding 50%, primarily due to stress transmission resulting from varus-valgus angulation, horizontal rotation, and anteroposterior sliding.

Unlike hip implants, there is little difference among manufacturers in terms of materials used for knee joint prostheses; the primary distinctions lie in design. Current follow-up studies after total knee arthroplasty (TKA) have revealed that some patients experience moderate flexion instability and anterior knee pain postoperatively. These are common issues associated with existing knee prostheses and significantly impact patients’ quality of life after surgery. Other frequent complaints contributing to patient dissatisfaction after TKA include recurrent swelling and walking difficulties, which may indicate moderate flexion instability of the knee. Moderate flexion instability is characterized by stability at 90° of knee flexion but instability at 30°–45° of flexion. Although this type of instability is less pronounced than extension instability, it often impairs activities such as ascending and descending stairs, which involve moderate knee flexion.

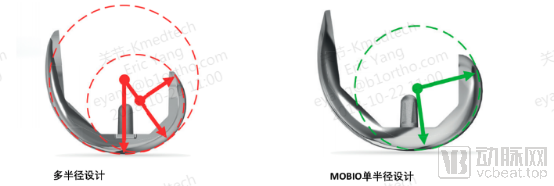

Manufacturers employ varying design solutions. Some adopt the single-radius principle; compared with traditional multi-radius prostheses, single-radius designs provide superior stability at mid-flexion, enabling patients to feel more stable during daily activities such as climbing stairs, getting in and out of vehicles, and squatting to sit or stand. Meanwhile, relative to multi-radius prostheses, they enhance quadriceps efficiency in knee extension, facilitate easier knee flexion, reduce patellar stress, lower the incidence of patellar pain, and improve patient satisfaction.

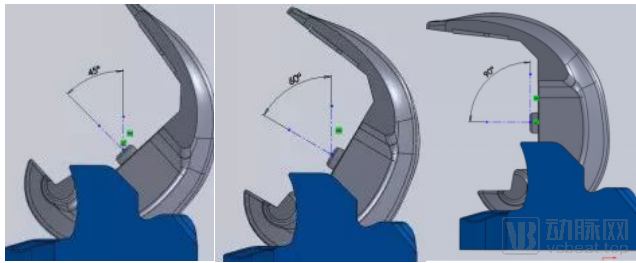

Some manufacturers have adjusted the contact between the post and the cam to address moderate flexion instability in patients after surgery. In early cam-post designs, contact between the post and the posterior wall of the cam occurred at knee flexion angles of 10°–45°. This configuration provided high knee stability; however, cam-post engagement occurred during normal walking (light knee flexion of 0°–45°), leading to accelerated polyethylene post wear and compromising prosthesis longevity. In contrast, late cam-post designs engaged only after 75° of knee flexion, thereby avoiding excessive contact and effectively preventing post wear. However, this design caused patients to experience knee instability during stair climbing (moderate knee flexion). A mid-term cam-post contact strategy was therefore adopted. During flexion, the contact surface between the cam and the post gradually shifts downward from top to bottom. At greater degrees of flexion, the cam contacts the base of the post, reducing impact forces and effectively preventing post fracture. Contact between the post and the posterior wall of the cam occurs at 45° of knee flexion, ensuring that no additional wear is incurred during normal walking. The formation of a dual-articulating surface between the post and the cam reduces contact pressure on the post, thereby minimizing wear.

45° flexion, 60° flexion, 90° flexion

One of the causes of postoperative anterior patellar pain is the design flaws of femoral condyles currently available on the market. Existing femoral condyles feature an excessively thick anterior profile and suboptimal trochlear design, which reduce the contact area and increase contact pressure.

Some manufacturers have modified the trochlear groove design to facilitate smooth, full-range motion of the patella from extension to deep flexion, particularly between 45° and 60°. A specially designed transition surface enables the contact between the patella and the trochlear groove to gradually shift from central area contact to linear contact on the medial and lateral sides, ensuring overall smooth movement.

Some manufacturers have adopted an arcuate design on both sides of the condyles in knee joint prostheses, deepening the trochlear groove and reducing soft tissue pressure. The rounded chamfers on both sides of the trochlea further mitigate friction between the prepatellar muscles and ligaments, thereby addressing postoperative anterior knee pain.

Summary: Maintaining knee joint stability is achieved through the combined effects of the patient’s intrinsic knee stability and the constraint level of the prosthesis. The status of the patient’s native knee stability determines the choice of prosthesis. Modern prosthetic materials and design techniques for artificial joints are advancing rapidly. Although there is a wide variety of brands among the aforementioned prostheses, their design philosophies are similar, each with its own distinctive features. Corresponding instrumentation systems also have their respective advantages and disadvantages; there is no absolute superiority or inferiority.

4.1 The international orthopedic market exhibits slow growth, a stable competitive landscape, and high concentration

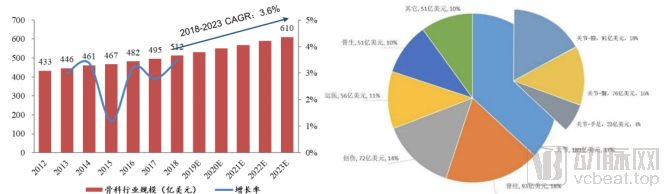

According to the ORTHOWORLD study, the orthopedics industry accounted for 9% of the global medical device market share in 2017, making it the fourth largest segment (the other three being IVD diagnostics, cardiovascular, and medical imaging) and the third largest consumables segment. From 2012 to 2018, the global orthopedics market grew from $43.3 billion to $51.2 billion, with a compound annual growth rate (CAGR) of 3%. It is projected to continue growing at a CAGR of 3.6% from 2018 to 2023, reaching a market size of $61 billion by 2023.

Global Orthopedics Market Size and Growth Rate; Revenue and Proportion of Global Orthopedics Sub-segments in 2018

Data Source: ORTHOWORLD, Southwest Securities

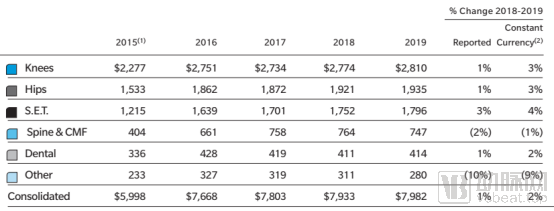

According to the ORTHOWORLD study, artificial joints accounted for 37% of the market in 2018, totaling $18.9 billion (knee: $9.1 billion; hip: $7.6 billion; small joints: $2.3 billion), making it the largest category. This was followed by spine (18%), trauma (14%), sports medicine (11%), bone biologics (10%), and others.

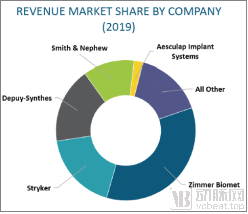

In 2019, the global joint replacement market was primarily dominated by five major players: Johnson & Johnson, Stryker, Link, Zimmer Biomet, and Smith & Nephew.

Zimmer Biomet ranked first, capturing a 27% market share, while Stryker and Johnson & Johnson-DePuy held 19% and 18%, respectively. Zimmer Biomet, Stryker, Johnson & Johnson, and Smith & Nephew collectively accounted for nearly 80% of the market, indicating a highly concentrated landscape.

4.2 China’s Joint Market Continues Steady Growth, with National Policies Favoring Import Substitution

Orthopedic medical devices have largely reached maturity in developed countries, where the major industry players are also concentrated. In contrast to the gradually slowing growth rate within the industry in these nations, China’s orthopedic market is poised to maintain robust high-speed growth over the next decade. This outlook is driven by rapid economic expansion, an aging population, advancements in science and technology, and the increasingly strong demand for healthcare among the general public.

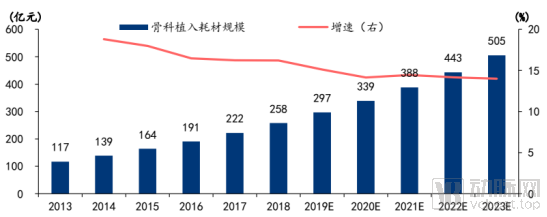

According to data from the Southern Institute of Pharmaceutical Economics, the market size of domestic orthopedic implant consumables reached RMB 25.8 billion in 2018, with a compound annual growth rate (CAGR) of 17.1% from 2014 to 2018. The institute projects that the market size will reach RMB 50.5 billion by 2023, representing a CAGR of 14.2% from 2019 to 2023, a growth rate higher than the global average.

Market Size and Growth Rate of Orthopedic Implant Consumables in China

Data Source: Southern Medical Economics Institute, Huatai Securities

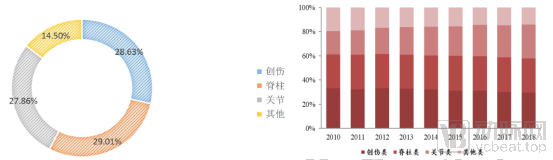

In 2018, the spine segment surpassed trauma to become the largest market segment in China, accounting for 29.01%; trauma ranked second at 28.63%; and joints ranked third at 27.86%. This structure differs from the global landscape, where joints constitute the largest orthopedic market segment.

2018 Market Share Distribution in Orthopedic Implant Sub-segments; Trends in the Market Share of Domestic Orthopedic Sub-sectors from 2010 to 2018

Data source: China Medical Device Blue Book (2019 Edition), Southwest Securities

China’s orthopedic consumption structure differs significantly from the global average, particularly from that of developed countries in Europe and the United States. This disparity is primarily attributed to gaps in domestic consumption levels and consumer mindsets; however, China is rapidly converging toward the standards observed in developed nations. As the growth rate of joint surgeries in China outpaces that of spinal and trauma procedures, the share of joint-related interventions continues to rise. Looking ahead, China’s orthopedic consumption structure is expected to align closely with the global pattern, ultimately positioning joint care as the leading segment.

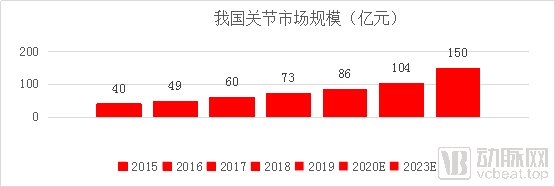

According to data provided by the Southern Economic Research Institute, China’s joint market size reached RMB 7.3 billion in 2018, a year-on-year increase of 21%. The market is projected to maintain a compound annual growth rate (CAGR) of 17% from 2018 to 2023, with its size exceeding RMB 15 billion by 2023.

Data Source: CFDA Southern Institute of Pharmaceutical Economics, Southwest Securities

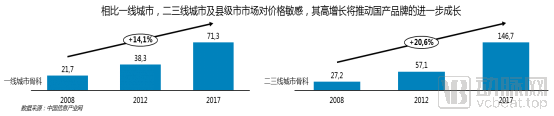

According to data from China Information Industry Network, market growth in China’s second- and third-tier cities and county-level cities is significantly faster than that in first-tier cities. Markets in second- and third-tier cities and county-level cities are price-sensitive; domestically produced joint prostheses are priced lower than imported ones and enjoy higher reimbursement rates, resulting in substantially lower out-of-pocket costs for patients compared with imported products. The growth of the orthopedic market in these regions benefits domestic joint prosthesis manufacturers.

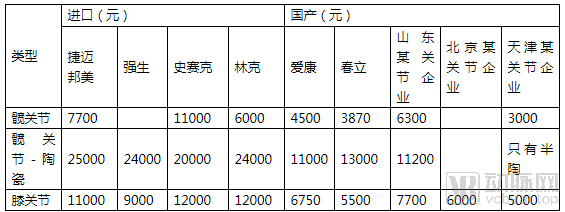

Regarding the competitive landscape of joint implants in China, according to data from Weiyi Orthopedics, the number of hip implantations in China reached 396,500 units in 2018, with 183,800 units being imported products and 212,700 units being domestically produced. Domestic products accounted for 53.91%, while imported products accounted for 46.08%, indicating that domestic hip joints dominated the market. In 2018, the number of knee implantations in China was 191,600 units, among which 143,400 units were imported products and 48,200 units were domestically produced. Imported products accounted for 74.84%, while domestic products accounted for 25.15%, showing that imported products held an absolute leading advantage. The ranking of total joint implantations in China in 2018 is shown in the table below:

Summary: The penetration rate of joint surgery in China is low. With the continuous development of China's economy, the penetration rate of joint surgery has been increasing. It is expected to maintain a compound annual growth rate (CAGR) of 17% from 2018 to 2023, which is significantly higher than the global average and exceeds that of the spine and trauma segments, making it the largest sub-segment in orthopedics by 2023. Currently, the localization rate for hip joints in China exceeds 50%, reaching 53.91%, while there is a significant gap in knee joints, with the market share of domestic products being less than 30%. There is substantial room for future growth, particularly in second- and third-tier markets. Under the national policy supporting import substitution, domestic joint manufacturers are poised for favorable development.

5.1 Zimmer Biomet

Zimmer Biomet’s core business is joint reconstruction, generating $4.745 billion in revenue in 2019, a 3% year-over-year increase, thereby firmly maintaining its position as the global leader in the joint reconstruction market. Revenue growth for its joint reconstruction business in the Asia-Pacific region slowed significantly, declining from over 5% in 2018 to 3–4% in 2019. Zimmer Biomet’s financial report also noted that its product pricing faced pressure in 2019 due to cost-containment measures by governments worldwide and pricing pressures from local healthcare systems.

As the Asia-Pacific leader, China has undoubtedly seen Zimmer Biomet’s growth slow down in the country.

5.2 Stryker

Stryker is one of the world’s leading medical technology companies. Stryker’s solutions focus on minimally invasive and open treatments for the shoulder, knee, hip, and small joints. Stryker offers a comprehensive and innovative portfolio of products and business solutions.

Stryker’s joint replacement business generated $3.198 billion in 2019, representing a year-over-year increase of 5.3%. In international markets excluding the United States, the joint replacement business achieved growth rates of 8.4% in 2018 and 5.5% in 2019. Within this segment, growth in the Asia-Pacific market slowed.

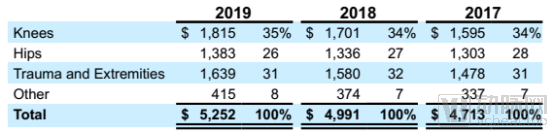

From the perspective of the joint market, Stryker’s orthopedics business is primarily focused on the U.S. market, where knee joints account for 74.2% and hip joints for 63.8%. In 2019, growth in the international market (with the Asia-Pacific region not separately disclosed) was sluggish, with the total growth for hip and knee joints reaching only 1.5%, down from 5% in 2018. As China is part of Stryker’s international market, based on the 1.5% growth of Stryker’s international joint business and the 5.5% growth of all its products in the Asia-Pacific region, it is estimated that Stryker’s joint business growth in China in 2019 did not exceed 5%, likely approaching 1.5%, which is significantly lower than the organic growth rate of the Chinese joint market itself.

5.3 Johnson & Johnson (DePuy)

DePuy Synthes is a subsidiary of Johnson & Johnson. DePuy Synthes offers one of the most comprehensive portfolios of orthopedic products and services worldwide, spanning joint reconstruction, trauma, spine, sports medicine, craniomaxillofacial surgery, power tools, and biomaterials. With approximately 18,000 employees across 60 countries and regions, DePuy Synthes generates annual sales of $10 billion and supports nearly one million orthopedic procedures globally each year. In 2015, DePuy Synthes acquired Olive Medical, gaining its visualization systems. This acquisition expanded DePuy’s product lineup, propelled its entry into the arthroscopic visualization market, and enhanced therapeutic options for patients suffering from pain or injuries in the shoulder, knee, hip, and small joints.

Johnson & Johnson Medical’s joint business generated $2.918 billion in revenue in 2019, a year-on-year decrease of 0.06%. The international joint business outside the United States recorded $1.166 billion in revenue in 2019. This indicates that Johnson & Johnson Medical’s growth in the Chinese market has slowed down.

5.4 Smith & Nephew

Smith & Nephew, founded in 1856, is a global leader in four key areas: orthopedic joint reconstruction, advanced wound management, sports medicine, and trauma, ranking first worldwide in the sports medicine sector. Headquartered in London, UK, the company maintains offices in 32 countries, employs approximately 15,000 people, and markets its products in over 100 countries globally. It is listed on both the London Stock Exchange and the New York Stock Exchange.

Smith+Nephew’s sports medicine business primarily focuses on joint repair, providing surgeons with a comprehensive range of instruments, technologies, and implants required for minimally invasive joint procedures, including the treatment of soft tissue injuries and degenerative conditions affecting the knee, hip, and shoulder.

According to Smith & Nephew’s 2019 annual report, its revenue in China reached $336 million in 2019, up from $270 million in 2018, representing a year-on-year growth of 24.4%. In contrast, the Emerging Markets segment, which includes China, saw a year-on-year growth of 11.7% in 2019, underscoring China’s leading position within the emerging markets.

Smith & Nephew’s main products span segments such as sports medicine, trauma, joints, and advanced treatment solutions. The joint reconstruction market accounts for 32.2% of the company’s total revenue, making it the largest segment. In 2019, Smith & Nephew achieved a 24.4% growth in China, demonstrating its continued strong growth potential.

Summary: Based on the revenue disclosures of major international orthopedic companies, the Asia-Pacific market serves as a growth engine for these manufacturers, with growth rates significantly higher than those in other regions. However, in recent years, particularly since 2017, the growth rate in the Asia-Pacific region for imported joint implant manufacturers—including Zimmer Biomet, Stryker, and Johnson & Johnson Medical (DePuy)—has gradually declined and is now markedly lower than the growth rate of China’s domestic joint implant industry. In contrast, Chinese domestic joint implant enterprises have generally recorded growth rates exceeding 30%, indicating clear signs that China is supporting domestically produced products.

Currently, approximately 32 companies in China have obtained regulatory approvals for artificial hip joints, and 22 companies have obtained approvals for artificial knee joints.

Hip Joint: Weigao, Beijing Kingcharly (B-one), Smith & Nephew, United Orthopedic, Beijing AK Medical, Beijing Chunli Zhengda, Beijing Baimtec, Tianjin Kangernuo, Wuhan DGS Biomedical, Shanghai Fusheng Medical, Shanghai Youke Orthopedics, Tianjin Renli Orthopedics, Tianjin Zhengtian Medical, Dezhou Jinyueying Medical, Shenzhen Bone Medical, Tianjin Viman Biological, Beijing Zhong'an Taihua, Beijing Bestar, Jiangsu Jinlu Group, Beijing UCM Jinghang, Shenzhen Jingwei Medical, Xiamen Double Medical, Tianjin Miaoya Biological, Tianjin Huajian Orthopedics, Beijing Tianxinfu Medical, Shanghai Shengshi Medical, Beijing Montaigne Medical, Shanghai Puwei Medical, Beijing Lidakang, Suzhou Xinrong Bolt, Hubei Walker Medical, Link Orthopedics

Knee Joints: Weigao, Beijing Kingcharly (B-one), Smith & Nephew, United Orthopedic Corporation, Beijing AK Medical, Beijing Chunli Zhengda, Beijing Montagen Medical, Beijing Lidakang, Dezhou Jinyueying Medical, Tianjin Huajian Orthopedics, Beijing Youcai Jinghang, Beijing Bestar, Shenzhen Born Medical, Tianjin Zhengtian Medical, Beijing Huakang Tianyi, Xiamen Double Medical, Tianjin Miaoya Biotechnology, Shenzhen Jingwei Medical, Wuhan Desheng Bayer, Shanghai Shengshi Medical, Beijing Baimatec, Beijing Virari Medical

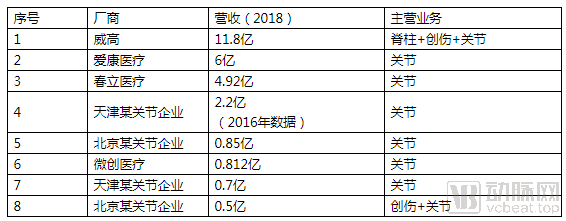

According to Bone’s orthopedic big data, the revenue of domestic orthopedic joint companies in 2018 is shown in the table below:

As can be seen from the 2018 revenues of each manufacturer in the table above and the 2019 revenues obtained through interviews, domestic manufacturers basically achieved a growth rate of over 30%, surpassing the industry's growth rate.

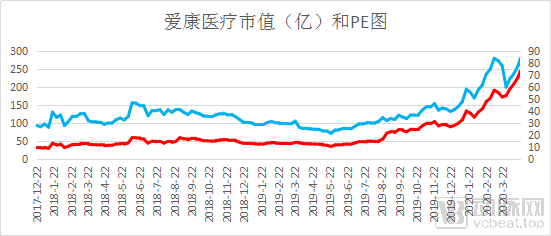

6.1 iKang Healthcare

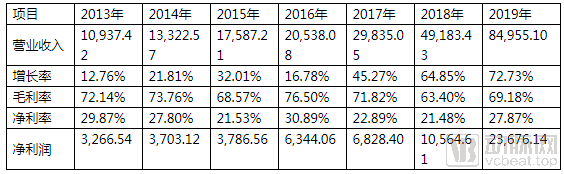

AK Medical was established in 2003 and listed on the Hong Kong Stock Exchange in 2017 (stock code: 01789). It is China’s first medical device company to commercialize 3D printing technology for implants used in joint and spinal replacement surgeries, while providing systematic clinical solutions. As a leading brand in joint implants in China, AK Medical continues to maintain its leadership position in the bone and joint implant market, achieving remarkable results through its comprehensive product portfolio covering hip and knee joint implants.

Unit: 10,000 yuan

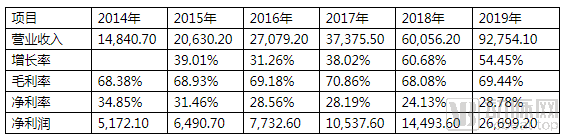

From 2014 to 2019, AK Medical achieved a compound annual growth rate (CAGR) of 35.72%, with growth rates exceeding 50% in both 2018 and 2019. Benefiting from this rapid expansion, AK Medical’s market capitalization and P/E multiple also increased significantly.

The chart below shows the market capitalization (red line) and P/E ratio (blue line) of AK Medical. As of April 21, 2020, AK Medical’s market capitalization reached RMB 24.6 billion, with a trailing twelve-month (TTM) P/E ratio of 82.6.

Data Source: Wind

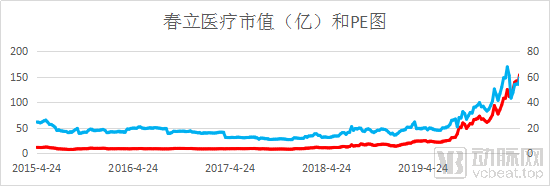

6.2 Chunli Zhengda

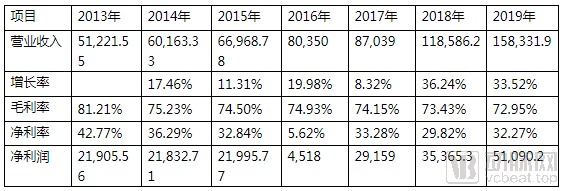

Chunli Medical, established in 1998, is a well-established domestic orthopedic company that initially built its reputation on joint products. It specializes in the R&D, manufacturing, and sales of high-quality surgical implants for hips, knees, and spine, along with accompanying surgical instruments. The company was listed on the Hong Kong Stock Exchange in 2015 under stock code 01858. Chunli Medical’s flagship product is ceramic joints, and its oncological joint prostheses are also highly regarded.

Unit: RMB 10,000

Chunli Medical achieved a compound annual growth rate (CAGR) of 34% from 2013 to 2019, with growth rates exceeding 60% in both 2018 and 2019. Benefiting from this rapid expansion, Chunli Medical’s market capitalization and P/E multiple also increased significantly.

The chart below shows Chunli Medical’s market capitalization (red line) and P/E ratio (blue line). As of April 21, 2020, Chunli Medical’s market capitalization reached RMB 15.4 billion, with a trailing twelve-month (TTM) P/E ratio of 58.4.

Data Source: Wind

6.3 Weigao Orthopedics

Weigao Orthopedics, established in 2005, has collaborated with Medtronic for several years. Its product portfolio covers the full range of orthopedic implants, making it the largest orthopedic implant company in China. It is a controlling subsidiary of Weigao Shares (Stock Code: 01066).

Based on the materials disclosed in May 2016 when Weigao Orthopedics conducted a back-door listing through Hengji Daxin, as well as the revenue data for Weigao Group’s orthopedic segment disclosed by Wind, the financial status of Weigao Orthopedics is shown in the table below. Unit: RMB 10,000

Note: The data for 2013–2015 are disclosed by Weigao Orthopaedics through its backdoor listing via Hengji Daxin; the data for 2016–2019 are from the annual reports of Weigao Group. As the annual reports did not disclose costs by business segment, the gross profit margins for 2016–2019 are forecast figures disclosed by Weigao Orthopaedics in connection with its backdoor listing via Hengji Daxin.

6.4 MicroPort Medical

MicroPort Scientific Corporation originated from Shanghai MicroPort Medical (Group) Co., Ltd., established in 1998. As a leading Chinese high-end medical device group, it has more than 260 marketed products covering ten major fields: cardiovascular intervention, orthopedic implants and reconstruction, rhythm management, electrophysiology, aortic and peripheral vascular intervention, neurovascular intervention, diabetes and endocrine management, and surgical solutions. The company was listed on the Hong Kong Stock Exchange in 2010 under stock code 00853. In January 2014, it completed the acquisition of the OrthoRecon business (“Joint Reconstruction Business”) and related assets of Wright Medical Group, Inc. (hereinafter referred to as “Wright”) for a total transaction amount of USD 290 million (approximately RMB 1.8 billion). Since then, MicroPort Orthopedics has become the sixth largest global orthopedic company specializing in hip and knee joint reconstruction, with its international and domestic businesses accounting for 60% and 40% of its operations, respectively. The annual sales revenue of the acquired OrthoRecon division was approximately USD 270 million, representing about 60% of Wright’s total sales. In 2018, MicroPort’s joint system business generated domestic operating revenue of RMB 80 million.

6.5 Youcai Jinghang

Beijing Youcai Jinghang Biotechnology Co., Ltd., established in 2014, is primarily engaged in the research and development, production, and sales of orthopedic implants. Youcai Jinghang has long collaborated with renowned domestic and international medical experts, materials scientists, and scholars to develop more than 30 series of “Jinghang” brand surgical implant prostheses for hips, knees, and the spine. These products include: porous-coated artificial hip joints, hydroxyapatite-coated hip joints, Series A artificial knee joints, Series C knee joints, hinged artificial knee joints, artificial shoulder joints, spinal internal fixation systems, and spinal fusion devices, along with their corresponding instrumentation. In September 2016, the company completed an angel financing round invested by AVIC High-Tech, with the amount undisclosed.