"Beauty" as the Driving Force: Accelerating the Prosperity of Dental Consumption — 2020 China Oral Healthcare White Paper

This report conducts a comprehensive study of the entire industry, centered on in-depth interviews, industry data, and market data, and supplemented by qualitative and quantitative consumer questionnaire surveys. Specifically, we interviewed senior executives from multiple dental healthcare chain institutions; the market research included a total of 2,427 valid samples; market data was derived from big data on the consumption behaviors of nearly 70,000 individuals; and industry data was sourced from authoritative bodies such as the National Bureau of Statistics and the National Health Commission.

In the “2020 White Paper on Oral Healthcare,” we present five directional conclusions regarding the current development of the oral healthcare industry. Below is a brief interpretation of the full text of the white paper:

1. Industry Overview:Oral healthcare demand exceeds 50%, treatment penetration rate constrains industry development, supply imbalance in service system, shift from "treatment" to "prevention"

2. Industrial System:“The Appearance Economy” Will Become a Key Factor Accelerating the Prosperity of the Dental Industry

3. Supply Side:The Youthful Shift in Consumer Demographics, Aesthetic Dentistry, and Trust-Based Consumption Constitute the “New” Characteristics of Dental Medical Service Consumption

4. Demand Side:The internet-based dental care model is gradually becoming the core business format of dental medical services, and precise patient acquisition will become the optimal choice for dental healthcare institutions.

5. Enterprise Side:Aggregation and Distribution: Internet Dental O2O Platforms Have Found a New Direction

China’s oral healthcare services industry is in a phase of rapid development, driven primarily by policy evolution, demand dynamics, and supply capacity. Compared with 2018, the oral healthcare consumer market continues to exhibit high disease prevalence, surging demand, supply–demand imbalances, and ongoing policy optimization. In response to these opportunities and challenges, the oral healthcare sector is undergoing transformation.

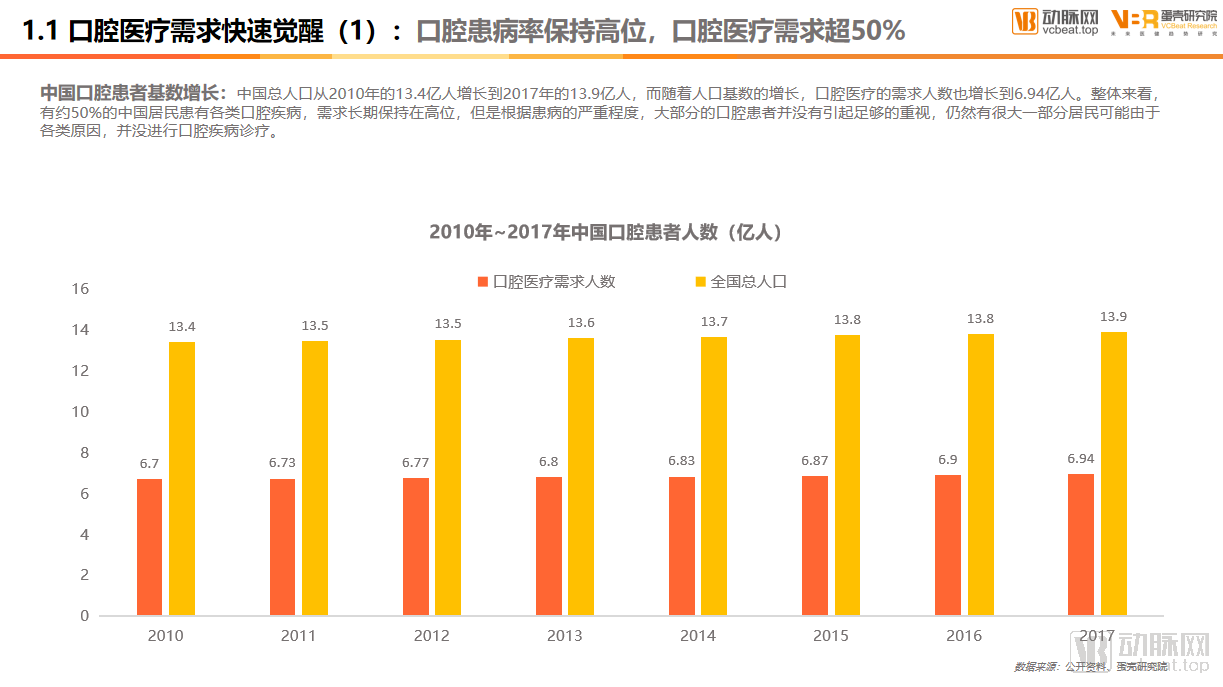

Oral disease prevalence remains high, with over 50% of the population having dental care needs

China's total population grew from 1.34 billion in 2010 to 1.39 billion in 2017, and with this expanding demographic base, the number of individuals requiring dental care rose to 694 million. Overall, approximately 50% of Chinese residents suffer from various oral diseases, keeping demand consistently high. However, due to varying degrees of disease severity, most patients do not attach sufficient importance to their condition, and a significant portion of the population remains untreated for oral diseases due to various reasons.

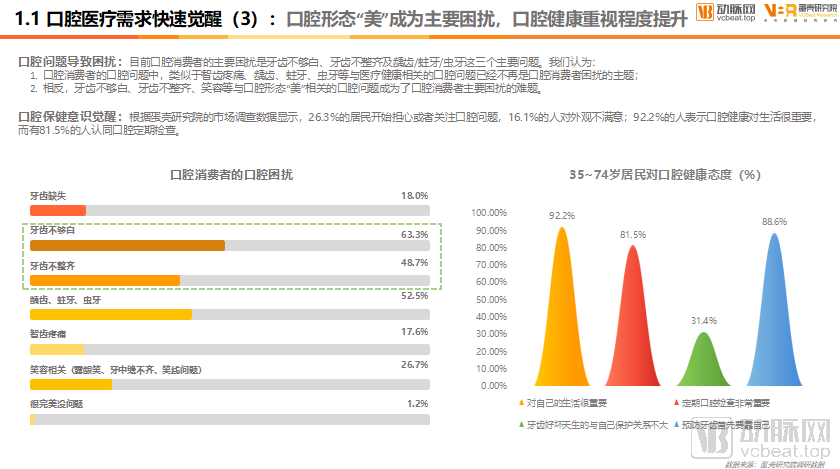

Aesthetic Concerns in Oral Morphology Become a Primary Issue, While Awareness of Oral Health Rises

Our survey reveals that the primary concerns of dental care consumers are currently teeth discoloration, misaligned teeth, and dental caries (cavities). Oral health issues such as wisdom tooth pain and dental caries are no longer the main sources of concern for these consumers. Instead, aesthetic-related issues, including teeth discoloration, misalignment, and smile appearance, have become the predominant challenges troubling dental care consumers.

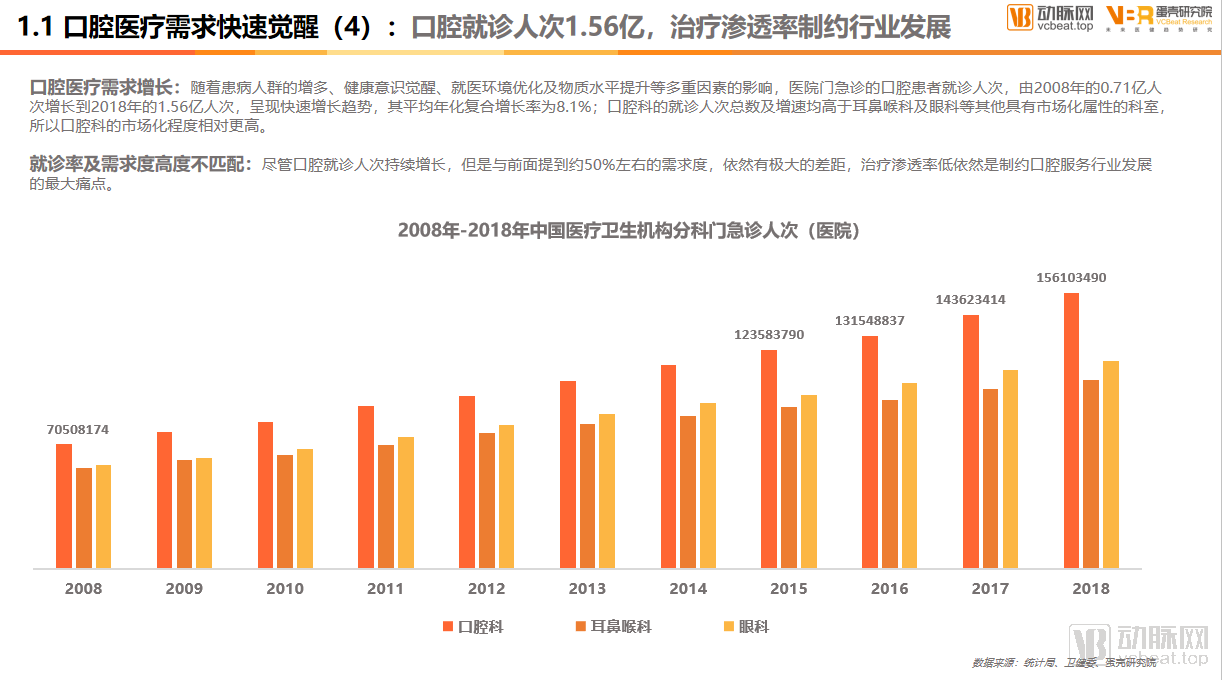

156 million dental visits: a significant mismatch between consultation rates and demand, with treatment penetration constraining industry growth

Driven by multiple factors, including a growing patient population, heightened health awareness, an optimized healthcare environment, and improved living standards, the number of outpatient and emergency dental visits in hospitals increased from 71 million in 2008 to 156 million in 2018.

However, from the perspective of oral disease prevalence, there is a significant mismatch between consultation rates and demand: although the number of dental visits continues to grow, it still falls far short of the approximately 50% demand rate mentioned earlier. The low treatment penetration rate remains the most critical bottleneck constraining the development of the oral healthcare services industry.

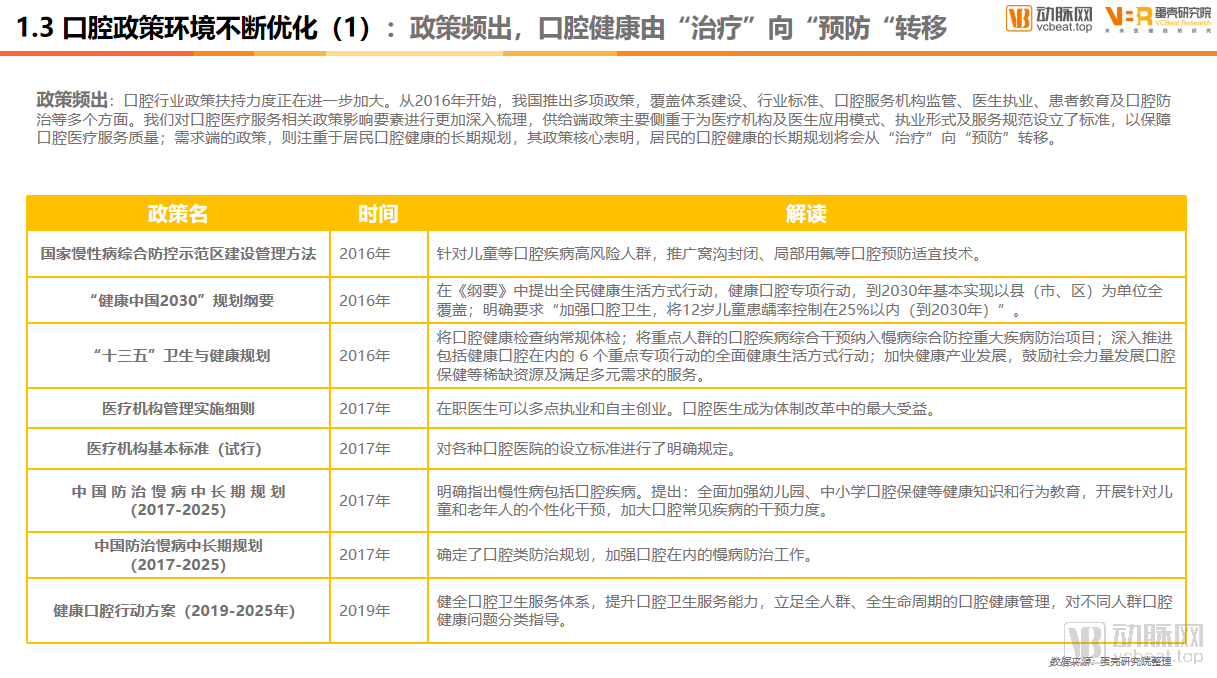

Frequent Policy Releases: Oral Health Shifts from “Treatment” to “Prevention”

Based on insights into the current state of dental healthcare consumption, we have found that dental medical services currently integrate concepts of both health and aesthetics. They possess the common characteristics of the general healthcare industry while also belonging to the category of consumption-upgrade products. Against the backdrop of economic development and consumption upgrading, China’s dental healthcare service industry is in a phase of rapid growth.

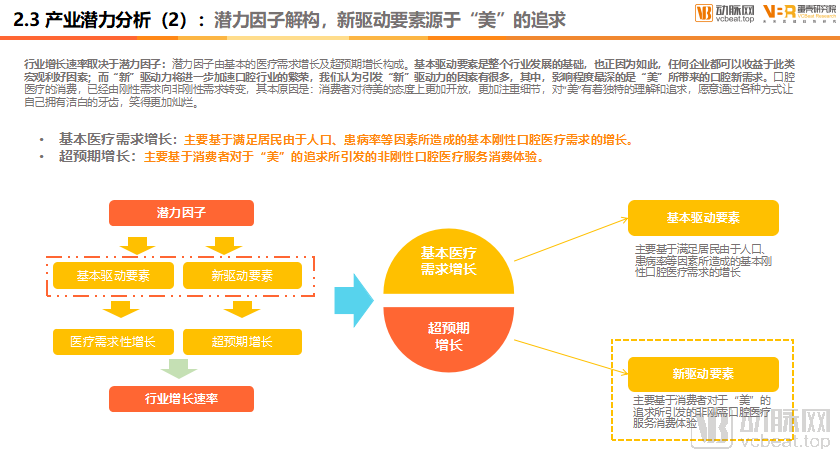

With the continuous development of the dental services industry, a market system centered on the terminal market has basically taken shape. Starting from an analysis of the entire industrial value chain, we will deconstruct the scale and market potential of the dental medical services industry. By assessing this potential, we believe it stems from two sources: fundamental drivers that fuel the growth of basic medical demand, and emerging drivers that trigger above-expected growth.

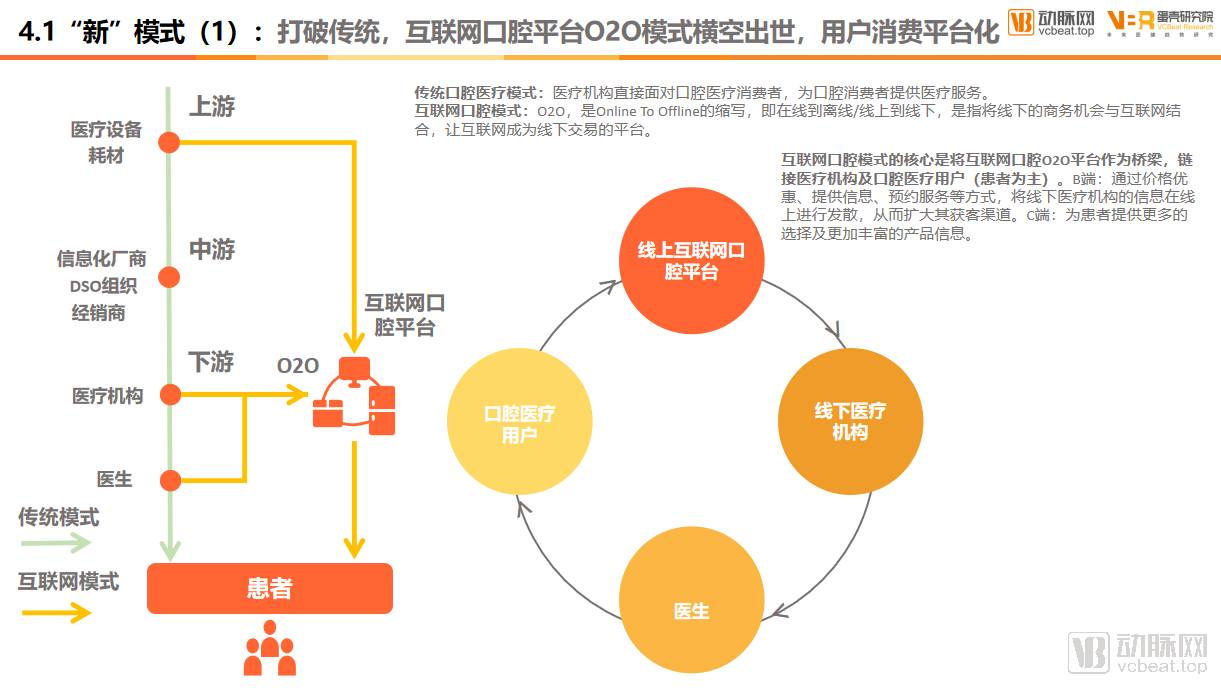

The Dental Industry Chain Takes Shape, with Internet Dental Platforms Building Bridging Links

The entire oral healthcare industry comprises five key entities: upstream manufacturers of consumables and instruments; midstream distributors of traditional dental equipment and consumables, as well as providers of informatics software; and downstream various medical institutions, internet-based dental platforms, and dentists. From the current stage of development, the industrial chain has taken shape, with internet-based dental platforms gradually emerging as a critical link connecting the entire industry.

Market Size: 139.8 Billion; Potential Factors Determine Industry Outlook

Based on dental visit data from the 2019 China Health and Family Planning Statistical Yearbook, as well as publicly available information compiled and estimated by us, we have derived the following figures: the average per-capita expenditure per dental visit is approximately RMB 472.5; there were 296 million dental visits nationwide, including approximately 156 million outpatient and emergency visits at hospitals, and approximately 140 million dental services provided by standalone or chain clinics. In light of these data, we estimate that the size of China’s dental medical service industry in 2018 was approximately RMB 139.8 billion, representing a year-on-year growth of about 24%.

Industry Growth Rate: Depends on the Potential Factor,The potential factor consists of basic driving elements and new driving elements.Fundamental drivers underpin the growth in medical demand, while new drivers spark growth that exceeds expectations. The “new” driving forces behind this outperformance will further accelerate the prosperity of the dental industry. We believe there are many factors contributing to these new drivers, with the most profound being the emerging dental demand driven by aesthetics.

Oral healthcare services integrate the concepts of health and aesthetics. Compared with 2018, the trend toward a younger consumer base has become increasingly pronounced, while the upgrade in consumption within the oral healthcare industry is accelerating further. To gain insights into the consumer profiles of oral healthcare users, we conducted extensive market research and data cleaning. From the basic characteristics of oral healthcare consumption to the behavioral preferences of online oral healthcare consumers, we systematically analyzed consumer preferences along the decision-making journey, exploring what online oral healthcare consumers need and what factors influence their decisions.

1"Oral Health User 'Self-Portrait'"

>>>>

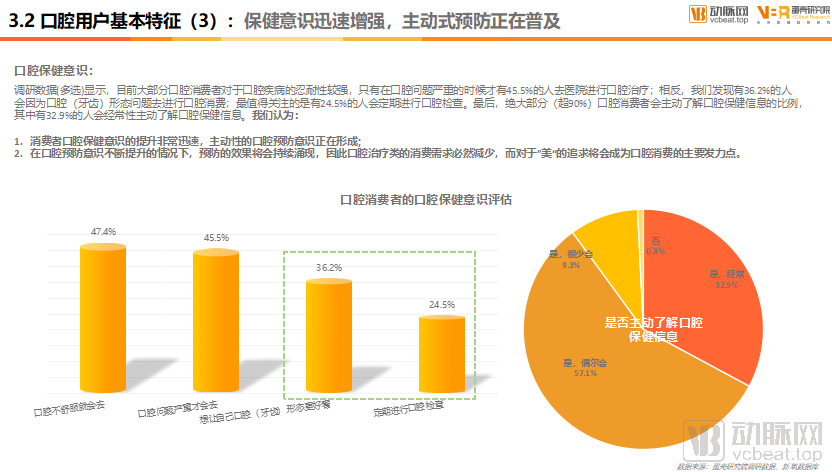

Health Awareness Is Rapidly Increasing, and Proactive Prevention Is Becoming Widespread

Survey data (multiple-choice) indicate that most dental care consumers currently exhibit a high tolerance for oral diseases, with only 45.5% seeking professional dental treatment when their condition becomes severe. In contrast, we found that 36.2% of individuals pursue dental services due to aesthetic concerns regarding the shape or appearance of their teeth. Notably, only 24.5% undergo regular dental check-ups. Finally, an overwhelming majority (over 90%) of dental care consumers proactively seek information on oral health, with 32.9% doing so frequently.

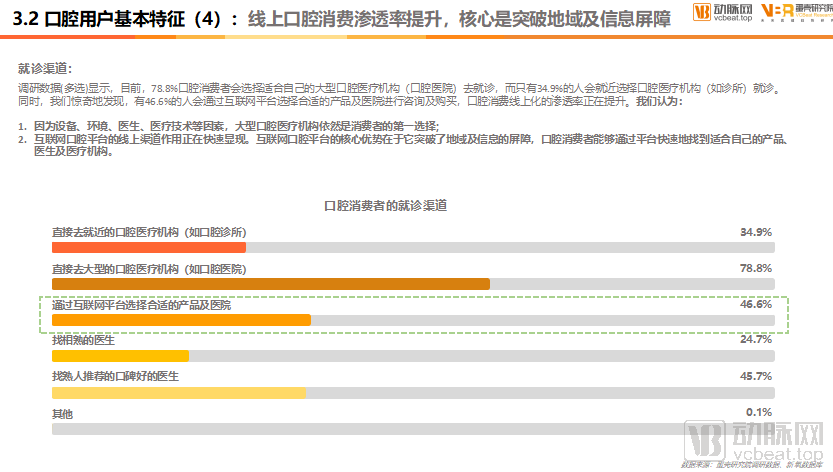

Rising Penetration of Online Dental Consumption: Breaking Down Geographic and Information Barriers

Survey data (multiple-choice) indicates that currently, 78.8% of dental consumers choose to seek treatment at large-scale dental healthcare institutions (such as dental hospitals) that suit their needs, while only 34.9% opt for nearby dental healthcare facilities (such as clinics). Meanwhile, we surprisingly found that 46.6% of individuals use internet platforms to select appropriate products and hospitals for consultation and purchase, indicating a rising penetration rate of online dental consumption.

From Dental Patients to Digital Dental Users: A Further Upgrade in Consumer Awareness

Through a questionnaire survey, VCBeat Research Institute investigated the purchasing channels of 1,814 users, focusing on whether they had purchased oral healthcare service products via internet-based dental platforms (such as So-Young, Meituan, and Alibaba). The survey results showed that 63.7% of consumers, totaling 1,221 individuals, had previously purchased internet-based dental products. Further investigation revealed that these respondents perceived the value of internet-based dental platforms to be primarily reflected in two major aspects:

1. Break through geographical and informational barriers, offering a wider selection of projects, institutions, and physicians;

2. Gain a more comprehensive understanding of one’s needs through multiple approaches to facilitate decision-making;

From general dental care consumers to users of online dental healthcare services, this shift reflects an upgrade in consumer awareness. Next, let us examine the consumption characteristics of users of online dental healthcare services.

2User "Self-Portrait" of Internet Dental Medical Services

>>>>

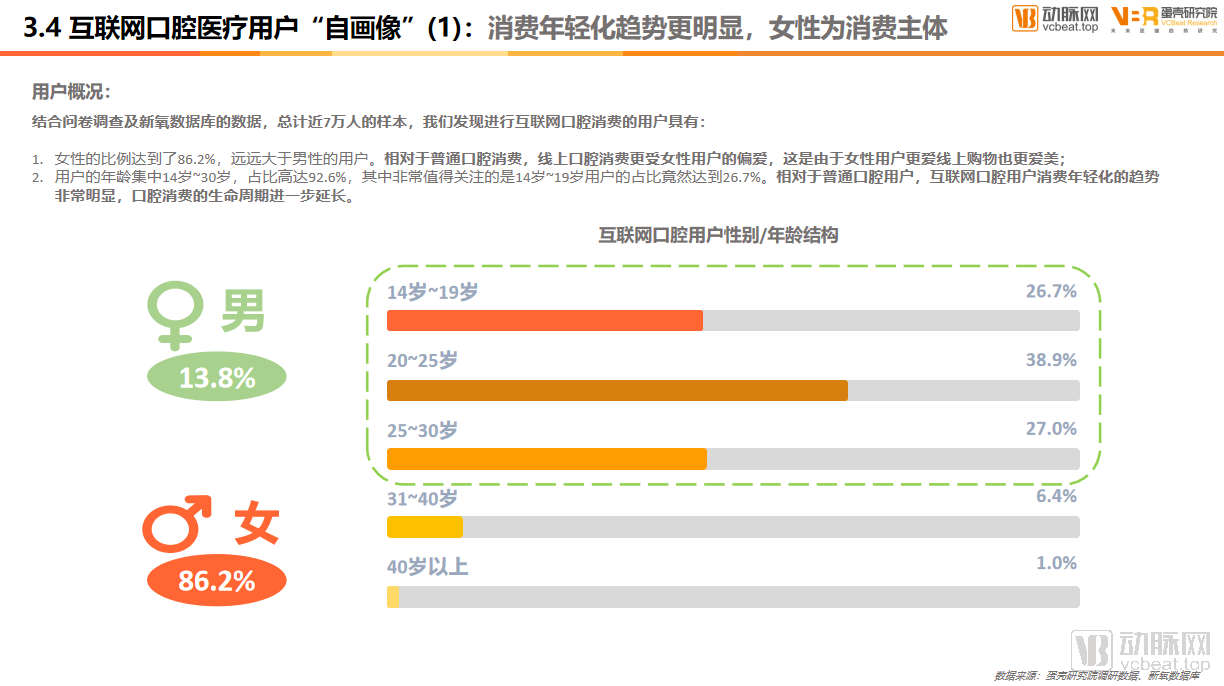

The Trend of Younger Consumers Is More Pronounced, with Women as the Primary Consumer Group

The proportion of female users reached 86.2%, significantly higher than that of male users. Compared with traditional dental care consumption, online dental care services are more favored by female users, driven by their greater propensity for online shopping and stronger focus on aesthetics. The user base is predominantly aged between 14 and 30 years, accounting for 92.6% of the total. Notably, users aged 14 to 19 represent a substantial 26.7%. In contrast to traditional dental care consumers, internet-based dental care users exhibit a pronounced trend toward younger demographics, further extending the lifecycle of dental care consumption.

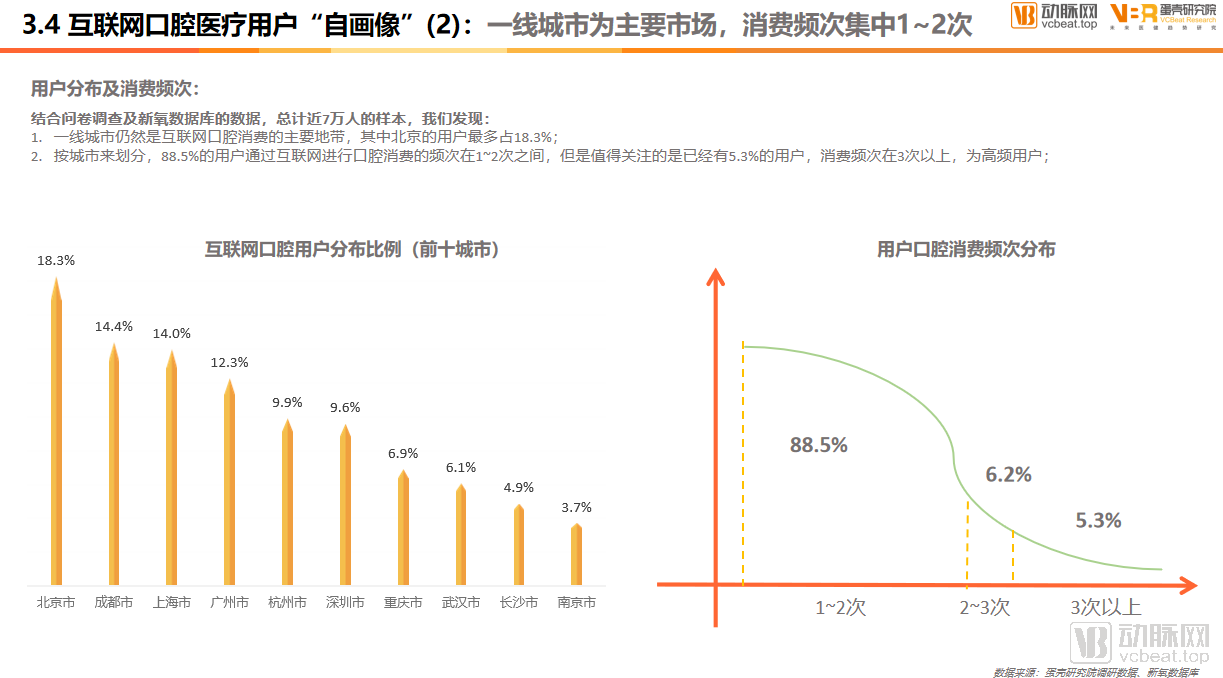

First-tier cities serve as the primary market, with consumption frequency concentrated at 1–2 times.

Tier-1 cities remain the primary hubs for online dental consumption, with Beijing accounting for the largest share of users at 18.3%. By city, 88.5% of users engage in online dental services 1–2 times; however, it is noteworthy that 5.3% of users are high-frequency consumers, utilizing these services more than three times.

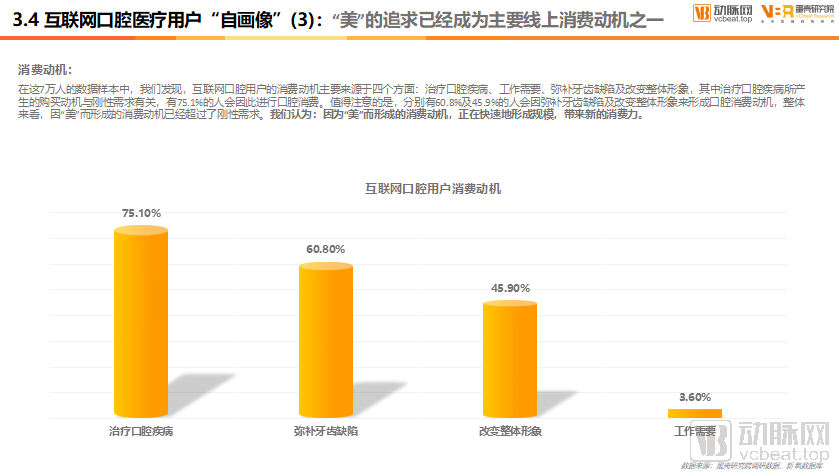

“The pursuit of ‘beauty’ has become one of the primary drivers of online consumption.”

The consumption motivations of online dental users primarily stem from four aspects: treating oral diseases, occupational requirements, correcting dental defects, and enhancing overall appearance. Among these, the purchase motivation driven by the treatment of oral diseases is related to rigid demand, with 75.1% of individuals engaging in dental consumption for this reason. Notably, 60.8% and 45.9% of individuals are motivated to consume dental services to correct dental defects and improve their overall appearance, respectively. Overall, consumption motivations driven by “aesthetics” have surpassed those driven by rigid demand. We believe that consumption motivations driven by “aesthetics” are rapidly scaling up, generating new consumer spending power.

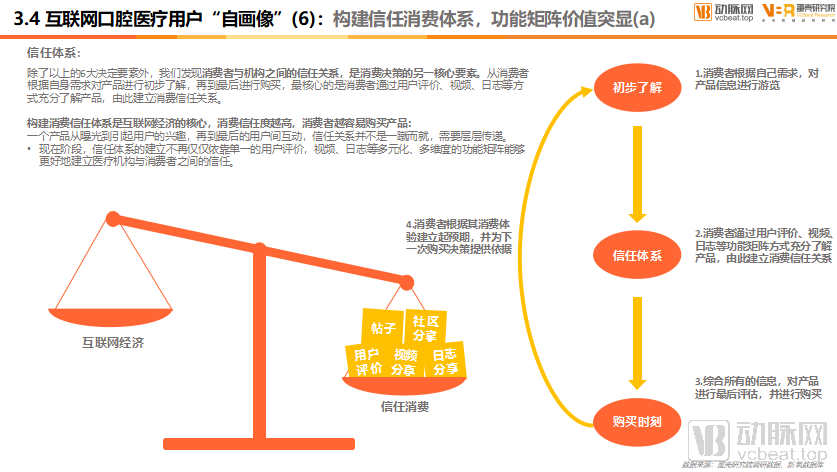

Building a Trust-Based Consumption System: The Value of the Functional Matrix Stands Out

The trust relationship between consumers and institutions is another core element of consumer decision-making. From the initial understanding of products based on their own needs to the final purchase, the most critical aspect is that consumers fully understand the product through user reviews, videos, logs, and other means, thereby establishing a relationship of consumer trust.

Building a consumer trust system is the core of the internet economy. The higher the level of consumer trust, the more likely consumers are to purchase products. From product exposure to generating user interest, and finally to interactions among users, trust relationships are not established overnight but require gradual, layered cultivation.

At this stage, the establishment of a trust system no longer relies solely on individual user reviews; a diversified, multi-dimensional functional matrix—including videos and logs—can more effectively build trust between healthcare institutions and consumers.

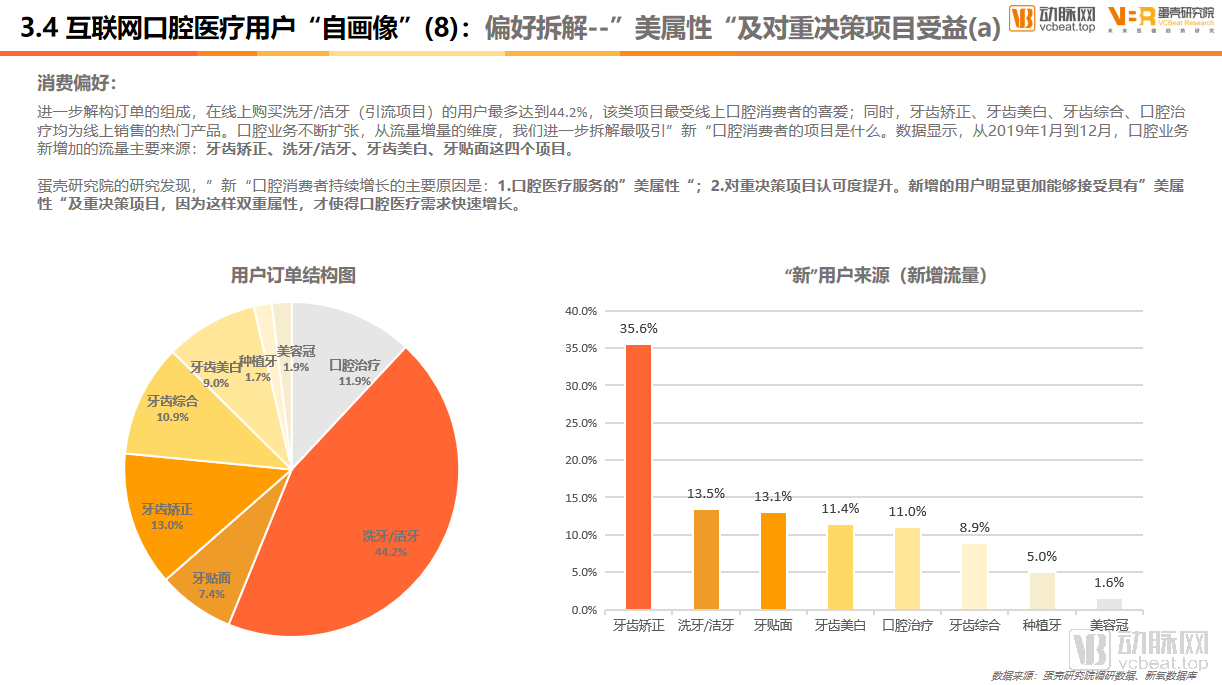

Preference Breakdown—“Aesthetic Attributes” and Benefits for High-Stakes Decision-Making Projects

The online dental healthcare services most favored by online consumers are dental cleaning/scaling (customer acquisition offerings). Meanwhile, orthodontics, teeth whitening, comprehensive dental care, and general dental treatments are also popular products in online sales. As the dental business continues to expand, we further break down which services are most attractive to “new” dental consumers from the perspective of incremental traffic growth. Data shows that from January to December 2019, the primary sources of newly added traffic for dental services were orthodontics, dental cleaning/scaling, teeth whitening, and dental veneers.

Research by VCBeat Institute reveals that the primary driver behind the sustained growth of “new” dental consumers is:1. The "aesthetic attribute" of dental medical services; 2. Increased recognition for high-involvement decision-making projects.New users are significantly more receptive to services with “aesthetic attributes” and high-involvement decision-making; it is this dual nature that has driven the rapid growth in demand for dental medical services.

In the report, we provide a detailed analysis of the key decision-making nodes for online dental care consumers across multiple dimensions—including user profiles, consumption motivations, visitation pathways, consultation journeys, decision factors, trust systems, consumption preferences, and payment methods—and have mapped out their decision-making pathways.

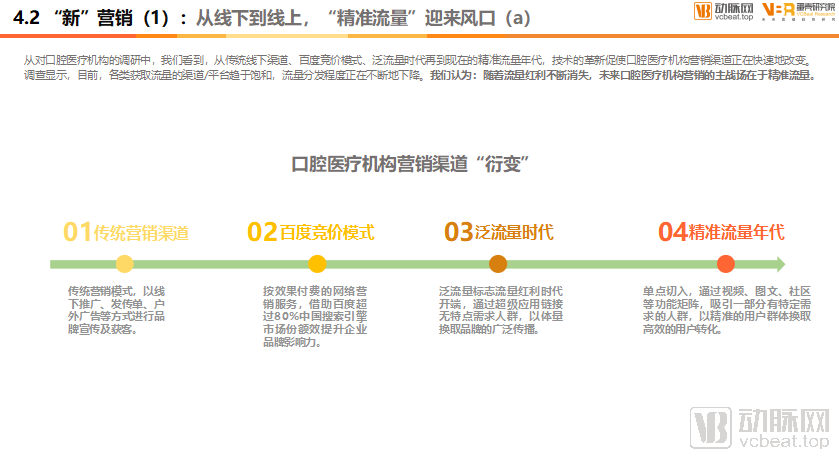

As the oral healthcare services industry continues to upgrade, VCBeat has observed that platform-based enterprises founded on internet technologies are rapidly penetrating the market, continually transforming traditional patterns of medical care and consumption. Marketing strategies for internet-based dental platforms are also undergoing continuous exploration, evolving from traditional offline channels and Baidu’s pay-per-click bidding model, through the era of broad traffic acquisition, to the current age of precision targeting. Technological innovations are driving rapid changes in the marketing channels employed by dental healthcare institutions.

Breaking with Tradition: The Emergence of the O2O Model for Internet Dental Platforms and the Platformization of Consumer Spending

The core of the internet-based dentistry model is to use an online-to-offline (O2O) dental platform as a bridge connecting healthcare institutions and dental patients (primarily patients). On the B-side, it expands customer acquisition channels for offline medical institutions by disseminating their information online through price discounts, information provision, and appointment services. On the C-side, it offers patients more choices and richer product information.

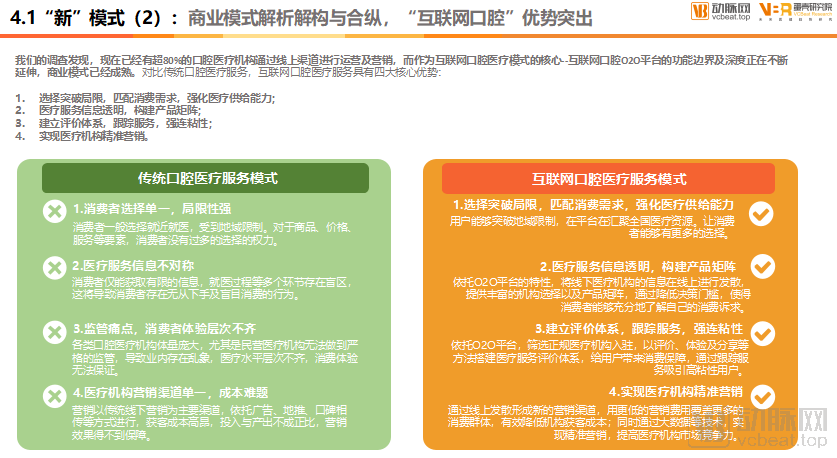

Business Model Analysis: Deconstruction and Strategic Alliances, with Prominent Advantages in “Internet Dentistry”

Our survey reveals that over 80% of dental healthcare institutions now leverage online channels for operations and marketing. As the cornerstone of the internet-based dental care model, internet dental O2O platforms are continuously expanding their functional boundaries and depth, with their business models having reached maturity. Compared to traditional dental healthcare services, internet-based dental healthcare services offer four core advantages:

1. Break through limitations, align with consumer demand, and strengthen healthcare supply capacity;

2. Enhance transparency of medical service information and build a product matrix;

3. Establish an evaluation system, track services, and strengthen user stickiness;

4. Achieve precision marketing for healthcare institutions.

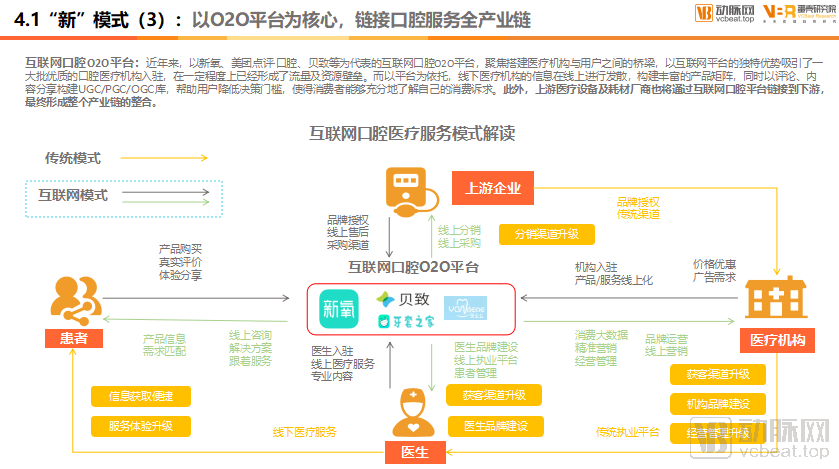

Centered on the O2O platform, linking the entire industrial chain of dental services

Internet-based Dental O2O Platforms: In recent years, internet-based dental online-to-offline (O2O) platforms, represented by SoYoung, Meituan-Dianping Dental, and Beizhi, have focused on building bridges between medical institutions and users. Leveraging the unique advantages of internet platforms, they have attracted a large number of high-quality dental medical institutions to join, thereby establishing certain barriers in terms of traffic and resources. Relying on these platforms, offline medical institutions disseminate information online, construct diverse product portfolios, and build user-generated content (UGC), professional-generated content (PGC), and occupationally-generated content (OGC) libraries through reviews and content sharing. This helps lower the decision-making threshold for users, enabling consumers to fully understand their consumption needs. Furthermore, upstream manufacturers of medical equipment and consumables will also connect with downstream entities via these internet dental platforms, ultimately achieving integration across the entire industry chain.

From Offline to Online, “Precision Traffic” Seizes the Opportunity

From our surveys of dental healthcare institutions, we have observed that technological innovation is rapidly transforming their marketing channels, evolving from traditional offline channels and Baidu’s pay-per-click bidding model, through the era of broad-traffic acquisition, to the current age of precision traffic.

Surveys indicate that current channels and platforms for acquiring traffic are approaching saturation, with the efficiency of traffic distribution continuously declining. We believe that as the dividends from traffic growth continue to dissipate, the primary battlefield for marketing in dental medical institutions will shift toward precision-targeted traffic.

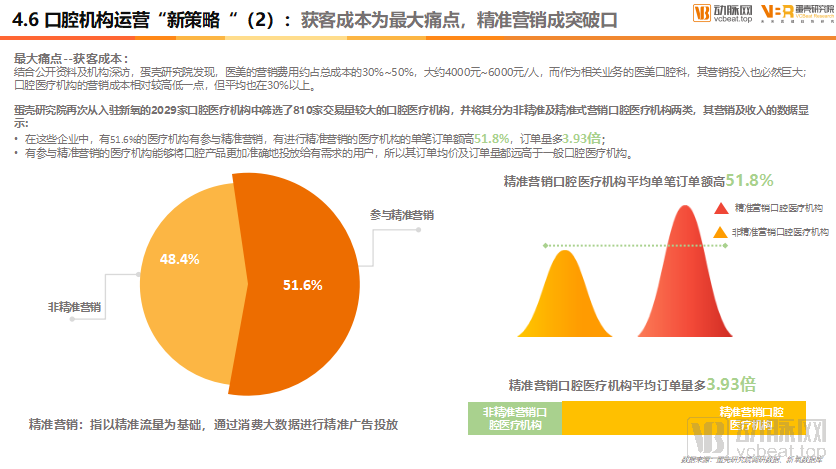

Customer Acquisition Cost Is the Biggest Pain Point, While Precision Marketing Becomes the Breakthrough

Based on public information and in-depth interviews with industry institutions, VCBeat Research Institute has found that marketing expenses in the medical aesthetics sector account for approximately 30%–50% of total costs, amounting to roughly RMB 4,000–6,000 per customer. As a related segment, dental aesthetic services also entail substantial marketing investments. While marketing costs for dental medical institutions are relatively lower, they still average above 30%.

VCBeat Research Institute once again selected 810 dental medical institutions with higher transaction volumes from the 2,029 dental medical institutions registered on So-Young, and categorized them into two groups: those employing non-targeted marketing and those employing targeted marketing. Data on their marketing activities and revenue reveal the following:

1. Among these enterprises, 51.6% of medical institutions participated in precision marketing; those engaging in precision marketing achieved a 51.8% higher average order value and 3.93 times the order volume;

2. Healthcare institutions that engage in precision marketing can more accurately target dental products to users with specific needs, resulting in significantly higher average order values and order volumes compared to general dental healthcare providers.

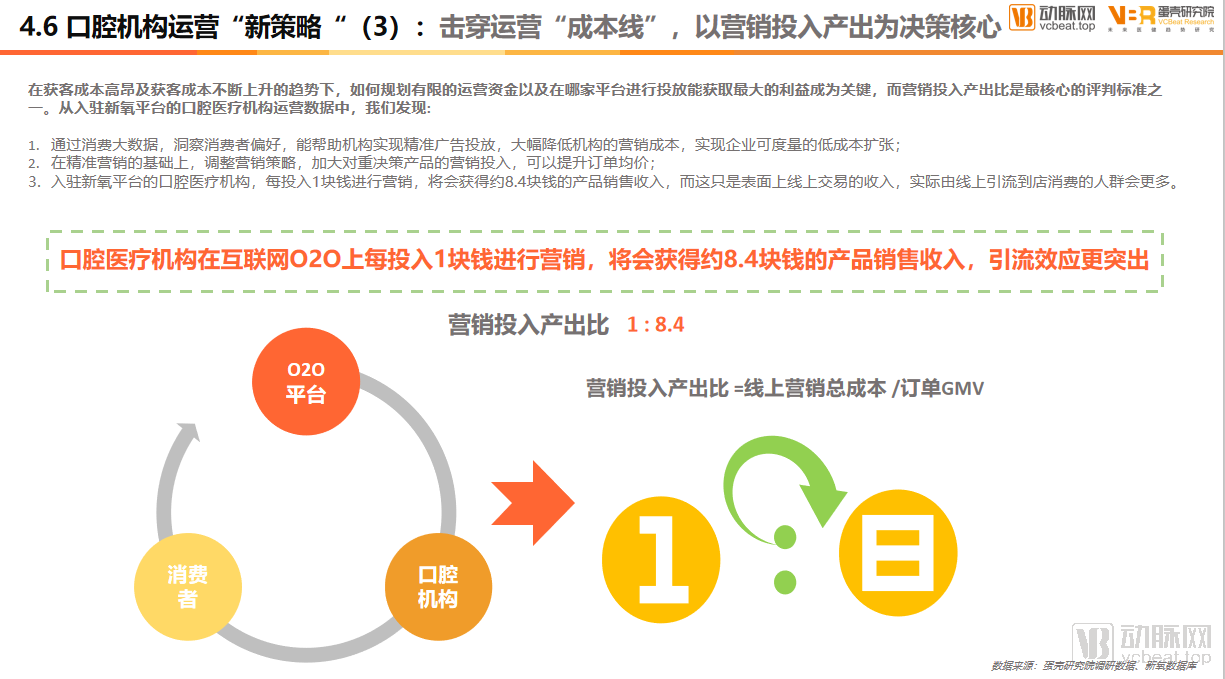

Breaking Through the Operational “Cost Line”: Making Marketing ROI the Core of Decision-Making

Amid high and rising customer acquisition costs, how to allocate limited operational funds and which platforms to advertise on for maximum benefit have become critical issues, with marketing return on investment (ROI) being one of the core evaluation metrics. Based on the operational data of dental institutions on the So-Young platform, we found:

1. By leveraging consumer big data to gain insights into consumer preferences, institutions can achieve precise ad targeting, significantly reduce marketing costs, and enable measurable, low-cost business expansion;

2. By adjusting marketing strategies based on precision marketing and increasing investment in the promotion of high-consideration products, the average order value can be increased;

3. For every 1 yuan spent on marketing by dental medical institutions listed on the SoYoung platform, approximately 8.4 yuan in product sales revenue is generated. This figure reflects only online transaction revenue; in reality, a larger volume of customers are driven online to make offline in-store purchases.

As the core of the internet-based dental care model, online-to-offline (O2O) dental platforms are a key focus of our research. With the continuous expansion of internet platform services, the emergence of various dental-specific platforms signals that internet companies have targeted the vast market for dental medical services. In this environment, competition among internet dental platforms is becoming increasingly fierce. Recognizing their own strengths and weaknesses is essential for standing out, a challenge that every enterprise is currently contemplating.

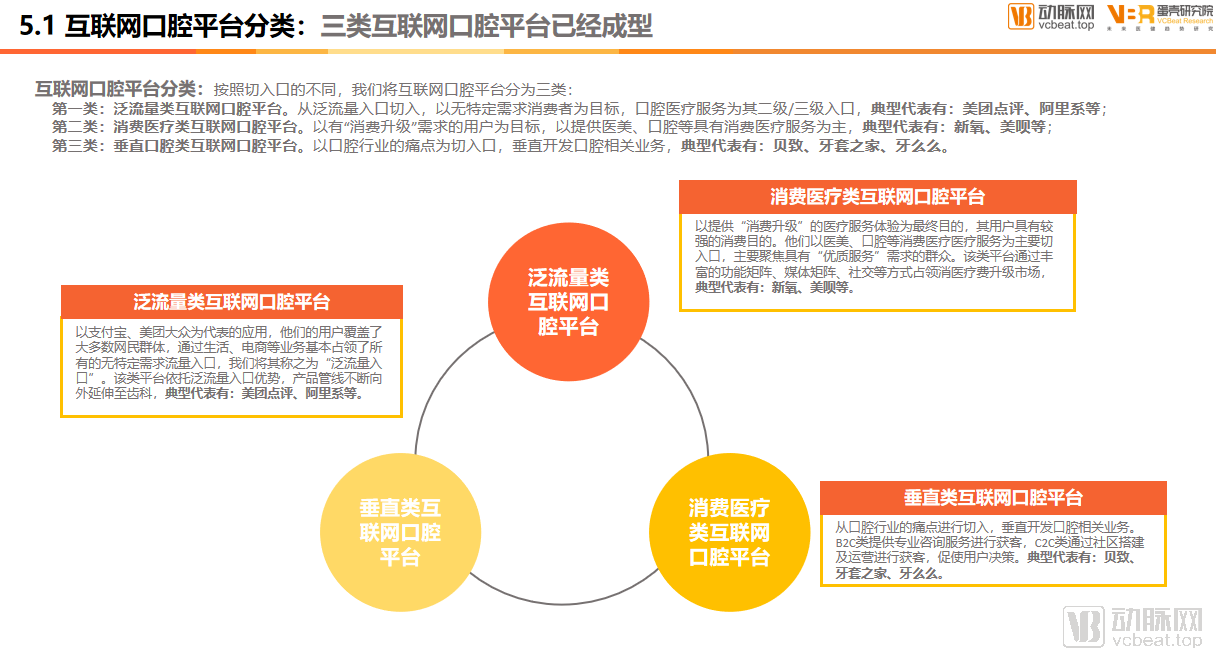

Three Types of Internet Dental Platforms Have Taken Shape

Based on different entry points, we categorize internet dental platforms into three types:

Category I:Internet-based dental platforms driven by broad-traffic channels. These platforms enter the market through high-volume, general-traffic portals, targeting consumers without specific dental needs, with dental medical services serving as secondary or tertiary entry points. Typical representatives include Meituan-Dianping and Alibaba-affiliated platforms.

Category II:Internet-based dental platforms in the consumer healthcare sector. Targeting users with “consumption upgrade” needs, they primarily provide consumer-oriented medical services such as aesthetic medicine and dentistry. Typical representatives include SoYoung and Meibei.

Category III:Vertical online dental platforms. These platforms address pain points in the dental industry by vertically developing dental-related services. Typical representatives include Beizhi, Yatao Zhijia (Brace Home), and Yameme.

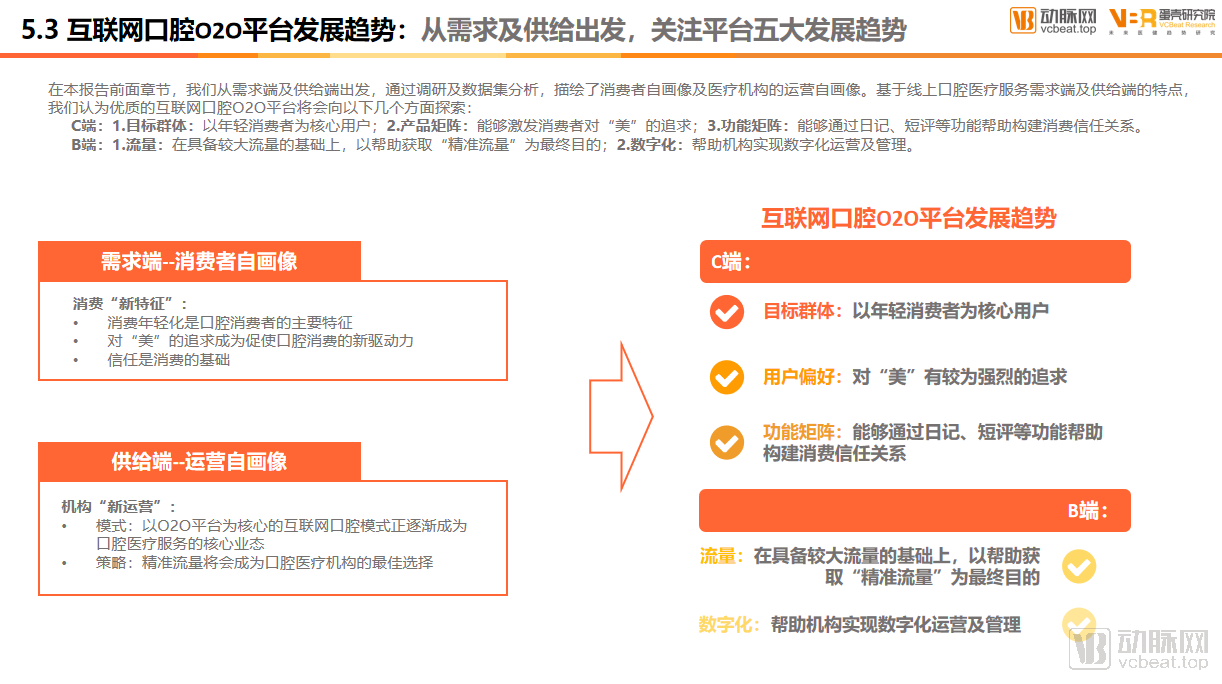

Focusing on the Five Major Development Trends of Platforms from the Perspectives of Demand and Supply

In the earlier sections of this report, we outlined consumer profiles and operational profiles of healthcare institutions by examining both the demand and supply sides through surveys and dataset analysis. Based on the characteristics of the demand and supply sides in online dental healthcare services, we believe that high-quality internet-based dental O2O platforms will explore the following areas:

C-end:1. Target Audience: Young consumers as the core user base; 2. Product Matrix: Capable of stimulating consumers’ pursuit of “beauty”; 3. Functional Matrix: Helps build consumer trust through features such as diaries and short reviews.

B-side:1. Traffic: Based on a foundation of substantial traffic volume, with the ultimate goal of facilitating the acquisition of "targeted traffic"; 2. Digitalization: Assisting institutions in achieving digitalized operations and management.

A retrospective analysis of the entire report, spanning from the current state of the industry and its supply chain to its underlying development logic, reveals that the oral healthcare sector is undergoing a new transformation. The future of the oral healthcare industry is poised to be remarkable, with potential drivers—comprising both fundamental and emerging factors—propelling rapid industry advancement. The oral healthcare services segment now stands at a pivotal juncture; in the face of opportunities and challenges, how can enterprises rise to the occasion and thrive?

There are many development trends in the oral care services industry, with the market being the most sensitive to its evolution. Through an analysis of the oral healthcare services sector using VCBeat’s research framework, we have identified numerous common trends. By filtering and analyzing these trends with data, we believe that changes in two dimensions—consumption structure and business models—will significantly influence the future development path of the oral healthcare industry. These changes encompass five major trends involving consumer demographics, social awareness, demand-side dynamics, supply-side dynamics, and payment mechanisms.

Trend 1: Consumer Demographics – The Trend Toward Younger Consumers Is Becoming Increasingly Pronounced

The proportion of consumers under the age of 25 is also rising rapidly. The new consumer cohort formed by those born in the late 1990s and early 2000s exhibits distinct consumption patterns and a curiosity-driven mindset. Their purchasing desires are driven by multiple factors, such as the pursuit of individuality and fashion trends. Meanwhile, having been born into an era of information explosion characterized by the internet and smartphones, they are keen on acquiring vast amounts of information online.

Trend 2: Social Awareness – The Pursuit of “Beauty” Continues to Rise

The new consumer cohort formed by those born after 1995 and 2000 has a high pursuit of beauty. Women remain the absolute main force in pursuing “beauty,” but nowadays, an increasing number of men are also beginning to pay attention to their appearance. In addition to common facial features, more and more people are starting to focus on the aesthetics of their teeth for a bright smile.

Trend 3: Demand Side—New Consumption Patterns

Application of 5G Technology and Facial Diagnosis Technology. The interconnectivity between platforms and enterprises will become increasingly tight. Platforms will build integrated medical services for institutions, offering services such as oral health consultations and remote dental diagnosis and treatment, which will significantly increase consumers’ reliance on the internet. Consumption patterns will further upgrade, with online consumption and online consultations deepening dependence on internet-based dental care.

Trend 4: Supply Side – Optimization of Supply Capacity

Digital Healthcare, Marketing Channel Optimization, and Industry Chain Integration. The digitalization of healthcare will further accelerate. Leveraging digital tools to reduce marketing costs, enhance operational efficiency, and optimize the supply chain system will become core competencies for enterprises. Meanwhile, internet-based dental platforms will play a pivotal role in providing digital management solutions, high-quality channels, and linking the upstream and downstream segments of the industry chain.

Trend 5: Payment Side – Penetration of Financial Products

Penetration of Medical Insurance. The trend of financial product penetration is accelerating. Dental service providers and insurance institutions are jointly developing diversified insurance products to complement the national basic medical insurance system, thereby addressing consumers’ multi-tiered needs. By entering from the payment side, medical insurance serves as a new customer acquisition channel for enterprises and demonstrates a commitment to dental care consumers.

The Rise of Consumer-Oriented Dental Care: Aesthetic-Driven Growth Accelerates Industry ProsperityThe dental industry is currently navigating a landscape filled with both opportunities and adjustments. Stakeholders across the sector should gain a clear understanding of prevailing industry pain points by examining the current market status; identify the specific needs of younger consumer demographics from the demand side; explore pathways to optimize supply-side capabilities; align institutional requirements and operational strategies with underlying industry logic; and formulate corporate development roadmaps based on future trends.

The above is an excerpt from the report. The complete framework of the report is as follows. Scan the QR code to access the mini-program and read the full report for free:

Scan to get the full report