Major Shifts in China's Health Insurance: Long-Term Care Insurance Expansion, Critical Illness Policy Revisions, and the Looming Surge of Medical Insurance

Since the beginning of this year, the health insurance industry has appeared calm on the surface, but in reality, many significant developments have taken place.

First, the central government articulated its vision for a “multi-tiered medical security system.” This was followed by health insurance companies releasing their annual reports, revealing that more than half had achieved profitability, thereby ending the trend where higher health insurance premiums correlated with greater losses. Subsequently, the pilot program for long-term care insurance expanded from 15 to 29 cities. Most recently, revisions were made to the “Guidelines for the Use of Disease Definitions in Critical Illness Insurance,” which added certain covered conditions and relaxed the payout criteria for specific definition clauses.

Quietly, from the macro to the micro level, significant changes have emerged in the development trends of health insurance. The most notable shift is a new direction in the structure of existing specialized insurance products: critical illness insurance will no longer dominate alone, as long-term care insurance and medical insurance will advance in tandem. In particular, medical insurance, due to its closest alignment with the nature of medical security, is poised to become the insurance category with the greatest growth potential in the future.

However, the pain points and bottlenecks currently facing the industry are also very obvious. The existing operational capabilities are difficult to match the industry's growth rate of nearly 30%. There seems to be an insurmountable and indescribable bottleneck and gap between the two major fields of the medical industry and the health insurance industry. Health insurance has been unable to access the core data of medical care and medical insurance. It is still uncertain when this gap and rupture will be bridged by policy or technology.

Through interviews with numerous industry insiders, VCBeat aims to document the significant changes currently unfolding in the sector, along with the underlying causes and logic driving them.

We believe that only those willing to embrace these changes can seize the opportunities of the era and take control of their own destiny.

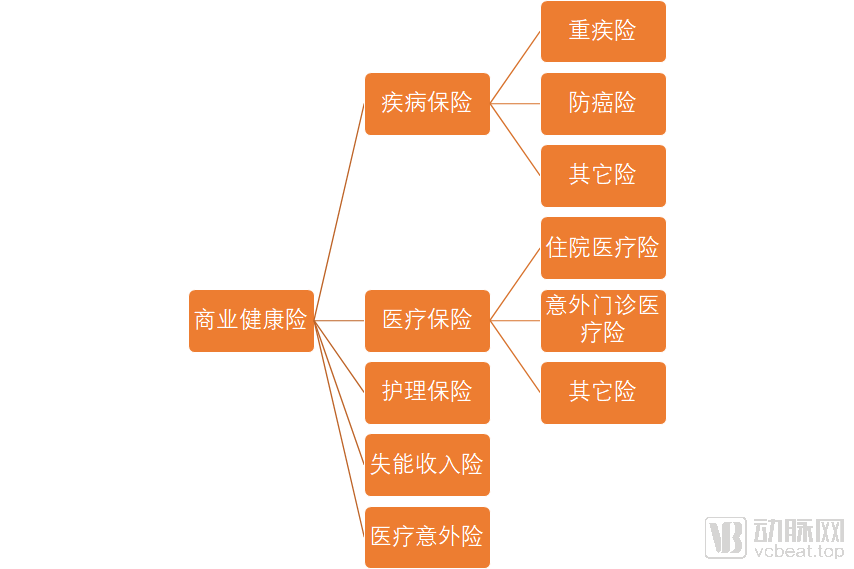

(Note: The secondary categories in the figure can be classified into different insurance products based on various criteria; for the purposes of this article’s narrative, they are categorized as shown above.)

Since the promulgation of the “New Health Insurance Regulations” at the end of 2019, commercial health insurance has been categorized into five major types, with medical accident insurance being the newly added category under the new regulations.

According to data disclosed by the China Banking and Insurance Regulatory Commission, disease insurance and medical insurance accounted for the vast majority of the RMB 706.6 billion in gross written premiums in 2019, while long-term care insurance and disability income insurance combined accounted for only 1% of the market share, with the share held by medical accident insurance, a new product category, being negligible.

Notably, critical illness insurance and million-yuan medical insurance each account for the vast majority of their respective categories within disease insurance and medical insurance.

Over the past five years, the compound annual growth rate (CAGR) of health insurance has been approximately 30%. According to statistics from the China Banking and Insurance Regulatory Commission (CBIRC), original premium income from health insurance business reached RMB 264.1 billion in the first quarter of this year, representing a year-on-year increase of 21.6%. Based on these figures, the health insurance market is projected to reach a scale of one trillion yuan this year.

In such a rapidly growing market, health insurance appears to have a rather distorted product structure, with critical illness insurance and million-yuan medical insurance nearly representing the entirety of China’s commercial health insurance sector.. The formation of this distorted structure is influenced by a variety of historical, social, and institutional factors, which will not be discussed in detail here. Instead, we should look to the future, examining the direction in which health insurance is evolving and the opportunities and challenges facing each specialized insurance segment.

Fifteen years ago, Tang Ziou, then a doctoral candidate in health economics at Fudan University, authored a thesis titled “Research on Shanghai’s Long-Term Care Insurance (LTCI),” which explored the potential for the development of long-term care insurance in China.

Fifteen years on, Tang Ziou, now Chief Health Economist at Haorensheng Technology, has finally witnessed the large-scale implementation of long-term care insurance in China, a vision he had envisioned many years ago.

On May 6, 2020, the National Healthcare Security Administration released the “Guiding Opinions on Expanding the Pilot Program of the Long-Term Care Insurance System (Draft for Comments),”The document proposes expanding the pilot cities for the long-term care insurance system from the original 15 to 29, and explicitly states that social forces should be introduced to participate in the administration of long-term care insurance services.From a regulatory perspective, this policy affirms the pilot experience accumulated over the previous four years and sets a developmental tone of integrating social insurance with commercial insurance for the long-term care insurance system.

Long-term care insurance refers to health insurance that provides compensation for nursing expenses incurred when the insured, due to aging, illness, or other causes, is in a state of physical or cognitive impairment and requires specialized care from social institutions or at home; whereas long-term care refers to the provision of a series of health care, personal care, and social service items over a sustained period to individuals who have lost their ability to perform activities of daily living or who have never possessed such abilities.

Currently, the population in China with nursing care needs (including those who are disabled or partially disabled) has exceeded 40 million. With the advent of population aging, this group is projected to grow to a scale of 100 million in the future. This may be a challenge that no other market around the world has ever faced.

According to Liu Zhichen, Chief Expert in the Healthcare Industry at China Unicom Group and a Senior Strategic Expert in the Big Health Sector, the policy logic behind the expansion of long-term care insurance pilots stems from the motivation to control medical insurance costs.

In the composition of medical insurance expenditures, inpatient medical costs account for the largest share. If these costs can be effectively managed through long-term care and health management, it will curb the rapid growth of medical insurance fund expenditures at the source, thereby achieving a surplus in the medical insurance fund.

Under our previous medical insurance reimbursement policies, health interventions and health management prior to the onset of disease were not covered. Reimbursement was only provided once hospitalization became necessary due to serious illness. The former reimbursement framework primarily focused on inpatient care, which significantly contributed to the excessive consumption of medical insurance funds. Liu Zhichen stated, “With the gradual establishment of a diversified financing and multi-tiered security system involving medical insurance funds, public health funds, and commercial health insurance, the future direction of reform will undoubtedly involve refined, lifecycle-based classified management centered around profiling key populations.”

“Positioning long-term care as a significant public welfare benefit is crucial.” Liu Zhichen observed that although Japan is a society with a high degree of aging, many elderly people living alone still receive quality care services, which is largely attributable to their relatively mature service system and long-term care insurance payment mechanism.

“At present, Chinese society needs to address a systemic issue: the coverage of long-term care costs under social insurance,” explained Liu Zhichen. He noted that China’s current social security framework, known as the “Five Insurances and One Housing Fund,” does not include a long-term care insurance system for the elderly. This means that medical expenses can only be covered by medical insurance when the elderly fall ill, while their daily living expenses are covered by pensions. However, if an elderly person is disabled or partially disabled and does not require prolonged hospitalization, the substantial costs of caregiving must be borne entirely out-of-pocket by the elderly individual and their family.

Although some pilot cities in China have launched trial operations of long-term care insurance, the issue of funding has yet to be adequately resolved.

“In the long run, long-term care insurance should actually be addressed through a mandatory insurance system. In other words, it should be incorporated into the statutory social security framework, for example, by implementing a ‘six insurances and one housing fund’ model that includes long-term care insurance. This would require everyone to pre-save for their elderly care insurance during their working years, with benefits utilized in old age. Only in this way can we fundamentally resolve the payment challenges associated with the large population in China that will require elderly care in the future.”

Liu Zhichen acknowledged that there are still some technical support issues. For instance, as the physical conditions of elderly individuals vary, the payment standards for long-term care insurance should be assessed and differentiated accordingly. Furthermore, since an individual’s health status changes over time, regular assessments are necessary to determine the appropriate payment standards for long-term care insurance.

“The state should establish unified assessment criteria for payment under long-term care insurance.” Liu Zhichen believes that China’s systematic design of its long-term care system requires significant improvement and strengthening in multiple areas, including fiscal mechanisms, insurance schemes, service workforce development, and quality assurance.

The long-term care market is so vast that promoting large-scale implementation at this juncture is essential. However, two key issues must be addressed in this process.

On one hand, how should the funding mechanism for long-term care insurance be determined? Specifically, should long-term care coverage be integrated into the existing social insurance system, or should alternative financing models, such as commercial insurance, be adopted? This constitutes one aspect of the issue. On the other hand, once beneficiaries require long-term care services, what should be the primary role of insurers—whether commercial or public medical insurance providers? Should their focus be primarily on financial reimbursement or on directly providing care services?

In Tang Ziou’s view, the expansion of long-term care insurance (LTCI) pilot programs has elicited more concern than joy. “For a long time, third-party nursing institutions have been underdeveloped in China. If they are established abruptly in a campaign-like manner, how can quality be assured? We actually face a severe shortage of resources on the supply side of long-term care,” said Tang Ziou.

During the initial pilot operations of long-term care insurance, companies such as Ping An and Taikang participated and accumulated valuable experience. According to Zhang Xiaoyao from the Pension Health Insurance Systems Department at Taikang, although some pilot models have achieved notable success, they still face the challenge of an unclear business model.

Zhang Xiaoyao cited several examples he had observed: taking a pilot city for long-term care insurance as an example, the local government settles payments with third-party companies on a per-capita basis. Although the population base is indeed large and the total funding appears substantial, it is actually very difficult to ensure that these funds are allocated appropriately to their intended purposes while maintaining profitability. Currently, even achieving break-even is challenging, with most operators running at a loss.

“At least in the early stages, there will be no profits; however, as the business model becomes clearer and the market more standardized, slight surpluses may eventually emerge,” said Zhang Xiaoyao. He added that with the expansion of pilot programs and increased regulatory attention, the long-term care market holds significant future opportunities.

Figure: Payment Status of Long-Term Care Insurance in the Initial 15 Pilot Cities, Compiled by VCBeat

Recently, the relevant regulatory authorities have revised the "Standard for the Use of Disease Definitions in Critical Illness Insurance" issued in 2007.

The main changes in this revision are as follows:First, optimize disease classification and establish a tiered system for critical illnesses; second, increase the number of covered conditions and moderately expand the scope of coverage; third, broaden the scope of disease definitions and refine their connotations. For consumers, the revised critical illness definitions further expand the scope of coverage, provide clearer and more reasonable claim conditions, adopt more objective and authoritative reference standards, and ensure more standardized and uniform descriptions.

As consumers, we can tangibly perceive the following changes. First, the scope of coverage has been further expanded. Based on the existing definitions of critical illnesses, three additional severe conditions have been included: severe chronic respiratory failure, severe Crohn’s disease, and severe ulcerative colitis. Meanwhile, scientific grading has been applied to three core critical illnesses—malignant tumors, acute myocardial infarction, and sequelae of stroke—with corresponding definitions added for three mild forms of these conditions, thereby broadening the scope of coverage. Second, the claim conditions have become more reasonable. In line with the latest medical practices, the claim requirements for certain definition items have been relaxed. For example, for “heart valve surgery,” the original requirement of “open-chest surgery” has been removed and replaced with “incision into the heart,” effectively enhancing consumer protection rights. Third, the referenced standards are more objective and authoritative. Quantifiable objective standards or widely recognized criteria are adopted as much as possible to minimize subjective judgment, making the determination of critical illnesses clearer and more transparent.

Of course, some previously covered critical illnesses have been excluded from coverage or had their payout ratios reduced. Among these is thyroid cancer, which has been frequently discussed; its payout ratio was adjusted from 100% before the revision to 20%. Meanwhile, two mild conditions—carcinoma in situ and borderline tumors—have been completely removed from the scope of critical illness insurance coverage.

(Comparison of Payouts for Selected Conditions Before and After the Revision of Critical Illness Insurance)

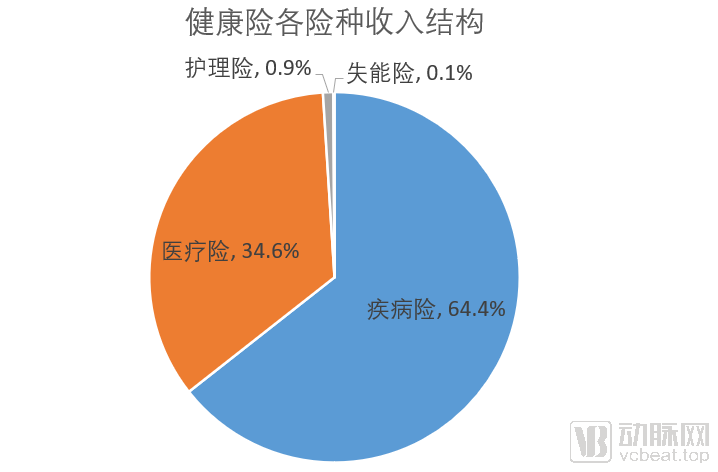

For a long time, critical illness insurance has been the largest component of health insurance. According to data released by the China Banking and Insurance Regulatory Commission (CBIRC), premium income from critical illness insurance reached RMB 410.7 billion in 2019, accounting for 58% of total health insurance premiums.

Why Does Critical Illness Insurance Account for the Majority of Health Insurance Volume? What Are the Existing Issues?

In Tang Ziou’s view, critical illness insurance is the least operationally challenging among the five major subcategories of health insurance. From product design and actuarial calculations to claims settlement, its operational complexity is relatively low. From a risk control perspective, coverage under critical illness insurance is binary—claims are paid if the insured event occurs, and not paid if it does not—reflecting an operating model similar to that of life insurance.

“Simple and crude.” Zhang Xiaoyao used these four words to answer this question, further citing the example of million-yuan medical insurance. “Million-yuan medical insurance is indeed simple and crude: it immediately sets a deductible of RMB 10,000–20,000, meaning that any hospitalization expenses within this range are not reimbursable. Regarding the so-called ‘million-yuan’ coverage, the actual reimbursement limit is based on the user’s hospitalization costs, rather than implying a flat payout of RMB 1 million upon diagnosis of a critical illness. Currently, million-yuan medical insurance products focus more on customer acquisition and are increasingly tied to public hospitals and basic medical insurance schemes. This design stems largely from a lack of refined management and cost-control capabilities.”

According to Jiang Guanjun, a partner at Mingde Actuarial Consulting Company, critical illness insurance faces issues such as limited product variety, homogenization of offerings, and insufficient operational capabilities. “The only link between critical illness insurance and the healthcare industry is the requirement for a diagnostic certificate; once the certificate is provided, the insurer simply pays out the predetermined benefit,” said Jiang. He noted that among the major subcategories of health insurance, medical insurance is poised for significant growth in the future.

In numerous policy documents in recent years, the phrase “insurance returning to its fundamental role of protection” has frequently appeared. Within the current protection landscape, medical insurance can bridge the coverage gap between basic social health insurance and critical illness insurance, representing a direction jointly anticipated and pursued by both the market and policymakers.

As the population ages, healthcare expenditures are rising, and the out-of-pocket portion of patients’ medical costs continues to increase, intensifying the financial burden of medical expenses. Currently, mainstream products in the health insurance market are predominantly critical illness insurance policies; however, most individuals do not reach the severity threshold required for critical illness coverage. Consequently, a protection gap exists between basic social medical insurance and critical illness insurance, highlighting the significant growth potential for medical expense insurance. In recent years, “Million-Yuan Medical Insurance” has precisely addressed this gap, gaining widespread market popularity due to this advantage. This trend underscores the genuine market demand for medical cost coverage.

However, given the current issues plaguing the industry, medical insurance remains a hard-to-crack market. Core medical data and national health insurance data are still held by relevant regulatory authorities and are subject to strict oversight. Without access to such data, it is difficult for medical insurance providers to conduct actuarial analysis and implement effective risk control measures.

Medical insurance encompasses three major categories of risk control technologies: health promotion (preventing the onset of chronic diseases), chronic disease management (preventing disease progression), and managed care (managing medical services). These three categories involve hundreds of risk points, making operational challenges immense. In Tang Ziou’s view, underwriting medical insurance is extremely difficult, and currently, virtually no commercial insurance company in China possesses sufficient risk control capabilities.

Insufficient capabilities naturally lead to increased risks. According to multiple industry insiders interviewed in this article, the vast majority of commercial insurance companies are operating at a loss in their medical insurance segments. Their primary motive for doing so is to secure market share and establish strong collaborative relationships with public health insurance programs. Once medical data is made accessible to commercial insurers in the future, they will be able to achieve profitability rapidly.

In the realm of medical data, Zhang Xiaoyao noted that previous attempts to support refined operational management by directly collecting data from hospitals and third-party platforms faced significant challenges in practical implementation. Beyond the high costs associated with establishing data connectivity channels, there was also the issue of inconsistent data standards across different hospitals and platforms. This necessitated substantial human resources for data organization, cleaning, and standardization, leading to a surge in costs. “The data retrieved at great expense failed to adequately support refined operations and management.”

For innovative health insurance companies, amidst the numerous industry pain points they face, the viable strategy is to build up strength, deepen their engagement in the sector, and pursue refined operations.

“Across every stage of the health insurance industry’s operations, ‘as long as you put down roots and implement sufficiently refined management, there will be considerable room for growth,’” said Jiang Guanjun.

In terms of product innovation, commercial health insurance has currently been sold to approximately 200 million healthy individuals. The remaining over one billion people have not yet purchased commercial insurance, with the majority being what the industry currently refers to as “substandard risks.” By developing differentiated products tailored to specific populations, and from an actuarial perspective, as long as premiums are aligned with their risk profiles, insurance companies can indeed underwrite such business.

In claims processing, the vast majority of insurers currently focus primarily on gathering sufficient information to assess how claim payments should be disbursed: What is the total amount of medical expenses? How much has been covered by basic medical insurance? And what is the payable amount under commercial health insurance? Once these figures are clearly reconciled, the process is essentially considered complete. However, with refined operational management, insurers could further analyze where the claim payments are allocated—whether to pharmaceuticals, diagnostic tests, or surgical procedures. They could also evaluate whether medical expense expenditures deviate significantly from industry averages and identify any potential instances of over-treatment.

In practice, however, we need to implement more granular management to determine exactly where each claim payment is allocated—whether to pharmaceuticals, surgical procedures, or diagnostic tests and laboratory examinations. We must also assess whether the medical expenditure patterns of a specific company or customer cohort differ significantly from overall medical spending trends. Therefore, we should conduct more refined data collection.

In terms of medical services bundled with health insurance, most providers currently merely replicate basic offerings such as appointment registration and medication guidance. But is it possible to truly integrate the medical ecosystem and launch services that better align with user needs?

Every node in the industry chain represents an opportunity.

However, given the current state of the industry, the primary direction for health insurance is integration with public medical insurance., which is the most obvious general direction for health insurance as defined by policy and market demand.

In upcoming articles, we will delve into how commercial health insurance integrates with public medical insurance, exploring the pain points, pathways, and future directions of this integration. Stay tuned.