The Dawn of Health Insurance 3.0: Integrating with Public医保 and Unlocking Data-Driven Growth

On June 18,“Major Shifts in Health Insurance: Expansion of Long-Term Care Insurance, Revision of Critical Illness Insurance, and a Potential Surge in Medical Insurance”In the previous article, we analyzed the trends in the three major categories of health insurance. In this article, we will primarily examine how health insurance can integrate with basic medical insurance, which is currently the most pressing need in the industry.

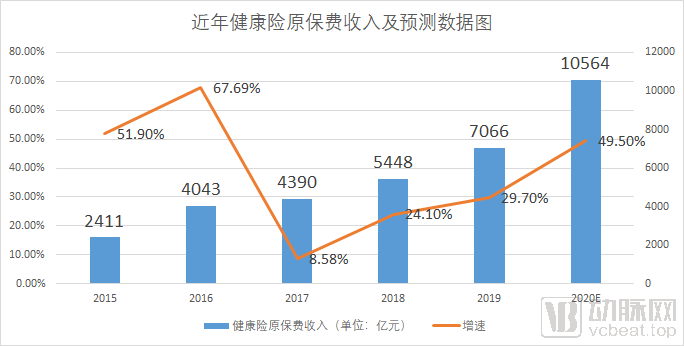

Over the past five years, the compound annual growth rate (CAGR) of health insurance premium income has exceeded 30%. In the first quarter of 2020, health insurance premium income reached RMB 264.1 billion, a year-on-year increase of 21.6%. Whether among specialized insurance categories or within specific segments of the healthcare sector, health insurance appears to be uniquely positioned.

At this point, it seems unnecessary to seek further reasons to explain the rapid growth and promising prospects of health insurance. To some extent, “health insurance is a vast blue ocean” has become an industry consensus.According to documents issued by the China Banking and Insurance Regulatory Commission (CBIRC) earlier this year, China’s health insurance market is projected to reach a scale of RMB 2 trillion by 2025.

At the current stage of the industry, the most critical issue worth attention is how to capture a share of the health insurance market. Through research and interviews, VCBeat has identified a clear and highly profitable direction for current industry development: integrating with basic medical insurance.If the industry’s focus has previously been disproportionately placed on insurance technology innovation and the development of health insurance TPA (Third-Party Administrator) services, then since the beginning of this year, based on the directions we have observed in policy and industry trends, the greater opportunity for health insurance lies in its integration with public medical insurance.

Beyond strategic direction, various industry developments have painted a clear picture: health insurance has entered the true 3.0 era, with the sector once again standing on the horizon.Numerous industry mirrors facing one another—established or newly emerged policies and concepts, along with the boundaries they are opening up; pressing pain points and bottlenecks awaiting resolution; data pending openness; and optimistic ecological visions of emerging trends—superimpose and reflect each other, creating a mirage-laden city of mirrors.

“The launch of million-yuan medical insurance represents a historic and landmark event for the insurance industry. Since the introduction of the first such product, ‘Zunxiang Yisheng,’ numerous insurers have flocked into this market. Measures such as increasing coverage limits, lowering premiums, reducing deductibles, and expanding services have significantly benefited consumers and reduced information asymmetry between agents and policyholders in the insurance market,” said Yu Dongwei, a senior partner at Mingya Insurance Brokers. He noted that with growing awareness of protection needs, health insurance has attracted increasing attention, while the development of the internet has accelerated the dissemination of insurance knowledge. “When introducing health insurance products to clients today, there is no longer a need to explain why they should purchase health insurance; instead, we directly recommend policies suited to their family’s needs and help them manage risks effectively.”

The million-yuan medical insurance was launched in 2016, a year when the premium income of health insurance reached 404.3 billion yuan, with a growth rate of 67.69%.Marked by the advent of million-yuan medical insurance, China’s health insurance industry has entered the 2.0 era.

Reviewing the development trajectory of China’s health insurance industry and drawing on multiple dimensions—including landmark events, market growth rates, technological iterations, and policy impacts—this article divides the industry’s evolution into three stages:

1.0 Era (1995–2015): The industry was in its exploratory and growth phases, experiencing organic growth driven by macroeconomic development.

During this phase, the industry remained in its nascent stage due to residents’ low awareness of insurance and limited income. In 1995, critical illness insurance was introduced in China, initially as a rider to life insurance policies, with limited disease coverage that typically included only seven major critical illnesses. In 1996, main insurance products providing lifetime coverage were launched. The comprehensive development of commercial health insurance began in 1998, when the state established a universal basic medical insurance system. The growing number of commercial insurance operators and the expansion of individual insurance agents both contributed to the growth of the health insurance sector.

2.0 Era (2016–2019): Marked by the launch of “Million-Yuan Medical Insurance,” the industry embarked on large-scale innovation in product design, distribution channels, technology, and market penetration. In 2016, health insurance premium income recorded a growth rate of 67.69%, and the sector maintained robust growth in the subsequent years.

(Figure: Health insurance revenue data in recent years and forecast data)

At this stage, internet property insurers such as ZhongAn Online and Taikang Online have been vigorously expanding their million-yuan medical insurance offerings, while a large number of small and medium-sized insurers have entered the health insurance market, intensifying competition. This has led to high homogenization of health insurance products across the industry, along with insufficient personalized, diversified, and customized product design.

In the 3.0 era, with the introduction of multiple landmark policies and a market size approaching one trillion yuan, health insurance will become infrastructure akin to “water, electricity, and gas.” In the future, a diversified protection system combining “basic medical insurance and commercial insurance” will cover the majority of the country’s population.

(The image shows the major policies intensively issued by regulators over the past six months.)

The policy logic behind the intensive rollout of these measures is to enhance the payment efficiency of the medical insurance fund and achieve both revenue expansion and cost containment in its overall operation. Established in 2018, the National Healthcare Security Administration (NHSA) is driving the deepening of healthcare reform in its capacity as a “super buyer,” yet its fundamental mission remains to ensure the stable operation of the medical insurance fund. Given that revenues for the medical insurance fund are relatively stable, developing commercial health insurance to jointly expand the scope of medical security has emerged as seemingly the most ideal path.

On March 5 this year, the top-level design was unveiled. In the policy document “Opinions on Deepening the Reform of the Medical Security System,” one sentence“Establish a multi-tiered medical security system with basic medical insurance as the mainstay, medical assistance as the safety net, and complementary development of supplementary medical insurance, commercial health insurance, charitable donations, and mutual medical aid.”...the expression, like endless sunlight shining on people's faces.

In its past development, the health insurance industry has also borne excessive expectations from capital, with a large influx of funds pouring into the sector.

(Figure: Selected investment and financing deals in 2020)

As we can see, the health insurance sector has reached later-stage financing rounds, with substantial funding amounts, and has already produced listed companies such as Huize Insurance.At some point in the future, a wave of health insurance IPOs may emerge.

However, from a more realistic industry perspective, the health insurance sector may once again find itself at a critical juncture. The industry currently faces pain points such as product homogenization, fragmented core data, and insufficient technological integration. As market demand continues to rise and the market scale experiences substantial growth, can the current health insurance industry truly capture this trillion-yuan market?

“In a sense, the health insurance industry is just getting started.” Ren Bin, founder of Baoxian Geke (Insurance Geek), said this in a previous interview with VCBeat.

Setting aside the numerous pain points and bottlenecks in the industry for now, current policies and market demands are steering health insurance toward integration with public medical insurance.

Recently, an intriguing development has emerged in the industry: the rollout of inclusive supplementary medical insurance programs across various regions. In many cities, including Chengdu and Zhuhai, local residents can now use funds from their personal basic medical insurance accounts to purchase these inclusive insurance plans.Basic medical insurance not only creates demand for supplementary coverage beyond its scope but also consciously promotes the widespread adoption of commercial health insurance.

The Huimin Insurance Project actually reveals the major trend of integrating public medical insurance with commercial health insurance.

The benefits of integrating and bundling commercial health insurance with public medical insurance are evident. On one hand, commercial insurers can leverage the infrastructure of public medical insurance for management purposes. During this process, access to public medical insurance data and the capability to process such data will directly empower commercial health insurance operations.; On the other hand, some commercial insurance companies already possess the corresponding technological capabilities to directly undertake projects related to basic medical insurance.

“Allowing the use of individual medical insurance accounts to purchase health insurance holds significant implications for the industry, and we hope the sector will seize this major opportunity,” said Dr. Tang Zi’ou, Chief Health Economist at Haorensheng Technology. He noted that using medical insurance accounts to buy commercial insurance effectively adds a leverage effect to medical coverage payouts.

Tang Ziou stated, “To put it plainly, the funds accumulated over a long period in one’s personal medical insurance account are insufficient to cover the costs of a single illness episode; therefore, purchasing health insurance provides individuals with substantial financial protection.”

However, according to Tang Ziou, there are three major pain points in the current integration of commercial health insurance with basic medical insurance:

The first is data. If there is a thorough integration of social insurance and commercial insurance, the matter would be relatively easy to handle; the concern lies in mere superficial linkage. Commercial insurance carries greater operational risks than social insurance. If commercial insurance is linked with social insurance but information asymmetry persists, it will lead to uncontrollable risks.

Second is the uniqueness of the system. In China, although the government leads medical insurance, its control over more than 80% of public hospitals is very weak, making it difficult to achieve refined management. If medical insurance cannot effectively regulate such a supply side of medical services, how can commercial insurance manage it?

Third is the adequacy of market development. Since this involves integration, it is essential to fully leverage the proactive nature of the market. If market development is insufficient, the underlying drive for technological innovation may also be lacking.

Jiang Guanjun, a partner at Mingde Actuarial Consulting, also highlighted a significant pain point in the industry. “I believe that, to a large extent, participants across the medical and pharmaceutical ecosystem may not fully understand how health insurance operates, while the health insurance sector, in turn, lacks sufficient understanding of healthcare. Currently, healthcare and health insurance remain two relatively independent ecosystems.” In Mr. Jiang’s view, both sides should now strive to develop a profound understanding of each other’s domains. This lack of mutual understanding is likely a fundamental reason why many stakeholders are currently more inclined to offer critical illness insurance rather than medical expense insurance, as the former entails lower management complexity.

Zhang Xiaoyao from the Health Insurance System Department of Taikang Pension has over a decade of experience in collaborating with medical insurance programs, and he shared some industry practice models. Currently, policy trends clearly indicate that commercial health insurance must serve as a robust supplement to public medical insurance. However, commercial health insurance remains significantly underdeveloped. Compared to state-run public medical insurance, it lags far behind in terms of coverage, scale, and policy support. “The disparity in magnitude is simply enormous.”

According to Zhang Xiaoyao, there are three entry points for integrating commercial health insurance with basic medical insurance.First, approaching from the perspective of medical insurance administration, many companies have already taken the lead. For instance, Ping An Medical Insurance Technology has made significant inroads in this field, while other insurers such as Taiping are also eager to enter. Taikang has already secured dozens of projects related to payment method reforms in various pooled insurance regions. The second entry point involves commercial insurance assuming coverage for long-term care insurance and critical illness insurance. The third entry point is designing and developing new types of commercial health insurance products, enhancing data processing capabilities and refined operational management, thereby truly serving as a beneficial supplement to the national basic medical insurance system.

In this context, Zhang Xiaoyao particularly emphasized that the third entry point coincides with the most significant pain points and challenges in commercial health insurance. Currently, commercial health insurance suffers from limited product diversity and severe homogenization. “In other words, if your company develops a new insurance product, it is quickly replicated by all competitors. Moreover, management practices remain extensive rather than refined, and underwriting and claims adjudication are overly arbitrary, failing to achieve precise management. Where does the problem lie? It stems from the unequal status between basic medical insurance and commercial health insurance.”

For instance, in the acquisition of medical data, commercial health insurance operates from a highly passive position. Since current commercial health insurance products are primarily targeted at individual policyholders, the data accessible to insurers is limited to what policyholders voluntarily provide. Such submissions often consist of unstructured formats like photocopies and photographs, leaving commercial health insurers without effective channels to obtain structured, clean, and high-quality data.

“Unable to access the actual data, we only obtain some images or copies. These data fail to achieve a high level of integrated and precise management in practice, relying solely on manual visual identification and entry, followed by case-by-case processing, which results in extremely low efficiency. Therefore, the biggest pain point in the current model of commercial health insurance is the channel for data acquisition.”

In Zhang Xiaoyao’s view, although the government has introduced numerous policies to support commercial health insurance, these measures have not fundamentally altered the dominant position of hospitals in medical practice, nor have they challenged the primary role of national basic medical insurance in payment. Hospitals currently determine their own clinical practices independently of commercial insurance, and post-treatment reimbursement through national medical insurance is also unrelated to commercial insurers. “Historically, commercial health insurance could only target a very small segment of high-end clients, partnering with premium hospitals to provide upscale medical services. While this niche market exists, it is too small. Moreover, the general public has not yet developed the habit of purchasing high-end medical insurance. Although the commercial health insurance market is improving, its coverage remains significantly limited compared to that of national basic medical insurance.”

From the current models adopted by major insurers such as Ping An and Taikang to integrate with basic medical insurance, it is evident that they have deep-seated strategic considerations. Whether engaging in government-administered medical insurance operations or participating in long-term care and critical illness insurance programs, their ultimate aim is to establish in-depth cooperation with the basic medical insurance system. This approach not only helps build strong relationships and enhance operational capabilities but also prepares them for further integration of commercial insurance with basic medical insurance, while granting access to valuable medical insurance data.

According to a senior industry insider, the vast majority of health insurance projects undertaken by major insurers are currently operating at a loss. For commercial insurance companies, the primary considerations are to gain familiarity with public health insurance data and to hone their capabilities in processing such data.

“Once the government releases policies allowing commercial insurance companies to leverage national health insurance data for product design, underwriting, and claims processing of commercial health insurance, it is believed that these insurers will promptly respond to national policies, upgrade and expand their existing commercial health insurance offerings, and achieve automated, refined, and personalized operations. This will enable the formation of new business models, allowing them to quickly recoup their initial investments in the national health insurance system through profits from commercial health insurance.”