MGI Tech's Major Funding Ignites the Domestic Gene Sequencer Market

Within just one month, Qitan Technology, MGI Tech, and Sena Biotech successively announced the completion of their financing rounds. Once again, domestically produced gene sequencers have become a hot topic in the healthcare sector.

For years, the sequencer industry has been monopolized by a few foreign giants. Although MGI Tech’s frequent moves in the past two years have sounded the charge for the counteroffensive of domestically produced sequencers, achieving full import substitution may still take some time, given its current market share. Beyond the fiercely competitive NGS market, third- and fourth-generation sequencing technologies have also drawn significant attention following Illumina’s acquisition of PacBio. Qitan Technology, which recently secured financing, is a pioneer in fourth-generation sequencing.

So, what exactly are first-, second-, third-, and fourth-generation sequencing technologies? How large is the global sequencer market? Which domestic companies are currently positioning themselves in the development of Chinese-made sequencers? And which instruments have received approval for clinical use? We will address these questions one by one in this article.

In the current field of gene sequencing, sequencing technologies are categorized into four generations based on their core sequencing principles. In reality, there is no inherent technical superiority or inferiority among these four generations; rather, they are primarily classified according to the chronological order of their emergence.

Sanger sequencing requires four separate reaction systems, each containing a different ddNTP (dideoxynucleoside triphosphate). Because ddNTPs lack the 3’-OH group necessary for chain elongation, DNA synthesis terminates whenever a ddNTP is incorporated. Consequently, the DNA strands synthesized in the four reactions terminate at positions corresponding to A, T, C, and G, respectively, generating fragments of varying lengths that are separated by gel electrophoresis. By comparing the electrophoretic results of the four samples, the sequence of the target DNA can be determined.

Sanger sequencing, due to its high accuracy, remains widely used and is considered the gold standard for gene sequencing. However, its low efficiency, low throughput, and difficulty in sequencing unknown sequences make it challenging to achieve large-scale applications at the genomic level.

NGS sequencing employs the sequencing-by-synthesis method. Initially, adapters are ligated to both ends of the DNA fragments to be sequenced, enabling their anchoring onto a flow cell. Subsequently, these DNA fragments undergo cyclic amplification to form DNA clusters within specific regions. During the sequencing process, four types of nucleotides, each labeled with a distinct fluorescent signal and equipped with a reversible terminator, are introduced into the reaction system. The reversible terminator ensures that only one nucleotide is incorporated per cycle. After incorporation, the instrument identifies the added nucleotide in each DNA cluster by detecting the fluorescent signal. The terminator is then cleaved, allowing the next cycle of synthesis to proceed.

Next-generation sequencing (NGS) has become the most widely used sequencing technology worldwide due to its high accuracy and high throughput. Companies such as Illumina and Thermo Fisher Scientific primarily offer NGS platforms.

However, the inherent difficulty of second-generation sequencing in handling long fragments, coupled with prolonged turnaround times due to extensive sample preparation, paved the way for the emergence of third- and fourth-generation sequencing technologies.

Third-generation sequencing primarily relies on fluorescence detection and also employs the sequencing-by-synthesis approach. Consequently, some argue that third-generation sequencing should not be classified as a distinct category.

Third-generation sequencing primarily employs physical nanopores or specialized materials to isolate the reading region of individual molecules. For instance, Pacific Biosciences’ technology anchors DNA polymerase at the base of a nanopore, ensuring that the nucleotides being analyzed remain positioned at the bottom of the nanopore, closest to the fluorescence detection site, thereby enabling long-read sequencing.

The benchmark enterprise for third-generation sequencing is the foreign company Pacific Biosciences. Illumina once attempted to acquire this company to expand into the long-read sector, but the deal was ultimately rejected by antitrust regulators in the United States and the United Kingdom. In China, Genetron Health (formerly Hanhai Gene) has also made strides in this field. The technology employed by Genetron Health originates from an overseas company called Helicos. Compared with Pacific Biosciences’ advantages in long-read sequencing, Genetron Health’s technology primarily focuses on short-read applications.

Fourth-generation sequencing technology is widely regarded as the next generation of sequencing technologies, with little controversy.

Fourth-generation sequencing technology utilizes protein-based nanopore channels. Under the influence of an applied voltage, unwound single-stranded DNA passes through the nanopore channel proteins at a controlled rate. As each nucleotide base traverses the nanopore, it induces distinct changes in electrical signals. By analyzing the magnitude and variation of the ionic current using complex algorithms based on recurrent neural networks (RNNs), the specific type of each base is identified, enabling real-time sequence determination.

Fourth-generation sequencing, owing to its unique technical characteristics, features highly compact instruments, with the smallest models being handheld. Furthermore, as it eliminates the need for extensive sample preparation, it is frequently employed in rapid detection applications. Accuracy and throughput have been key areas of focus for improvement in fourth-generation sequencing. Due to currently limited accuracy, its primary application remains in microbial detection.

Oxford Nanopore is the most renowned provider of fourth-generation sequencing technology globally. Its desktop and handheld devices have become the benchmark for fourth-generation sequencing.

Turning to domestically produced sequencers, there is currently virtually no enterprise making concentrated investments in first-generation sequencing. In contrast, for second-, third-, and fourth-generation sequencing, companies are actively exploring pathways for the domestic production of sequencers.

Domestic Sequencer Manufacturers

VCBeat has identified a total of 15 companies that are either offering sequencer products or have explicitly stated that they are engaged in sequencer R&D. This number is indeed relatively low for the rapidly evolving field of genetic testing.

Upon closer examination, the high technical barriers and the market structure, which is currently dominated by a few enterprises, make it difficult for startups to quickly enter the sequencer industry. However, from another perspective, this also means that the industry is rife with opportunities for companies with sufficient technological confidence. Therefore, we believe that the sector remains a blue ocean in China, and several recent large-scale financing rounds may spark a new wave of entrepreneurship.

To date, domestic companies entering the R&D and production of Chinese-made sequencers can be mainly divided into two categories: collaborative partnerships and independent in-house development.

Among these partners, the companies all entered the market through the niche segment of third-party clinical testing, seeking to establish instrumental platforms for their third-party medical testing services. Illumina is the largest partner, with four companies independently manufacturing Illumina sequencers through OEM (original equipment manufacturer) arrangements. Thermo Fisher previously collaborated with Daan Gene and CapitalBio to produce the DA8600 and BioelectronSeq 4000, respectively; however, neither product currently appears on the NMPA’s public registry of domestically produced medical devices.

Several companies with in-house R&D capabilities each have their own unique technological pathways.

Most companies established earlier have primarily developed next-generation sequencing (NGS) instruments, such as WinGenomics, Zongxin Technology, and OneChip Bio; moreover, the majority of these enterprises already have mature products being marketed.

As the leading player in China’s domestic sequencing instrument industry, MGI Tech has had six products approved for registration by the National Medical Products Administration (NMPA), two of which have already exceeded their validity periods. MGI Tech’s technology originated from Complete Genomics (CG) and has been further developed on the foundation of CG’s technological platform.

MGI Tech stated to VCBeat: “In addition to core technologies such as DNA Nanoballs (DNB) and Patterned Arrays, which offer advantages including high sequencing accuracy, low cost, and low duplicate read rates, MGI Tech has continuously developed new technologies such as CoolMPS and stLFR to further enhance read length and sequencing accuracy while reducing sequencing costs. Moreover, over 90% of the components in its instruments are now domestically produced in China, achieving true autonomy and control over core tools.”

GenoCare (formerly Hanhai Genomics) is an early-established company specializing in third-generation sequencing products. Its technology originates from Helicos BioScience in the United States. While this technology does enable single-molecule sequencing, its read length has remained limited to approximately 35 base pairs, failing to achieve the long-read capabilities offered by PacBio.

WanZhong YiXin stands out as somewhat distinct. By employing semiconductor-based sequencing technology, WanZhong YiXin focuses its products on the low-throughput sequencing market, aiming to expand the reach of sequencers with cost-effective and high-efficiency solutions. As Hu Wenchuang, founder of WanZhong YiXin, stated, “The key to maximizing the value of precision medicine lies in implementing gene sequencing at the grassroots and community levels.”

In the past two years, self-developed companies have gradually begun to move towards fourth-generation sequencing technology.

Qitan Technology is naturally a standout among them, with its products achieving a single-read accuracy of 85% and a throughput of 1 Gb, gradually approaching the data benchmarks set by the industry leader, Oxford Nanopore. Another startup, Jinshi Technology, is also strategically positioning itself in the development of fourth-generation sequencers.

An industry insider shared with us, “From a technical standpoint, it is overly challenging to use solid-state nanopores to enable single-stranded DNA translocation and achieve single-molecule sequencing via electrical signals; such high precision is difficult to realize at an industrial scale. Therefore, companies currently developing fourth-generation sequencers have opted for biological nanopores.”

Currently, apart from Illumina, Thermo Fisher Scientific is virtually the only company in the sequencer market capable of competing with Illumina on a global scale. Although companies such as Roche, MGI Tech, PacBio, and Oxford Nanopore are aggressively entering this sector, their current market shares remain relatively limited. Relevant market estimates indicate that Illumina and Thermo Fisher Scientific together control approximately 90% of the global sequencer market.

Sequencers are critical business units for companies, but they are essentially one-time purchases with limited market demand and low depreciation rates. Moreover, the gross margin on the equipment itself is relatively low, making it difficult to serve as a primary profit driver. Therefore, sequencing instrument manufacturers must rely more heavily on reagents and consumables compatible with their sequencers to achieve profitability.

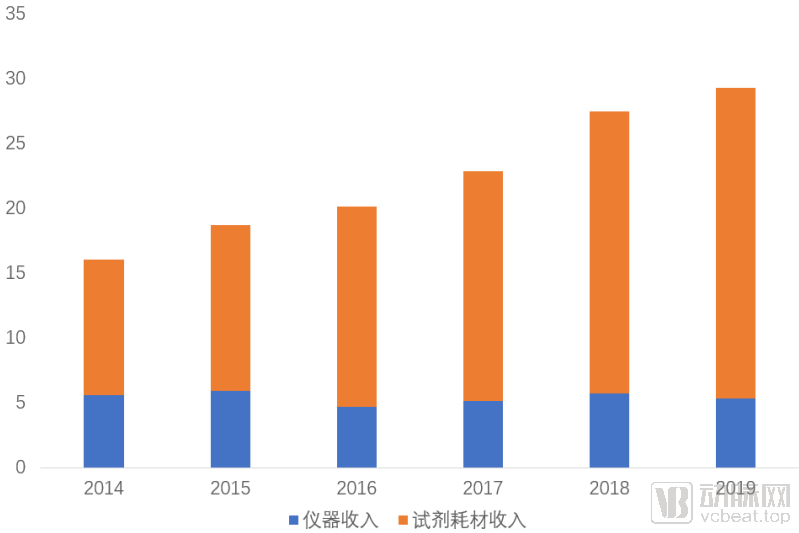

Illumina's Product Revenue Changes in Recent Years

Taking Illumina as an example, although it remains the world’s largest supplier of sequencing instruments, its instrument sales have long shown signs of weakness. Financial reports indicate that Illumina’s sequencing instrument sales reached $517 million in 2019, down from $535 million in 2018. Its share of total revenue also declined to 14.6% as other revenue streams grew.

In fact, over the past six years, Illumina’s instrument revenue has essentially stagnated, remaining at approximately $500 million. Meanwhile, revenue from reagents and consumables has continued to grow. The proportion of instrument revenue within its total product revenue declined from 35.1% in 2014 to 18.3% in 2019.

On the one hand, the market demand for sequencing instruments is long-term and sustained; on the other hand, the reagents and consumables used in sequencing must be the original manufacturer’s compatible products. Due to the inelastic demand generated by the use of sequencing instruments, enterprises and institutions have very weak bargaining power over supporting reagents and consumables. Therefore, Illumina’s monopoly in sequencing instruments means that it effectively controls the fluctuations of the entire NGS market.

Thermo Fisher only disclosed its sequencing-related revenue in 2017; therefore, estimating the current market size of sequencers based on 2017 data would be relatively more accurate.

In 2017, Illumina’s product revenue reached $2.289 billion. Thermo Fisher Scientific reported in its 2017 financial statements that its sequencing revenue for the year was “slightly below $418.36 million.” As one of the world’s largest providers of life science solutions, Thermo Fisher’s sequencing revenue is derived almost entirely from sales of its own instruments and reagents/consumables, with virtually no revenue coming from services.

Based on this, we can roughly estimate that Illumina and Thermo Fisher Scientific hold a 90% market share of sequencers and related reagents and consumables at a ratio of 5.5:1. Illumina accounts for approximately 76% of the market. Accordingly, the global market size for sequencers and related reagents and consumables in 2019 was estimated to be around $3.85 billion.

Currently, sequencers are mainly distributed among third-party medical testing institutions and research organizations, with a relatively low penetration rate in the hospital market. As the demand for sequencing continues to rise, more sequencers will be deployed within hospital settings. To enter hospital environments, sequencer products must obtain medical device registration certificates. So, which products currently qualify for clinical use?

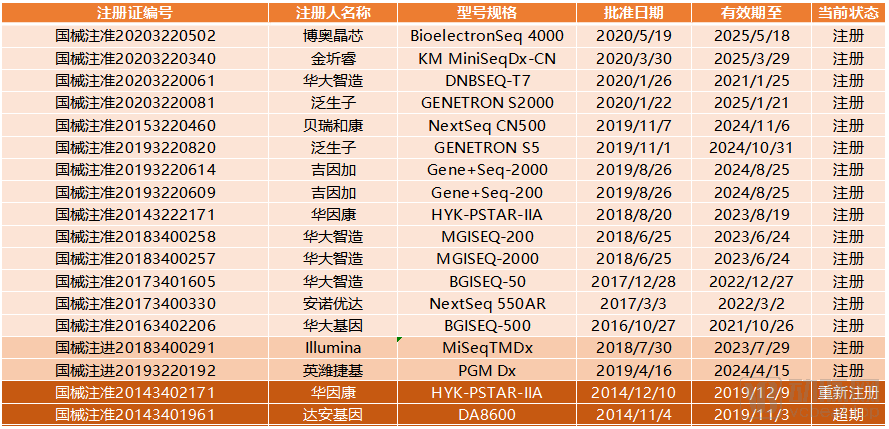

Registration Information for Sequencers Retrieved from the NMPA Website

The query page on the National Medical Products Administration (NMPA) website shows that there are currently 14 domestically produced gene sequencers registered. Among them, MGI Tech has the largest number of products, with a total of five models (including one product registered under BGI Genomics).

These 14 products are primarily sourced from eight different companies and fall into four distinct R&D categories.

The first category is, of course, fully independent research and development., such as Huayinkang's sequencers.

The technical core of Class II products originates from acquisitions., which is the approach adopted by MGI Tech. In March 2013, BGI Genomics acquired the U.S.-based Complete Genomics for $117.6 million and established MGI Tech based on its technology, initiating its strategic layout in sequencers through independent research and development.

The third category involves collaboration with overseas sequencer manufacturers., primarily responsible for contract manufacturing. Its main partners are naturally the two companies with the highest global market share: Berry Genomics and Annoroad Gene Technology have chosen to collaborate with Illumina, while Genetron Health has also partnered with Thermo Fisher Scientific. Although it appears that the product resulting from the collaboration between Illumina and Annoroad Gene Technology reached the market earlier, in terms of regulatory approval, Thermo Fisher Scientific had already collaborated with Da An Gene in 2014 to develop the DA8600 sequencer and successfully obtained a Class III medical device approval from the National Medical Products Administration (NMPA). However, the registration certificate for this product has now expired, and information about this instrument is no longer available on Da An Gene’s official website.

The fourth category of products involves collaboration with domestic sequencer manufacturers.For instance, Genetron Health’s GENETRON S2000 is a product co-manufactured with MGI Tech. The in-house production of clinical-grade sequencers has completed Genetron Health’s strategic layout in genetic testing instruments, includingAutomated Sample Loading System,Biochip Readeretc., enabling Genetron Health to provide users with comprehensive genetic testing services.

GenePlus has adopted a similar strategic layout. According to relevant reports, the core technology underlying GenePlus’s Gene+seq product series is DNBSEQ technology, one of MGI Tech’s core technologies. This product integrates GenePlus’s upstream and downstream deployments in sequencing, including automated library preparation systems, tumor gene detection kits, and all-in-one automated NGS analysis and interpretation systems for oncology, thereby enabling GenePlus to provide users with comprehensive end-to-end sequencing services.

In addition to these 14 registered domestically produced products, Da An Gene’s DA8600 has exceeded the validity period of its approval certificate but has not been resubmitted for registration.

Several major foreign sequencer manufacturers, in addition to collaborating with domestic companies on product development, are also attempting to sell directly to the Chinese market through imports. In July 2018, Illumina introduced its MiSeq Dx into China’s clinical market via an import-export company based in Shanghai. Thermo Fisher Scientific, meanwhile, registered its complete gene sequencing system in China through its subsidiary Invitrogen, which includes the Model 7469 gene sequencer.

Beckman Coulter, which provides Sanger sequencing (first-generation sequencing) solutions, has also entered the Chinese market with its products through similar approaches; however, the approved certification is for Class II medical devices.

Applications of gene sequencers are mainly found in research institutes and third-party testing laboratories, while their use in hospitals remains relatively limited.

For instance, a search for “sequencers” on the China Government Procurement Network reveals that the majority of tender notices for sequencing systems and instruments are issued by research institutes, with only sporadic procurement records from large hospitals.

Although next-generation sequencing (NGS) technology is relatively mature, its current clinical application remains primarily concentrated in two major areas: non-invasive prenatal testing (NIPT) and tumor genetic testing. NIPT relies on sequencing technology to distinguish between maternal and fetal DNA fragments, while tumor genetic testing requires the detection of changes as small as single nucleotide variants. Therefore, these two application scenarios have an essential demand for accurate gene sequences, which cannot be replaced by other testing methods.

It has been suggested that the COVID-19 pandemic has prompted many hospitals to recognize the application of gene sequencing in pathogen infection. However, taking COVID-19 as an example, VCBeat conducted a classification and statistical analysis of SARS-CoV-2 nucleic acid detection kits in March 2020. Among the 116 kits included in our statistics, 111 employed PCR-based detection methods, such as fluorescent PCR, isothermal amplification, and digital PCR. Only two products utilized sequencing methods, and these were primarily intended to assist researchers in sequencing the genome of the novel coronavirus.

Detection of pathogenic microorganisms, particularly in large-scale screening, primarily requires binary “yes or no” determinations rather than precise identification of every base pair in the DNA sequence. PCR technology is already sufficient for this purpose, making the application of next-generation sequencing (NGS) in such contexts somewhat excessive.

Of course, gene sequencing is not entirely unsuitable for pathogen detection. For certain pathogens that are difficult to identify and have a low clinical incidence, gene sequencing can identify rare pathogens more quickly than traditional culture methods, enabling timely and precise diagnosis for patients with severe infections. However, this does not constitute a rationale for hospitals to establish their own gene sequencing capabilities. The frequency of such cases in any single hospital is relatively low, making this testing demand more suitable for third-party clinical laboratories. We are already seeing companies such as Jinshi Genomics and Jieyi Biotechnology positioning themselves in this field.

Therefore, domestic sequencers have a better chance of entering the market by first gaining traction in third-party medical testing or scientific research.

Currently, many gene sequencing devices in China are housed in third-party medical testing laboratories, particularly in specialized testing (“specialty test”) laboratories that focus on providing genetic testing services. As indicated by the data we previously compiled, many of these companies have begun manufacturing their own gene sequencing equipment through acquisitions, partnerships, and other means.

Strategic deployment in genetic testing equipment not only ensures a company’s own sequencing capabilities but also significantly enhances the comprehensiveness of its end-to-end solutions. Taking Genetron Health as an example, after obtaining regulatory approval for its sequencers, the company provides an entirely self-manufactured product portfolio when collaborating with hospitals to establish joint laboratories.

In addition to specialized testing institutions, companies such as KingMed Diagnostics are also actively expanding into the field of gene sequencers. In fact, KingMed Diagnostics has accumulated substantial resources in genetic testing and established several partnerships. For instance, in January 2018, KingMed Diagnostics collaborated with Illumina to develop detection systems for tumors and genetic diseases. Its former wholly-owned subsidiary, JinQirui, also partnered with Illumina to develop the MiniSeq Dx, which received approval from the National Medical Products Administration (NMPA) for market launch.

Research institutes represent another major market for gene sequencers in China. In the field of biology, demand for gene sequencing is widespread and highly complex. Due to the diversity of these needs, many research institutes opt not to purchase their own gene sequencing equipment but instead outsource sequencing services. This trend has given rise to a number of gene sequencing companies specializing in life science research, such as Novogene.

Third-party medical testing laboratories and hospitals impose stricter requirements on equipment. In addition to the mandatory use of NMPA-approved products, brand reputation also exerts a significant influence.

However, the requirements in scientific research are relatively more flexible. Although brand effect does have a certain impact on the research field, researchers are often willing to try new things. As long as the products can provide accurate data, researchers generally maintain a positive attitude toward domestic brands. Therefore, for domestic sequencer brands, starting with the scientific research sector is naturally the optimal choice.

Collaborating with peripheral industries related to sequencing companies can achieve unique promotional effects. For instance, MGI Tech chose to cooperate with Geneseeq and GenePlus, selling its products through an OEM model. This strategy essentially represents an attempt to broaden its sales channels by leveraging tumor NGS companies.

Beyond tumor NGS, sequencing technologies have numerous other application scenarios, such as pathogen detection and single-cell sequencing. These applications are all seeking more cost-effective sequencing solutions, where the price advantage of domestic sequencing systems can be fully realized.

For example, the single-cell sequencing market is essentially monopolized by 10X Genomics. Nevertheless, many Chinese companies are actively positioning themselves in this sector to explore pathways for import substitution. In this regard, collaboration between domestically produced sequencers and Chinese enterprises specializing in single-cell library preparation would enable full localization of the single-cell sequencing workflow, which would undoubtedly have a positive impact on expanding the domestic market.

Although many companies in the single-cell sequencing industry currently develop their solutions based on Illumina’s platforms, Lin Wei, founder of Yinwan Cell, told VCBeat that switching platforms would not be difficult for them: “If we need to change platforms, we only need to replace the primers and adapters used during library preparation. This poses no problem for us at all.”