China's Medical Device R&D Outsourcing Market Surges: Core Services Shift from Clinical Trials to Integrated Development and Manufacturing

On August 1, 2019, the National Medical Products Administration (NMPA) issued the "Notice on Expanding the Pilot Program of the Medical Device Registrant System," extending the pilot program to 21 provinces and decoupling medical device registration from production. The implementation of the Medical Device Registrant System pilot will expand the scope of contract research organizations (CROs) in the medical device sector, extending their services from clinical trials and registration to include research and development (R&D) and manufacturing, thereby further broadening their business scope.

Medical device R&D outsourcing services have, through initial development, become a key strategic option for medical device developers to reduce upfront investment, accelerate regulatory submission processes, and mitigate product launch risks. In 2019, the market size of China’s medical device R&D outsourcing industry reached RMB 10 billion, with an expected compound annual growth rate exceeding 20% in the coming years, indicating that this sector remains a vast blue ocean.

So, where are the major opportunities in China’s medical device R&D outsourcing industry? What is its business model? What is the current state of corporate management and operations? What challenges exist in business development? And what are the future trends?

To address the aforementioned questions, VCBeat Research conducted surveys of over 30 companies engaged in medical device R&D outsourcing services, interviewed industry experts, and compiled and analyzed the resulting data to produce the “Innovation Report on the Medical Device R&D Outsourcing Services Industry.” This report aims to comprehensively analyze the industry from multiple dimensions, including policy, market, and operations, and provides in-depth profiles of companies such as Medisino, Juyi Technology, Zhizhong Technology, Huitong Medical, Xiangkang Technology, and Ruiyi Kesheng, with the intention of offering industry participants relatively comprehensive industry insights.

Core Viewpoints:

1. Clinical trials are the core service of medical device CROs, while medical device CDMOs primarily focus on small-scale pilot production and post-market manufacturing

2. Pilot programs for the Medical Device Registrant System were launched in 21 provinces (autonomous regions or municipalities directly under the Central Government), creating a policy window period for the industry

3. The industry’s market size has reached RMB 10 billion, with a projected compound annual growth rate (CAGR) of over 20% in the coming years.

4. Orthopedic implants and in vitro diagnostics (IVD) are key focus areas for medical device R&D outsourcing services, while “high-end and intelligent” solutions—represented by emerging fields such as artificial intelligence, surgical robots, and medical 3D printing—represent the future direction of these services.

5. R&D outsourcing service providers for medical devices will be a key focus for investment institutions and the medical device industry

6. Referrals from existing clients and online marketing are the primary customer acquisition channels for medical device R&D outsourcing service providers, with 55% of clients originating from these sources.

Outsourced R&D services for medical devices encompass five stages: preclinical research, small-scale pilot production, clinical trials, regulatory submission, and post-market production. Targeted services are provided for each stage, primarily including market research, risk management, product finalization, facility design and construction, process optimization, clinical trial protocol design, preparation of submission dossiers, and large-scale contract manufacturing. Companies providing outsourced R&D services for medical devices fall into two categories: medical device CROs (Contract Research Organizations) and medical device CDMOs (Contract Development and Manufacturing Organizations).

Medical Device CROs (Contract Research Organizations) are enterprises that primarily provide clinical research services for product development to medical device developers through contractual agreements. Clinical trials constitute the core service of medical device CROs, aiming to help medical device developers accelerate the clinical trial process and expedite entry into the regulatory submission phase.

Medical Device CDMO (Contract Development and Manufacturing Organization) refers to enterprises that primarily provide process research and development, design, and manufacturing services to medical device developers through contractual agreements, with a focus on small-scale pilot production and post-market commercial manufacturing. It aims to help medical device developers enhance quality control, shorten pilot production cycles, reduce production costs, and improve production efficiency.

Figure 1. Main Service Contents of Each Stage in the Outsourcing of Medical Device R&D

Image source: VCBeat.

The service offerings of medical device CROs and medical device CDMOs are closely interconnected and mutually supportive, yet distinct differences exist between the two. The former focuses on enhancing R&D capabilities and represents a technology-intensive outsourcing model; the latter features higher entry barriers, where advanced process expertise and substantial asset scale are prerequisites for capturing market share, constituting an outsourcing model that is both technology-intensive and capital-intensive.

Policy is a critical factor influencing industry development. The launch of the pilot policy for the Marketing Authorization Holder (MAH) system for medical devices has invigorated the medical device R&D outsourcing services sector. Medical device R&D entities can outsource laboratory research, small-scale trial production, large-scale manufacturing, and quality control to professional R&D outsourcing service providers. This shift creates substantial new growth in the medical device R&D outsourcing market, attracts more companies to enter the field, and accelerates industry development.。

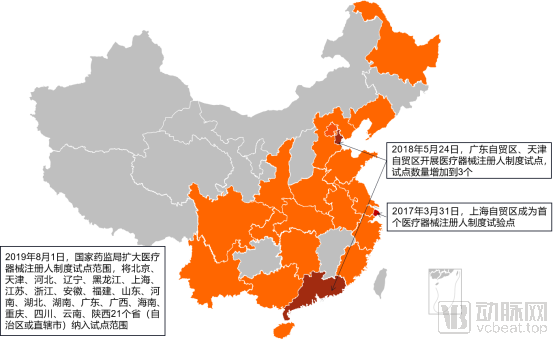

Figure 2. Pathway for the Expansion of the Pilot Scope of the Medical Device Registrant System

Image source: VCBeat

On August 1, 2019, the National Medical Products Administration (NMPA) issued the "Notice of the NMPA on Expanding the Pilot Program for the Medical Device Registrant System," encouraging 21 provinces (autonomous regions or municipalities directly under the Central Government), including Beijing, Tianjin, and Hebei, to carry out pilot programs for the medical device registrant system. Subsequently, all 21 pilot provinces (autonomous regions or municipalities) successively introduced supporting policies, marking the expansion phase of the pilot program for the medical device registrant system.It is expected that the remaining provinces will also introduce pilot policies for the Medical Device Registrant System before the end of this year, at which point the pilot program will be implemented nationwide. This will invigorate the entire domestic medical device R&D outsourcing services market and create development opportunities for relevant enterprises.。

As evidenced by the pilot expansion trajectory, the Marketing Authorization Holder (MAH) system for medical devices was initially piloted in the free trade zones of Shanghai, Guangdong, and Tianjin. Leveraging national policy support and the concentration of industrial resources such as technology, talent, and capital, these regions enabled rapid results from pilots on outsourced medical device R&D services. This facilitated the accumulation of experience for replication in other provinces, thereby accelerating the development of the outsourced medical device R&D services industry.

However, judging from the current scope of the pilot program for the Marketing Authorization Holder (MAH) system for medical devices, it is mainly concentrated in the eastern coastal provinces and those central and western provinces with relatively strong economic development. Pilot work has not yet been launched in economically less developed provinces such as Guizhou, Jiangxi, Gansu, Qinghai, and Tibet.

Figure 3 Main Contents of the Pilot Policy for the Medical Device Registrant System

Image source: VCBeat infographic

An analysis of the pilot policies for the Medical Device Registrant System across 21 provinces reveals five key areas with significant impact on the medical device R&D outsourcing industry: quality management, cross-regional contracted manufacturing, information management, registrant eligibility criteria, and industrialization of medical devices.

(1) The pilot programs in all 21 provinces explicitly encourage third-party institutions to assess the operational status and effectiveness of the quality management systems (QMS) of registrants and trustees. As the establishment of QMS is one of the core services provided by medical device R&D outsourcing enterprises, the engagement of third-party institutions by registrants and clients for quality management purposes creates new business growth opportunities for these outsourcing firms.

(2)Cross-regional contract manufacturing can further stimulate the cross-regional flow of medical device production factors. Provinces including Shanghai, Jiangsu, Zhejiang, Anhui, Hunan, Heilongjiang, Sichuan, Yunnan, Shaanxi, Hubei, Liaoning, Chongqing, and Hainan all permit registrants to engage in cross-provincial contract manufacturing. This means that CDMO services are no longer confined to their home provinces but can expand their service scope to cover 21 pilot provinces, providing sample production and scaled-up post-market manufacturing.

(3)Information management enables end-to-end traceability and monitoring throughout the entire product lifecycle. By leveraging their strengths in information management across R&D processes, manufacturing workflows, and product quality control, medical device R&D outsourcing service providers can deliver efficient product management services to their clients.

(4)Natural persons, such as scientific researchers, may also serve as medical device registrants. Medical device R&D outsourcing service providers can develop consumer-facing (C-end) customer resources, thereby creating new sources of incremental market growth.

(5)Shanghai, Jiangsu, Zhejiang, and Anhui jointly issued the “Interim Measures for Cross-Regional Supervision of the Medical Device Registrant System in the Yangtze River Delta Region,” exploring new mechanisms for cross-provincial industrial transfer, differentiation and restructuring, innovation agglomeration, and information-based regulation. This initiative aims to promote extensive cross-provincial collaboration across innovation and industrial chains, fostering specialized and large-scale medical device industry clusters. To this end, leading contract research organizations (CROs) in the medical device sector can integrate industrial chain resources to enhance their comprehensive service capabilities, expanding their client base from individual enterprises to entire medical device industry clusters and providing them with integrated R&D outsourcing services.。

It is evident that the pilot policies for the Medical Device Registrant System, issued at both national and local levels, have unleashed substantial market demand for medical device R&D outsourcing services. Relevant enterprises should seize this opportunity to refine their R&D outsourcing service systems, optimize service offerings, expand their market footprint, and capture a larger market share.

According to market research, there are approximately 200,000 medical device R&D companies in China. With an estimated penetration rate of 1/10 for outsourced medical device R&D services and an average customer unit price of RMB 500,000, the market size amounts to RMB 10 billion.。

With the pilot implementation of the Medical Device Registrant System, new entities such as hospitals and universities have emerged in the downstream market of the medical device R&D outsourcing industry. Following the issuance of the pilot policy for the Medical Device Registrant System, scientific research institutions, universities, hospitals, and researchers are permitted to develop products and arrange for their post-market production through contractual manufacturing arrangements. Consequently, the downstream market of the medical device R&D outsourcing industry has added 34,354 hospitals, 272 medical universities, and other institutions.

Following pilot programs in 21 provinces and municipalities, research institutions, universities, medical facilities, and scientific researchers within these regions are gradually emerging as new clients for medical device R&D outsourcing service providers. The growing demand from numerous downstream entities for services such as R&D and clinical trials is poised to drive a new round of industry growth. For instance, Osida, established in 2004, took the lead in 2018 by launching CDMO platforms in Shanghai and Shenzhen. It has built approximately 20,000 square meters of cleanroom facilities, featuring more than 20 compliant production lines covering active devices, passive devices, and IVD products, along with over 10 independent inspection, testing centers, and laboratories, and more than 200 high-end imported inspection, testing, and production equipment units. Meanwhile, Osida shares hardware resources, professional talent, cloud-based management software, and specialized supply chains, becoming the first third-party service platform in China to help clients obtain registration certificates under the “Medical Device Registrant System.”

Foreign medical device developers are also key clients of medical device R&D outsourcing service providers. In 2019, the National Medical Products Administration (NMPA) accepted 5,593 applications for the registration of imported medical devices, representing a 32% increase compared with 2018. According to Chinese regulations, applicants for the registration of imported medical devices must be either representative offices established in China by overseas manufacturers or domestic legal entities designated by such overseas manufacturers. The registration requirements for imported medical devices have facilitated the growth of the medical device R&D outsourcing industry, accelerated the entry of foreign medical devices into the domestic market, and further expanded the market size.

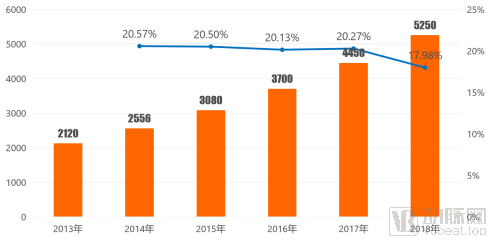

Outsourced R&D services for medical devices rely on the development of the medical device industry.In 2018, the market size of China's medical device industry reached RMB 525 billion, with a compound annual growth rate (CAGR) of 20% from 2013 to 2018. The market size is projected to exceed RMB 1 trillion by 2023. Among these, medical devices such as orthopedic implants, cardiovascular implants, and in vitro diagnostics are expected to grow at rates above the average level.

Figure 4 Market Size of China's Medical Device Industry, 2013–2018 (RMB 100 million)

Data source: Qianzhan Industry Research Institute; graphic by VCBeat.

Driven by factors such as population aging, centralized procurement, and import substitution, the orthopedic implant market is projected to achieve an annual growth rate exceeding 16% in the coming years. The development of the orthopedic market will attract more medical device companies to enter the field, thereby driving the growth of the contract research and development (CRO) services market for medical devices in this sector.

High-end medical device sectors, including cardiovascular implants, CT, MRI, color Doppler ultrasound, and endoscopy, are benefiting from policy support and gradually gaining momentum in the “import substitution” campaign. Their future market growth rate is expected to surpass that of other medical device segments. Given the higher value and pricing of high-end medical devices, companies operating in this field can more effectively enhance their core competitiveness.

The in vitro diagnostics (IVD) market is projected to achieve a compound annual growth rate (CAGR) of 18%. Among the segmented sectors, immunoassay, molecular diagnostics, and clinical chemistry hold the largest market shares, accounting for 38%, 20%, and 19% of the total IVD market, respectively.Currently, medical device R&D outsourcing services are predominantly offered in the field of in vitro diagnostics (IVD). It is advisable to extend the service chain to encompass stages such as research and development design and contract manufacturing.

Therefore, as the medical device market is projected to grow at a high compound annual growth rate (CAGR) of 20%, driven by the pilot policy for the Marketing Authorization Holder (MAH) system and by technological and business model innovations among medical device R&D outsourcing service providers, the penetration rate and growth pace of the R&D outsourcing services market will continue to rise, with its future CAGR expected to exceed 20%.

The medical device R&D outsourcing services industry has broad prospects, but there are also some pain points at present.

First, there is a shortage of specialized talent.The medical device R&D outsourcing services industry demands high-caliber professionals with multidisciplinary expertise in law, medicine, economics, and management. Professionals involved in R&D services and clinical trial services must possess in-depth knowledge across multiple sectors, including pharmaceuticals, machinery, electronics, plastics, and software.

The medical device R&D outsourcing service industry is a high-tech sector characterized by multidisciplinary integration and knowledge intensity. However, recent university graduates often fail to meet corporate requirements, necessitating long-term development through vocational training and practical education. Existing interdisciplinary professionals in the market possess strong competitiveness, forcing medical device R&D outsourcing firms to compete with investment institutions, medical device manufacturers, and pharmaceutical companies for this talent. Furthermore, the growing number of enterprises has significantly increased demand for relevant professionals, exacerbating the talent shortage within the industry. Consequently, the scarcity of specialized professionals constitutes a core bottleneck hindering the development of the medical device R&D outsourcing service industry. Some companies are addressing this challenge by innovating their talent development mechanisms; for instance, MedisCreation has established comprehensive talent cultivation and incentive systems to actively nurture relevant professionals, thereby building a talent reserve for future growth.

Next is the complexity of medical devices.The medical device industry encompasses a wide variety of products and involves highly complex technologies. Contract research organizations (CROs) specializing in medical device R&D must possess multidisciplinary talent pools, invest in diverse R&D equipment, and maintain the capability to develop various types of medical devices, such as cardiovascular interventional devices, in vitro diagnostic (IVD) products, and orthopedic medical devices. Each category of medical devices has unique technical requirements, necessitating that CROs master the corresponding technologies. Yongming Medicine focuses on the field of cardiovascular and cerebrovascular interventions, having established a comprehensive service system covering R&D, clinical trials, and regulatory submission for cardiovascular and cerebrovascular interventional devices, thereby providing customized outsourcing services to relevant R&D entities.

Finally, the limitations of the system.Contract manufacturing services are currently immature and require improved regulatory policies. The Medical Device Registrant System stipulates that the registrant (the entrusting party) must transfer relevant technical documentation to the contract manufacturer (the entrusted party). However, collaboration between the two parties is still influenced by factors such as commercial trust and intellectual property protection. To date, most entrusting and entrusted parties are affiliated companies. For example, Shenzhen Medprin, as a wholly-owned subsidiary, has commissioned Guangzhou Medprin to manufacture cranio-maxillofacial repair systems, and MicroPort EP has commissioned its wholly-owned subsidiary, Yuanxin Medical, to produce single-channel electrocardiogram recorders. The refinement of this system requires time to mature. The full implementation of the Medical Device Registrant System will depend on continued policy advancement, strengthened regulation, and enhanced mutual trust in commercial collaborations.

Figure 5 Pain Points Facing the Medical Device R&D Outsourcing Service Industry

Image source: VCBeat.

Medical device R&D outsourcing service providers can leverage their professional expertise to help R&D teams reduce upfront investment, lower manufacturing costs, and shorten time-to-market, thereby demonstrating strong market competitiveness.

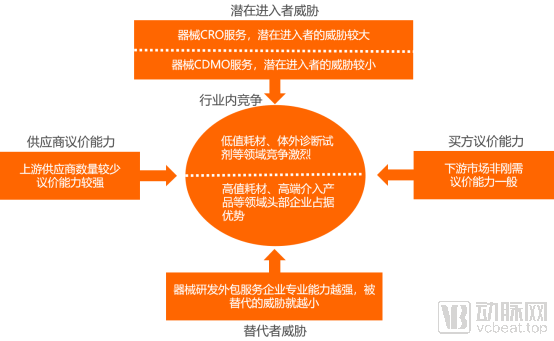

Upstream suppliers of outsourced medical device R&D services possess strong bargaining power. The upstream sector comprises healthcare institutions that provide clinical data for medical devices and regulatory testing agencies responsible for medical device registration. As of June 4, 2020, there were 883 clinical trial institutions for medical devices, while the number of regulatory testing agencies was approximately 30, predominantly government-affiliated, with few third-party testing organizations. Since most medical devices must undergo clinical trials and regulatory testing before market launch—a rigid requirement—and given the large number of new medical devices introduced annually, competition among clinical trial institutions and regulatory testing agencies remains limited, thereby strengthening their bargaining power.

The bargaining power of the downstream market for medical device R&D outsourcing services is moderate. The downstream sector comprises entities engaged in medical device research and development, which leverage the support of R&D outsourcing service providers to reduce upfront investments, mitigate R&D risks, enhance R&D efficiency, and minimize capital expenditure on manufacturing facilities. Consequently, the majority of medical device R&D entities require outsourcing services as a strategic supplement.

The threat of substitutes for medical device R&D outsourcing services is relatively low. The medical device R&D outsourcing industry is both talent-intensive and technology-intensive. In particular, large-scale medical device R&D outsourcing firms, leveraging their strong professional capabilities, face a low risk of being replaced.

The threat from potential new entrants in the medical device CRO sector is significant, whereas the threat in the medical device CDMO sector is relatively low. The medical device CRO industry is highly talent-dependent; thus, new entrants with a talent advantage can pose a substantial threat to incumbent firms. In contrast, the medical device CDMO industry requires not only talent but also significant investments in capital, laboratory equipment, and production facilities. These additional resource requirements raise entry barriers, thereby reducing the threat from potential new entrants.

The competitive landscape of the medical device R&D outsourcing industry is complex. In sectors such as low-value consumables and in vitro diagnostic (IVD) reagents, low entry barriers have led to a large number of service providers, resulting in intense competition. Conversely, high-value consumables, cardiovascular implants, and orthopedic implants present high entry barriers, with few companies capable of meeting the stringent requirements; in these fields, leading enterprises hold significant advantages.

The stronger the professional capabilities of medical device R&D outsourcing service providers, the lower their risk of being replaced, the greater their bargaining power, and the fewer their competitors.

Figure 6 Analysis of Competitiveness in the Medical Device R&D Outsourcing Service Industry

Image source: VCBeat.

VCBeat Institute, leveraging the VCBeat Orange Database and interviews with enterprises, has compiled a list of representative companies in the medical device R&D outsourcing services industry. Furthermore, by integrating relevant data, it has analyzed the industry’s management and operations across multiple dimensions, including service offerings, inception timeline, key resource investments, geographic coverage, and therapeutic areas served.

Table 1 Basic Information on Medical Device R&D Outsourcing Service Providers

Note: The above list features representative companies in the medical device R&D outsourcing services industry. It is not exhaustive, and the companies are listed in no particular order.

Data Source: Artery Orange Database

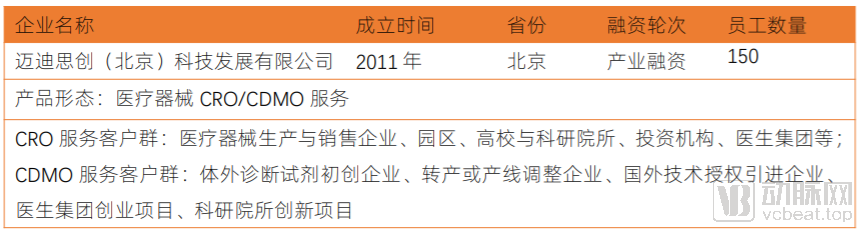

MediThink

InstrumentsCRO/CDMO Integrated Service PlatformMedicrea,Headquartered in Beijing, with branches and offices in Shanghai, Tianjin, Guangzhou, Chengdu, Wuhan, Shenyang, Zhengzhou, Wuxi, and other cities, it provides global customers with one-stop localized services for Chinese medical device registration and filing. MedisinoClinical trials have been conducted at more than 160 hospitals, with strong collaborative partnerships established with research institutions. A nationwide on-site clinical trial service network has been set up across 25 cities in China. The company has provided professional, high-quality, and efficient services to hundreds of medical device manufacturers worldwide, securing over 1,500 registration certificates for both imported and China-produced medical devices, and conducting more than 150 clinical research projects.

Juyi Technology

Giant Yi TechnologyHeadquartered in Shanghai, it is dedicated to providing contract research and development, clinical trials, regulatory registration, and contract manufacturing services to small and medium-sized medical device enterprises, universities, and clinical healthcare institutions worldwide.Scope of Services: Encompassing device innovation concept and technical research, product development, supply chain management, and contract manufacturing.、The entire process of clinical development, regulatory registration, and market launch. Juyi Technology accelerates domestic import substitution through flexible and efficient collaboration models, modularizes its technology platforms, and matches different products with the most suitable platforms based on their specific requirements.

Zhizhong Technology

Zhizhong TechnologyEstablished in 2011 at the Wuhan Optics Valley Bio-City, the company is committed to building a team grounded in “technical talent.” It specializes in professional services for the technological translation of medical devices. To date, the team comprises over 130 members, including more than 30 individuals holding master’s degrees or higher.ZhiZhong TechnologyBacked by Tsinghua TusVentures and Matrix Partners China, and supported by the Ministry of Science and TechnologyFunded by the “Science and Technology Innovation Fund” and the “Torch Program,” certified under the ISO 9001 and ISO 27001 management systems, and involved in the development of multiple industry standards and registration guidelines for medical devices.,Provides integrated solutions for medical device companies, including technical regulatory affairs, clinical trials, contract manufacturing, consulting, and training.

Currently,LeadingMedicineMedical Device R&D Outsourcing Service Providers Are Strategically Positioning ThemselvesR&D Design and Contract Manufacturing Services.Although R&D design and contract manufacturing services currently face significant implementation challenges, it is undeniable that they represent the future direction of the industry and a new growth engine. We predict that over the next five years, R&D-focused medical device contract research organizations (CROs) will become a key focus for investors and the medical device industry. Leading companies will gradually capture market share currently held by smaller firms, and R&D design will emerge as the fastest-growing business segment for medical device CROs.

Most medical device R&D outsourcing service providers establish subsidiaries or offices in economically developed regions and medical device industry clusters to handle local business and cover surrounding provinces and cities. Their registration and filing services encompass China, the United States, the European Union, and other countries or regions, with most companies offering nationwide coverage across China for capabilities in registration, clinical trials, and related areas. In contrast, services such as R&D design and contract manufacturing typically cover only the locations of their workshops or laboratories and the adjacent two or three provinces and cities.。

The development of the medical device industry is correlated with regional economic levels. Eastern China, characterized by a robust economy and advanced healthcare standards, exhibits substantial demand for medical devices, thereby driving local industry growth. Furthermore, the region’s convenient transportation, strategic geographic location, and economic prosperity have attracted numerous foreign medical device enterprises, fostering industrial development and even creating cluster effects. Additionally, the high concentration of research institutions and laboratories in eastern China enhances R&D and innovation capabilities, leading to greater innovation in medical devices. Consequently, medical device R&D outsourcing service providers currently achieve higher cost-effectiveness when conducting related business in eastern China.

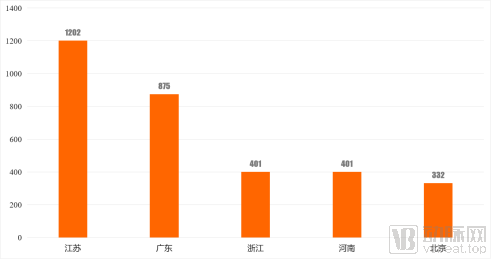

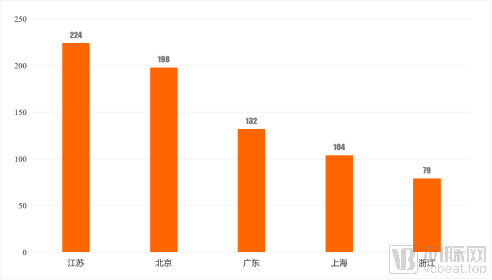

The development of the medical device industry varies across provinces and cities in China. According to the "2019 Annual Medical Device Registration Work Report" released by the National Medical Products Administration (NMPA), domestically registered Class II and Class III medical devices are primarily concentrated in economically developed regions. Specifically, Jiangsu, Guangdong, Zhejiang, Henan, and Beijing collectively accounted for 51.7% of the total number of first-time registrations for Class II medical devices in China in 2019; Jiangsu, Beijing, Guangdong, Shanghai, and Zhejiang together accounted for 69.1% of the total number of first-time registrations for Class III medical devices in China in 2019. Therefore, regions such as Jiangsu, Guangdong, Beijing, Zhejiang, Henan, and Shanghai have become the main competitive arenas for medical device research and development outsourcing service providers. Companies including Juyi Technology, Mediscreation, Tigermed Jietong, Osida, Sigma Medicine, Deneng Medicine, Aotai Kang, and Lingshi Medical have established offices or branches in Jiangsu, Beijing, Guangdong, Shanghai, and other locations.

Figure 7 Top 5 Regions in China by Number of First-Time Registrations for Class II Medical Devices in 2019

Source: Arterial Orange Database; Chart by VCBeat.

Figure 8 Top 5 Regions in China by Number of First-Time Registrations for Class III Medical Devices in 2019

Data Source: Artery Orange Database, Chart by VCBeat.

Different industrial clusters specialize in different segments of the medical device sector.The Guangdong-Hong Kong-Macao Greater Bay Area has gathered R&D and manufacturing enterprises specializing in medical imaging equipment, large-scale radiotherapy devices, and tumor hyperthermia equipment. The Yangtze River Delta industrial belt has concentrated R&D and manufacturing enterprises focused on disposable medical devices and consumables, ophthalmic equipment, medical imaging equipment, and radiofrequency tumor hyperthermia devices. The Beijing-Tianjin-Hebei Bohai Rim industrial belt has assembled R&D and manufacturing enterprises dedicated to medical imaging equipment, computer-navigated surgical systems, anesthesia ventilators, orthopedic devices, and cardiovascular devices.Medical device R&D outsourcing service providers may select appropriate industrial clusters to conduct their operations, based on their areas of expertise or key sectors they plan to prioritize.

Jinxian County in Jiangxi Province and Changyuan City (formerly Changyuan County) in Henan Province are prime regions for contract research and development (CRO) services in the medical device industry. Jinxian County has long been a hub for manufacturers of low-end medical devices, but it is currently upgrading toward “high-end and intelligent” production, creating numerous business opportunities. In 2018, the county was home to 136 medical device manufacturing enterprises, including 36 above designated size, with the total output value of medical devices exceeding RMB 15 billion. In 2019, the main business revenue of Jinxian’s medical device industry reached RMB 46.17 billion. That same year, Nanchang Municipality stepped up support for the sector in Jinxian by establishing a RMB 10 billion industrial fund and a RMB 50 million special-purpose fund to bolster the development of a trillion-yuan medical device industry cluster. A branch office of the medical device regulatory authority was also set up in Jinxian to strengthen oversight and services for local enterprises, while supporting the introduction and cultivation of contract development and manufacturing organizations (CDMOs) and launching CDMO pilot programs. In 2020, Jinxian County planned to develop the Jiangxi Medical Device Science and Technology Industrial Park, covering 1,950 mu, to further promote the growth of the local medical industry. In summary, Jinxian County is driving the transformation and upgrading of its medical device industry, fostering healthier development and creating new opportunities for medical device RDO service providers.

Changyuan City has gathered a large number of R&D and manufacturing enterprises specializing in low-value medical consumables. In 2018, Changyuan City was home to 2,324 medical device manufacturers and distributors, holding over 2,000 medical device product registration certificates covering products such as injection and puncture devices. Among these, medical consumables and anesthesia kits accounted for 60% of the national market share. In 2018, the total output value of Changyuan’s medical device industry exceeded RMB 10 billion. In 2019, Changyuan City formulated the Medical Device Industry Development Plan (2019–2035), aiming to strengthen the development of the medical device sector and promote the growth of the local medical device R&D outsourcing services industry.

Acceptance of medical device R&D outsourcing services varies across different subsectors of the medical device industry,Companies engaged in the R&D and production of high-value medical devices and consumables exhibit a higher acceptance of outsourced medical device R&D services, whereas those focused on low-value medical devices and consumables demonstrate lower acceptance.. Companies engaged in the R&D and production of high-value medical devices and consumables face substantial costs, have high demands for technical and research talent, and bear significant risks in independently conducting R&D, clinical trials, and manufacturing. Medical device R&D outsourcing service providers possess strong professional advantages in these areas. Consequently, companies developing and producing high-value medical devices and consumables exhibit greater acceptance of outsourcing services and a stronger willingness to pay. The situation is reversed for companies involved in low-value medical devices and consumables.

In the fields of cardiovascular intervention, orthopedic intervention, neurointervention, in vitro diagnostics (IVD), and large-scale imaging diagnostics, there is a wide variety of high-value medical devices and consumables, such as drug-coated balloons, vascular stents, PCR analyzers, and MRI equipment. Companies in these sectors have strong demand for research and development (R&D) outsourcing services, and most medical device R&D outsourcing service providers operate within these areas.

The number of companies offering R&D outsourcing services in emerging fields such as artificial intelligence, surgical robots, and 3D printing is also gradually increasing. This is primarily because products in these sectors are experiencing rapid growth in clinical application and involve high technical barriers. To accelerate time-to-market, relevant R&D enterprises tend to adopt R&D outsourcing models.

In fields such as ophthalmology, dentistry, and medical aesthetics, the requirements for technology and talent are relatively low, and the risks associated with R&D, manufacturing, and clinical trials are also lower. Consequently, the demand for R&D outsourcing among related enterprises is weak, resulting in a relatively small number of companies providing such R&D outsourcing services.

The above outlines the key highlights of the report. The complete framework is provided below. Scan the QR code to access the mini-program and read the full report for free:

I. CROs and CDMOs Are the Core Pillars of Medical Device R&D Outsourcing

II. Pilot Program for the Medical Device Registrant System Unlocks Demand, Propelling the Industry into a Growth Phase

III. Market Size Reaches RMB 10 Billion, with Orthopedic Implants and In Vitro Diagnostics as Key Service Focus Areas

IV. Core Business Will Shift from Clinical Trial Services to R&D and Manufacturing Services

V. Technological Innovation and Business Model Transformation Expand Operational Boundaries and Enhance Market Competitiveness

Special thanks to Mr. Dong Binzhe, CEO of Medisino; Mr. Cao Changqing, CEO of Juyi Technology; Mr. Zeng Jianhui, Chairman and General Manager of Zhizhong Technology; Mr. Zhao Xiaodong, CEO of Dewei Medical; and Mr. Mao Shuo from Qiming Venture Partners for their strong support of this report.

The field of outsourced R&D services for medical devices falls within the FOCUS 100 Healthcare Industry Innovation Tracks. FOCUS 100 aims to spotlight the 100 most innovative “golden tracks” in the healthcare sector. Leveraging proprietary industry data as its core, it builds a theoretical model framework around key industry drivers such as policy orientation, technological transformation, business model innovation, and capital trends, thereby producing insightful research reports on niche segments of the healthcare industry.

Previously, we have released"Innovation Report on the Imaging FFR Industry", "Innovation Report on the Nucleic Acid Testing Industry", "Digital Innovation Report on Diabetes Management", "Innovation Report on the Pharmaceutical Digital Marketing Services Industry"Awaiting report. We will continue to roll out more in the future."Real-World Study Report," "Digital Hypertension Management Report," "Digital Medical Ultrasound Report," "Cardiovascular Implantable Device Industry Report," "Commercial Health Insurance Report"...and other reports in the FOCUS 100 Healthcare Industry Innovation Series. To this end, VCBeat Research Institute cordially invites relevant enterprises to participate in the research for these reports. If you are interested, please feel free to contact us. For specific details, please consult Ms. Xiao Peiling, Corporate Specialist, at 152-2316-2186 (WeChat ID same as phone number).