Secrets in the 387-Page Financial Reports of China's Top Six Health Insurers: Revenue and Channel Transformation Signal an Industry Inflection Point

Amazing!

A newly minted analyst who has not read the disclosures of the six major specialized health insurance companiesPage 387 Annual Financial Statements, one might assume that, riding the trillion-yuan wave of health insurance, these six companies must be raking in huge profits, right?

However, the reality is that three of these six companies have yet to turn a profit. Among the three companies with positive operating profits (total profits),Taibao Allianz Health Earned Only RMB 40,596 for the Full Year. This sum of money can only rent 1,000 square meters of office space in Shanghai's Lujiazui for one week.

From a macro perspective, health insurance is undoubtedly a sector that most venture capital firms seek for its potential to deliver outsized returns. In an industry with an annual growth rate exceeding 30%, identifying a company that demonstrates sustained growth within this sector can generate superior returns through the compounding effect of both factors.

But the fact is that this industry is not yet running so smoothly.Traditional production relations in the industry continue to leverage their historical advantages, while the force of innovation is hindered by heavily regulated data.If health and medical data are not truly integrated, it will be difficult to advance actuarial analysis and risk control, making it impossible to launch high-quality health insurance products.

These six major specialized health insurance companies occupy the upstream segment of the industry chain, yet why are most of them mired in losses? What circumstances do they face, what pains and growth are they experiencing, and what hopes and dreams do they carry?

To this end, VCBeat has analyzed the 2019 and historical annual financial statements of these six specialized health insurance companies to provide answers to these questions.

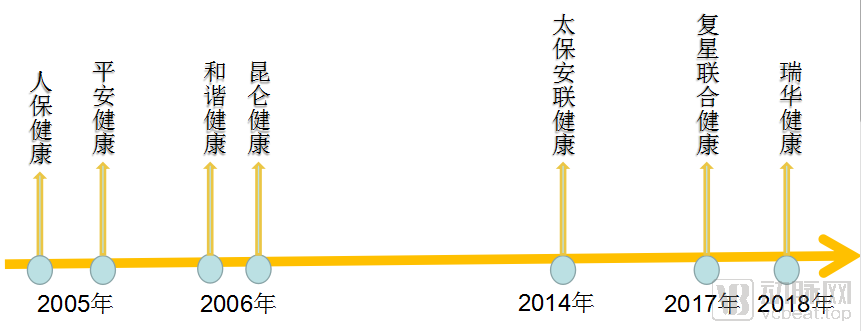

Establishment Dates of the Seven Specialized Health Insurance Companies

(Note: Given that Hexie Health is still under the takeover of the China Banking and Insurance Regulatory Commission, this article will no longer discuss the Hexie Health case except in special circumstances.)

There are currently seven specialized health insurance companies in China. PICC Health, established earliest, was approved for establishment in March 2005. Including PICC Health, four specialized health insurance companies were founded between 2005 and 2006. Ruihua Health was the last to be established, coming into being only in May 2018.

In terms of business scope, the seven companies are largely similar. For instance, Kunlun Health’s business scope includes “health insurance and personal accident insurance in both RMB and foreign currencies; government-commissioned health insurance services aligned with national healthcare security policies; consulting and agency services related to health insurance; reinsurance services related to health insurance; fund utilization activities permitted by national laws and regulations; and other businesses approved by the China Insurance Regulatory Commission (CIRC).”

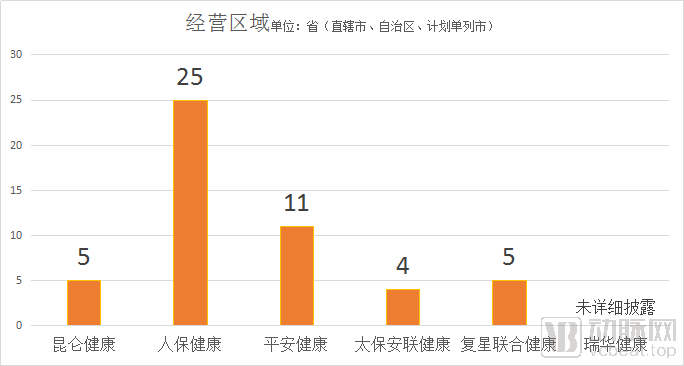

(Note 1: Ruihua Health did not disclose its operational regions in detail in its 2019 annual report.)

In terms of operational regions, there are currently significant differences among various insurers. PICC Health has the widest business scope, covering the vast majority of provinces (municipalities directly under the Central Government, autonomous regions, and cities with independent planning status) across China. In contrast, CPIC-Allianz Health’s operations are limited to only four regions: Beijing, Shanghai, Guangdong Province, and Sichuan Province. However, it is worth noting that with the rise of internet channels, regional barriers are likely to be broken down. The recent efforts by Fosun United Health and others in expanding through online insurance channels deserve close attention.

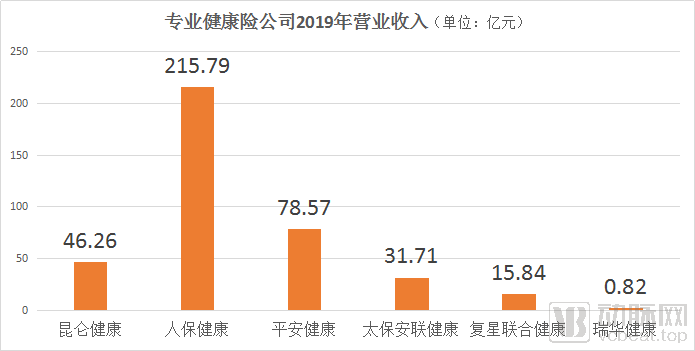

Differences in operational regions and establishment dates have, to some extent, influenced the revenue and asset scales of enterprises. Among these six specialized health insurance companies, PICC Health, which has the longest history and the largest operational scale, enjoys an absolutely leading position in terms of revenue. In 2019, PICC Health recorded operating revenue of RMB 21.579 billion, exceeding the combined total of the other five companies.

The combined operating revenue of the six specialized health insurance companies in 2019 totaled RMB 38.899 billion, accounting for 5.5% of the original premium income from health insurance in 2019.

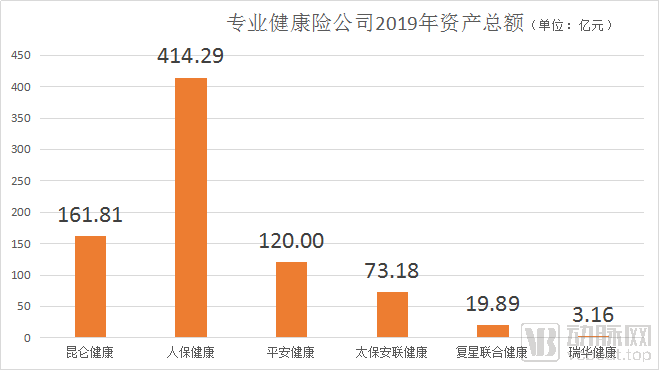

PICC Health also boasts an asset scale that is absolutely leading in strength, reaching RMB 41.429 billion in 2019; Ruihua Health, established only two years ago, has the smallest asset scale, amounting to merely RMB 316 million.

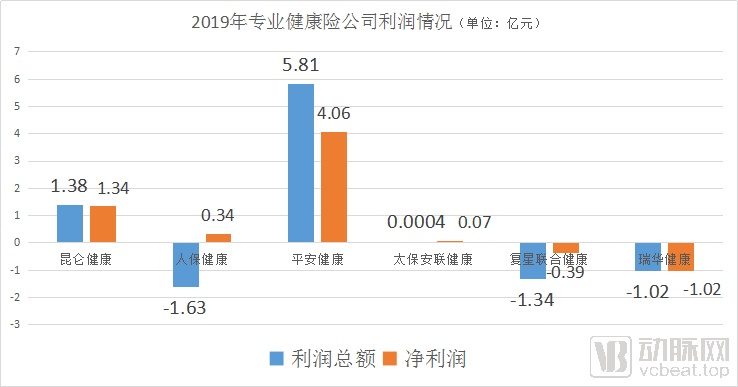

In terms of profitability, Ping An Good Doctor holds the leading position, having achieved an operating profit of RMB 581 million in 2019.

Note: Net Profit = Total Profit – Income Tax; Total Profit = Operating Profit + Investment Income + Subsidy Income + Non-operating Income – Non-operating Expenses. In light of industry conditions and the specific circumstances of the companies analyzed in this article, we have selected “Net Profit” and “Total Profit” as the two core indicators.

As shown in the figure, all four health insurance companies achieved profitability in 2019, except for Fosun United Health and Ruihua Health, which were still operating at a loss due to their relatively short establishment periods. However, a closer examination of their financial data reveals that PICC Health remained at a loss in terms of total profit; its reported profitability was attributable to the impact of deferred income tax. After excluding the effect of deferred income tax, Taiping Allianz Health’s profit amounted to only RMB 40,596.

Looking back on the 15-year development journey of specialized health insurance companies, they have long been in a state of exploration. In the early stages of the industry, when consumers’ awareness of risk protection was insufficient, specialized health insurance companies largely followed the lead of life insurers. Most notably, during the 2012–2017 period when the asset-driven liability model gained prominence, many specialized health insurers developed medium- and short-term care insurance products as a workaround to expand savings-oriented businesses, thereby compromising their professional specialization. At that time, the term “specialized” was less a badge of identity and more a constraint on it.

What has fundamentally transformed the operational logic of specialized health insurance companies is the strong regulatory guidance emphasizing “insurance as protection” and the surge in market demand. Rising living standards have heightened public awareness of risk protection, thereby generating broad market demand for protection-oriented products. As a result, specialized health insurance companies have entered a new stage of development, with promising growth prospects.

Based on a comprehensive review of industry trends and the companies’ own circumstances, 2020 will mark a pivotal turning point where the growth trajectories of the six specialized health insurance companies rise once again.

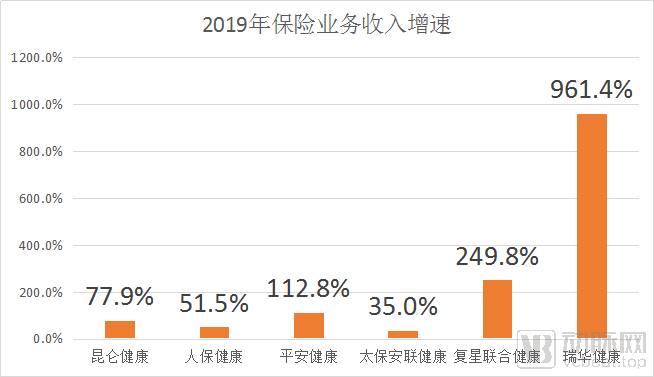

Although the 2019 financial reports of these six specialized health insurance companies showed less-than-optimistic operating profits, their premium income growth rates were remarkably attractive.

Note: Ruihua Health was established in May 2018. Its premium income from insurance business amounted to only RMB 740,000 in that year. Although it achieved a growth rate of 961.4% in 2019, its revenue scale remained relatively small.

From this, we can see that, except for Ruihua Health, which has a relatively short history and whose growth figures are not very meaningful for reference,In 2019, both Fosun United Health and Ping An Health doubled their insurance premium income compared to 2018, with Ping An Health achieving a growth rate of 112.8% and Fosun United Health reaching 249.8%.Meanwhile, the other three insurers also posted robust growth in premium income, with Taiping Anlian Health, the slowest grower among them, still achieving a 35.0% increase. All six specialized health insurance companies outperformed the “market average” in terms of premium income—In 2019, the premium income from health insurance reached RMB 706.6 billion, with a growth rate of 29.7%.

Following the macro-level analysis, we will now proceed with case-by-case analyses, as each company has its unique circumstances.

Fosun United Health: Significant Internet Advantages

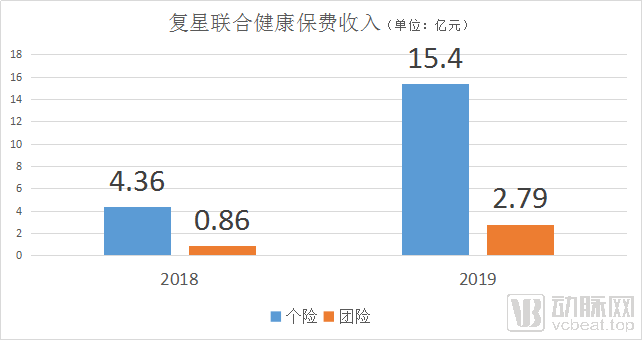

Fosun United Health Insurance’s premium income grew from RMB 520 million in 2018 to RMB 1.819 billion in 2019, with significant growth in both individual and group insurance businesses.

It is worth noting that within the composition of premium income, Fosun United Health’s individual insurance business far exceeds (by several times) its group insurance business, whereas other insurers primarily focus on group insurance. This disparity stems from Fosun United Health’s significant efforts in internet channels; since the internet targets atomized individuals, its individual insurance business substantially outweighs its group insurance business.

It is precisely for this reason that Fosun United Health’s total premium income in 2019 amounted to RMB 1.819 billion, while its expenditure on fees and commissions reached RMB 684 million, indicating exceptionally high channel costs.

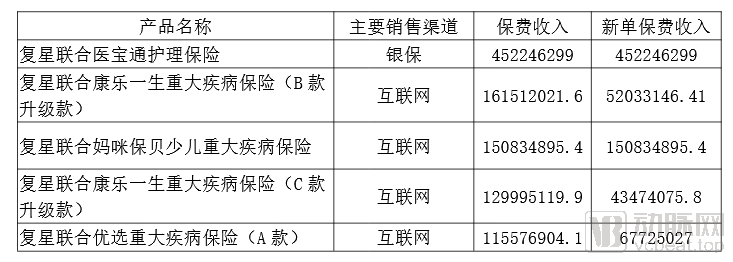

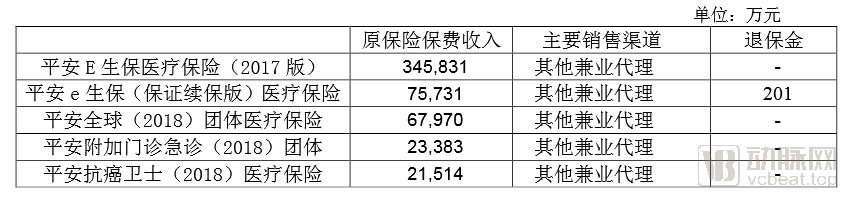

According to its 2019 annual report, the five major products that made significant contributions to premium income were primarily sold through internet channels.

(Image source: screenshot from the annual report)

Regarding future development, Fosun United Health will“Adhere to the principle that insurance is fundamentally about protection, persist in product innovation, maintain a product strategy focused on long-term and protection-oriented products, commit to value growth, and continuously explore the path of integrating healthcare with insurance.”It has been incorporated into its strategic deployment.

This may well be the path that the entire health insurance industry will continue to follow.

PICC Health: Individual Health Insurance Surges by 162.6%

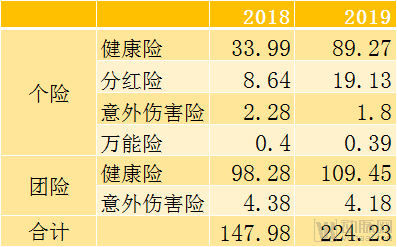

For PICC Health, whose premium income exceeded RMB 10 billion, its premium business revenue grew from RMB 14.798 billion in 2018 to RMB 22.423 billion in 2019, achieving a growth rate of 51.5%. On a more detailed basis, its individual health insurance premiums rose from RMB 3.399 billion to RMB 8.927 billion, recording a growth rate of 162.6%.

(PICC Health Insurance Business Revenue)Unit: 100 million yuan

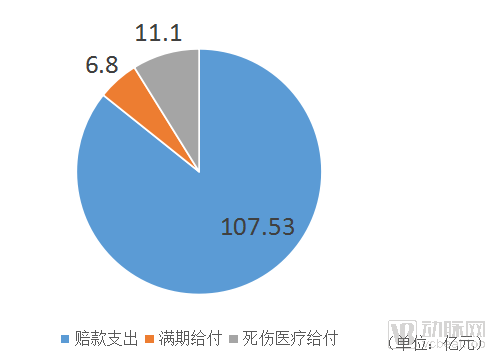

In terms of fee and commission expenses, PICC Health incurred only RMB 729 million in 2019, a figure slightly higher than the RMB 684 million reported by Fosun United Health. However, in terms of insurance business revenue, the former was more than ten times that of the latter. The largest component of PICC Health’s operating expenses was claims payments, which totaled RMB 12.542 billion in 2019.

![]()

(PICC Health's 2019 Claims Payment Data)

Notably, PICC Health separately disclosed the revenue and expenses of its health management services in its financial reports. In 2019, the company recorded RMB 32 million in health management revenue and RMB 42 million in expenses; in 2018, health management revenue amounted to RMB 22 million, with expenses totaling RMB 46 million.

Although PICC Health’s health management revenue was only at the tens of millions of yuan level, it posted losses for two consecutive years.However, industry experience suggests that ramping up health management services will significantly drive the entire business ecosystem, directly benefiting areas such as product actuarial analysis and claims expenditures.

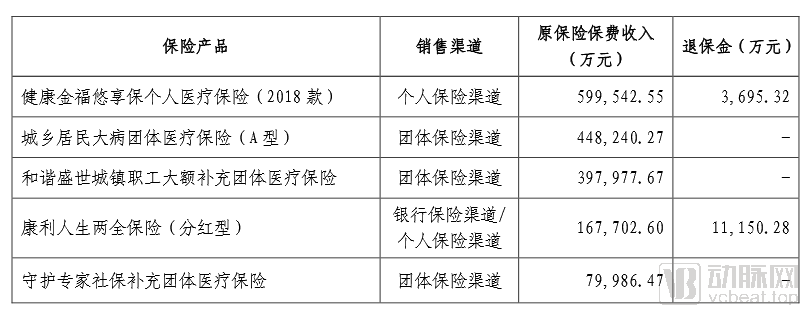

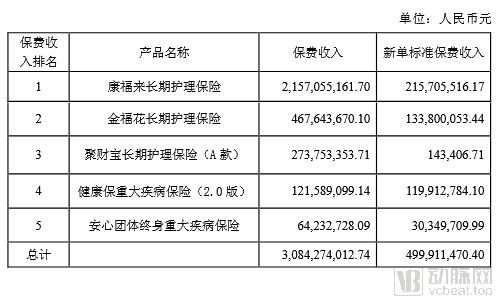

At the product level, its top five revenue-generating products are as follows:

(Image source: screenshot from the annual report)

Strategically,PICC Health Insurance proposes to build an operational model of “health insurance + health management + information technology” in the future.

Ping An Health: Health Management Business Reaches RMB 1 Billion Scale

From 2018 to 2019, Ping An Health delivered impressive financial results, with several core metrics doubling. Revenue increased from RMB 3.916 billion to RMB 7.857 billion, operating profit rose from RMB 319 million to RMB 582 million, and net profit grew from RMB 144 million to RMB 406 million.

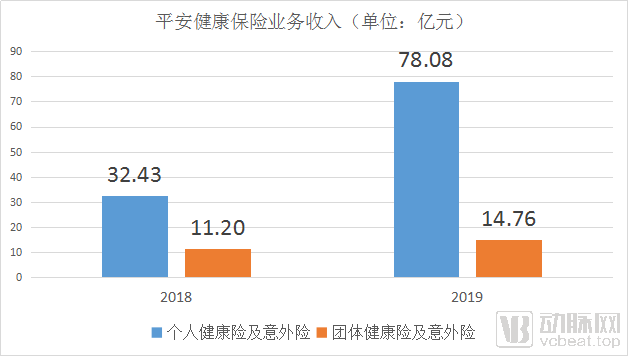

Specifically in the insurance business (Ping An’s statistics include both direct and reinsurance premiums), it grew from RMB 4.363 billion to RMB 9.285 billion.

As shown in the figure, Ping An Health’s insurance revenue structure demonstrates that individual health and accident insurance has experienced the largest growth rate, which is consistent with PICC Health.

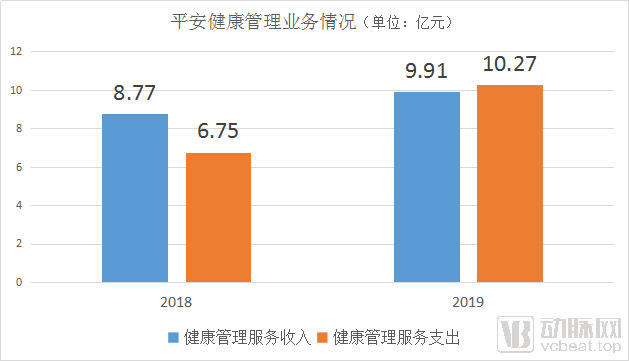

However, the above is not its most prominent business segment. Ping An Health’s standout operation is its health management business, which generated nearly RMB 1 billion in revenue in 2019. Looking ahead, the health management business is poised to become a new growth engine for Ping An Health, driving robust development across its entire ecosystem.

In terms of products, the premium income from the top five insurance categories accounted for 87% of Ping An Health’s total premiums.

(Image source: screenshot from the annual report)

From the above, we can see that,All of Ping An Health’s top five insurance products by revenue are medical insurance policies. Coupled with its massive health management business, Ping An Health is poised for significant future growth.

Strategically, Ping An Health has proposed to actively respond to the requirements of the national “Healthy China 2030” strategy, participate in the construction of the national healthcare security system, and strive to provide the public with multi-level and diversified protection. Based on professional services and risk control, it will develop businesses such as pure-protection medical health insurance and health services.

Kunlun Health: Investment-Driven, Turning Losses into Profits

In 2019, the most significant change for Kunlun Health was its turnaround from loss to profit, achieving a net profit of RMB 134 million, compared with a loss of RMB 770 million in 2018.

There are two reasons for the turnaround from loss to profit:First, in the health insurance business, Kunlun Health’s revenue grew from RMB 1.803 billion to RMB 3.355 billion, nearly doubling; second, regarding investment returns, Kunlun Health incurred an investment loss of RMB 111 million in 2018, whereas it achieved an investment gain of RMB 1.159 billion in 2019. The contribution of investment income to profits was the primary reason for Kunlun Health’s turnaround from losses to profitability.

In terms of products, the top five insurance categories by premium income for Kunlun Health are primarily dominated by in-force policies and critical illness insurance.

Taiping Anlian Health: Ceded premiums are the main source of revenue, with a meager annual profit of 40,596 yuan

From 2018 to 2019, Taibao-Allianz Health, a relatively young company, successfully turned losses into profits. In 2018, its total profit was a loss of RMB 172 million; by 2019, its total profit reached RMB 40,596.

Tai Bao Allianz Health’s entire revenue structure differs significantly from that of other specialized health insurance companies, where insurance business revenue primarily consists of gross written premiums.However, CPIC-Allianz Health’s gross written premiums accounted for less than 10% of its total revenue, with ceded reinsurance premiums constituting the vast majority.

Of its original premium income, group insurance premiums amounted to RMB 347 million in 2019, while individual insurance premiums totaled only RMB 7 million, with group insurance accounting for the vast majority.

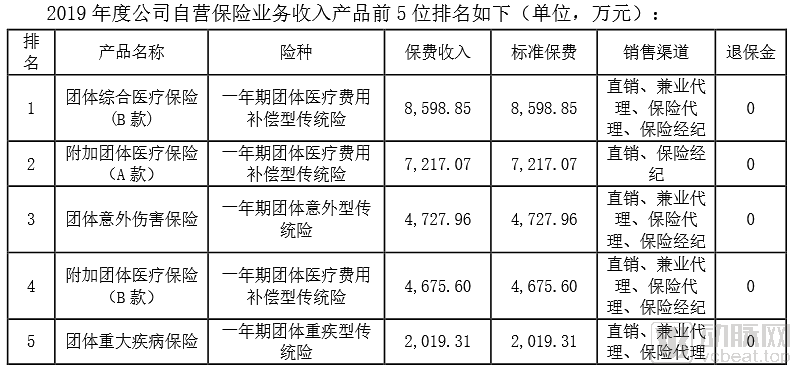

In terms of product offerings, Taibao Allianz Health has a limited portfolio, primarily consisting of one-year group medical insurance policies, with insufficient product innovation. This is partly attributable to its relatively short operating history.

(Image source: screenshot from the annual report)

In its 2019 annual report, Taiping Allianz Health Insurance provided a self-assessment:Due to market conditions, the overall development model and value proposition of the short-term health insurance market are still being explored, leading to uncertainties in business growth. In terms of business models, companies’ own approaches remain in the exploratory phase, and specialized health insurers need to further investigate sustainable operating models.

Ruihua Health has been in operation for a relatively short period; therefore, this article will not provide an in-depth analysis.

After analyzing the data from the six major specialized health insurance companies, we can see that their development over the past one to two years has been a mix of challenges and opportunities:On the positive side, all of these companies outperformed the broader market in insurance business revenue, with firms such as Fosun United Health and Ping An Health even achieving doubled revenues. Specifically, in the health insurance segment, every company recorded growth exceeding 50%, significantly surpassing the market average. On the negative side, although specialized health insurance companies are currently in a favorable industry spotlight, their profitability remains lackluster. Only Ping An Health and Kunlun Health have generated substantial profits, while the others appear to remain in a state of “uncertainty.”

From multiple perspectives, including policy, market size, and market demand, 2020 is destined to be a “breakout year” for the development of health insurance, presenting professional health insurance companies with unique opportunities.

Based on industry practices, specialized health insurance companies may break through in the following three areas:

First, the industry must return to the core principle that “insurance is fundamentally about protection.” An analysis of the top five premium-generating products from these six specialized health insurance companies reveals that several firms suffer from a severe shortage of long-term medical coverage products, with their revenue still reliant on persistent financial-type products. This deviates from the current overarching policy directives. The true path forward lies in breaking away from legacy models and focusing on designing and developing products that provide genuine health and medical protection.

Second, the industry’s current level of technological and digital integration is insufficient, a shortcoming that is particularly evident in distribution channels. The health insurance sector remains relatively conservative and traditional, with policy enrollment still heavily reliant on paper copies and scanned documents. This hinders data accumulation and the application of advanced technologies. Achieving end-to-end digitization would enable technological innovations, such as artificial intelligence, to propel the industry toward broader horizons and greater opportunities.

Third, health insurance companies should strengthen their presence in the healthcare services sector. Policyholders do not purchase insurance with the expectation of filing claims; rather, they seek access to medical coverage and high-quality healthcare services. If the term “health insurance” is deconstructed into “health” and “insurance,” it becomes clear that what customers are truly buying is “health.” In this regard, specialized health insurers should strive to enhance users’ health management, facilitate convenient access to medical care, and streamline the processes for insurance claims and reimbursements.

From the current perspective, for all participants in the health insurance industry, including specialized health insurance companies,Now may be a moment for everyone to regain their footing.

"Keep your feet on the ground, and look up at the stars."

(Special thanks to Jiang Guanjun, Partner at Mingde Actuarial Consulting, and Hao Xinya, Analyst at EO Intelligence, for their generous support in preparing this article.)