Hygeia Healthcare Soars Over 40% on HKEX Debut, Signaling a Capital Spring for Private Specialty Medical Services?

VCBeat has learned that on June 29, 2020, Hygeia Healthcare Holdings Co., Ltd., a leading oncology healthcare group in China, listed on the Main Board of The Stock Exchange of Hong Kong Limited, becoming a focal point of the industry.

During its IPO, Hygeia Healthcare’s shares surged 23.24% at the opening, trading at HK$22.80. The international offering was oversubscribed by 25 times, while the Hong Kong public offering saw an oversubscription of 608 times. By the close of trading on the day, Hygeia Healthcare’s share price settled at HK$26.00, marking a 40.54% increase and bringing its total market capitalization to HK$15.6 billion.

Hygeia Healthcare was established in 2009 as a specialized medical investment group with Sino-US joint venture backing. Centered on oncology, the company focuses on the investment, construction, and operational management of chain cancer treatment and neurology medical institutions. Zhu Yiwen serves as the Chairman of the Group. Through direct equity ownership or management rights, Hygeia Healthcare operates or manages a network of ten hospitals centered on oncology, located across seven cities in six provinces in China. Additionally, the company provides services to 14 hospital partners (including hospitals under its trusteeship) in nine provinces across China for their radiotherapy centers. According to relevant information, Hygeia Healthcare completed four rounds of financing in the primary market, involving institutions and enterprises such as Changling Capital, Warburg Pincus, Boyu Capital, CITIC Capital, Huagai Capital, BOC Guangdong Financial Holdings, and WuXi AppTec.

Just over a month ago, Sanbo Brain Hospital, a well-known specialized neurology hospital group, announced the completion of its Series B equity financing, exceeding RMB 800 million. In early June, Haoyunbang, a premium chain of specialized reproductive health clinics, also closed a new round of financing. Since 2015, the healthcare services sector, particularly specialized clinic chains, has remained highly active, with significant financing secured in the primary market across dentistry, medical aesthetics, ophthalmology, and pediatrics.

The entire market is generally optimistic about specialized medical services, believing that theirPossesses advantages such as counter-cyclical resilience and ample cash flow.. However, at the same time,The Four Pain Points Inherent to the Specialized Chain Healthcare Services Industry: High Capital Investment, Slow Return on Investment, Long Business Cycles, and Difficult Exit Strategies, which has also cast doubt on the development of specialized medical services. In 2019, the specialized medical services sector remained relatively quiet in the capital markets, and this year’s COVID-19 pandemic has significantly impacted the growth of private specialized service providers.

The recent IPO of Hygeia Healthcare, along with the latest financing rounds for companies such as Sanbo Brain Hospital and Haoyunbang, all signal a recovery in the specialized medical services market. However, we are well aware that the development of any industry is not achieved overnight. What remaining challenges and pain points exist in the private specialized medical services sector? How have policies evolved? What best practices have emerged within the industry? What are the future trends? Has the sector truly entered a “springtime” for capital investment? To address these questions, VCBeat engaged in discussions with enterprises in the private specialized medical services sector, as well as investors actively monitoring and participating in this field.

As a heavily regulated sector, the healthcare industry’s fortunes are often shaped by the direction of policy winds.

From the perspective of policy trends,The Private Specialized Medical Services Industry Is Reaping the Dividends of Reform. In 2015, China began to accelerate the promotion of tiered diagnosis and treatment and facilitate multi-site practice for physicians,Encourage Private Capital to Enter the Primary Healthcare Service Sector, with the aim of enhancing the overall efficiency and service quality of China’s healthcare system, striving to achieve “initial diagnosis at primary care level, two-way referral, separate management of acute and chronic conditions, and coordination between different levels of care.”

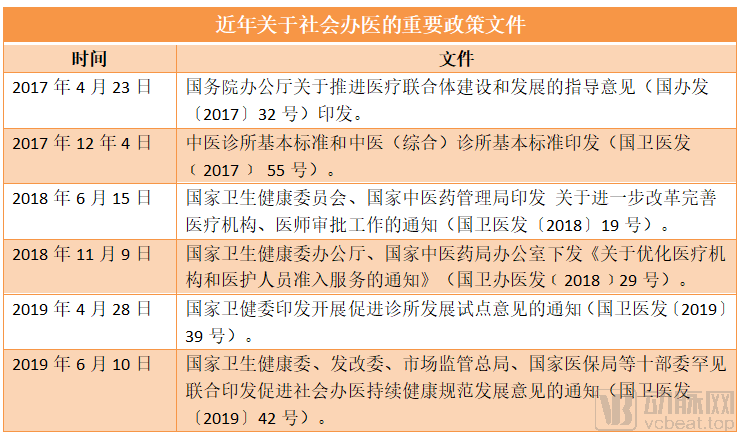

In May 2017, the State Council issued the “Opinions on Supporting Social Forces in Providing Multi-level and Diversified Medical Services.” The release of these “Opinions”Enabling the implementation of a series of policies supporting the establishment of private chain clinics., for example, doctors may operate clinics while employed, the approval system for clinic establishment is abolished, companies are permitted to open clinics, geographic restrictions on clinic location are removed, private clinics are integrated into the national medical insurance system, and a single legal entity may apply to establish multiple chain clinics.

In June 2019, the National Health Commission released 22 new policies to promote the development of private hospitals, emphasizing that the government would increase its support for socially operated medical institutions. From 2019 to 2020, pilot programs for the filing-based management of clinics were launched in 10 cities, including Beijing, Shanghai, Shenyang, Nanjing, Hangzhou, Wuhan, Guangzhou, Shenzhen, Chengdu, and Xi’an. This moveReduced the procedural requirements and entry barriers for chain outpatient clinics to obtain qualifications.The policy will also support private medical institutions in joining telemedicine collaboration networks to enhance their diagnostic and treatment service capabilities.

The relaxation of policies has boosted the development of the private specialized medical services industry. According to data released by the Statistical Information Center of the National Health Commission on June 6, 2020, the total number of hospitals in China reached 34,154 in 2019, an increase of 1,145 from the 33,009 recorded in 2018. Among these, the number of public hospitals decreased by 102, while the number of private hospitals increased by 1,447. The number of private hospitals rose to 22,424, accounting for approximately 65.7% of the total.

In terms of volume, private hospitals are experiencing robust growth, yet their share of total service provision remains modest. Data from the Statistical Information Center of the National Health Commission shows that in 2019, public hospitals recorded 3.27 billion patient visits (accounting for 85.2% of all hospital visits), while private hospitals accounted for only 570 million visits (14.8% of the total). Undoubtedly,The overall competitiveness of private hospitals remains weak.。

There are three reasons behind this. First,A Period of Adjustment Is Still Needed Between Policy Liberalization and Marketization, the implementation of relevant policies may be delayed due to various factors; second,Public Trust in Public Hospitals Far Exceeds That in Private Hospitals, and this cannot be changed overnight; it requires continuous promotion by the entire industry. Third, the new policy on multi-site practice has only been in place for three years, and free practice by medical personnel within the provincial scope has just begun.Medical human resources remain scarce.。

Nevertheless, as a vital force in the private healthcare sector, companies specializing in specialized medical services are able to achieve rapid expansion and realize economies of scale, owing to their standardized business models and strong replicability. Consequently, this sector continues to attract sustained attention from the capital markets.

For private specialized medical service enterprises, what aspects do investors focus on?

Firstly,Market Size and the Prominence of Supply-Demand Imbalances, secondlyShould we prioritize strategic positioning in sub-sectors with stronger consumer-oriented attributes?. The choice of track determines the pace of a company's growth. For private specialized medical service providers, only by not relying on medical insurance and avoiding competition with public hospitals for market share and patients can they secure favorable room for development.

Furthermore, for individual stores, investors evaluate the ramp-up period and return on investment (ROI), requiring the achievement of specific operational and financial metrics. For chain stores, they assess regional distribution, standardization levels, and economies of scale. Subsequently, indicators such as conversion capability, patient retention, and repurchase rates are examined.

The choice of track determines the market size and the pace of development. The design of products and services determines the strength of conversion capability; the optimization of medical processes and efficiency improvements determine patient retention; while physician quality and brand operational capabilities ultimately determine patient repurchase rates.. Through this cycle, a closed-loop service system for medical specialties is formed.

“For Changling Capital, weFocus and persistence are centered on three elements: inclusiveness, efficiency enhancement, and innovation.“Inclusive” means we prefer to invest in healthcare companies that benefit a larger population. “Efficiency enhancement” refers to improving the overall efficiency of the healthcare system. “Innovation” pertains to those with unique and distinctive ideas,” Jiang Xiaodong, Managing Partner of Changling Capital and the exclusive Series A investor in Hygeia Healthcare, told VCBeat. As an early-stage investor, in the process of accompanying portfolio companies through their growth,First, genuinely understand and align with the company’s mission; second, leverage acquired best practices and abundant resources to support the growth of portfolio companies.。

In addition to Hygeia Healthcare, Changling Capital also served as the sole Series A investor in Gushengtang, the leading chain operator of traditional Chinese medicine (TCM) outpatient clinics. Gushengtang currently operates nearly 50 clinics across approximately 20 cities, with revenues exceeding RMB 1 billion in 2019. The company achieved a compound annual growth rate (CAGR) of over 40% in revenue during the four-year period from 2016 to 2019 and has already attained profitability at scale. According to Jiang Xiaodong, two key factors underpin Gushengtang’s outstanding performance.

First, adopt a long-term perspective rather than being confined to immediate gains and losses.“Building a chain of traditional Chinese medicine (TCM) clinics is an extremely challenging endeavor. The founding team of Gushengtang recognized the industry’s inherent issues early on and has been actively exploring solutions. Regardless of external opinions—whether optimistic or pessimistic in the short term—they have remained steadfast in advancing their mission.”

Second, it must be sufficiently innovative and distinctive.“Gushengtang has pursued a development path quite distinct from that of the vast majority of enterprises, as it has gained a clear understanding of the essence of the traditional Chinese medicine (TCM) industry, scaled up its operations continuously, and achieved strong financial performance.”

Oriental Speech Therapy, a speech therapy institution also backed by Changling Capital, currently operates nearly 40 centers across more than 20 cities in China. It generated revenue of nearly RMB 500 million in 2019, with a compound annual growth rate (CAGR) of close to 80% over the previous four years (2016–2019), and has already achieved profitable operations at scale. “Like Gushengtang, Oriental Speech Therapy exhibits both of these characteristics,” said Jiang Xiaodong.

In the field of specialized medical services, there is an unavoidable benchmark enterprise: Aier Eye Hospital. Understanding its model and latest developments can provide insights into the industry's height and direction.

As the largest ophthalmic medical institution in China, Aier Eye Hospital’s main business scope includes the diagnosis and treatment of ophthalmic diseases, surgical services, and medical optometry and glasses fitting. Under its global strategic layout, the company has expanded year by year, extending its network of ophthalmic medical institutions to Europe and the United States. As of December 31, 2019, Aier Eye Hospital operated 105 hospitals and 65 outpatient departments within China; additionally, there were 275 hospitals and 37 outpatient departments under its merger and acquisition funds.

From the perspective of business layout, the current model of Aier Eye Hospital is as follows:The tiered chain system is further improved, and multi-level ophthalmic medical services are gradually being implemented.. While accelerating the construction of its medical network system, Aier Eye Hospital actively aligns with the international industrial ecosystem to promote the clinical translation and innovation of ophthalmology and visual science.

According to Aier Eye Hospital's 2019 annual report, the company achieved an operating revenue of RMB 9.99 billion in the past year, a year-on-year increase of 24.74%; the net profit attributable to shareholders of the listed company was RMB 1.379 billion, a year-on-year increase of 36.67%. During the reporting period, Aier Eye Hospital recorded 66.2823 million outpatient visits, a year-on-year increase of 15.56%, and performed 608,300 surgical procedures, a year-on-year increase of 7.76%. The operating revenue approached the RMB 10 billion mark.

What Sets Aier Eye Hospital Apart in Achieving Such Remarkable Success?

1. The tiered chain model builds brand equity and customer stickinessAier Eye Hospital leverages its four-tier chain model—comprising central, provincial/municipal, prefectural-level city, and county-level hospitals—to achieve internal sharing of technical resources. Lower-tier hospitals within the company receive technical support from higher-tier institutions, optimizing resource allocation and enabling tiered treatment for patients with varying conditions. Patients with complex or difficult cases can be referred from lower-tier to higher-tier hospitals, ensuring full utilization of medical resources across all levels. Benefiting from standardized tiered chaining, Aier Eye Hospital demonstrates high replicability and strong capabilities for geographic expansion.

Second, R&D expenditures have continued to grow steadily.According to annual report data, Aier Eye Hospital’s R&D expenditure has shown a significant increase: over an eight-year period, it rose from RMB 3.092 million in 2012 to RMB 152.3 million in 2019. This growth reflects Aier Eye Hospital’s continuous investment in the clinical application of ophthalmic technologies. In its 2020 strategic plan, Aier Eye Hospital is advancing an information technology strategy centered on comprehensive cloud migration, independent research and development, clinical informatization, internet hospitals, and ophthalmic big data. Meanwhile, the company is prioritizing the development of internet-based ophthalmic hospitals to enhance an integrated online-offline service model for ophthalmic medical care and eye health management.

Third, ample equity incentivesAt Aier Eye Hospital, technically skilled or managerial professionals with core competencies can become partner shareholders to jointly establish new hospitals with Aier, including newly built, expanded, or acquired facilities. To incentivize talent, Aier has implemented various incentive programs, such as equity-based incentives under its partnership model, to enhance management efficiency and accelerate expansion. These partnership and equity incentive plans have provided the company with a robust pipeline of hospital assets suitable for consolidation. While boosting the motivation of core talent, these initiatives also address the challenges of medical talent shortages and attrition accompanying the company’s rapid expansion.

Founded in 2014, Haoyunbang has been deeply engaged in the field of assisted reproduction. “Through exploring and attempting various business models and pathways, Haoyunbang has enabled its entire team to gain a deeper understanding of the reproductive health industry,” Huang Sen, founder of Haoyunbang, told VCBeat. Leveraging the advantages of its proprietary internet platform, Haoyunbang remains committed to establishing outpatient clinics as its core operational foundation, gradually creating a closed-loop system that integrates online platforms with offline clinic services for seamless conversion and care. To date, Haoyunbang has established specialized reproductive outpatient clinics in Beijing, Guangzhou, Jinan, Wuhan, and other cities, and has also built its own reproductive center in Thailand.

“Opening a single store is relatively straightforward, but the capabilities required to successfully launch and operate multiple stores are distinctly different; this is precisely what makes chain expansion both challenging and appealing.” In Huang Sen’s view,Entrepreneurs in the field of specialized medical services should pay attention to three key points. First, they must have a deep understanding of the demand for specialized diseases, user needs, and industrial forms. Second, they need to possess medical capabilities, including top-tier medical resources and experts within the enterprise. Third, enterprises must have the ability to utilize SaaS (Software as a Service) to exponentially amplify their replicable capabilities.

In practice, specialized medical service enterprises must first establish a robust single-store model. Without a clear single-store model, all subsequent operations are unfeasible. How can one simply assess the viability of a single-store model? First, evaluate whether there is sufficient patient volume willing to seek outpatient care at the clinic. Second, determine whether the revenue generated can support normal store operations. Third, examine the ramp-up period required for the store to reach maturity. Fourth, assess how long it takes for the store to break even and achieve profitability. “To put it plainly, if your clinic were relocated, could it survive, and how well would it perform?” said Huang Sen.

Once the single-store model is established, replicability must be considered.. In this regard, medical specialty service providers should note that,The barrier to entry for core medical technologies should not be too high., the training cycle for physicians cannot be too long, otherwise it will affect the efficiency of replication; in addition,The existing supply of physicians should be relatively abundant.For example, since the majority of patients in China seek care at tertiary hospitals, primary care physicians often face underutilized workloads and urgently need to improve their clinical competence. Implementing systematic training programs to better leverage the existing physician workforce could help address primary care demand to a certain extent.

Based on the above analysis, it is evident that in the field of private specialized medical services, the gradual liberalization of policies, increased attention and involvement from capital, and refined corporate operations will make the entire market more vibrant and full of potential.During this process, an increasing number of high-quality private specialized service enterprises will emerge.Come。

Of course, it is worth noting that the pain points in the private specialized healthcare service industry still persist. How to effectively address these issues and seize emerging trends will be a critical consideration for every “trendsetter” in the field of specialized medical services.

Through communications with industry players and investors, combined with VCBeat’s past coverage and relevant corporate data, we believe there are five key trends in specialized medical services that warrant attention.

First, the ability of enterprises to leverage SaaS will become increasingly important.“SaaS value can be understood as the value of the Internet, which brings benefits on three levels: first, it enables enterprises to build a ‘strong headquarters’; second, it empowers them with rapid replication capabilities; and third, it allows for data accumulation from the outset, thereby unlocking the value of subsequent data mining,” said Huang Sen, founder of Haoyunbang.

During their development, many specialized healthcare service providers often fail to fully appreciate the value of Software-as-a-Service (SaaS). In reality, the continuous refinement of SaaS solutions parallels the standardization of enterprise business processes. Furthermore, regarding timing, it is advisable to implement SaaS as early as possible. In the early stages, employee acceptance of SaaS tends to be relatively high. However, as the company scales up, employees become entrenched in their existing workflows, and the growing workforce size significantly reduces overall acceptance of SaaS systems.

Second, the sharing of core medical resources will become a new direction for the industry.. As specialized healthcare service providers continue to replicate and expand their operations, they must not only focus on patient acquisition and traffic generation but also address how to train, retain, and serve the relatively scarce resource of physicians. This dynamic has created market opportunities for shared medical resources.

For example, United LiGe Second Medical Aesthetic Hospital, a chain brand in the medical aesthetics industry, has established a shared surgical center. By adopting an “asset-light” business model, the institution supports physicians in launching their own practices. Specifically, the hospital provides facilities such as laboratories, operating rooms, non-surgical treatment areas, and dental units, along with nursing staff, anesthesia services, and ward accommodations. This arrangement effectively offers physicians a venue for multi-site practice and comprehensive intraoperative support, while the hospital’s revenue is primarily derived from hourly fees charged to the physicians.

Third, for the private healthcare sector, medical service capabilities and expert resources will become increasingly important.. Taking Sanbo Brain Hospital, a specialized neurology chain medical group, as an example, its flagship hospital is Sanbo Brain Hospital Affiliated to Capital Medical University. In the rankings of medical service capabilities published by the Beijing Municipal Health and Family Planning Commission, this hospital has consistently ranked among the top in neurosurgery alongside Tiantan Hospital and Xuanwu Hospital for many consecutive years.

In terms of its expert team, Sanbo Brain Hospital boasts renowned neurology specialists such as Luan Guoming, Yu Chunjiang, Shi Xiang’en, Wang Baoguo, Yan Changxiang, Wu Bin, Lin Zhixiong, and Fan Tao. Unlike other private hospitals in the industry, Sanbo Brain Hospital adopts the model of an “academic-style private hospital.” In other words, it has established a systematic talent development mechanism that allows physicians to pursue unrestricted academic growth, providing robust support in areas such as research project initiation, funding applications, and professional title evaluations.

Fourth, market recognition and trust in premium brands will continue to strengthen.As previously mentioned, public trust in public hospitals in China is significantly higher than that in private hospitals. Therefore, for specialized private healthcare service providers, prioritizing brand building will foster sufficient patient trust.

However, prioritizing brand building involves more than just marketing and promotion; it also encompasses high-quality service experiences and medical standards. Excessive marketing not only fails to generate positive word-of-mouth and a strong brand reputation but can also instill insecurity in patients, thereby eroding their trust.

Fifth, high-quality players will also emerge in even more specialized or niche medical specialty service sectors.. In fields such as pediatric dentistry, rehabilitation, otorhinolaryngology and ophthalmology, and dermatological aesthetic medicine, there is still significant room for improvement in patient education. Under these circumstances, offering segmented and precise positioning while ensuring the quality of medical services and patient experience can effectively capture the corresponding customer base.

For example, in the burn and scald rehabilitation sector, which features relatively low-frequency and niche demand, clinics in the market are predominantly internal medicine or general practice clinics. Due to constraints such as staffing quotas, hospitals often categorize this specialty under “General Surgery.” In hospitals with more specialized burn care capabilities, such as West China Hospital and Shanghai Ruijin Hospital, “Burns and Plastic Surgery” departments have been established, integrating burn treatment with medical aesthetics. Consequently, there is currently a lack of specialized institutions for the diagnosis and treatment of burns and scalds in the market.

Amid such market opportunities, Wenlan Medical has adopted a differentiated strategy, focusing on enhancing service quality, operational efficiency, and patient convenience. By concentrating on the burn rehabilitation sector, it has established an integrated diagnosis, treatment, and service system encompassing offline clinics, telemedicine platforms, and the research, development, and sales of burn-specific pharmaceuticals. To date, more than ten facilities have been opened, with the flagship store in Suzhou serving approximately 50 to 70 patients daily.

From the golden age of financing in the specialized medical services sector in 2015, to the relative silence in the capital markets in 2019, and the subsequent slowdown in development amid the COVID-19 pandemic in 2020,Private specialized medical service providers are undergoing adjustments to adopt new models and business formats.This has also injected new momentum into the development of the industry.

The listing of Hygeia Healthcare, along with the financing rounds for Sanbo Brain Hospital and “Haoyunbang,” are all demonstrating to the market the immense potential of specialized medical service enterprises. As healthcare reform continues to deepen, and as the overall living standards of the Chinese people continue to rise—accompanied by greater emphasis on and investment in health—we firmly believe that an increasing number of companies in the specialized medical services sector will emerge with revenues in the tens of billions and market capitalizations in the hundreds of billions, akin to Aier Eye Hospital.