The Golden Age of Medical Devices: The Rise of Local Innovation

In recent years, domestic medical device innovation has risen rapidly. The primary market has seen the emergence of unicorn companies such as United Imaging Healthcare, Venus Medtech, and MicroPort CardioFlow. In the secondary market, Mindray’s market capitalization has exceeded RMB 300 billion, while Chunli Medical’s stock price has surged more than tenfold over two years. These developments seem to herald the arrival of a golden age for Chinese-made medical devices.

So, what stage is China’s medical device industry currently at? What changes have occurred in China’s medical device industry over the past 40 years? What insights do the high-performing pharmaceutical stocks on the U.S. stock market offer for domestic investment? Which sub-sectors within the medical device industry hold greater promise for future development?

In April 2019, Haitong Securities released a report titled “The Golden Age: The Dawn of China’s Medical Device Innovation Wave,” proposing the concept of a “golden age” for medical devices and sparking industry-wide discussion. Now, following continuous research and analysis, Haitong Securities has published a new report titled “The Golden Age of Medical Devices: The Rise of Local Innovation,” addressing the aforementioned questions.

The report states:

1. In emerging medical device sectors, such as TAVR, early screening for colorectal cancer, bioresorbable stents, and ventricular assist devices (artificial hearts), domestic companies have obtained regulatory approval ahead of foreign competitors, securing a dominant market position. This suggests that domestic products are likely to dominate the future incremental growth of China’s medical device market.

2. In the traditional medical device sector, domestic manufacturers are gradually making breakthroughs in the high-end market. The substitution rate for domestically produced products is continuously increasing in areas such as PET-CT, high-end color Doppler ultrasound, chemiluminescence immunoassay, high-end patient monitors, and orthopedic joint devices. The replacement of imported devices with domestic alternatives in China's existing medical device market has begun to undergo a qualitative change.

3. The Chinese medical device industry is undergoing profound changes, with the rapid rise of domestic innovation and the advent of a golden age for investment in China’s medical device sector.

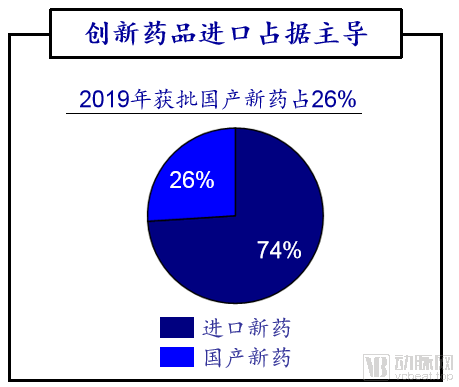

In the field of innovative drugs, foreign companies dominate. In 2019, the National Medical Products Administration (NMPA) approved a total of 53 new drugs, among which 39 were imported and only 14 were domestically produced, accounting for 26.4% of the total.

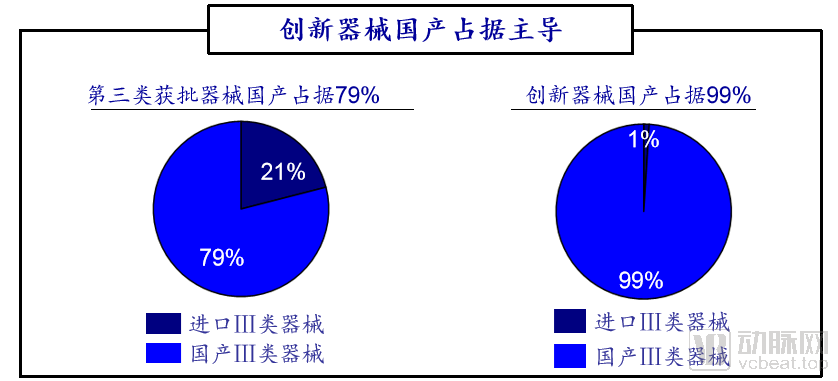

In contrast to pharmaceuticals, the innovative medical device sector is dominated by domestic enterprises. In 2019, a total of 1,335 Class III medical devices, which are characterized by high technological content, received approval; among these, 1,055 were domestically produced, accounting for 79.0%. Since the launch of the Special Review Procedure for Innovative Medical Devices in 2014, a total of 73 innovative medical devices had been approved by the end of 2019, with 72 being domestically produced, representing 98.63%.

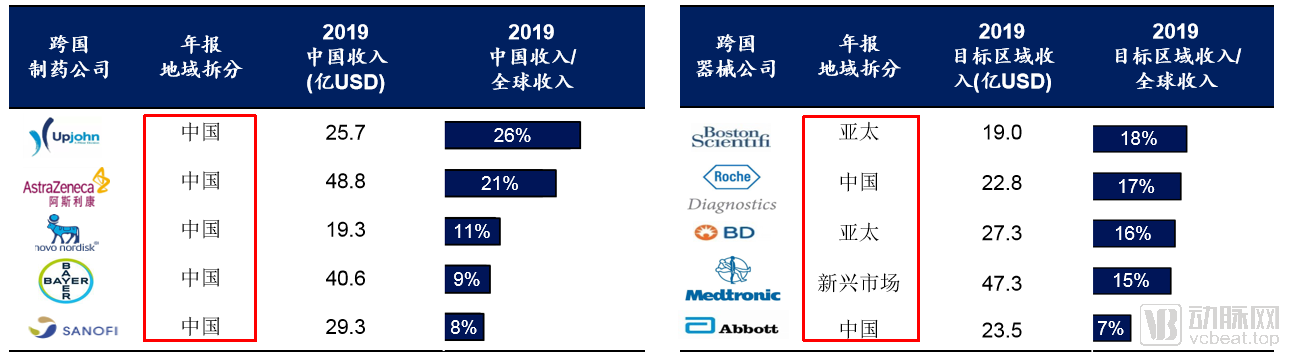

From a revenue perspective, it is also evident that the operating environment for domestic medical device companies is favorable. Multinational pharmaceutical companies have demonstrated strong performance in China; for instance, Pfizer Upjohn and AstraZeneca derived 26% and 21% of their global total revenues from their China operations, respectively. In contrast, the China business accounts for a relatively small proportion of multinational medical device companies’ overall operations. Some device manufacturers do not even disclose China-specific revenue separately, instead reporting it collectively as part of the Asia-Pacific region or emerging markets. Among major multinational medical device corporations, Haitong Securities estimates that Medtronic’s revenue from China accounts for less than 10% of its total (with emerging markets contributing 15%).

China Revenue of Multinational Pharmaceutical and Medical Device Companies

In specific medical device segments, domestic companies are accelerating their growth. For instance, in the chemiluminescence segment, Chinese firms such as Mindray and Autobio achieved revenue growth rates in 2019 that far outpaced those of IVD giant Roche (<10%). United Imaging Healthcare has also broken import monopolies in high-end MRI and PET-CT systems, beginning to capture market share previously held by multinational medical device corporations.

In summary, compared with pharmaceuticals, the development opportunities and environment in China’s medical device sector are more favorable.

The development of Chinese medical device companies can be roughly divided into three stages. In the first stage, domestic enterprises represented by Mindray Medical, Autobio Diagnostics, and Maccura Biotechnology started as distributors, then transitioned to independent research and development (R&D), with their products gradually moving from the low-end to the high-end market.

Phase II: In alignment with the strategy of domestic substitution, Chinese companies such as Lepu Medical and MicroPort Medical have focused on the research and development of high-tech medical devices, competing with multinational corporations for market share in China.

Phase III: Domestic enterprises represented by Venus Medtech, MicroPort Endovascular, United Imaging Healthcare, and Nanwei Medical have pursued independent R&D and local innovation, with some original Chinese-made products even achieving a leading position globally.

Innovation is the core of China’s medical device industry development, and R&D investment determines the ceiling for market capitalization. For example, Mindray Medical, the top-ranked Chinese medical device company, spent over RMB 1.6 billion on R&D in 2019, with cumulative R&D investment exceeding RMB 10 billion. Its current market capitalization has surpassed RMB 300 billion.

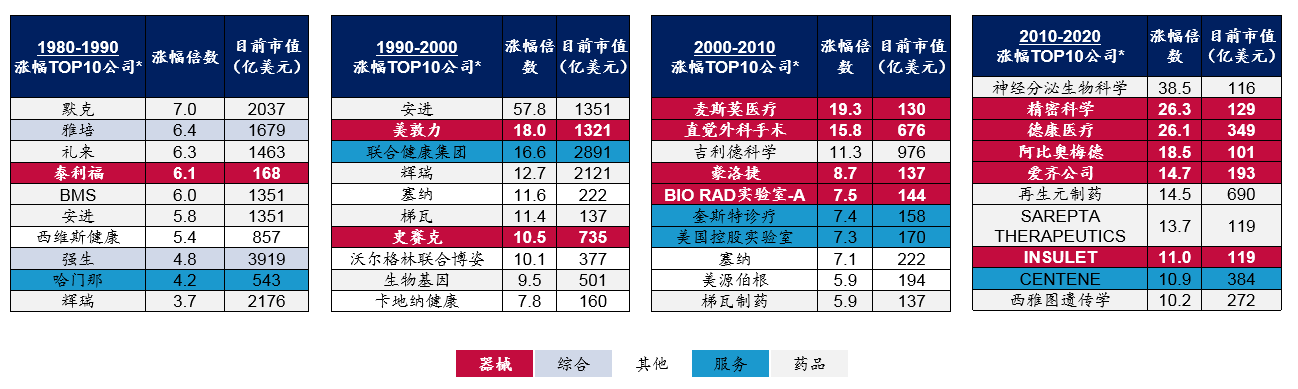

U.S. pharmaceutical companies are more mature than their A-share counterparts, and the development trends of U.S. healthcare stocks offer valuable insights for the A-share market. Since 1980, medical device companies have increasingly dominated the top ten best-performing stocks in the U.S. healthcare sector. In 2010, the top ten gainers included notable device manufacturers such as Exact Sciences, Dexcom, Abiomed, Align Technology, and Insulet.

Top 10 U.S. Pharmaceutical Companies by Stock Price Growth from 1980 to Present

It is foreseeable that many giants will also emerge among Chinese medical device companies in the future. So, which niche sectors are more likely to give rise to such industry leaders? Haitong Securities believes that large-scale market segments tend to produce companies with high market capitalizations.

According to the report “Evaluate MedTech, World Preview 2018, Outlook to 2024” published by the global consulting firm Evaluate, IVD, cardiovascular, imaging, orthopedics, and ophthalmology are among the sectors with the largest global market sizes.

Evaluate MedTech, World Preview 2018,Outlook to 2024

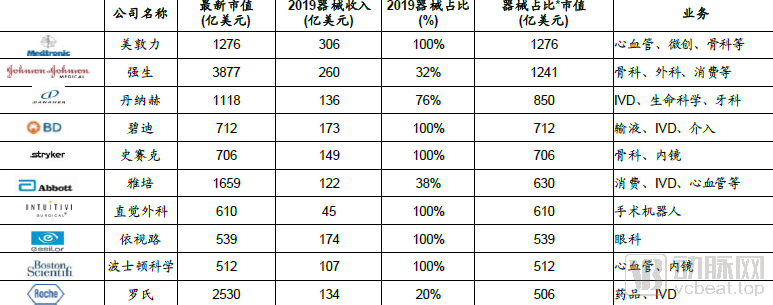

The top 10 medical device companies by global market capitalization also concentrate their core businesses in areas such as cardiovascular care, orthopedics, and in vitro diagnostics (IVD), which corroborates the view that large-scale sectors are more likely to produce high-market-cap companies.

Business Segments of the Top 10 Global Medical Device Companies by Market Capitalization

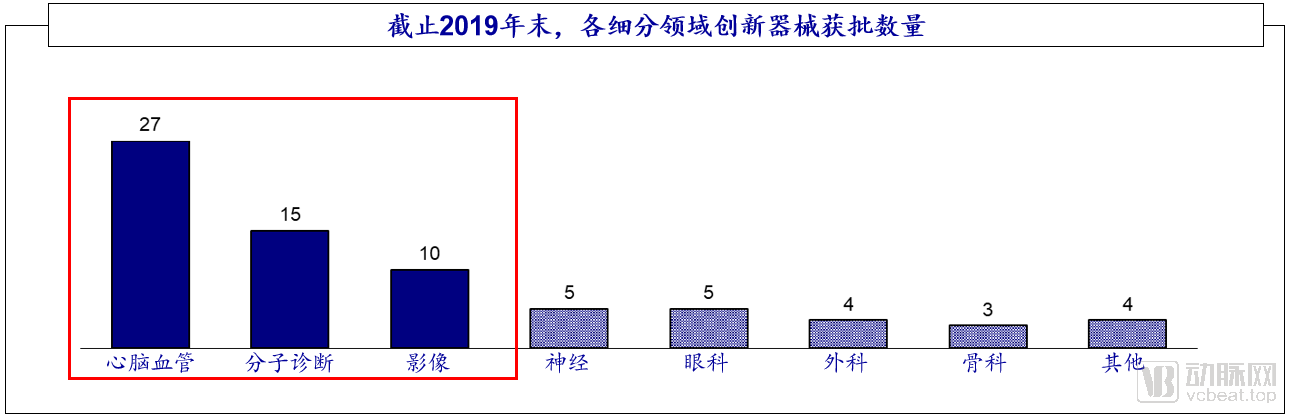

From another dimension, in terms of innovation activity, the fields of cardiovascular and cerebrovascular health, molecular diagnostics, and medical imaging in China are highly active. Since the launch of the Special Review Procedure for Innovative Medical Devices by the National Medical Products Administration in 2014, a total of 73 innovative devices had been approved by the end of 2019. Among these, 27 were cardiovascular and cerebrovascular devices, accounting for 37%; molecular diagnostic and imaging devices numbered 15 and 10 respectively, representing 21% and 14%. Other fields included neurology (7%), ophthalmology (7%), surgery (5%), and orthopedics (4%).

Therefore, Haitong Securities believes that there will be significant growth opportunities in fields such as in vitro diagnostics (IVD), cardiovascular care, orthopedics, and minimally invasive interventional therapy, making it an opportune time to invest in medical device companies operating in these sectors.

Minimally Invasive Interventional Therapy

Minimally invasive surgery is one of the major directions of surgery in the 21st century, reducing traditional large surgical incisions of tens of centimeters to small incisions of a few centimeters, greatly reducing postoperative pain for patients and shortening their recovery time.

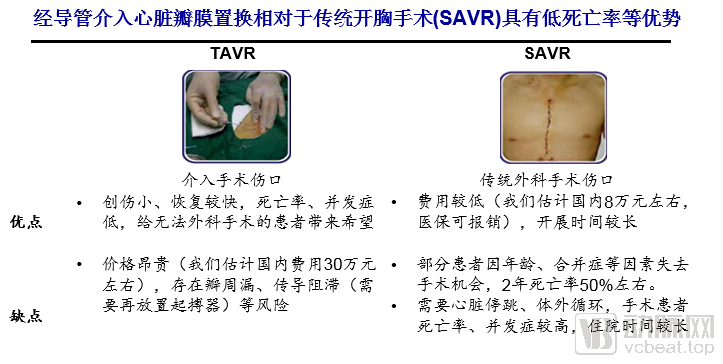

PCI (Percutaneous Coronary Intervention) is a representative minimally invasive interventional therapy, sparing patients the risks and suffering associated with traditional open-chest coronary artery bypass grafting. Transcatheter heart valve replacement is another minimally invasive interventional approach that offers advantages over traditional open-heart surgery, including reduced trauma, faster patient recovery, and lower rates of mortality and complications.

Minimally invasive interventional therapy is a disruptive innovation that will bring about significant changes to the industry and harbor substantial development opportunities.

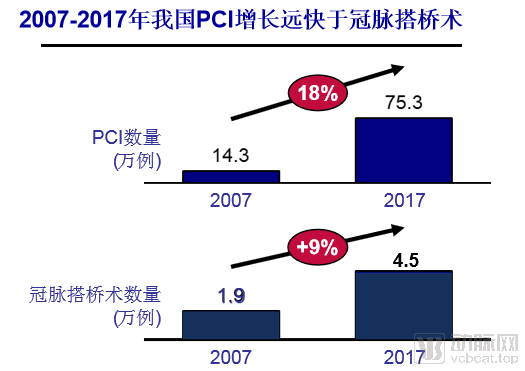

Minimally invasive interventional therapies have developed rapidly. In 2007, China performed a total of 143,000 percutaneous coronary intervention (PCI) procedures, compared with 18,000–20,000 coronary artery bypass grafting (CABG) surgeries during the same period. According to the Report on Cardiovascular Diseases in China, a total of 753,000 PCI procedures were performed nationwide in 2017. Meanwhile, the 2017 White Paper on Cardiac Surgical Procedures and Extracorporeal Circulation Data in China reported 45,000 CABG surgeries during the same year. The growth rate of PCI has been significantly faster than that of CABG. The rapid increase in the volume of minimally invasive interventional procedures has enhanced the market penetration of related medical devices, cultivated the market, and laid the foundation for the subsequent boom in the minimally invasive interventional therapy market.

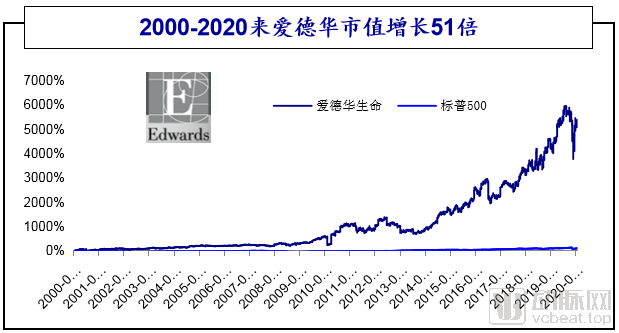

Prior to 2007, Edwards Lifesciences primarily focused on heart valves and cardiac critical care. The company’s major turning point occurred in 2007 with the European launch of its disruptive transcatheter heart valve, the Edwards SAPIEN, after which it entered a phase of rapid growth. With the introduction of the second- and third-generation transcatheter heart valves, SAPIEN XT and SAPIEN 3, and the gradual expansion of transcatheter aortic valve replacement (TAVR) to patients with severe aortic stenosis at intermediate surgical risk, the company’s transcatheter aortic valve revenue experienced explosive growth, driving a continuous rise in its market capitalization. Since 2000, Edwards Lifesciences’ market capitalization has grown from $850 million to $43.99 billion, representing a 51-fold increase. The success of Edwards Lifesciences demonstrates that minimally invasive interventional therapies also hold significant growth opportunities in China.

In minimally invasive interventional therapy, devices such as cardiovascular stents, transcatheter heart valves, endoscopes, and balloon catheters are all essential equipment for performing minimally invasive interventional procedures, and they also represent key areas of innovation for domestic manufacturers.

System Integration

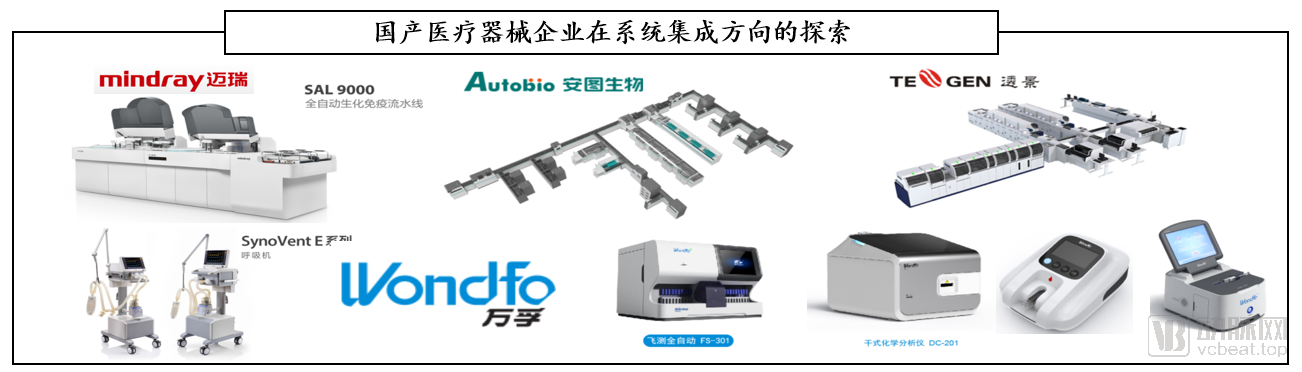

System integration is also a key direction for innovation, with Chinese medical device companies actively exploring this area. Examples include Autobio’s Autolas A-1 Series fully automated laboratory track system, Mindray’s SAL 9000 fully automated biochemistry and immunoassay track system, Lifeome’s fully automated high-throughput immunoassay system, Mindray’s integrated ICU solution, and Wondfo’s “One-Square-Meter Laboratory” concept, which combines several instruments such as its immunofluorescence platform, electrochemical blood gas analyzers, coagulation analyzers, and interference-free biochemistry analyzers.

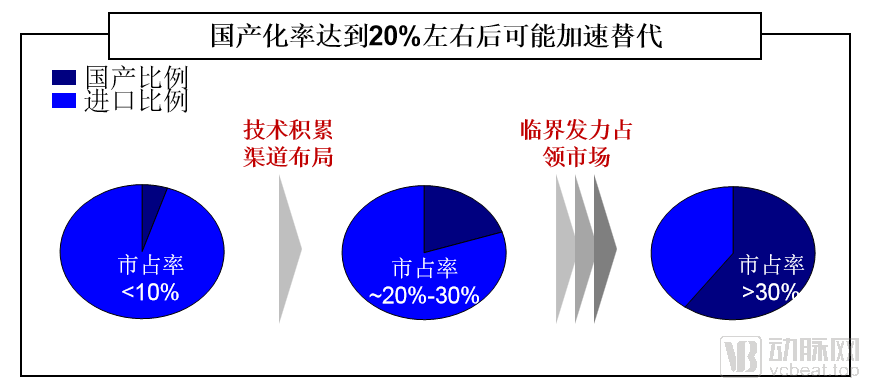

Haitong Securities believes that once the domestic market share of a certain type of medical device reaches 20%-30%, import substitution may accelerate.

The phase of achieving 0–10% domestic production rate is often a process of technological accumulation and channel development. When the domestic share reaches the critical range of 20–30%, it indicates that domestic technologies and distribution channels for such medical devices have established a solid foundation. Driven by external catalysts such as policy support, market penetration will accelerate, potentially enabling a rapid transition from 30% to over 50% in domestic substitution.

Currently, the market share of chemiluminescence instruments has exceeded 20%, but that of reagents remains below 20%. Amidst COVID-19 antibody testing and the downward pricing trend for chemiluminescence reagents, accelerated substitution may occur. In addition, the domestic production rate of medical devices such as carotid artery stents, distal protection devices, peripheral vascular stents, and intracranial vascular stents is approximately 20%, placing them at the tipping point of explosive growth. It is expected that these products will experience accelerated import substitution in the near future.

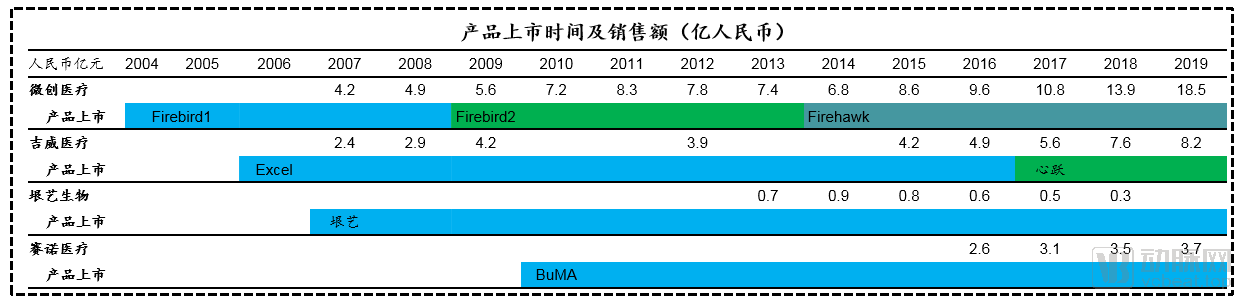

In the field of cardiac stents, since MicroPort released its first-generation product in 2004, its sales revenue has grown rapidly, reaching RMB 1.85 billion by 2019. Companies such as Jiwei Medical, Yinyi Biological, and Sino Medical also launched their respective products in 2006, 2007, and 2010. As the market expanded, the sales revenues of these companies continued to rise, generating substantial profits for them.

Launch Dates and Sales Revenue of Cardiac Stent Products

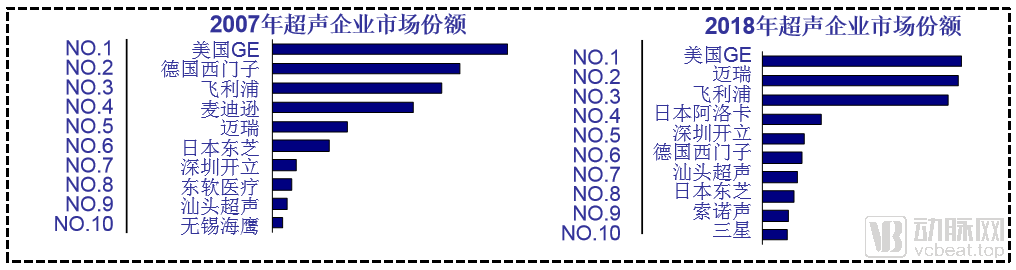

Unlike the cardiac stent sector, market share in the ultrasound industry is gradually concentrating among leading enterprises. In 2007, the domestic ultrasound market was predominantly dominated by foreign companies such as GE, Siemens, Philips, and Medison, while Chinese manufacturers including Mindray, Sonoscape, Neusoft Medical, Shantou Ultrasound, and Wuxi Haiying intensified their efforts to capture market share. By 2018, GE, Mindray, and Philips collectively accounted for nearly 60% of the domestic ultrasound market share, exceeding the combined share of all other competitors.

Comparison of Market Share Among Ultrasound Companies

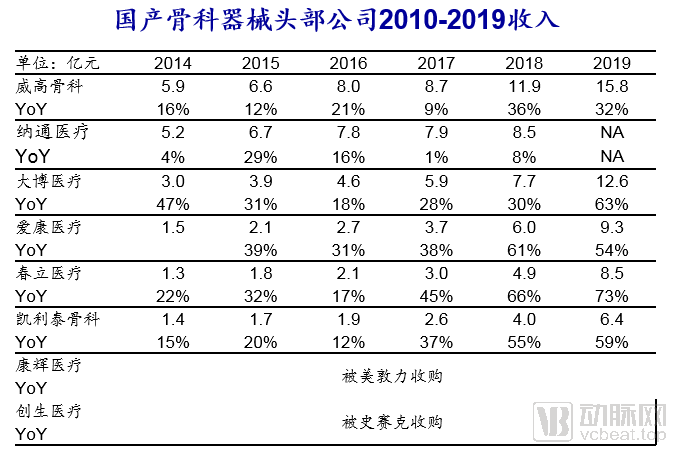

In the orthopedic sector, leading Chinese orthopedic device manufacturers have achieved steady and rapid growth. Companies such as Weigao Orthopaedics, Nato Medical, Double Medical, AK Medical, Chunli Medical, and Kindly Orthopaedics maintained annual revenue growth rates of approximately 10%–30% from 2010 to 2017. Since 2018, their revenue growth rates have risen to around 50%–70%, indicating robust corporate expansion.

Finally, Haitong Securities recommends that medical device companies place greater emphasis on first-mover advantage. The reasons are as follows:

1. Medical devices have long life cycles, and first-mover advantages tend to accumulate;

2. Medical devices require iterative development, and first-mover companies possess more extensive experience;

3. For medical devices, especially high-value consumables, physicians have established usage habits;

4. Sales channels established by medical device companies hold greater value.