Breaking the Sustainability Bottleneck: How Huimin Insurance Achieves Long-Term Viability Amid Multi-City Expansion and Strong Coverage Push

Recently, inclusive "Huimin Bao" (city-specific supplemental medical insurance) has emerged as a star product in the commercial health insurance sector. Cities such as Guangzhou, Nanjing, Huizhou, Zhuhai, Foshan, and Chengdu have successively launched their own Huimin Bao plans, with Nanjing and Guangzhou subsequently releasing claims reports for these schemes.

According to reports, Nanjing’s “Huimin Jiankang Bao,” with an annual premium of RMB 49, processed a total of 3,185 claims during its first year of operation, with total payouts approaching RMB 14.2 million. Public data from Guangzhou shows that since the launch of “Guangzhou Huimin Bao” at the end of 2019, there were 277 claim notifications filed in the first three months of operation, with the highest single claim payment amounting to RMB 35,000.

On June 30, 2020, the annual enrollment period for individuals and enterprises in Chengdu’s inclusive insurance product, “Hui Rong Bao,” came to an end. Data from the Chengdu Healthcare Security Administration shows that more than 3.1 million Chengdu residents enrolled during the 55-day enrollment window. This marks a significant explosive growth in inclusive insurance, suggesting that this new type of health insurance may have reached a turning point, rapidly transitioning from a market education phase to a market expansion phase.

In this article, VCBeat examines existing “Huimin” insurance products and interviews seasoned industry practitioners to explore three key questions: What is Huimin insurance? Why does society need this type of coverage? And where is it headed in the future?

Compared with general commercial health insurance, Huimin Insurance mainly reflects its inclusiveness through low purchase thresholds, low prices, and broad underwriting criteria. After a brief review of the Huimin Insurance products launched in various regions, VCBeat found that these insurance products differ in terms of participating entities, coverage for pre-existing conditions, premium pricing, and reimbursement scope, while sharing key commonalities such as low premium pricing and a wide range of insured individuals.

Comparison of Three Types of Commercial Health Insurance

Specifically, Huimin Insurance differs from existing commercial health insurance products, such as critical illness insurance and million-yuan medical insurance, in terms of the insured population, coverage methods, scope of coverage, premium pricing, and rules for continuous enrollment. For instance, Huimin Insurance typically imposes no age limits or occupational requirements, with annual premiums generally priced below RMB 100, and premiums for continuous enrollees do not increase with age.

More importantly, in terms of coverage eligibility, Huimin Bao adopts an exclusion-based approach rather than an exhaustive listing method, thereby including more patients with pre-existing conditions. Guangzhou Huiminbao excludes two major categories of serious illnesses—specific malignant tumors and rare diseases—as pre-existing conditions, while providing coverage for patients with other types of diseases. In Chengdu, Huirongbao explicitly states that “individuals are eligible for enrollment regardless of whether they have pre-existing conditions or the nature of such conditions.”

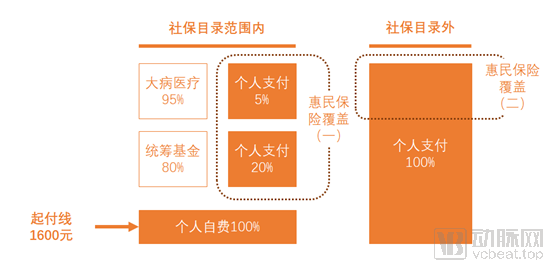

In terms of coverage, Huimin Insurance serves as a supplementary protection beyond the national basic medical insurance. Typically, Huimin Insurance defines two categories of coverage: medical expenses within the scope of basic medical insurance, and costs for specific high-cost drugs. Taking Huirongbao as an example, its covered liabilities include the out-of-pocket portion of medical expenses incurred at medical institutions after basic medical insurance reimbursement, as well as the costs of drugs purchased at designated hospitals and pharmacies that fall within the payment scope of the "Huirongbao Specific High-Cost Drug List," as illustrated in the figure below.

Display of Coverage Scope for Huimin Insurance (Using Guangzhou as an Example)

Since Shenzhen launched its government-backed critical illness insurance in 2015, Chen Mingdong, one of the designers of this insurance product, has witnessed the fluctuations in innovative practices of social-commercial integrated health insurance across various regions over the past few years. He has also personally participated in the design and operation of products at multiple key junctures during this period.

He told VCBeat that inclusive health insurance has a long history and has undergone rapid development and iteration, driven by multiple factors including the intensive rollout of supportive policies, an aging population, rising medical demands, and increasing pressure on the national basic medical insurance fund’s payout capacity. “In 2015, the Shenzhen Municipal Government promoted the launch of the Shenzhen Government Critical Illness Insurance, which features inclusive benefits and can be regarded as the beginning of inclusive health insurance. This year marks the sixth year of its operation, during which both annual premiums and coverage rates have significantly increased,” said Chen Mingdong. “Following Shenzhen, many other cities, including Nanjing, Guangzhou, Huizhou, Foshan, and Zhuhai, have also launched similar initiatives.”

In March 2020, the State Council issued the “Opinions of the Central Committee of the Communist Party of China on Deepening the Reform of the Medical Security System” (hereinafter referred to as the “Reform Opinions”), which clarified the overall “1+4+2” reform framework. It stipulated that by 2030, a multi-tiered medical security system should be fully established, with basic medical insurance as the mainstay, medical assistance as the safety net, and the coordinated development of supplementary medical insurance, commercial health insurance, charitable donations, and mutual medical aid, thereby defining the systematic role of commercial health insurance.

Meanwhile, the Reform Opinions proposed promoting complementary integration among various types of medical security, enhancing coverage for catastrophic illnesses and diverse healthcare needs, and standardizing and strengthening cooperation with commercial insurance institutions and social organizations in the innovation of medical insurance governance. This marks the first appearance of the concept of “social-commercial integrated health insurance” in a national-level policy document, establishing strategic direction from a top-level design perspective for the subsequent development of inclusive supplementary medical insurance (Huimin Bao).

From this positioning, the integration of social insurance and commercial insurance—two distinct types of coverage with different attributes—should be regarded as the core characteristic of Huimin Insurance. Chen Mingdong told VCBeat that prior to the emergence of Huimin Insurance, social insurance and commercial insurance were highly segregated, with government procurement of services serving as the primary form of governmental support for the development of commercial health insurance. In the innovative design and operational practices of Huimin Insurance across various regions, relevant government departments have often been able to provide abundant non-fund medical insurance resources, such as data, distribution channels, and promotional support. Consequently, Huimin Insurance, which possesses both policy-oriented and market-driven attributes, has become an intermediate form bridging traditional social insurance and commercial insurance.

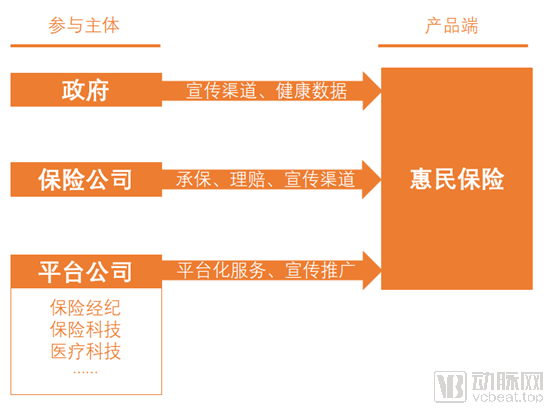

Compared with general commercial health insurance, Huimin Insurance features more diversified participating entities, typically involving three parties: the government, insurance companies, and platform companies, with their respective functions illustrated in the figure below.

Organizational Model of Huimin Insurance

The primary government entities involved in the design of inclusive health insurance are local healthcare security administrations. In addition to providing oversight and guidance, these agencies assist insurance companies or platform operators in product design and promotional campaigns. For instance, the Chengdu Healthcare Security Administration has explicitly stated that it will provide certain data support during the product design phase, contingent upon ensuring personal privacy protection and data security. Chen Mingdong told VCBeat that the boundaries of the healthcare security administration’s involvement in inclusive health insurance are clearly defined, and such insurance will not lose its market-oriented nature due to government endorsement.

For local governments, participating in the promotion of inclusive supplementary medical insurance serves a dual purpose. On one hand, it represents an innovative implementation of national directives to deepen healthcare security system reforms. On the other hand, it helps alleviate poverty caused by illness that falls outside the scope of basic, broadly covered public health insurance responsibilities. By leveraging market-based mechanisms to upgrade healthcare security, it reduces the payment burden on basic medical insurance and enhances residents’ awareness of both social and commercial insurance.

Underwriting and claims settlement are the primary responsibilities of insurance companies. Currently, both co-underwriting by multiple insurers and sole underwriting by a single insurer are widely adopted across various regions. Furthermore, during the enrollment period for Huimin Bao (city-specific supplementary medical insurance), insurance companies leverage their branch networks and channel resources for promotional activities. In the later claims settlement phase, insurers’ mature claims operation systems play a pivotal role in handling inquiries, processing documentation, and executing payouts. The emergence of Huimin Bao has provided insurance companies with new avenues for business growth.

The structure and functions of platform companies are relatively complex. Chen Mingdong stated that insurance brokerage firms, insurtech companies, and health-tech companies are all attempting to establish platform companies, with the current mainstream model being the construction of a platform service system centered around insurance brokerages. “The agency sales of insurance products require specific licenses to ensure the lawful and compliant collection of premiums. Among the participants in platform companies, only insurance brokerage firms hold the financial qualifications issued by the China Banking and Insurance Regulatory Commission (CBIRC), making them the common initiators of such platforms,” Chen Mingdong explained.

Furthermore, as a new form of commercial health insurance, Huimin Insurance possesses dual financial and medical attributes, with the participation of medical technology companies serving as a critical link in connecting medical resources. A review of select Huimin Insurance policy terms by VCBeat revealed that some cities have set unreasonable deductibles for the reimbursement of out-of-pocket in-hospital expenses, rendering certain coverage clauses substantively ineffective; meanwhile, other cities have overlooked the risks associated with the onset and progression of diseases in clinical practice by offering comprehensive coverage, thereby causing underwriting losses for the insuring companies.

“Cost and risk control pose the greatest challenge to the operational teams of inclusive insurance products,” pointed out Chen Mingdong. In the past, commercial insurers primarily relied on accumulated experience from previous projects to enhance their risk control capabilities. Without the support of a professional medical team during insurance product design and the selection of healthcare service providers, it is difficult to transition from fragmented medical services to a coverage model that aligns with the genuine clinical needs of patients and physicians, thereby making it challenging to effectively manage the quality, timeliness, standards, and processes of external providers.

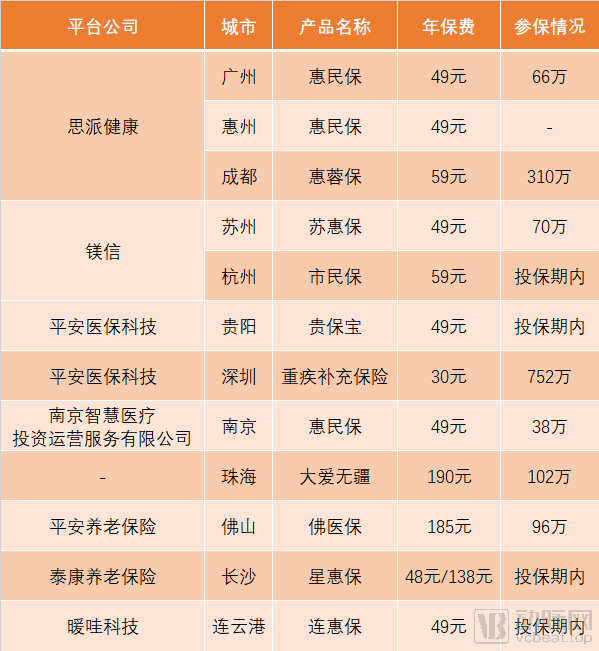

Statistics on City-Specific Supplementary Health Insurance Plans (Data as of Press Time)

Among the 12 cities that publicly announced enrollment information for their Huimin Bao (inclusive health insurance) schemes, Guangzhou, Huizhou, Chengdu, Suzhou, Hangzhou, Guiyang, and Nanjing all selected platform companies with medical backgrounds. Notably, Medbanks Network Technology and Magnesium Health served three and two cities, respectively, making them the platform companies with the highest level of participation in Huimin Bao initiatives.

In mid-2019, Chen Mingdong left a major domestic insurance technology company to join Medbanks Health. He shared with VCBeat insights into the continuous iteration of Medbanks Health’s inclusive insurance services in Guangzhou, Huizhou, and Chengdu. Chen told VCBeat that, overall, Medbanks Health’s practices demonstrate a trend shifting from underwriting by a single entity to multi-entity underwriting, from exclusion-based lists to comprehensive coverage for patients with pre-existing conditions, and from simple expense reimbursement to the integration of multiple value-added services.

In April 2020, the Chengdu Municipal Healthcare Security Administration issued the “Guiding Opinions on Promoting the Development of Health Insurance and Improving the Multi-tiered Medical Security System” (Cheng Yi Bao Fa [2020] No. 19). This was the first document in China to implement the State Council’s “Reform Opinions” regarding the strategic deployment of building a multi-tiered medical security system. In Chengdu, the Healthcare Security Administration boldly proposed piloting a new operational model for health insurance characterized by the separation of underwriting and operations, clear division of labor, balanced checks and constraints, and multi-party win-win outcomes. The aim was to expand the supply range of health insurance products and continuously enhance the precision and substance of health insurance coverage. The issuance of this policy undoubtedly provided stronger policy support for the development of inclusive insurance.

In Chengdu, Medbanks Health leverages the medical resources accumulated through its specialty pharmacy business under the Medbanks Group to provide key professional consulting on product design and operational management capabilities for local inclusive insurance products. Meanwhile, it integrates resources across the entire healthcare industry chain to build a comprehensive medical service system for participants in these inclusive insurance schemes. “For platform companies, specialized industry chain resources can become core competencies in product design and sales,” said Chen Mingdong.

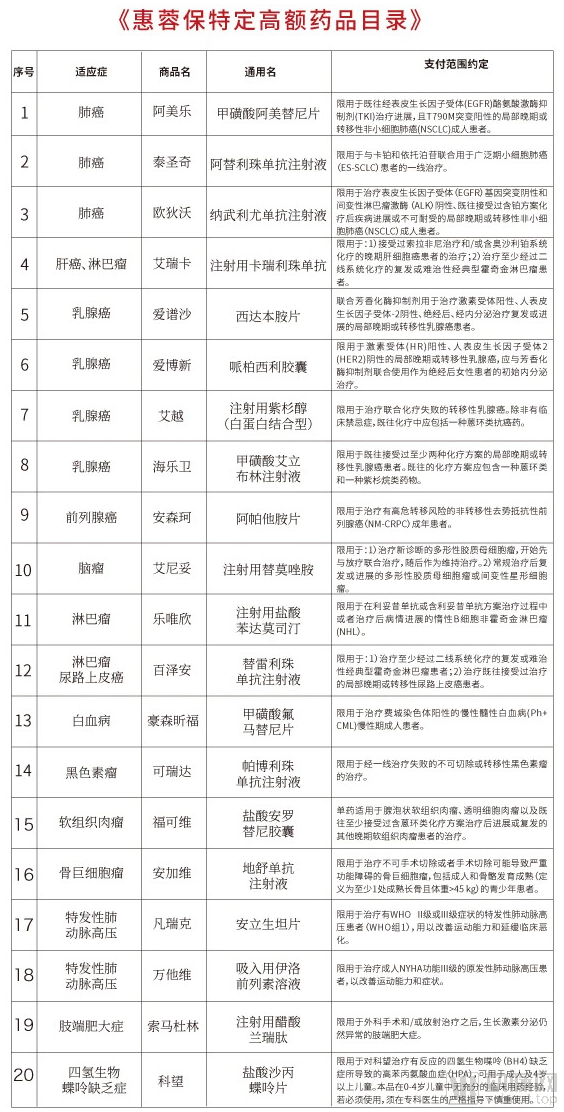

Taking the special high-cost drug list as an example, it is an indispensable component of the coverage scope of Huimin Bao (city-specific supplemental medical insurance), and also a vulnerable link where many Huimin Bao plans tend to lose control during subsequent operations. The design and updating of the special high-cost drug list reflect, to a certain extent, the operational team’s capability in managing risks and controlling costs.

Example of the Special Drug List (Taking Huirongbao as an Example)

Chen Mingdong told VCBeat that when designing the drug formulary, the team seeks expertise and resources from Medbanks’ pharmacy business line, taking into account factors such as the National Reimbursement Drug List, therapeutic efficacy, sustained drug supply capacity, adverse reactions, and cost-effectiveness, with dynamic adjustments made on an annual basis. “Breaking through the development bottlenecks of city-specific supplemental medical insurance (Huiminbao) is essentially a matter of integrating industry chains,” Chen stated. “Platform companies need to exert stronger control over pharmaceutical resources, including prescription review capabilities, as well as robust operational capabilities in insurance claims processing.”

Regarding the recent explosive growth of Huimin Insurance, Chen Mingdong also expressed his concerns: “If Huimin Insurance is treated merely as a short-term business highlight, it will quickly devolve into vicious market competition, and products lacking long-term operational planning will rapidly shrink.” In Chen Mingdong’s view, Huimin Insurance should prioritize expanding population coverage and ensuring sustainable, stable operations as its key objectives.

As for the potential that inclusive health insurance offers to practitioners in the commercial health insurance sector, Chen Mingdong stated that if overall operations run smoothly, inclusive health insurance could cover 300–500 million people in China. Based on an annual premium of RMB 100 per person, this would correspond to a market size of RMB 30–50 billion. However, the long-term stable operation of inclusive health insurance imposes stringent requirements on risk control and cost management. Moreover, several critical links require support from professional medical knowledge and resources; otherwise, product operations would be unsustainable, leading to detrimental impacts on the interests of the government, insurance companies, and patients alike.

Recently, another practitioner in the Huimin Insurance sector shared his insights on the future development of this new type of insurance with VCBeat. We have compiled these thoughts below, hoping to offer inspiration to more participants in the Huimin Insurance market.

First, to a certain extent, it is necessary to uphold public welfare and non-profit nature.

Huimin Insurance is a category of products deeply involved in design and underwritten by commercial insurance companies. This type of product is bound by an operator’s paradox: profitability cannot be the measure of its success or failure. It has been reported that in one city, the loss ratio for such a product in its first year was only 35%, approximately half that of commercial health insurance. This does not indicate successful product design or operations; on the contrary, such an outcome is regarded as a failure in implementation, posing a risk of discontinuation. Huimin Insurance, backed by local government support and benefiting from regional natural monopoly, must adhere to its policy-oriented, public-interest, and non-profit nature.

In cases where the annual loss ratio of a product is excessively low, the operational team of Huimin Insurance urgently needs to address public opinion, clarify the budget for project handling expenses and management profits, safeguard the product’s fund pool, provide compensation to disappointed policyholders, and seek understanding from industry peers who may be affected.

Second, at the outset of operations, the primary focus should not be on building and validating a profit model.

For commercial insurance companies and platform providers participating in inclusive supplementary medical insurance, excessively high profitability is often more perilous than low profitability or even losses. During the initial years of data accumulation and operational learning, the absence of annual losses may instead reflect deficiencies in a company’s capabilities and strategic planning. Specific practices by certain commercial insurers that embed implicit monetization channels directly into individual products should be addressed and regulated.

This practitioner argues that design or implementation details with greater potential to serve as covert monetization channels should be prioritized for immediate monitoring under the coordinated reform of healthcare, medical insurance, and pharmaceuticals (the “Three-Medical Linkage”) and broader health insurance reforms. Specifically, regarding the coverage of new and specialty drugs by supplementary commercial health insurance schemes for public benefit, a “centralized procurement plus negotiation” mechanism should be established promptly in accordance with strategic purchasing principles, so as to select drugs with high cost-effectiveness and reasonable price reductions for inclusion.

Third, inclusive health insurance must also strictly guard against fraud and deceptive claims.

He pointed out that inclusive supplementary medical insurance enjoys favorable timing and conditions, making it an ideal entry point for collaboration between basic medical insurance and commercial insurance to combat fraud and abuse. Specifically, at the current stage of the new healthcare reform and medical insurance system reform, payment reforms for inpatient and outpatient services are being advanced separately. Within the basic medical insurance framework, cost control can be effectively implemented for both scenarios. Since inclusive supplementary medical insurance covers reimbursement for both inpatient and outpatient expenses, whether within or outside the catalog, it should establish detailed review and management modules; otherwise, it will fall behind the concepts of the new healthcare reform.

Fourth, the exploratory phase of Huimin Insurance may be temporary

For insurance companies and platform providers participating in city-specific inclusive health insurance schemes, two critical issues must be clarified. First, how to establish long-term cooperative relationships with individual cities while ensuring that coverage rates and benefit levels meet established standards and comply with legal and industry regulatory requirements. Second, on what basis can the fragmentation of inclusive health insurance products be sustained over the long term between a given city and its neighboring regions? From the perspective of commercial insurance, prolonged fragmentation will inevitably lead to obsolescence. This implies that any competitive advantage derived from securing partnerships for inclusive health insurance in numerous local cities may only be temporary. Insurance companies and commercial health insurers must adopt a detached mindset and embrace change.

Fifth, in the future, Huimin Insurance may return to the track of medical insurance

Through open and candid collaboration within a specific period and phase, Huimin Insurance will achieve the following: the inevitable return to the medical insurance framework, the natural expansion into cross-regional operations, and the contingent promotion of commercial insurance development. Through this cooperation, basic medical insurance has broadened its pilot initiatives for implementing critical illness medical insurance and assistance programs, while commercial insurers have obtained valuable trial data aligned with their perceived value.

He believes that there is no essential difference in use value between Huimin Insurance and the large-sum and critical illness insurance components of the basic medical insurance system. In the future, once it achieves a mature scale and market recognition, it may be incorporated into the category of large-sum and critical illness insurance under the basic medical insurance framework. Furthermore, Huimin Insurance should gradually expand from first- and second-tier cities to pilot programs in impoverished areas, which will pose new challenges to the product design and operational capabilities of insurance companies and platform providers.