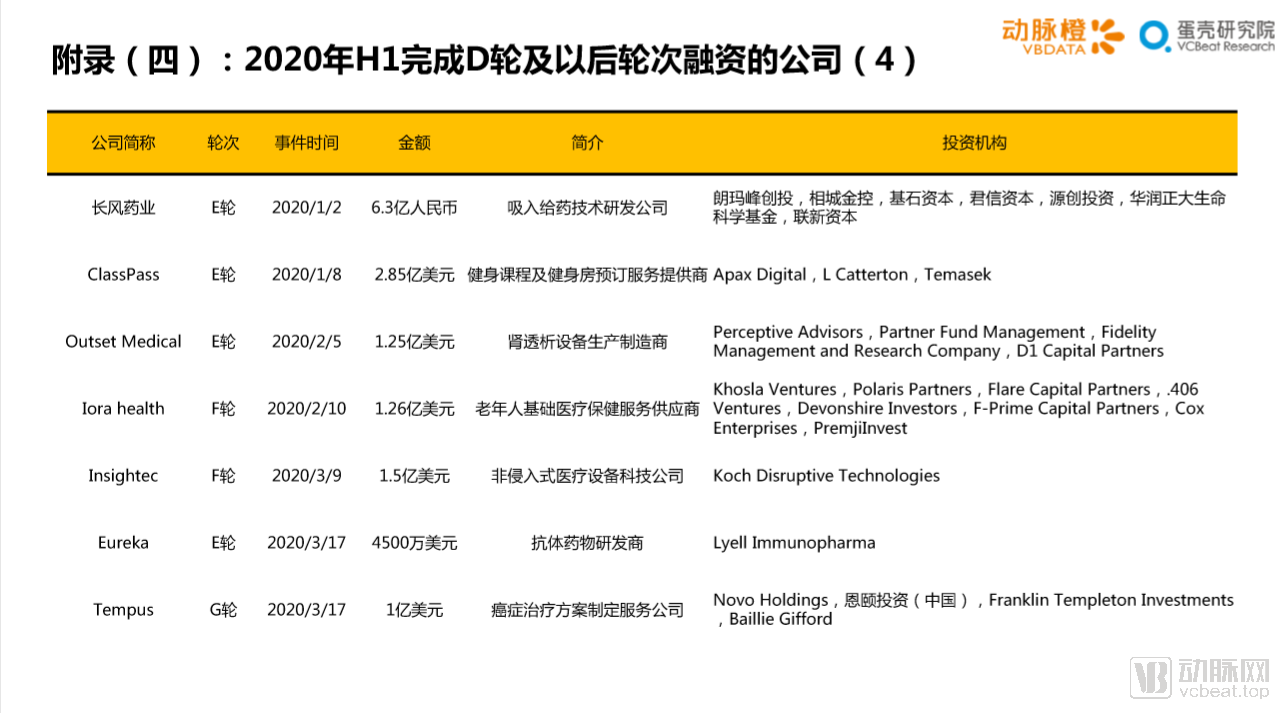

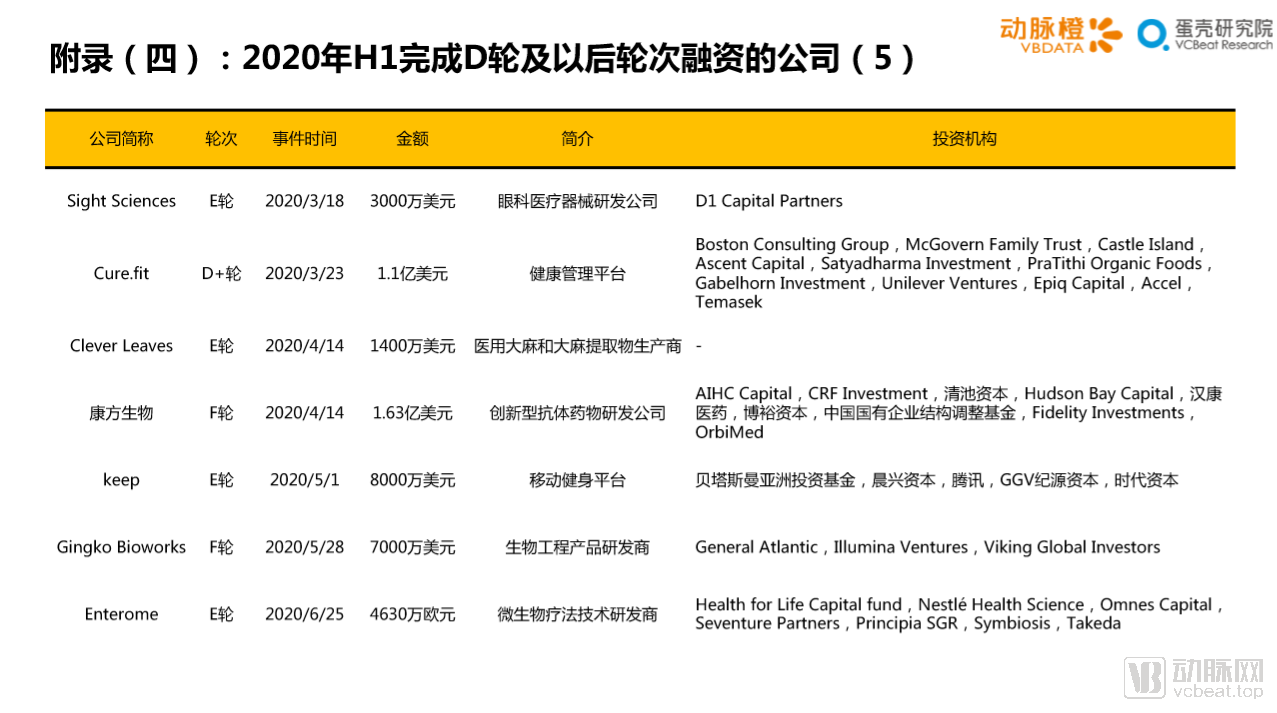

Global Healthcare Industry Capital Report H1 2020: Resilient Investment Amid Pandemic, Record IPOs, and Regional Shifts

I. Global Healthcare Financing Remains Active: In the first half of 2020, total global healthcare financing increased by 13% year-on-year. In China, while the total amount raised declined slightly, the number of financing deals dropped significantly by 36% year-on-year to 282, indicating a rise in capital concentration and greater difficulty for early-stage startups in securing funding.

II. The biopharmaceutical sector continues to maintain an absolute lead in both the number and volume of financing deals domestically and internationally; digital health is flourishing abroad, while the medical device and consumables sectors in China are showing strong momentum.

III. The pandemic has directly stimulated certain niche sectors in healthcare: global vaccine developers have accelerated their fundraising efforts, with mRNA technology gaining favor; overseas telemedicine concepts have heated up, driving simultaneous growth in both secondary and primary markets; in China, the in vitro diagnostics industry saw 39 financing deals totaling RMB 12.133 billion, already surpassing the full-year figures for 2019.

4. In terms of capital entry, GV, Khosla Ventures, and Sequoia Capital China were the most active investors in the first half of the year, with a total of 14 investments; regarding capital exit, among global investment institutions over the past decade, OrbiMed had the highest number of portfolio companies going public, while among domestic firms, CDH Investments’ portfolio companies delivered the most impressive IPO performance in the first half of this year.

V. Strong H1 2020 Performance in Healthcare IPOs: A-shares, U.S. stocks, and Hong Kong stocks saw 67 IPOs, raising over RMB 100 billion; the number of Chinese listed companies tripled quarter-on-quarter in Q2 2020.

6. China and the US Account for 91% of Global Healthcare Funding; Geographic Distribution of Healthcare Financing in China Is Shifting: Shanghai and the Yangtze River Delta Region Are Experiencing Robust Growth, Beijing Is Declining, and Guangdong Is Rising.

7. MGI Tech’s $1 billion financing round ranks it No. 1 globally in H1 2020 funding, with four Chinese companies making the list.

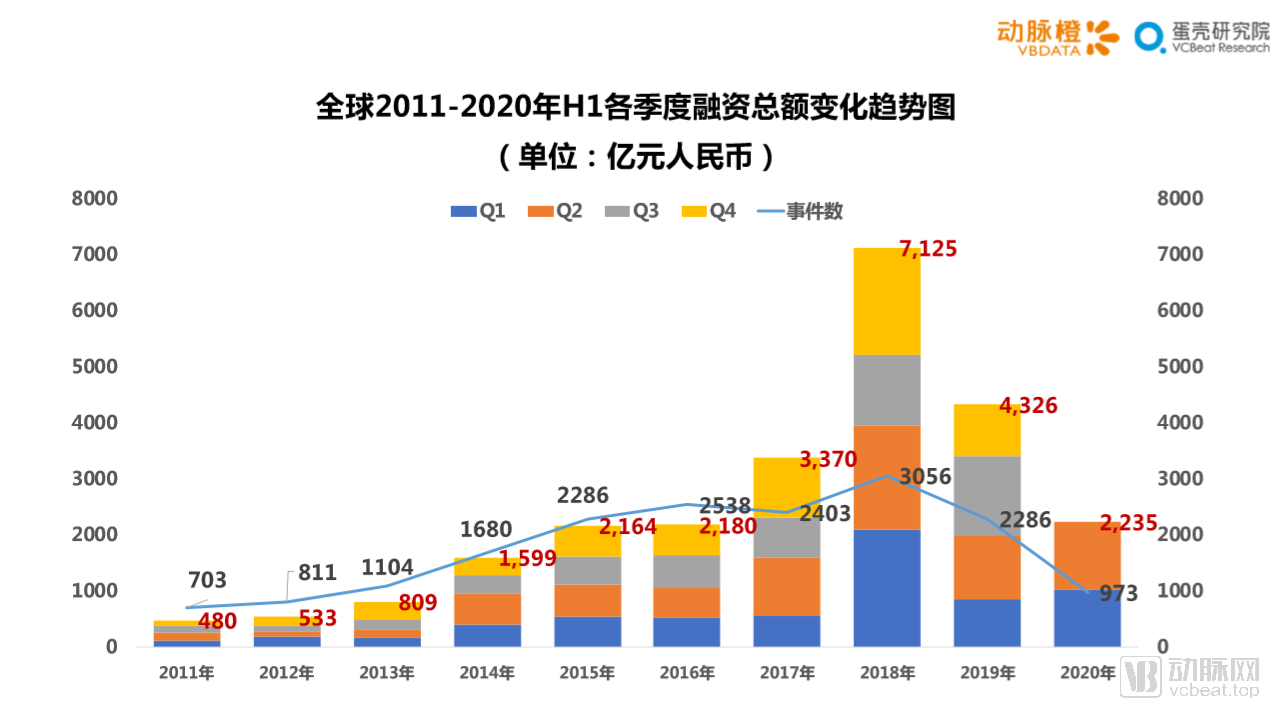

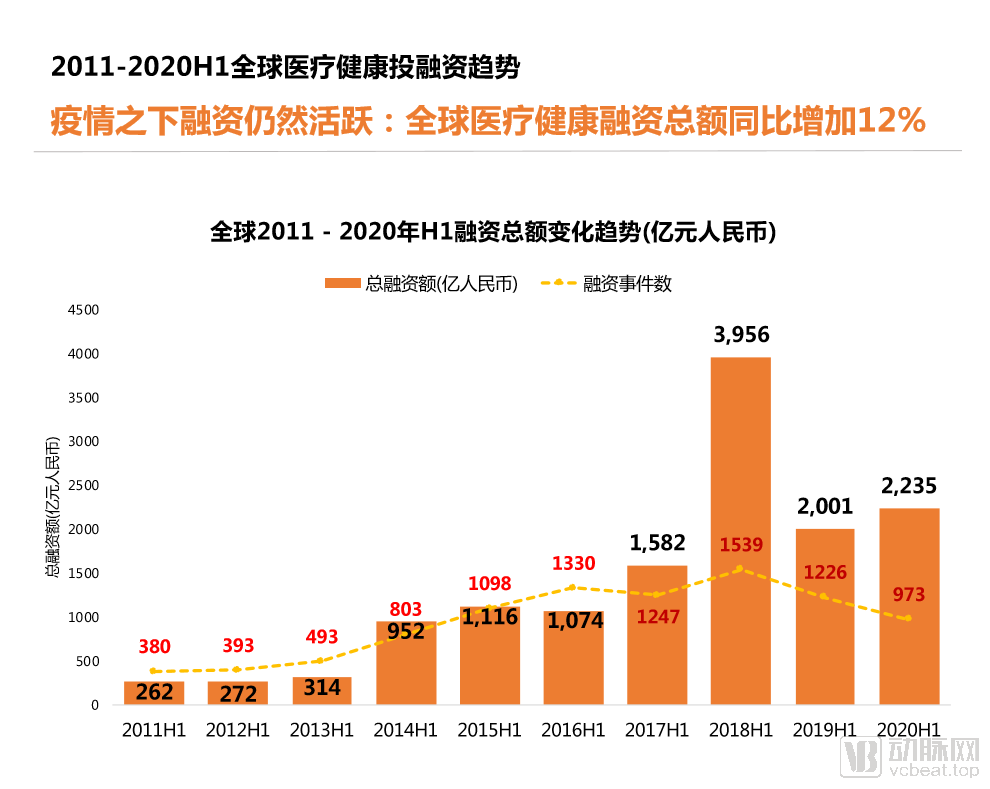

1.1 Financing in the Healthcare Industry Remains Active: Total Funding in H1 2020 Increased by 12% Year-on-Year

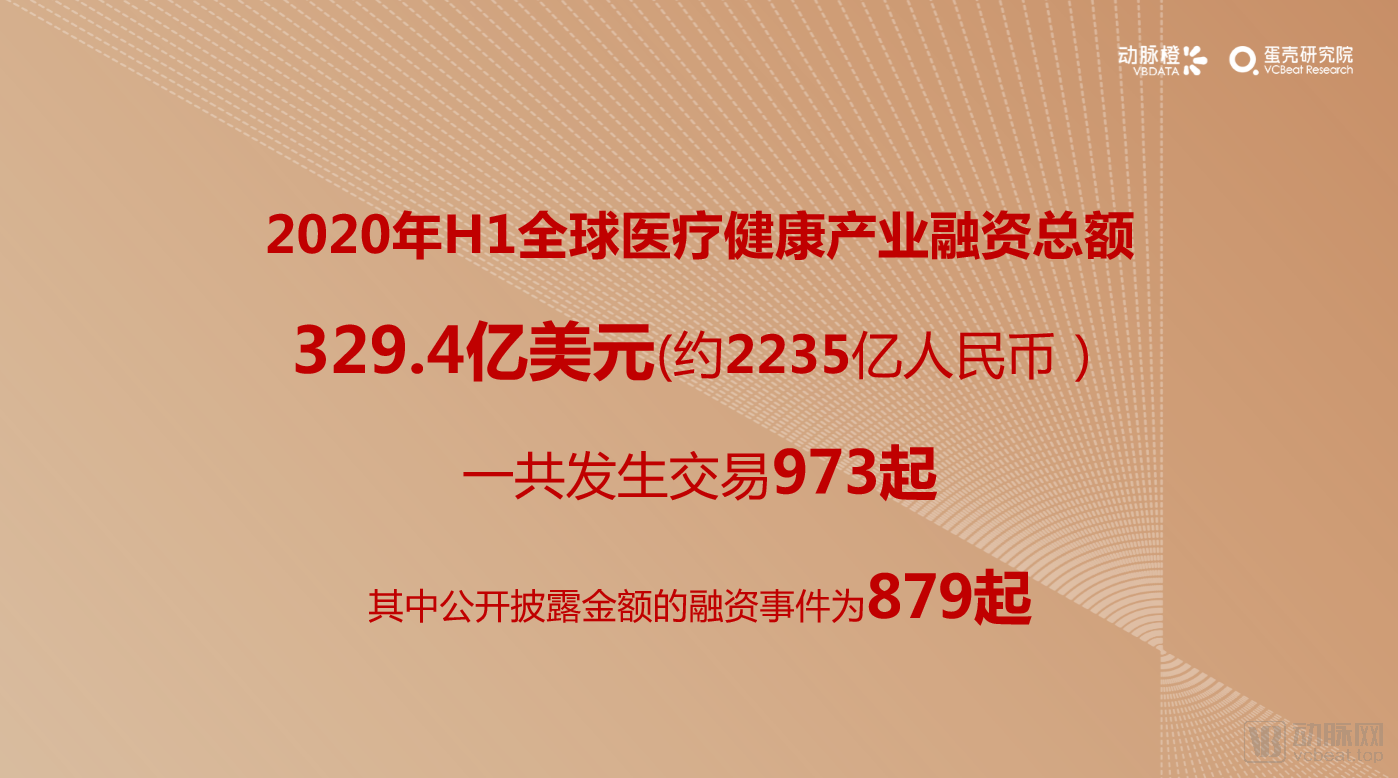

In the first half of 2020, a total of973 Financing Events(including 94 deals with undisclosed amounts), the total funding reached$31.85 billion(approximately RMB 223.5 billion),Financing amount increased by 12% year-on-year.

In the first half of 2020, a total of973 Financing Events(including 94 deals with undisclosed amounts), the total funding reached$31.85 billion(approximately RMB 223.5 billion),Financing amount increased by 12% year-on-year.

Although the total financing amount still increased year-on-year, the number of financing deals dropped to the lowest level in the first half (H1) of the past six years. The increased capital was distributed among fewer companies.This means that for most global healthcare startups, financing pressures increased in H1 2020.

However, the rise in the average financing amount per transaction also indicates that companies with strong capabilities and solid technical foundations can secure funding more smoothly.

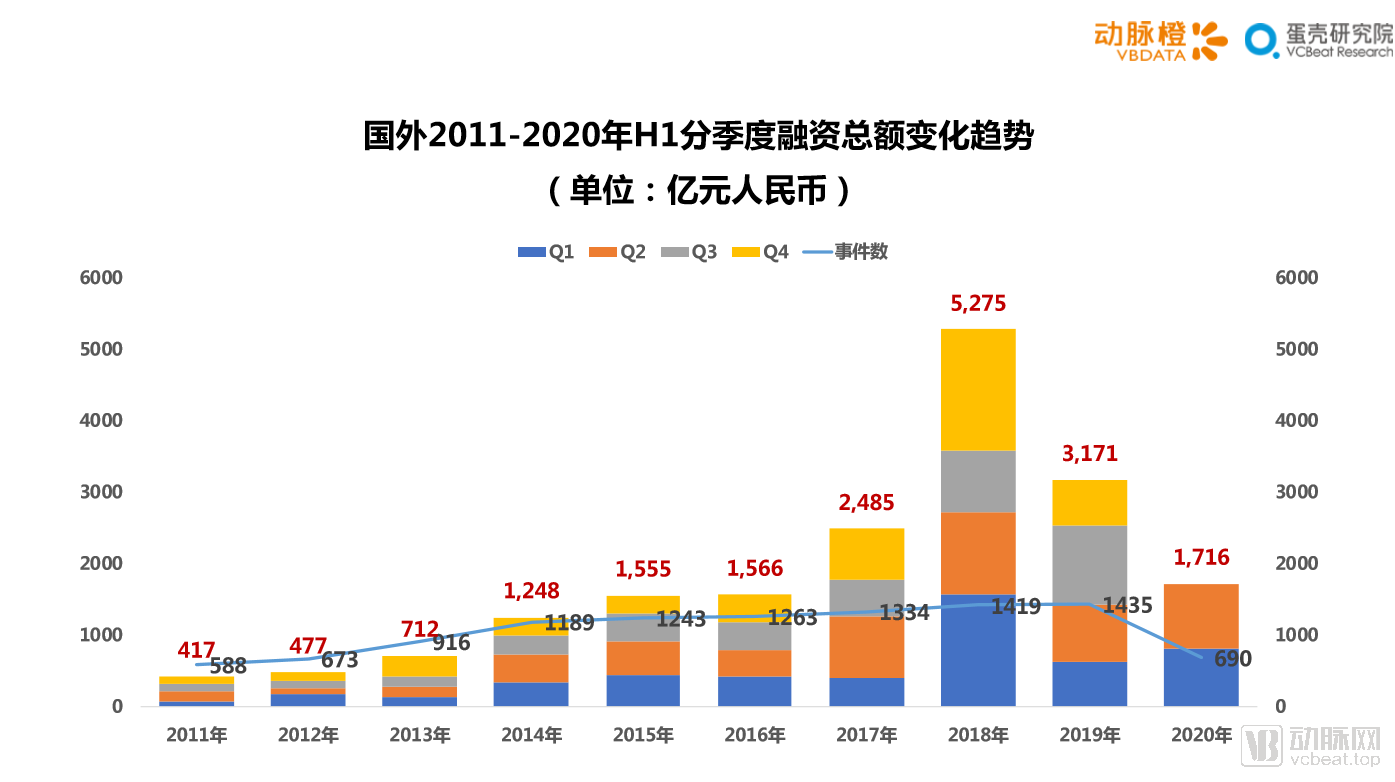

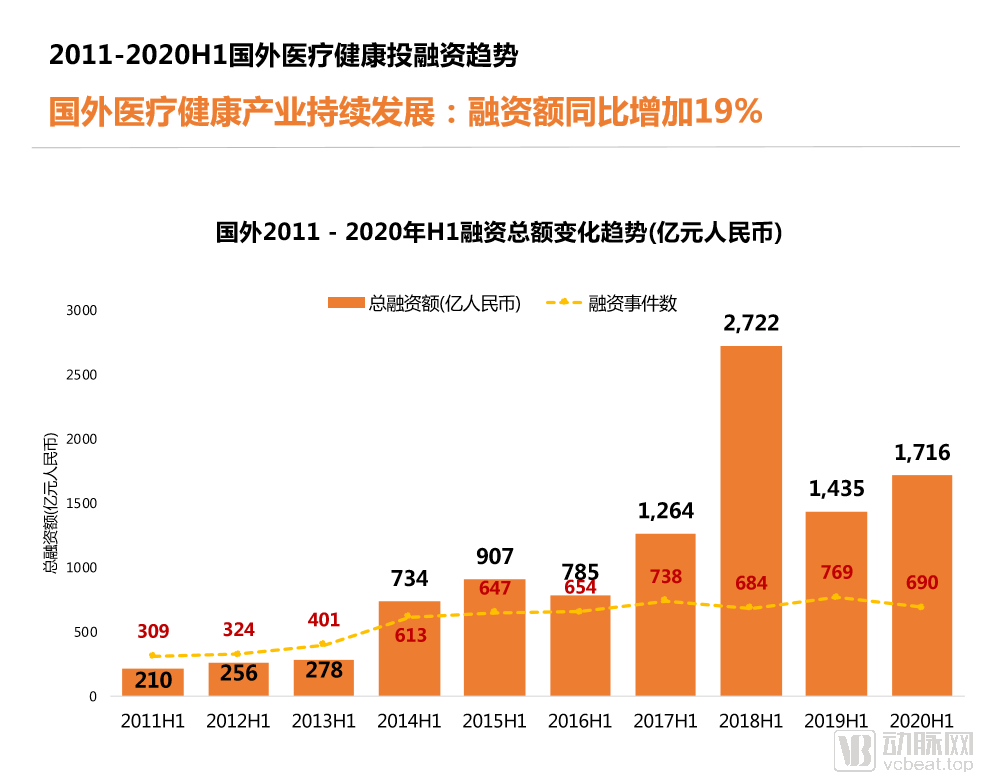

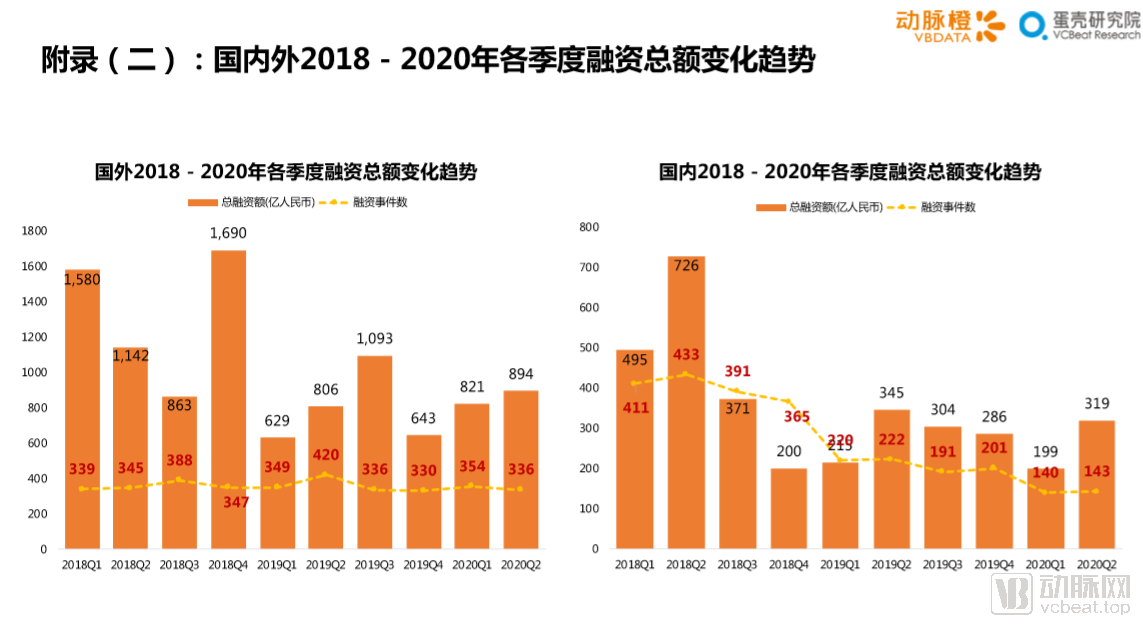

1.2 Sustained Development of the Overseas Healthcare Industry: Financing Volume Increased by 19% Year-on-Year

In the first half of 2020, the overseas healthcare industry continued to thrive,Total financing reached $24.45 billion(approximately RMB 171.58 billion); the number of financing events reachedFrom 690(including 23 incidents with undisclosed amounts).

Amid the severe turbulence in international capital markets, numerous industries, including tourism and entertainment consumption, have fallen into distress,Meanwhile, the primary market in the healthcare industry continues to thrive; although the number of transactions has declined slightly, total financing increased by 19% year-on-year.

Contrary to our expectations, the impact of the COVID-19 pandemic, a black swan event, has hardly dampened investment enthusiasm in the overseas primary healthcare market. After experiencing severe volatility in foreign capital markets, financing demands in sectors such as telemedicine, diagnostics, and vaccine R&D were met with even faster responses. The total financing amount in the first half of 2020 continued to grow, which is particularly commendable amid the pandemic.

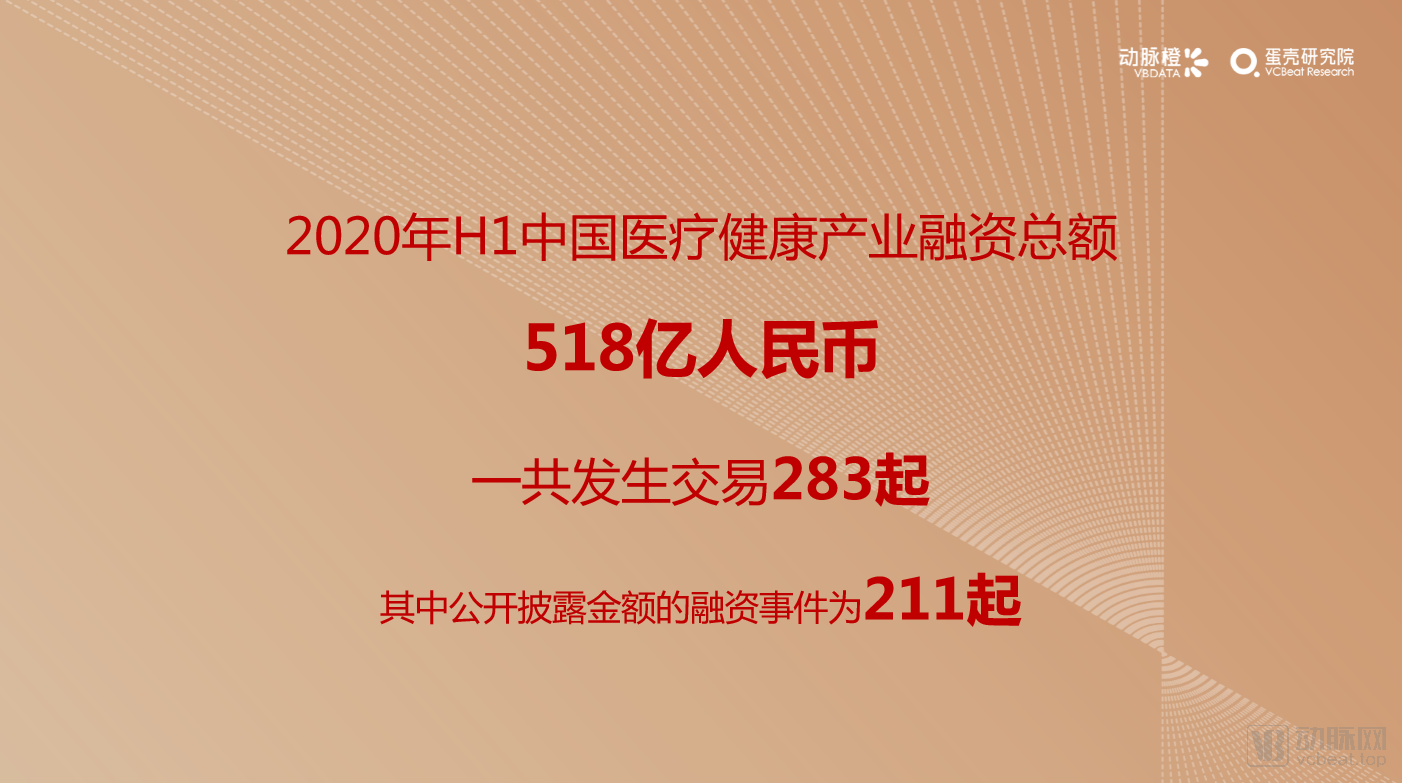

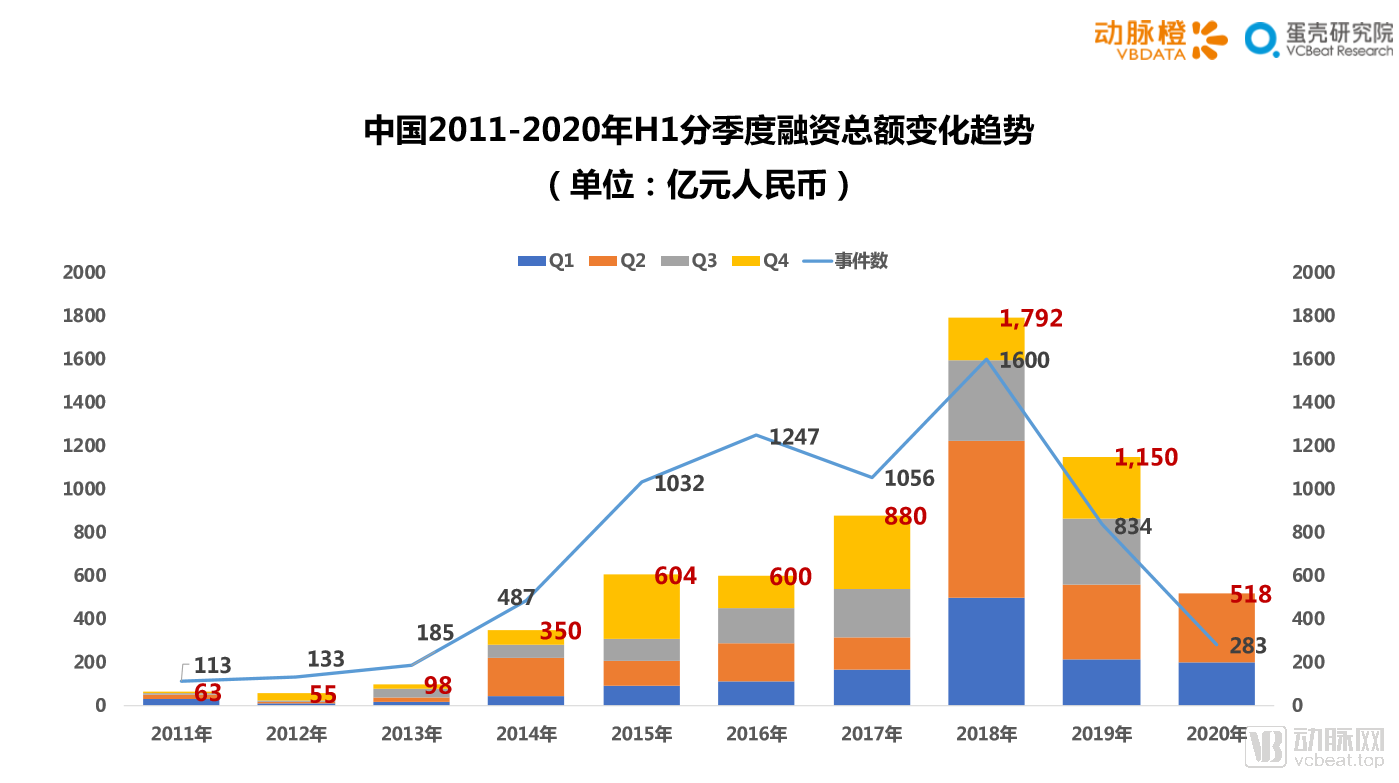

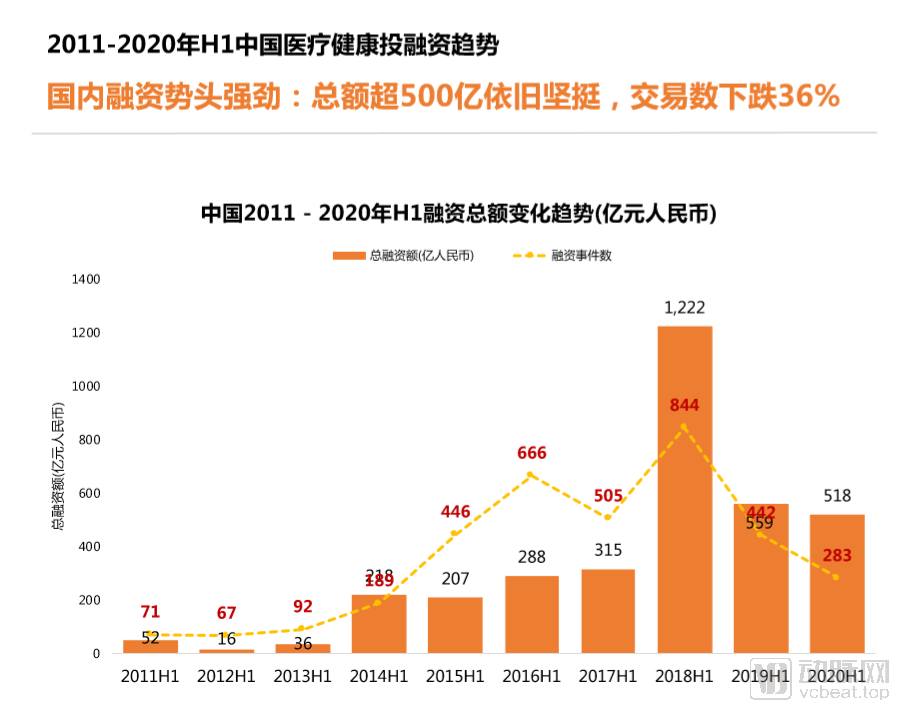

1.3 Strong Financing Momentum in China’s Healthcare Industry: Total Amount Remains Robust at Over RMB 50 Billion, While Number of Deals Drops by 36%

In the first half of 2020, a total of283 financing rounds, with a total funding amount of RMB 51.75 billion.

Affected by the dual impact of the COVID-19 pandemic and the tightening of overall financing capital in recent years, healthcare financing deals in China dropped significantly in the first half of 2020. The number reached its lowest point since the first half of 2015, representing a 36% year-on-year decline.

According to IT Juzi’s industry-wide data, there were 1,732 financing deals across all sectors in China during the first half of 2020, a year-on-year decrease of 64.4%; the total transaction amount reached RMB 463.16 billion, down 47% year on year. Amid the overall downturn in China’s primary market, total financing in the healthcare sector declined by only 7.4% year on year, surpassing RMB 50 billion.

Despite a sharp decline in the number of deals, total financing saw only slight adjustments, with 104 individual funding rounds exceeding RMB 100 million this quarter.

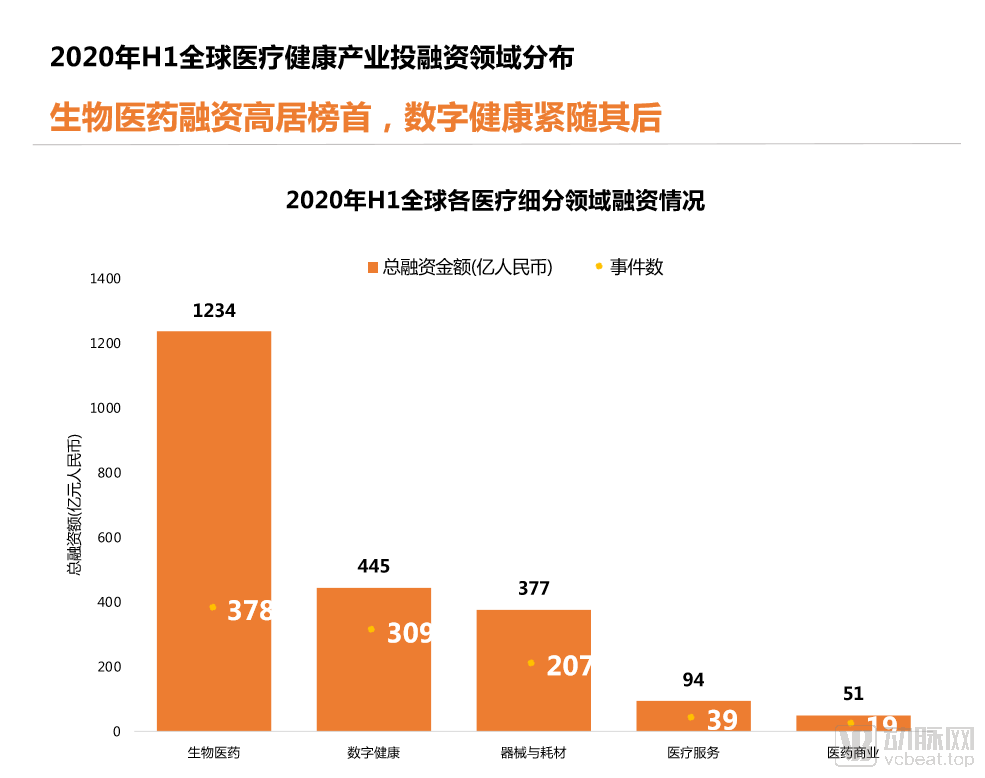

2.1 Global Distribution of Financing by Sector: Biopharmaceuticals Lead, Followed Closely by Digital Health

First Quarter of 2020,The global biopharmaceutical sector ranked first among sub-sectors, with 378 transactions and a total financing amount of RMB 123.4 billion.

In addition to the perennially hot field of biomedicine,Digital health funding remained highly active in H1 2020.The objective impact of the global COVID-19 pandemic, coupled with the strong performance of telemedicine companies in the secondary market since the outbreak, has further accelerated innovation and financing in the digital health sector.A New Wave of Health Financing Is Underway.

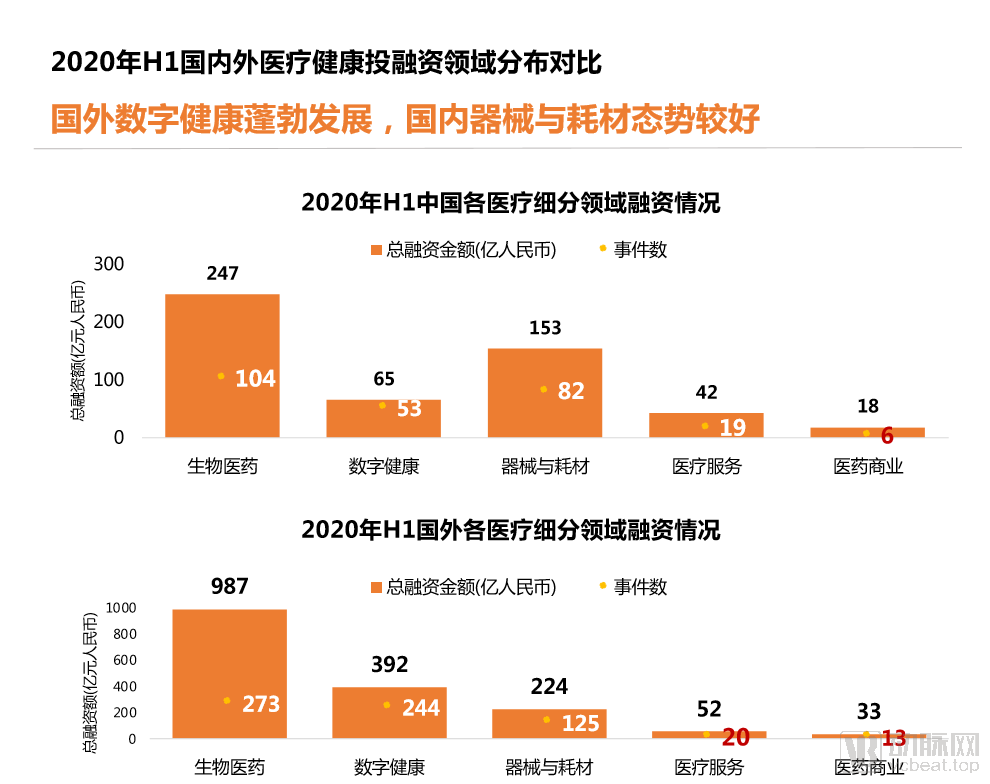

2.2 Digital Health Thrives Abroad, While Medical Devices and Consumables Show Strong Momentum in China

A comparison of the distribution of financing across various healthcare sectors in China and abroad during the first quarter of 2020 reveals thatBiopharmaceuticals remain the hottest sector for joint bets by both domestic and international investors.

However, the focus of financing varies across other sectors.Abroad, Digital Health Is Flourishing, in H1 2020, there were a total of 244 financing events, with cumulative financing amounting to RMB 39.2 billion; andChinaA Surge in Large-Scale Financing for In Vitro Diagnostic Companies, Including MGI TechResulting in higher expenditures in the medical devices and consumables sector.

2.3 Global Hot Investment Themes: Biopharmaceuticals, Healthcare Informatics, Internet+ Healthcare, IVD First Half of 2020,Global Biopharmaceuticals, Healthcare Informatics, Internet + Healthcare, and IVDTags such as these have high popularity.

First Half of 2020,Global Biopharmaceuticals, Healthcare Informatics, Internet + Healthcare, and IVDTags such as these have high popularity.

In addition to the perennially hot biopharmaceutical sector, digital health companies have received substantial financing support amid the pandemic, while in vitro diagnostics (IVD), which played a crucial role in COVID-19 testing, have gained increased attention.

From the perspective of round distribution, among the financing events involving hot tags in the first half of 2020,Series A financing rounds occurred most frequently, with a total of 272 deals. Meanwhile, the number of Series C financing rounds surpassed that of angel rounds, reflecting growing investor confidence in companies with relatively mature business models.,This is inMedical InformaticsThis is particularly evident in the field.

3.1 Global: Vaccine Developers in High Demand—mRNA Technology Shows Initial Success in COVID-19 Vaccine Development

In the first half of 2020, a total of 28 vaccine development companies in China and abroad secured financing, with the total amount reaching RMB 11.48 billion. These companies were primarily engaged in the research of viral vaccines and mRNA vaccines.

mRNA vaccines have played a pivotal role amid the global pandemic this year. Companies both in China and abroad are developing mRNA vaccines to combat COVID-19.mRNA vaccines from companies such as Moderna and Walvax Biotech have entered clinical trials.

CureVac is one of the global leaders in mRNA drug development, with its previous round of financing completed in 2016. Its outstanding performance in COVID-19 vaccine research and development drove a €300 million financing round. It is reported that CureVac will begin human clinical trials for its COVID-19 vaccine, with the first batch of vaccination tests starting in June.

Domestic SWM Biotech completes two rounds of financing in the first half of the year, advancing at a rapid paceItsProducts such as personalized mRNA cancer vaccines, mRNA infectious disease vaccines, mRNA therapeutics for protein-deficiency disorders, and mRNA therapeutics for genetic diseases. The company’s COVID-19 vaccine candidate is currently in the animal testing phase.

3.2 International: Telemedicine Concepts Gain Momentum—Primary and Secondary Markets Flourish in Tandem

In the first half of 2020, online medical consultations, online health management, home testing, and otherTelemedicine has undoubtedly been the big winner in overseas healthcare capital markets.Secondary market withTeladocandLivongo Healthrepresented by have seen their stock prices surge continuously since the pandemic. Meanwhile, the primary market hasOscar Health, American Well, and DispatchHealthRepresentative telemedicine companies have all secured over $100 million in Series C financing.

The outbreak and spread of the epidemic abroad have posed unprecedented challenges to global public health security. Although European and American countries have undertaken varying degrees of digital transformation in healthcare in recent years, the current epidemic has still exposed numerous deficiencies, including incompatible information systems, chaotic data management, limited cross-departmental collaboration, poor coordination between governments and hospitals, exorbitant costs of digital transformation, and the difficulty of maintaining a balance between personal privacy and the public interest.

The emergence of the pandemic temporarily altered this situation.CMS expanded reimbursement for telehealth services, and HHS eased penalties under HIPAA regulations, thereby enhancing collaboration among institutions.Driven by various factors,Overseas demand for telemedicine has surged dramatically, with American Well alone witnessing a more than tenfold increase in traffic. It is expected that financing enthusiasm for companies associated with the telemedicine concept will continue to intensify in the second half of the year.

3.3 China: In Vitro Diagnostics Financing Surpasses Full-Year 2019 Total—12.133 Billion Yuan Raised Across 37 Deals

In the first half of 2020, ChinaIn Vitro Diagnostics (IVD) SectorTotal Incidence37 Financing Events,Total financing reached RMB 12.133 billion.These companies focus on different fields, and their financing rounds are relatively early (Concentrated in Series A and Series B rounds)。

A comparison with the 2019 data, which showed that 33 in vitro diagnostic (IVD) companies secured a total annual financing of RMB 4.828 billion, reveals thatThe COVID-19 pandemic has directly stimulated a surge in financing within the IVD sector.

Since the outbreak of the COVID-19 pandemic, the in vitro diagnostics (IVD) industry has garnered increased attention, and the state has introduced multiple policies to accelerate the approval of diagnostic reagents. Driven by the public health infrastructure needs for detecting unknown pathogens such as the novel coronavirus,Promoted the R&D and commercialization of technologies such as mNGS, leading to particularly frequent financing activities in the molecular diagnostics sector during the first half of 2020.

In the post-pandemic era, with the state’s vigorous strengthening of public health and the disease control and prevention system,The IVD sector remains a hot track in the healthcare market, with oncology diagnostics, early cancer screening, and consumer-grade genetic testing services likely to attract significant capital interest.

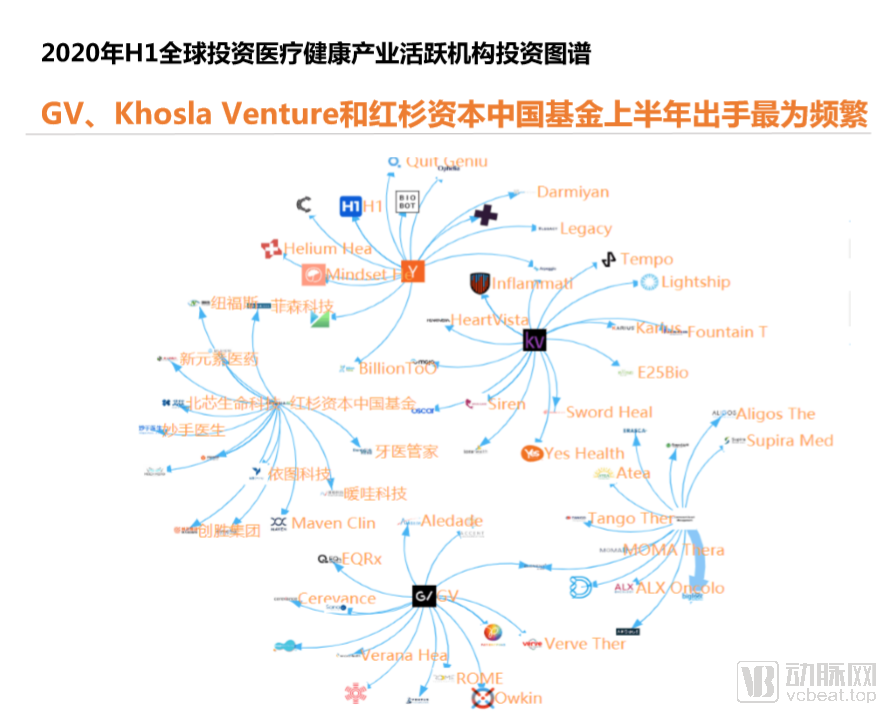

4.1 GV, Khosla Ventures, and Sequoia Capital China Were the Most Active Investors in the First Half of the Year

In H1 2020, the most active global investors in healthcare wereGV, Khosla Ventures, and Sequoia Capital ChinaAll transactions in the first half of the year were14 times, with investment areas includingBiopharmaceuticals, digital health and pharmaceutical commerce, healthcare services, and medical devices and consumables.

Among companies that have received cross-investments from active investment firms, those in the biopharmaceutical sector predominate, such as China’s Genor Biopharma, JW Therapeutics, and New Element Pharmaceuticals.

4.2 New Drug Development and Digital Health Draw Attention, with 13 Institutions Making More Than 10 Investments in Half a Year

First Half of 2020,A total of 13 institutions have made 10 or more investments.

In terms of sectors, active institutions favor biopharmaceuticals and digital health; in terms of funding rounds,An increase in investments in Series C and later-stage rounds became a characteristic of active institutional investors in the first half of 2020.

Compared with previous periods, China’s top-tier institutions appear to have exercised greater caution in their investment activities during the first half of this year. Among the 13 active institutions, onlySequoia Capital China was selected with 14 investments.

4.3 24 Companies Receive Co-Investment from Active Institutional Investors, with Innovative Drug R&D Garnering the Most Attention

Among the top 24 healthcare investment institutions by number of investments in the first half of 2020, 24 companies received backing from two or more of these investors, reflecting the potential and strength of these startups.

From the perspective of round distribution,The probability of being simultaneously invested in by two active top-tier firms around the Series C round is higher.On one hand, it is because the business models or R&D progress of companies at this stage are more mature; on the other hand,This corroborates the trend of active investment institutions shifting toward later-stage funding rounds.

In terms of company types, biopharmaceutical companies specializing in gene therapy and cell technologies appeared most frequently. In addition, during the first half of 2020, more digital health companies, such as healthcare informatics firms, gained favor among active institutional investors.Ready RespondersandRibbon Health, Internet + Healthcare CompanyRubiconMDand Digital Therapeutics CompaniesMindstrongetc.

Among the 24 companies are two Chinese firms: innovative biopharmaceutical R&D enterprisesTranscenta Holdingand Tumor Cell Immunotherapy CompanyJW Therapeutics。

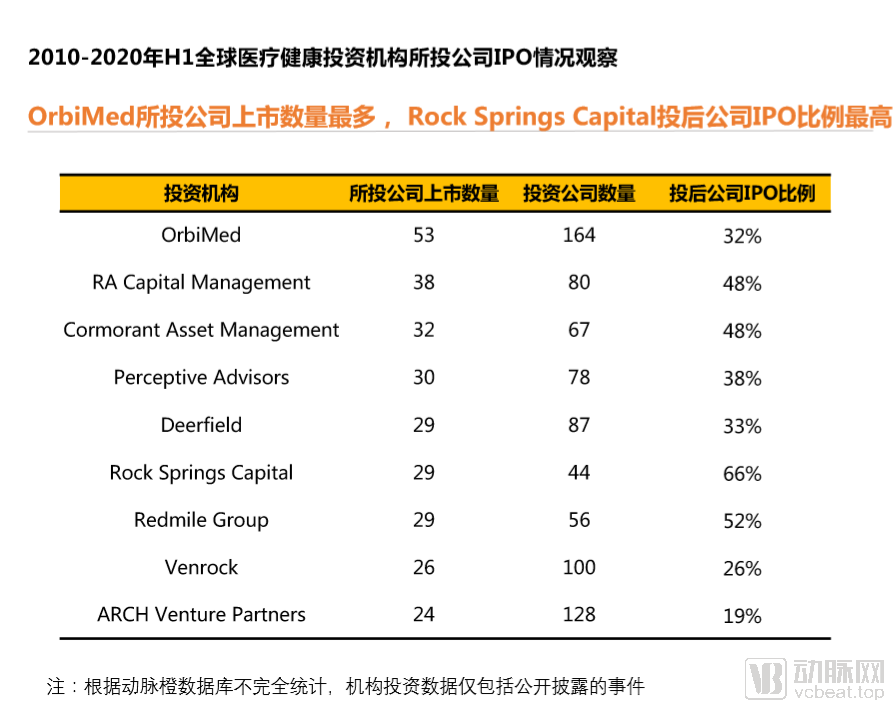

4.4 OrbiMed Has the Highest Number of Portfolio Companies Going Public, While Rock Springs Capital Has the Highest IPO Rate Among Its Portfolio Companies

Among investment institutions worldwide,An initial public offering (IPO) is one of the primary exit routes for invested companies.Among the nearly 8,000 institutions worldwide that have participated in healthcare investments,OrbiMed’s Portfolio Companies’ IPO Performance Over the Past DecadeThe Best-Performing Company. Of the 164 companies in its investment portfolio, 53 have gone public.

From the perspective of the listing ratio of investment companies, the institutions with the most accurate vision and the highest exit efficiency areRock Springs Capital. The companies invested in by the institution in the first half of this year include Everest Medicines, Athira, and Atea.

4.5 Among the top five investment institutions by number of portfolio companies that went public in H1 2020, OrbiMed led with eight listings, while two Chinese firms, CDH Investments and Lilly Asia Ventures, also made the list.

Among all investment institutions, the top five institutions in terms of the number of portfolio companies that went public in H1 2020 areOrbiMed, RA Capital Management, Vivo Capital, CDH Investments, Cowen Healthcare Investments, Perceptive Advisors, Redmile Group, Lilly Asia Ventures, and Versant Ventures.

Two firms, CDH Investments and Lilly Asia Ventures, made the list. The first half of this year was a harvest season for CDH, with five of its portfolio companies in China successfully going public. According to statistics from the VCBeat Orange Database, CDH has invested in a total of 58 healthcare enterprises, among which16 Healthcare Companies Successfully Complete IPOs, with several others exiting through mergers and acquisitions.

Notably, many companies that completed their IPOs in the first half of the year were jointly invested in by at least two institutions. Examples include Legend Biotech, Arcutis Biotherapeutics, and Imara.liPassage Bio, a developer of AAV gene therapies, has garnered optimism from four institutions. Without exception, all four invested in the company during its Series A round.

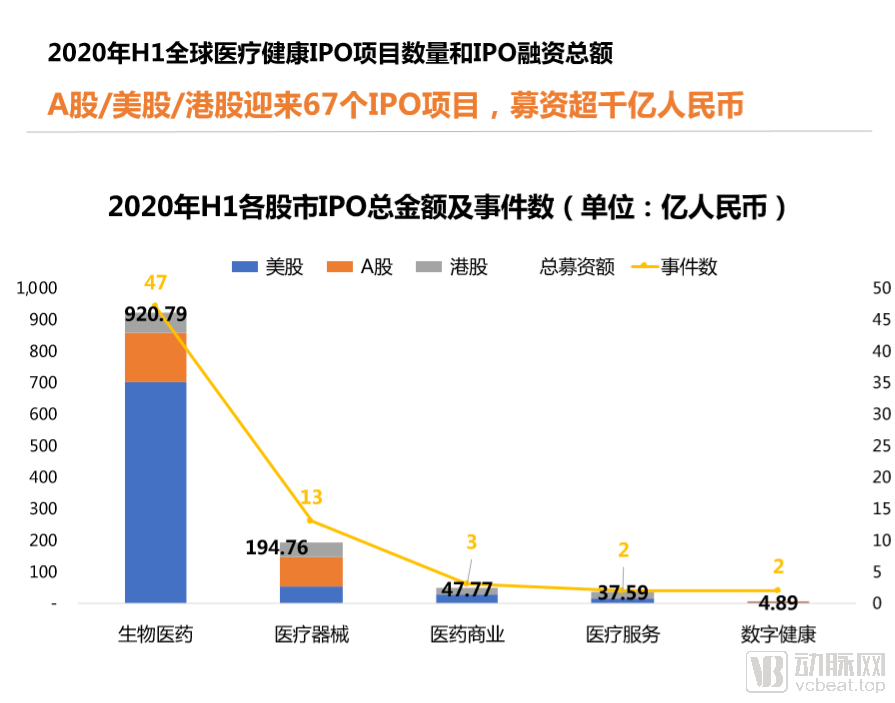

5.1 A-Shares, U.S. Stocks, and Hong Kong Stocks Welcome 67 IPOs, Raising Over RMB 100 Billion

In the first half of 2020, the U.S. stock market, A-share market, and Hong Kong stock market welcomed67 Listed Healthcare Companies.

Of these, 20 companies went public in Q1 and 47 in Q2. Compared with the 79 companies that listed in the first half of 2019, it is evident that the impact of the post-pandemic economic downturn on healthcare IPOs was not as severe as anticipated.Q2 2020 IPO activity was even more robust than in previous periods.

With the listing of 67 new stocks, coupled with the counter-trend surge of existing stocks in sectors such as telemedicine and biopharmaceuticals during the pandemic, both the U.S. stock market and China’s A-share market—the two major global equity markets—ended the first half of 2020 with overall gains.The healthcare sector has yielded substantial gains.

5.2 32 Chinese healthcare companies went public; the number of listed companies in Q2 2020 tripled quarter-on-quarter

In the first quarter of 2020, affected by the pandemic, the IPO processes of Chinese healthcare companies were delayed, with only eight healthcare enterprises listed on the A-share, Hong Kong stock, or U.S. stock markets.

However, in the second quarter following the resumption of work and production, bolstered by the STAR Market, the IPO process for Chinese companies in the secondary market was remarkably robust, with 24 newly listed companies makingIn the first half of 2020, the number of domestic companies listed reached 32.

From the perspective of company type, the vast majority of companies areBiopharmaceutical Company。

In light of the current state of China's secondary market,The pharmaceutical and biotechnology sector led the A-share market with a 40.28% gain over the past half-year.Although the A-share market experienced significant volatility over the past six months, it ultimately achieved a respectable performance in the first half of the year, driven by the gradual easing of pandemic impacts and the recovery of socioeconomic activities.

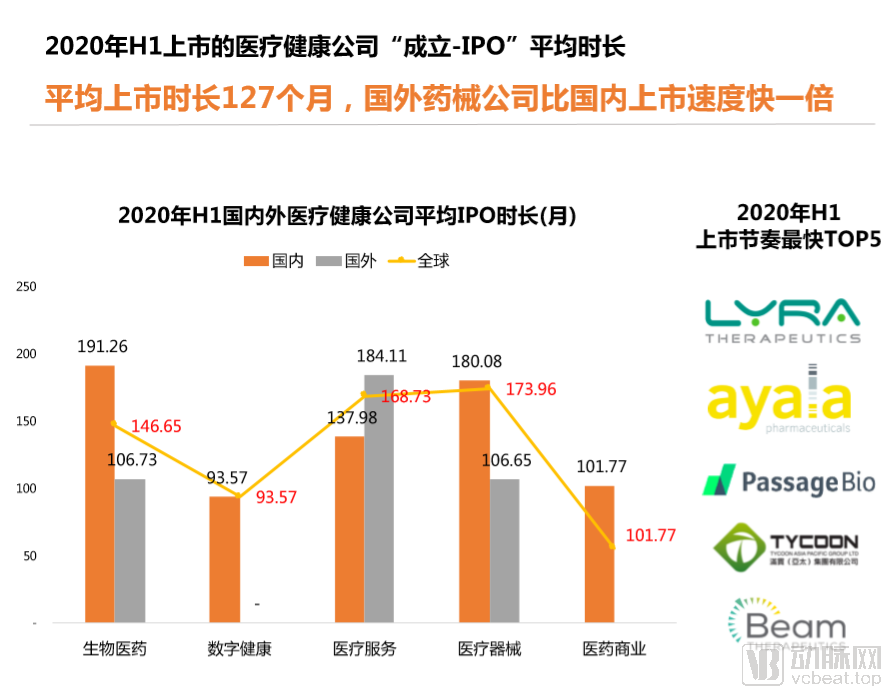

5.3 Average Time to Market is 127 Months; Foreign Pharmaceutical and Medical Device Companies Launch Products Twice as Fast as Domestic Ones

Of the 67 healthcare companies that went public in H1 2020,The average gestation period from establishment to IPO is approximately 127 months.

The relatively short time to IPO for digital health companies appears fast-paced in the healthcare industry, which inherently requires a longer period of consolidation.

Benefiting from the Nasdaq Stock Exchange’s support for innovative biotechnology and pharmaceutical companies,Foreign biopharmaceutical and medical device companies have a listing cycle that is nearly twice as fast as that of domestic enterprises.However, the launch of the STAR Market is expected to narrow this gap.

The Fastest to MarketLyra TherapeuticsFounded in November 2018, the company listed on NASDAQ in less than two years. Its proprietary technology platform, XTreo, enables precise, long-term drug delivery to affected tissues with a single administration. The company’s developed products, LYR-210 and LYR-220, are bioabsorbable polymer matrices administered via a non-invasive approach, providing up to six months of sustained therapy to the sinus passages. Their active ingredient, mometasone furoate, has been approved by the U.S. FDA.

6.1 Global: The United States Remains Dominant, with China and the US Accounting for 91% of Total Global Financing

In the first half of 2020, the five countries with the highest number of global healthcare financing events wereUnited States, China, United Kingdom, Canada.

First Half of 2020,The United States recorded 463 financing deals, raising $18.763 billion (RMB 131.73 billion).Leading globally, with China close behind; the United States and China together account for 91% of total funding and 90% of financing deals across all countries.

GermanyFinancing activities were relatively robust in the first half of 2020, primarily sourced frommRNA VaccinesCureVac’s R&D platform secured $300 million in financing due to its outstanding performance in COVID-19 vaccine development.

From the perspective of investment hotspots,Digital Health and BiopharmaceuticalsIt was a hot topic of global concern in the first half of 2020.

6.2 United States: California Dominates, with Massachusetts and New York Emerging as Secondary Hubs

In the first half of 2020,California, United StatesA total of 159 healthcare investment and financing events occurred, raising $6.69 billion (approximately RMB 46.95 billion), which is alsoThe Region with the Highest Frequency of Global Healthcare Venture Capital Investment Deals.

Massachusetts is renowned for its prominent biotechnology industry cluster and abundant healthcare resources,New York, by contrast, exhibits a vibrant atmosphere for digital health innovation. Due to the nature of biotechnology companies, although Massachusetts recorded just over 20 more deals than New York, its total financing volume was nearly three times that of the latter.

6.3 China: Shanghai and the Yangtze River Delta Show Strong Growth, Beijing Declines, Guangdong Rises

In terms of the scale of healthcare investment and financing in individual provinces and municipalities, the five regions with the most concentrated healthcare investment and financing activities in China during the first half of 2020 were, in order:Shanghai, Beijing, Guangdong, Jiangsu, and Zhejiang.

ShanghaiA total of 68 financing events occurred, raising RMB 11.48 billion,The city with the highest number of financing events in the first half of the year. Following the first time in Q1 2020 that the number of financing events and the total amount raised in a single quarter surpassed those in Beijing, it continued to outperform Beijing in the first half (H1) of the year.

From the perspective of regional cluster development, excluding Beijing,The Jiangsu-Zhejiang-Shanghai Region Has Seen Its Influence in the Healthcare Industry Expand in Recent Years, it is expected to become the largest healthcare industry cluster in China in terms of investment and financing scale.

Guangdong’s rise is equally noteworthy, with RMB 13.23 billion in financing secured in the first half of this year, making it the leading province for healthcare investment.

7.1 Global Top 10: MGI Tech’s $1 Billion Financing Round Tops Global H1 Funding, with Four Chinese Companies on the List

Among the top 10 companies by financing amount in the first half of 2020, there were six U.S. companies, four Chinese companies, and one German company. The financing amounts of these 10 companiesAll exceed RMB 1 billion.

Although in the rankingBiopharmaceutical Companies Still Dominate, but MGI Tech and Grail, two IVD companies, entered the top three in terms of financing amount in H1 2020, indicatingThe outstanding role of the in vitro diagnostics industry in epidemic prevention and control is further boosting its capital-attracting power.

MGI Tech, Everest Medicines, Mabwell, and Chengda Fangyuan in China...companies made the list. Founded in 2016, MGI Tech is one of only three companies worldwide capable of independently developing and mass-producing clinical high-throughput gene sequencers.

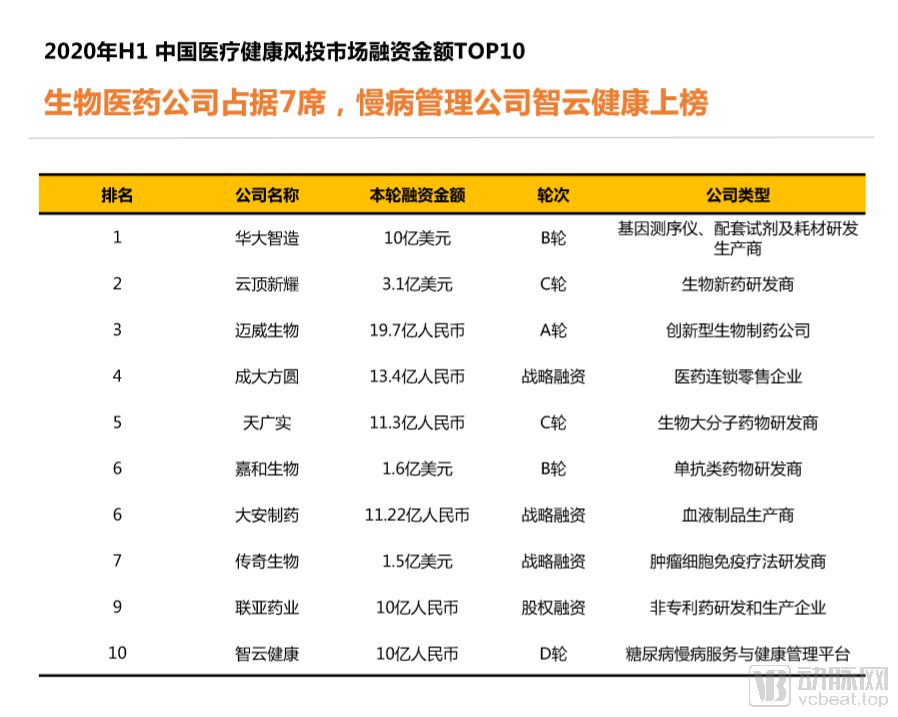

7.2 China’s Top 10: Biopharmaceutical Companies Claim Seven Spots, with Chronic Disease Management Firm Zhiyun Health Making the List

Among the top 10 companies with the highest financing amounts in China in Q1 2020,Biopharmaceutical Companies Continue to Hold a Dominant Position。

In the first half of 2020, there was a significant number of large-scale financing transactions in China's healthcare industry.There were as many as 104 instances of single financing rounds exceeding RMB 100 million.. Thus, even Zhiyun Health, which ranked tenth on the list, secured RMB 1 billion in financing.

As a digital health company focused on chronic disease management,Zhiyun Health Completes RMB 1 Billion Financinghas drawn significant attention. In its early stages, the company positioned itself as a platform offering diabetes management services for consumers (patients) and patient management solutions for physicians. It subsequently entered the realm of serious medical care by providing SaaS platforms to hospitals and establishing an e-commerce marketplace for pharmaceuticals. Later, the company expanded its focus from standalone diabetes management to comprehensive chronic disease management and launched an internet hospital.

Scan the mini-program QR code to download the full report for free.