Digital Health Funding Hits Record High of $5.4 Billion in H1 2020, Driven by Pandemic and Mega-Deals: Rock Health Report

Rock Health recently released its H1 2020 Digital Health Funding Report, analyzing changes in investment and financing within the sector during the first half of the year. Amidst the global pandemic and the U.S. economic recession, U.S. digital health companies raised a total of $5.4 billion in the first six months of 2020. The industry is on track to experience its largest funding year on record. Large deals once again drove the overall trend, with the average transaction size reaching a record high of $25.1 million in the first half of the year.

Rock Health reviewed the investment landscape in the first half of 2020 and shared its insights on the impact of COVID-19 on digital health innovation, funding trends, and investment sectors. VCBeat compiled the report.

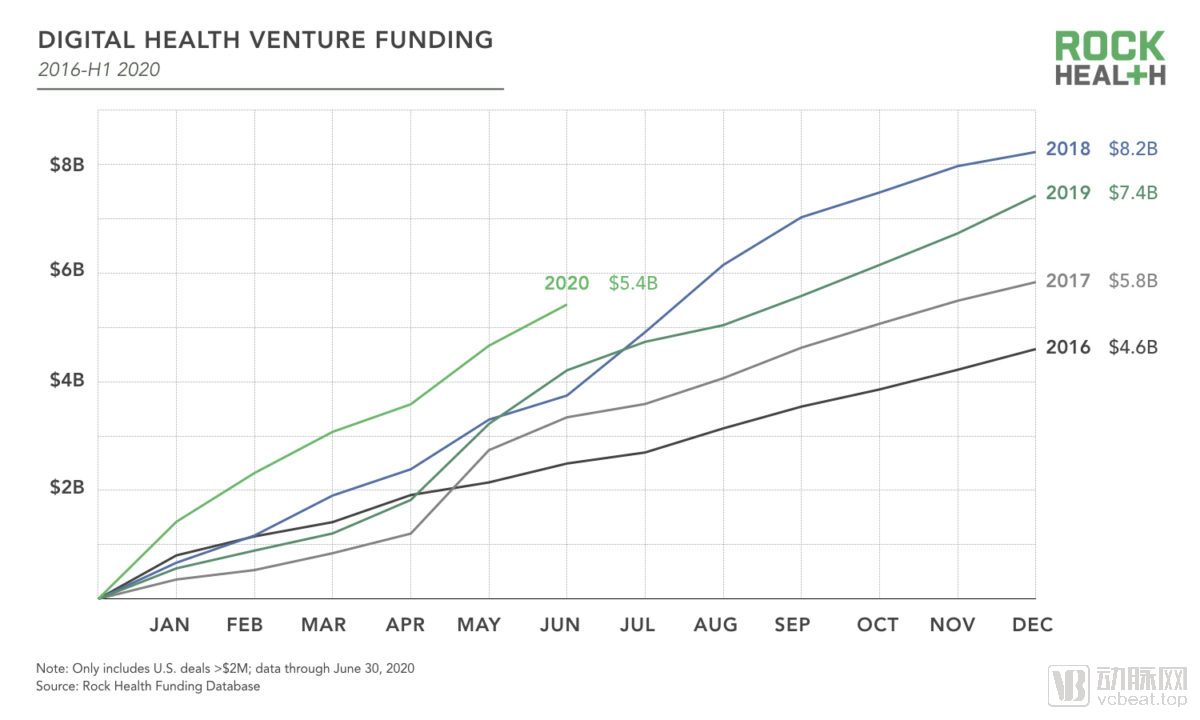

It has been a long, strange, and painful half-year. By the end of 2019, many venture capital firms focused on digital health interviewed by Rock Health were monitoring macroeconomic conditions, concerned about the potential impact of an economic recession. Rock Health believes that none of them anticipated what the first half of 2020 would bring: after the Dow Jones Industrial Average hit a record high in February 2020, the 10-year bull market came to an end, unemployment rose to its highest level since the Great Depression, and the stock market experienced the largest rebound in its history. Amidst this volatility, U.S. digital health venture capital investment has steadily set records for total annual funding, number of deals, and average deal size.

In the first quarter of this year, digital health investments secured a record-breaking $3 billion in funding. However, as the COVID-19 pandemic rapidly spread worldwide, both digital health investment and overall venture capital activity came to an abrupt halt in April. By May, investors flocked back to the digital health sector. Data shows that financing in the digital health field reached $5.4 billion in the first half of 2020, surpassing the previous record of $4.2 billion set in the first half of 2019 and marking the highest level for any first-half period from 2011 to 2020.

Although the digital health industry achieved record-high financing in the first half of 2020, Rock Health believes that this is just the beginning. On one hand, the United States officially entered an economic recession in February, and predictions regarding the spread of the COVID-19 pandemic and its impact on global supply chains, consumer confidence, and markets remain highly uncertain. Uncertainty in financial markets has been exaggerated, and even recent economic forecasts have become chaotic. Given this uncertainty, a potential second wave of the pandemic could quickly reverse the rebound in secondary markets and the growth in primary market investments seen in the second quarter. Although these pandemic conditions particularly align with investors’ appetite for digital health companies, their focus may shift amid a prolonged economic downturn.

2016–2020 H1 Digital Health Venture Capital Investment,Image from Rock Health

On the other hand, there has never been greater demand for digital technology-driven healthcare to date. Digital health investors have successfully validated this perspective.

Starting with an in-depth analysis of the Rock Health fund database, Rock Health has conducted a six-month review. This article explores the prospects of digital health investment, identifying who is investing and where their capital is flowing. Rock Health also examined two deeper potential investment areas driving trend development: on-demand healthcare services and remote disease monitoring.

Will Total Digital Health Funding Reach a Historic High in 2020?

At the end of the first quarter, Rock Health had predicted that digital health financing would slow down rapidly driven by the pandemic, and expected fewer digital health IPOs for the remainder of 2020. This held true throughout April, but the unexpected rise in May and June saw a significant increase in investment. As an investor, Rock Health, drawing from its own experience as well as those of other investors interviewed for this report, proposed three possible reasons for the stock market decline and subsequent reversal.

First, investors slowed their investment pace in March and April, likely due to risk aversion, which necessitated redirecting time and energy toward addressing the needs of their existing portfolios. This involved prioritizing current asset holdings, collaborating with portfolio managers to update financial and strategic plans, and reallocating capital in response to a rapidly changing environment.

Secondly, price uncertainty—particularly in late-stage transactions, which are more susceptible to secondary market volatility—may temporarily dampen investor enthusiasm and, in some cases, lead to irrational deals.

Finally, the record-breaking rebound in the stock market and the reduced volatility in the secondary market alleviated concerns about financial system instability (and a recurrence of the Great Financial Crisis). Coupled with the deregulation of digital health and the surge in demand for digital health solutions driven by the pandemic, this explains the reversal from a downward to an upward trend at the end of the first quarter.

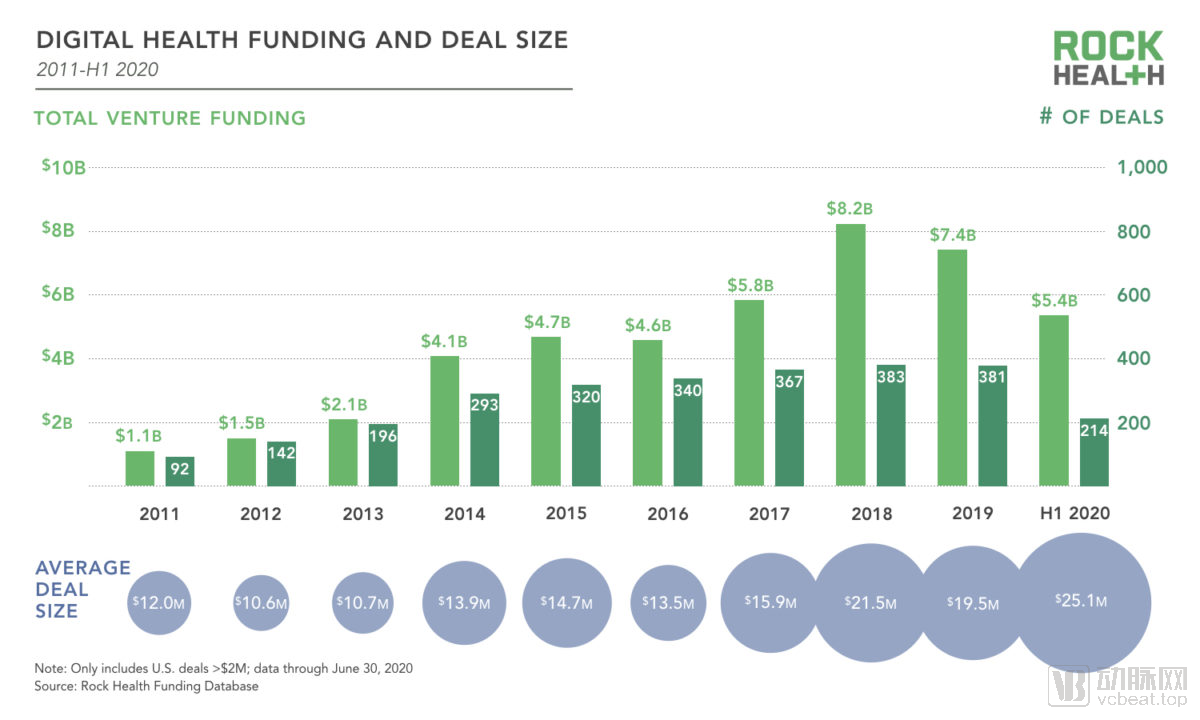

The reversal is highly significant. Digital health financing in the second quarter reached $2.4 billion, 33% higher than the quarterly average of $1.8 billion over the previous three years. In the first half of 2020, the average deal size for digital health companies was $25.1 million, significantly surpassing the historical record of $21.5 million set in 2018.

2011–2020 H1 Digital Health Funding and Transaction Volume,Image from Rock Health

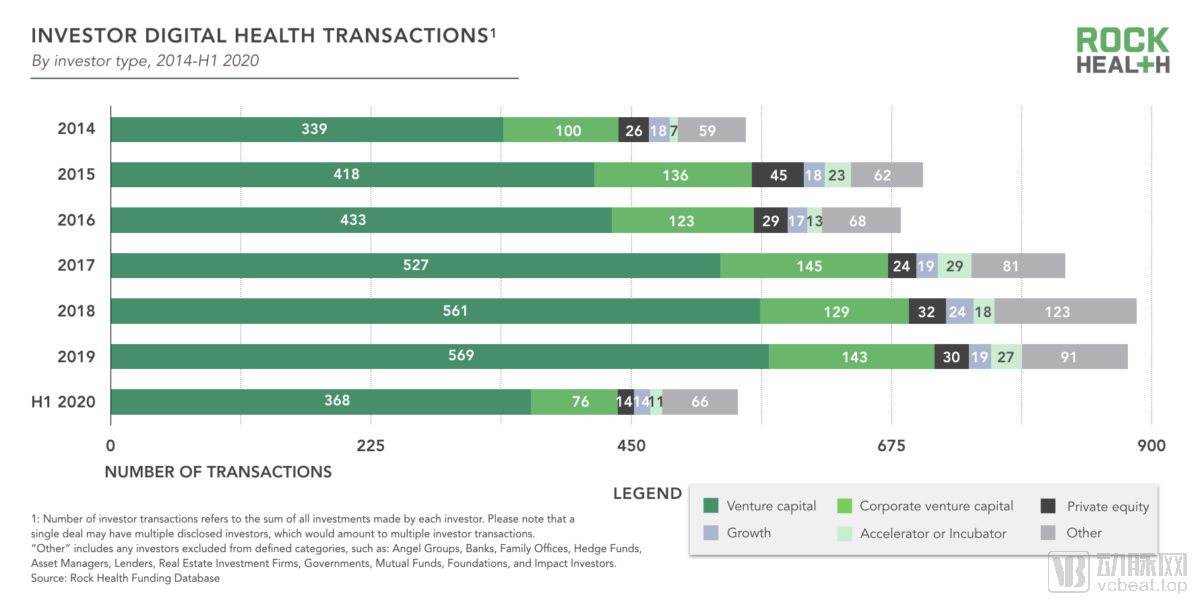

In 2020, the breakdown of investors was similar to previous years, with traditional venture capital firms accounting for 67% of the investor share, a two-percentage-point increase from 2019. The number of corporate venture capital (CVC) firms remained stable, representing 14% of total transactions.

2014–2020 H1 Digital Health TransactionsInvestors,Image source: Rock Health

Eleven mega-deals exceeding $100 million in the first half of the year led the development of digital health. Notably, five of these transactions occurred in May and June, precisely during the period when the COVID-19 pandemic caused an economic downturn in the United States.

1. ClassPass raised $285 million in its Series E funding round in January to expand its global operations and product offerings, providing users with in-person fitness classes.

2. Alto Pharmacy offers comprehensive digital pharmacy and prescription delivery services, completing a $250 million Series D financing round in January.

3. Due to the impact of the pandemic, Amwell raised $194 million in May to meet the growing demand for telehealth services.

4. Element Science, which manufactures wearable defibrillators that can prevent cardiac arrest, raised $146 million in its Series C financing round in March.

5. AI-driven drug discovery platform Insitro completed a $143 million Series B financing round in May.

6. DispatchHealth, which provides on-demand urgent care services, completed a $136 million Series C financing round in June.

7. Cedar, the developer of a healthcare system software platform for managing patient payments, completed a $102 million Series C financing round in June.

8. Mindstrong Health established a platform providing evidence-based treatment and psychiatry, completing a $100 million Series C financing round in May

9. Tempus completed a $100 million Series G financing round in March to redefine how genomic data is used in clinical settings

10. Verana Health raised $100 million in its Series D financing round in February, positioning itself as the “Google for physician-generated medical data.”

In the first half of 2020, companies invested in by Rock Health raised a total of $290 million. Avive, Benchling, DrChrono, Evidation, Omada Health, Virta, Vivante Health, and Wellth all completed financing rounds to support the evolving landscape of the healthcare industry.

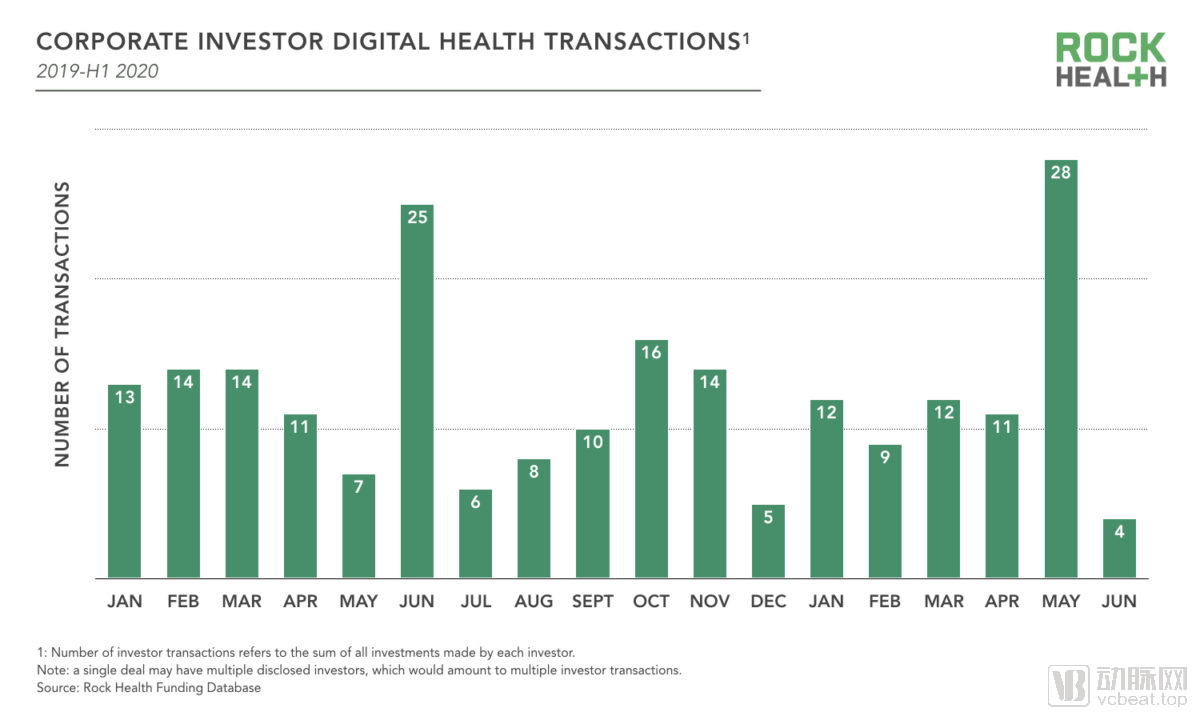

Corporate Venture Capitalists Completed More Deals Than Expected in the First Half of 2020

Despite the uncertainty and significant financial pressure facing many existing healthcare organizations, corporate venture capital (CVC) firms continue to invest actively. As of the first half of 2020, “strategic investors” remained stable, completing 76 deals in H1 2020 (equal to the number of CVC deals in 2019, with a total of 143 deals). CVC investment surged in May, with 28 deals recorded—150% higher than the average over the previous 12 months and surpassing the historical high of 26 deals set in November 2017.

Rock Health speculates that corporate venture capital (CVC) firms may view this crisis as an opportunity and accelerate their investments in digital health companies, rather than immediately pausing strategic investment initiatives while waiting for a return to normalcy. They believe that the pandemic will present them with favorable opportunities for development.

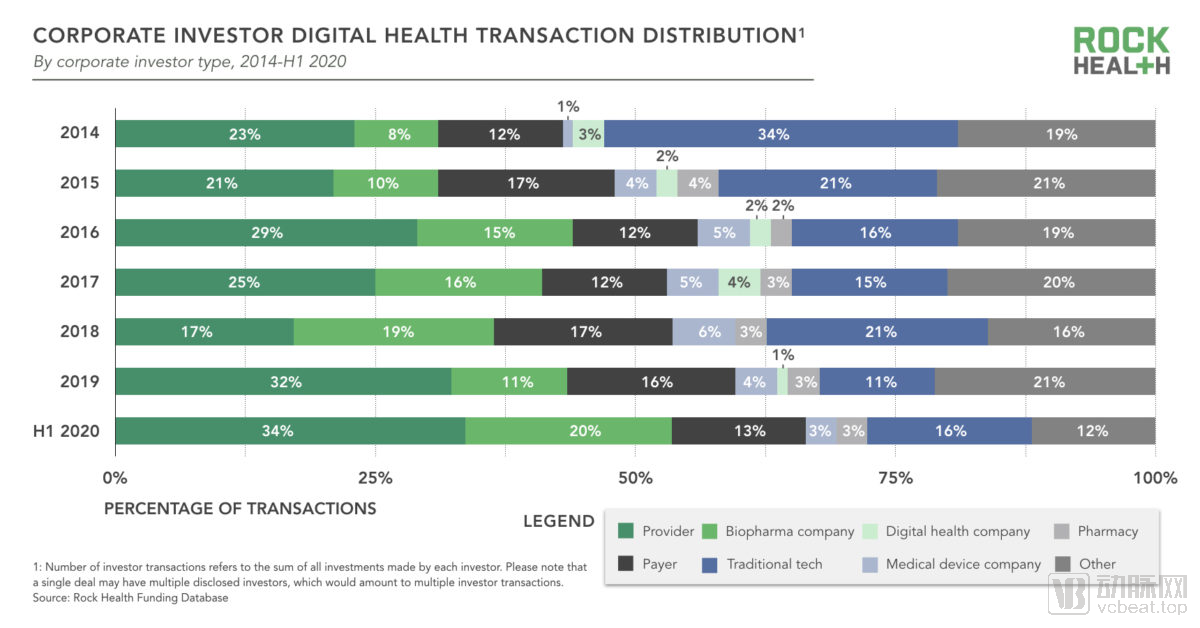

2019-2020 H1 Digital Health TransactionsCorporate Investors,Image source: Rock Health

In the first half of 2020, healthcare service providers (primarily health systems) accounted for 34% of all risk-based digital health transactions, representing the largest component of corporate venture capital (CVC) deals. Meanwhile, the pandemic inflicted a particularly severe blow on healthcare providers. For instance, inpatient services for elective treatments were postponed, and hospitals had to reallocate resources to prepare for and treat patients with COVID-19.

Despite these challenges, healthcare services venture capital funds continued to invest frequently in the first half of 2020, and healthcare services remained the most active area for strategic investment in the digital health sector. Rock Health will closely monitor changes in this segment, as potential second and third waves of the pandemic may affect the amount of dedicated capital available.

2014-2020 H1Distribution of Digital Health Deal Types by Investors,Image source: Rock Health

Compared with previous years, corporate venture capital (CVC) funds this year have invested in startups that provide consumer health information, on-demand medical services, precision medicine, and R&D solutions. Although Rock Health heard from many CVC investors early in the pandemic that they might shift their investment focus, data from various perspectives indicate that CVCs as a whole maintained their “current course and speed” in the first half of 2020.

Fei Ren, Vice President of The Riverside Company, stated that technology will be the key to corporate differentiation and effective competition; examples include quality quantification and tracking tools under the Value-Based Care (VBC) payment model, as well as tools for processing and tracking healthcare consumerism.

Has the pandemic accelerated capital concentration and later-stage funding growth?

Total financing across all industries amounted to $34.2 billion in the first quarter of 2020, comparable to the $34.0 billion recorded in the first quarter of 2019. However, funding in the digital health sector reached a record high of $3.0 billion in Q1 2020, compared with an average of $1.9 billion in 2019. In the first half of 2020, the average deal size for digital health startups was 29% higher than the overall level in 2019. Prior to the pandemic, Rock Health had noted that this market was gradually maturing. Rock Health observed that this trend accelerated in the first half of the year, as investors sought certainty amid uncertainty by providing larger rounds of financing to mature, late-stage digital health companies.

This may signal that investors are favoring high-quality, more mature healthcare companies. Financing data from the first half of 2020 supports this view. Compared with 2019, the transaction volume for Series C and later-stage deals in the first half of 2020 reached a record high.

In this scenario, companies seeking small-scale financing need not worry, as the top of the funnel remains active. Seed and Series A deals continue to account for 50% of all transactions (by volume), a trend that dates back to 2013.

M&A Activity Continues to Decline, but Digital Health Companies Are Thriving Amid Market Rebound

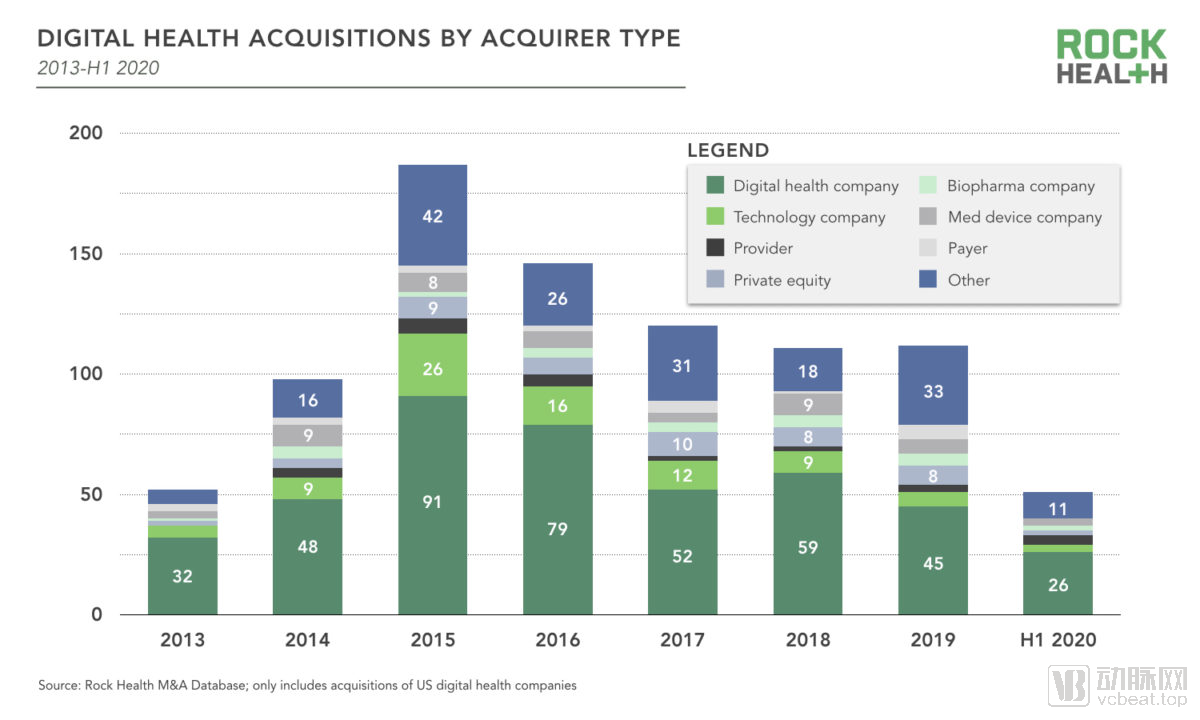

Mergers and acquisitions (M&A) remain a significant source of liquidity and returns for digital health investors. In the first half of 2020, 52 U.S. digital health companies were acquired, continuing a downward trend in M&A activity since its peak in 2015. Despite the economic slowdown, investors have generally continued to support acquisitions that consolidate market position. Notably, in this year’s deals, 52% of the acquirers were digital health companies, representing a 12-percentage-point increase from 2019.

2013-2020 H1Types of Acquisitions by Digital Health Companies,Image from Rock Health

Digital health companies are seeking external talent to scale up. Transactions in the first half of the year followed this trend.

1. In January, Teladoc acquired InTouch Health for $600 million to expand the capabilities of its telehealth platform.

2. In June, Lululemon acquired Mirror for $500 million to continue expanding beyond its retail business and further extend into digital fitness services.

3. Optum is in advanced negotiations with AbleTo regarding the $470 million acquisition of AbleTo to expand its remote behavioral health business.

4. Omada Health acquired Physera for $30 million in May, adding remote musculoskeletal care services to its care offerings.

5. Health Catalyst acquired Able Health for $27 million in February to enhance its capabilities in quality and regulatory compliance.

6. Virgin Pulse acquired Blue Mesa to expand its employer service offerings by integrating remote diabetes care and prevention into its existing platform products.

Surge in IPOs Improves Growth Prospects for Current and Future Digital Health Companies

By the end of the first quarter, the IPO outlook was extremely grim. Outside the digital health sector, Airbnb, a darling of the 2020 IPO class, postponed its IPO plans and raised $1 billion through private financing amid declining valuations. Rock Health is closely monitoring digital health companies on the listing pipeline to determine which ones can play a critical role in and provide support for the diagnosis and treatment of COVID-19.

The surge in the stock market and the widespread adoption of telemedicine services have paved the way for Amwell-fresh to go public this fall, raising $194 million. Teladoc, one of Amwell’s main competitors, announced during its first-quarter earnings call that its revenue increased by 41% year-over-year, with a 92% increase in new users, and highlighted the company’s rising stock price.

GoHealth, which operates a healthcare-focused health insurance marketplace, is also seeking to go public, aiming to raise $100 million in an initial public offering (IPO) later this year. Accolade, a provider of health benefits platforms, raised $220 million in its IPO on July 2, with an initial share price of $22 and a valuation of $1.2 billion.

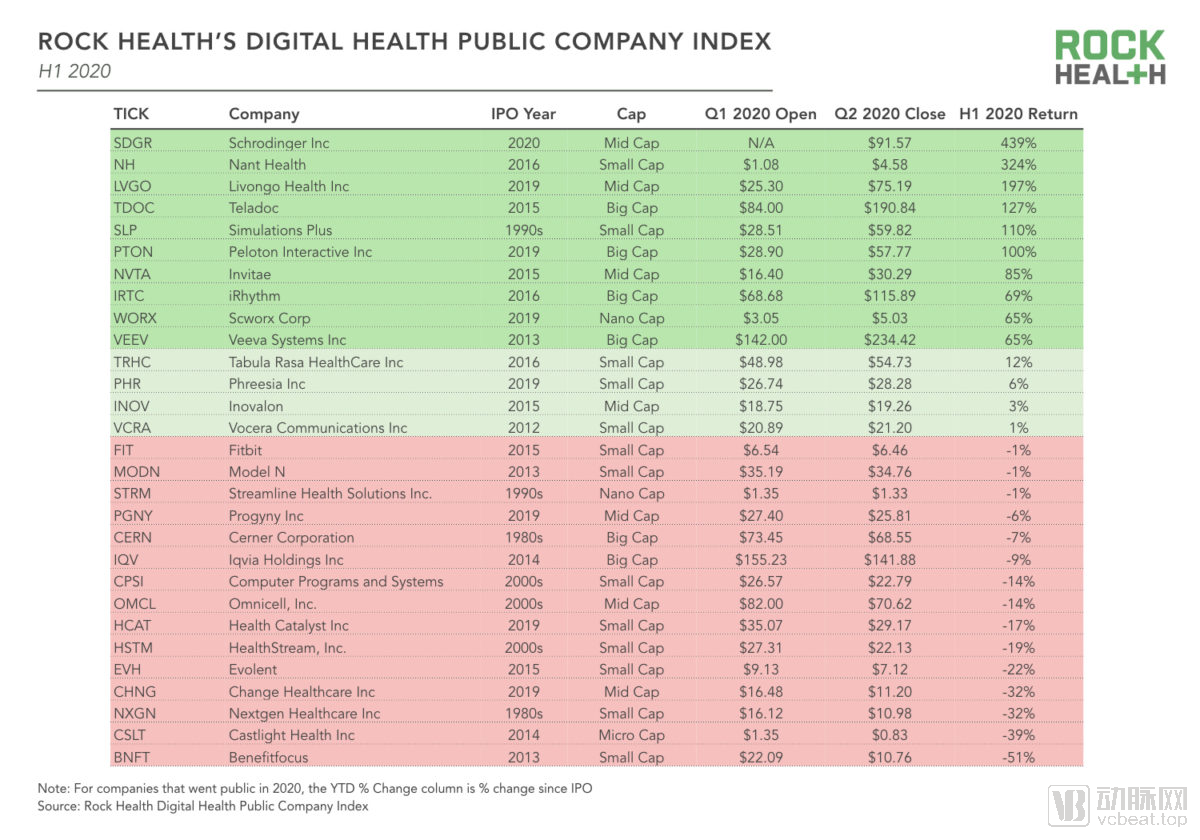

The Digital Health Public Company Index rose by 30% in the first half of 2020, outperforming the S&P 500 Index, which declined by 4%. After a three-year lull in digital health IPOs beginning in 2016, eight digital health companies went public over the past 12 months: Accolade, Livongo, Health Catalyst, Phreesia, Change Healthcare, Peloton, Progyny, and Schrödinger. As of June 30, 2020, the combined market capitalization of the six digital health companies that had their IPOs in 2019 reached $27 billion, representing a 50% increase from the end of 2019. Schrödinger, which listed in February 2020, saw its share price surge by 439% compared to its IPO price.

Rock Health 2020 H1 Digital Health IPO Index,Image from Rock Health

Keith Figlioli, a partner at LRVHealth, stated that the secondary market for digital health companies will continue to experience robust growth, with more capital being allocated to future financing activities to encourage further mergers and initial public offerings.

On-Demand Healthcare Services and Remote Monitoring Are Driving the Entire Industry Toward Telehealth

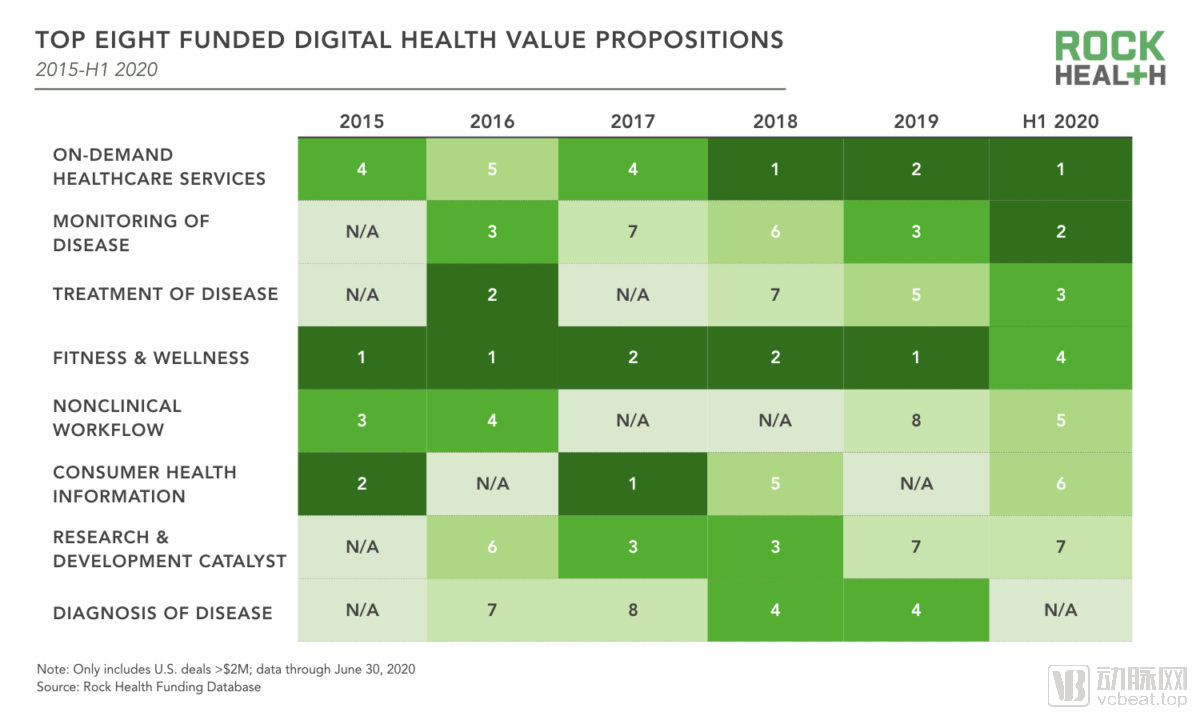

COVID-19 has prompted businesses to provide remote treatment and monitoring for patients, thereby accelerating the development of telemedicine. As patient demand for remote care surges, venture capitalists are seizing this opportunity. In the first half of this year, digital health companies offering on-demand medical services, such as Alto Pharmacy and Amwell, raised $1.1 billion, while disease surveillance companies raised $831 million.

2015-2020 H1Top 8 Digital Health Value Propositions,Image from Rock Health

2015-2020 H1Top 8 Digital Health Value Propositions,Image from Rock Health

In 2020, telemedicine companies raised $926 million. Surveys indicate that patients and healthcare institutions are increasingly inclined to use telemedicine to prevent COVID-19 infection, amid concerns about potential second or even third waves of the pandemic. According to reports, Amwell, a telemedicine giant, saw its usage increase by 158%. The dual benefits of bringing convenience to consumers and rationalizing capacity for providers suggest that remote care solutions are here to stay.

Meanwhile, telemedicine has reduced barriers to remote care and remote monitoring. In 2020, the introduction of the following policies will better assist healthcare institutions in providing telemedicine services:

1. CMS has expanded reimbursement coverage for telehealth services by waiving video requirements for many services, allowing charges for outpatient services provided remotely, and broadening the types of providers eligible for telehealth compensation. The long-term policy implications for the U.S. Department of Health and Human Services (HHS) remain unclear, but it is unlikely that pre-pandemic standards will be reinstated.

2. HHS announced that it would waive HIPAA penalties for telehealth services conducted in good faith and lower the penalty caps for certain violations.

3. Many governors and state health agencies have reduced state licensing barriers, making it easier for clinicians to provide healthcare services across state lines.

Overall, these changes have made it easier for digital health companies to scale up and meet the growing market demand for remote care solutions. Although some of these changes may not be permanent, consumers and healthcare providers have already experienced the value and convenience of remote care. Rock Health believes that these new care habits will create new care scenarios during the pandemic.

2020 Outlook: Surge in Consumer Demand, Investor Interest in Digital Behavioral Health

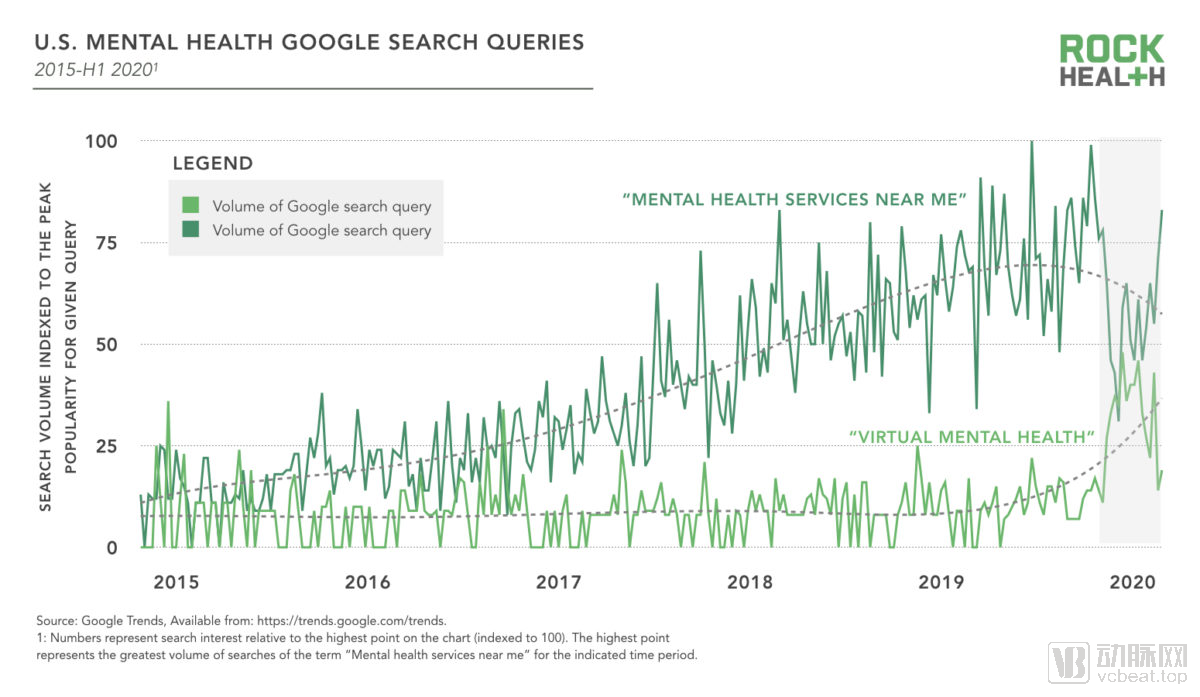

The pandemic has brought unprecedented anxiety and isolation to the public. Social, political, and economic instability have exacerbated the existing mental health crisis. According to a survey by Mental Health America, nearly 100,000 Americans believed that the H1N1 influenza would cause them anxiety or depression. In April 2020, a study found that 13.6% of U.S. adults reported symptoms of serious psychological distress, compared with 3.9% in 2018. Google searches for “mental health services near me” had been steadily rising over the past five years, but once stay-at-home orders were implemented nationwide, search volume dropped sharply. On the other hand, as people sought alternative options for personal behavioral health services, searches for “tele-mental health” rose rapidly at the end of the first quarter.

Google Searches for “Mental Health” in the United States, 2015–H1 2020Image from Rock Health

Digital behavioral health companies have received substantial funding in recent years. This has, to some extent, enabled the industry to address this shift in consumer demand, allowing those who have already developed scalable solutions to deliver novel, technology-driven behavioral health services.

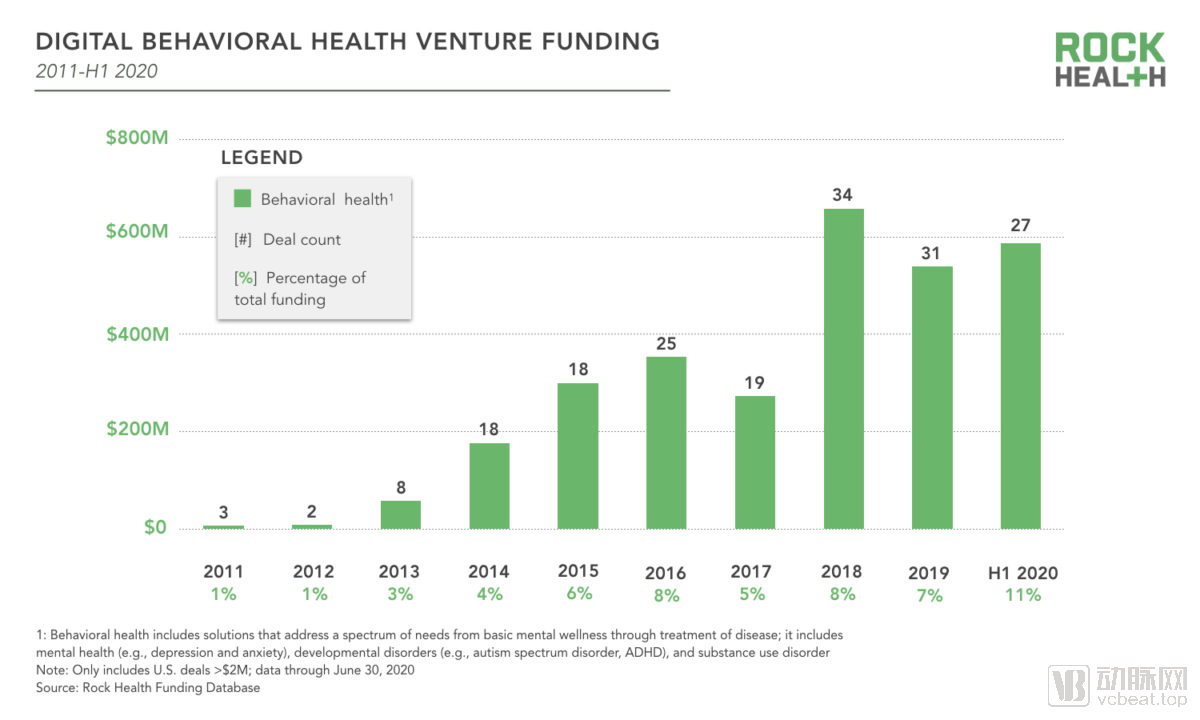

In the first half of 2020, digital behavioral health companies secured $588 million in funding, roughly equivalent to the total annual financing raised by the sector in any previous year (total behavioral health funding for the prior three years: $539 million in 2019, $658 million in 2018, and $273 million in 2017). Capital flowed toward companies with product-driven offerings, ranging from fully automated chatbots to video conferencing platforms facilitating patient-provider interactions. In the first half of 2020, the majority of funding was directed to digital behavioral health companies providing the following two types of services:

1. Capable of providing remote treatment solutions for patients with acute and chronic diseases

2. Clinical treatment (e.g., Lyra Health) or non-clinical services (e.g., Headspace)

2011–2020 H1 Digital Behavioral Health Investment, image from Rock Health

The following three companies raised the most funding, accounting for 54% of total behavioral health financing.

1. Headspace raised $140 million through two rounds of financing ($100 million in equity financing and $40 million in debt financing) to continue building its mindfulness meditation app.

2. Mindstrong has developed an application that pairs patients with a range of service providers to deliver personalized mental health care, while leveraging smartphone interaction patterns to track digital biomarkers for mood and cognition. The company completed a $100 million Series C financing round.

3. Lyra Health aims to provide users with customized behavioral and mental health care services, either remotely or in-person, through its own network, along with self-care courses and exercises. The company completed a $75 million Series C financing round.

The surge in financing has accelerated the rapid maturation of this sector. Although this may complicate the market for corporate and individual customers in the short term, healthcare companies with proven business models, clinical outcomes, and cultural competitiveness will stand out in the growing market.

Alyssa Jaffee, Vice President at 7wire Ventures, believes that the market for low-to-moderate acuity behavioral health is already highly saturated, but significant opportunities remain for companies addressing high-acuity mental and behavioral health issues.

Rock Health Predicts:

1. Macroeconomic conditions will play a significant role in the second half of 2020, but their impact on the digital health sector will be less pronounced than in other economic sectors.

2. They anticipate that macroeconomic turbulence will continue to spur interest among corporate buyers, consumers, and investors in healthcare digitalization, a trend that can offset the negative impact of the recession in the first half of the year. The “flight to quality” phenomenon observed among investors during this period is also expected to persist.

3. Not all digital health companies are the same. Compared with other industries, digital health startups that sell products to suppliers and employers may face more obstacles.

4. If financial system instability recurs, as it did during the previous recession, this industry or independent startups will be relegated to a secondary position.