31 Healthcare IPOs in H1 2020 Triple Combined Market Cap: Key Innovators to Watch

July 2020 was a month that Chinese investors would remember, as all four major A-share stock indices saw increased trading volumes and rose. The Shanghai Composite Index gained 5.71%, surpassing the 3,300-point mark, reigniting expectations for a move toward 3,500 points. Over the past half-month, the capital market, serving as a barometer of the real economy, has repeatedly sent positive signals. From an investment perspective, the turning point of the year appears to be emerging.

Recently, VCBeat conducted a systematic review of the initial public offerings (IPOs) of healthcare projects in the first half of 2020 and their post-listing performance, aiming to identify key trends worthy of continued attention.

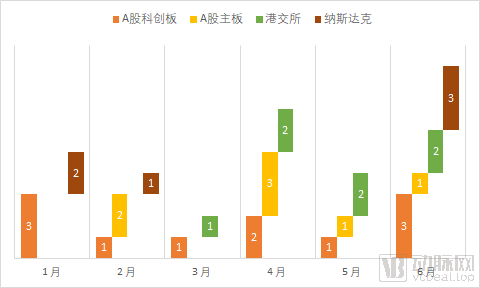

Over the past six months, a total of 31 healthcare projects have entered the capital markets, with new domestic healthcare listings appearing on the A-share Main Board, the STAR Market, the Hong Kong Stock Exchange, and NASDAQ. At least two healthcare companies completed their initial public offerings (IPOs) each month. June was the most active month for IPOs in the first half of the year, and the number of IPOs in the second quarter was significantly higher than in the first quarter.

Monthly Distribution of IPO Healthcare Projects in the First Half of the Year (Data Source: East Money Choice, as of June 30, 2020)

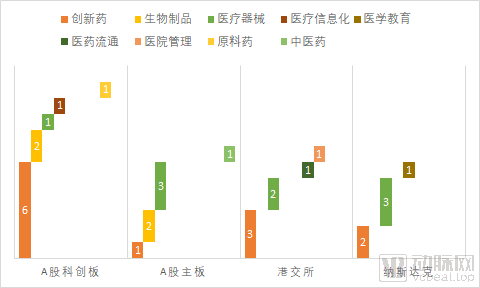

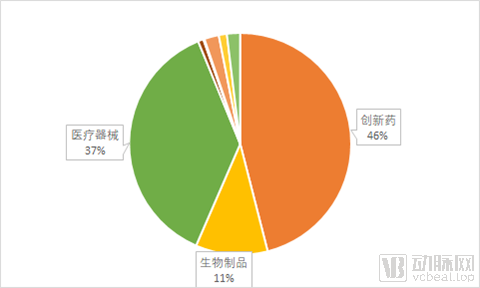

31 healthcare IPOs spanned seven subsectors: innovative drugs, medical devices, biologics, pharmaceutical distribution, hospital management, active pharmaceutical ingredients (APIs), and traditional Chinese medicine. Among these, innovative drug companies had the highest number of listings, followed by medical device companies.

Distribution of IPO Healthcare Projects by Sub-sector in the First Half of the Year (Data Source: East Money Choice, as of June 30, 2020)

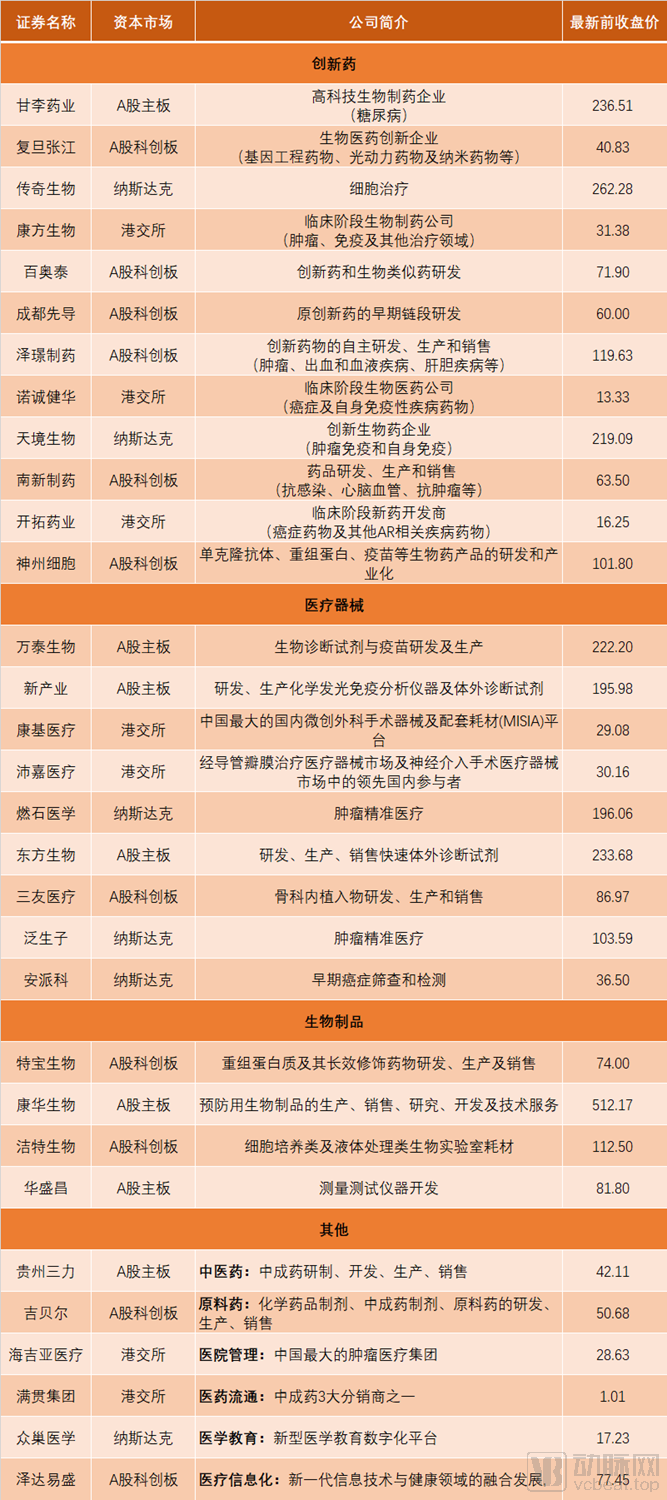

We have listed the full project inventory below:

Complete List of 31 IPO Projects (Data sourced from East Money Choice; market data as of July 15, 2020)

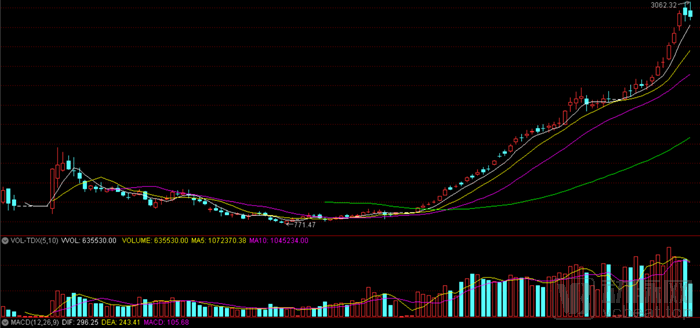

To clearly assess the overall post-listing performance of these new entrants in the capital market, we did not directly analyze the daily trading data of individual stocks. Instead, we aggregated the stock price movements of the aforementioned 31 companies over the past six months and constructed a new market index using total market capitalization as weights, following the methodology of the Shanghai Composite Index. This index uses January 20, 2020—the first trading day after the listings of Tebao Biology and Tianjing Biology, the earliest IPOs among the group in 2020—as its base date, with a starting value of 1,000 points.

Market Performance Index of 31 IPO Projects (Data from Tongdaxin; market data as of July 15, 2020)

As of July 15, the date on which we extracted the data, this index had risen to 2,905.73 points, with a low of 771.47 points and a high of 3,062.32 points during the period. In other words, healthcare companies listed in the first half of 2020 have collectively tripled their total market capitalization.

Since 2018, as an innovative initiative to establish a multi-tiered capital market, the Hong Kong Stock Exchange (HKEX) and the Shanghai Stock Exchange (SSE) have successively adjusted their listing rules, opening the door for a large number of unprofitable technology companies to go public. In June 2020, the ChiNext board of the Shenzhen Stock Exchange (SZSE) also launched reforms, officially kicking off the pilot registration-based IPO system. Under the latest rules, for unprofitable enterprises, the ChiNext board will eliminate the existing requirement that “there be no accumulated deficits in the most recent period” after a one-year transition period. It is conceivable that competition among major capital markets to secure high-quality, high-tech projects will intensify in the future.

Public annual reports show that among the 31 IPO projects, only Kangji Medical, Mangoo Group, and Hygeia Healthcare generated pre-tax profits in the previous financial period.The fact that the majority of IPO projects are unprofitable means that analyzing most targets in the emerging secondary market still requires adopting certain primary market methodologies. Moving forward, we will leverage data such as market capitalization, stock price fluctuations, average growth rates, and price-to-research ratios to identify noteworthy projects in the pharmaceutical and medical device sectors, and analyze their respective strengths and weaknesses.

Additionally, it should be noted that since most projects have not generated pre-tax profits or revenue, we adopted the industry-standard “Price-to-R&D Ratio” (R&D Expenses / Latest Market Capitalization) to assess the innovativeness and growth potential of the projects from the perspective of R&D investment.

In the primary market, project valuation levels are a closely watched indicator. Therefore, we first analyzed the average valuation of 31 healthcare projects categorized by sub-sector. The data shows that medical device projects topped the seven major sub-sectors with an average valuation of RMB 27.946 billion, followed by biological products projects at RMB 27.817 billion, and innovative drug projects in third place at RMB 23.099 billion.

In terms of industry trends, the traditional innovation model of import substitution remains a key rationale supporting Chinese-made innovative medical device projects in accessing capital markets and achieving high valuations. More than half of the medical device companies that went public in the first half of the year—including Wantai Biological, Kangji Medical, Peijia Medical, Snibe, Orient Gene, and Sanyou Medical—are advancing their product commercialization along the path of import substitution. For star IPO candidates such as Wantai Biological, Peijia Medical, and Kangji Medical, investors often estimate the growth potential of substitute products based on the market size of the targeted foreign blockbuster devices, thereby driving high valuations and market capitalization growth.

Secondly, domestically produced high-end medical devices have entered a period of capital realization, with heavily invested sectors such as cardiovascular and orthopedics beginning to yield results. High-end domestic medical devices have long been a key focus for early-stage investors. The successful public listings of Kangji Medical, a developer of minimally invasive surgical instruments; Peijia Medical, a developer of interventional devices; and Sanyou Medical, a developer of orthopedic implants, serve to validate the investment thesis of these institutions.

Third, a cluster of tumor NGS projects have gone public, eliciting mixed reactions from the capital market. In the first half of the year, Burnt Rock Medicine and Genetron Health, two precision oncology companies, launched their IPOs in quick succession, creating a brief surge of excitement within medical professionals’ social circles. Behind these listings, rumors have circulated that more similar projects are preparing to go public. As the most promising segment in the NGS field following NIPT (Non-Invasive Prenatal Testing), tumor NGS has undoubtedly attracted significant attention. Nearly all healthcare investors have reviewed such projects to varying degrees, and almost every healthcare investment fund has considered, at some point, entering the tumor NGS space. Amidst fierce market competition driven by product innovation and iteration, and vigorous efforts to break through in the capital markets, tumor NGS has become a focal point of concern. The evaluation criteria applied by investors in the NASDAQ market may well hinge on the assessment of a company’s ability to achieve market exclusivity.

Last but not least, the impact of the COVID-19 pandemic on the healthcare industry has been fully transmitted to the capital markets. This is evident in the concentrated listings of companies related to diagnostics and vaccines. For instance, Wantai Biological, New Industries, Orient Gene, and Ampak Technology are all stocks associated with the diagnostics concept, with Wantai Biological also pursuing a vaccine-focused strategy.

Medical Device Project Analysis (Data sourced from East Money Choice; market data as of July 15, 2020)

Wantai Bio, which listed on the main board of China’s A-share market in April, became a star stock in the pharmaceutical and biotechnology sector with 28 consecutive daily limit-ups within its first 50 days of trading. In our compiled ranking of medical device companies, Wantai Bio tops the list with a market capitalization of $71.605 billion and a surge of 1,932.11%, which is why we focus on it in this article.

Wantai Bio primarily operates in the businesses of in vitro diagnostic reagents (98%) and vaccines (2%). Just one week before its initial public offering, WanTai Bio’s bivalent HPV vaccine, Xinning, received the Biological Product Lot Release Certificate from the National Medical Products Administration (NMPA), marking its official market launch. Compared with imported HPV vaccines, Xinning leverages its lower price as a competitive advantage, demonstrating strong competitiveness in the mid- to low-end market segments. In China, demand for HPV vaccines remains robust. However, following the approval and entry of Merck’s quadrivalent HPV vaccine into the Chinese market, the market share of bivalent HPV vaccines has been significantly eroded.

In fact, measured by revenue share (RMB 1.184 billion in 2019), Wantai Bio’s core business was not vaccines (2%), but in vitro diagnostic (IVD) reagents (98%). Among these, enzyme-linked immunosorbent assay (ELISA) reagents and chemiluminescence reagents were the primary sources of income, accounting for 39% and 19%, respectively, with production-to-sales ratios approaching 100%. This segment of routine IVD reagents has long been a mature and highly competitive market, leading directly to elevated selling expenses; from 2016 to 2019, Wantai Bio’s selling expense ratio remained near 30%.

However, data from Shiyanlv indicates that Wantai Bio’s R&D investment is at a relatively strong level compared with medical device companies that went public during the same period. According to the prospectus, the company’s nine-valent HPV vaccine is currently in Phase II clinical trials. In China, its main competitors are Kelun-Weishi Biopharmaceutical, which is also in Phase II clinical trials, and Shanghai Bowei, which is conducting Phase III clinical trials.

As the hype around the bivalent HPV vaccine subsides, short-term control of sales expenses for in vitro diagnostic reagents and long-term development of innovative products may both be issues that investors in Wantai Bio need to consider.

In mid-May, Peijia Medical, one of the four domestic developers of transcatheter aortic valve replacement (TAVR) products in clinical stages, listed on the Hong Kong Stock Exchange. Founded by former executives from Medtronic, Otsuka China, and MicroPort Scientific, this high-tech company has attracted attention from top-tier investment institutions since its inception. Eight years after its establishment, Peijia Medical went public as a leading developer of medical devices for transcatheter valve therapies and neurointerventional procedures in China. The company garnered significant interest throughout its journey, with pre-IPO subscriptions exceeding 5,000 times, making it the “frozen capital king” of the first half of the year.

In this article, Peijia Medical has drawn our attention due to its price-to-research ratio of 1,057.02x. After all, once a company enters the secondary market, investor scrutiny of its products and market potential increases significantly. Clearly, Peijia Medical’s R&D intensity is far above the industry average and several times higher than that of other medical device companies with similar market capitalizations on the list.

Cardiovascular disease has long been the “leading killer” of elderly health. Against the backdrop of accelerating global aging, the future demand for minimally invasive interventional procedures, with their increasingly mature techniques, goes without saying. According to statistics, in 2018, the global number of patients eligible for TAVR was approximately 3 million, with around 120,000 procedures performed. In China, the corresponding patient population was approximately 700,000, with only about 1,000 procedures carried out, indicating substantial room for growth.

Previously, Peijia Medical had already launched TaurusOne®With nearly RMB 100 million invested in its development, this product was specially designed with diverse features to meet the needs of doctors and patients in China. In 2017, it received the “Innovative Medical Device” designation from the National Medical Products Administration (NMPA), thereby qualifying for the expedited review pathway. Currently, Peijia Medical is collaborating with six hospitals on TaurusOne® to conduct confirmatory clinical trials involving 125 patients.

On the other side of the coin, in terms of progress, Peijia Medical’s core focus area, TAVR, is not among the frontrunners. Domestic TAVR manufacturers such as Venus Medtech, Jiecheng Medical, and MicroPort CardioFlow have already obtained product approvals, and Edwards Lifesciences, the international benchmark company, has also recently secured approval for its products. Peijia Medical’s product lags behind by approximately one year. However, previously launched products have captured only a small share of the overall market, leaving Peijia Medical an opportunity to bridge the gap in timing through its technological advantages. In other words, for secondary market investors, the clinical trial results that Peijia Medical will announce in the future are critically important.

Sanyou Medical was the only medical device company to list on the SSE STAR Market in the first half of the year, bringing it into our analytical focus. With its core business centered on the R&D, manufacturing, and sales of implantable consumables for orthopedic surgery, Sanyou Medical is a leading player in China’s spinal implant consumables sector and one of the few companies capable of original innovation driven by clinical needs. Given the substantial demand in China’s orthopedic market, Sanyou Medical’s spinal product series ranked third among domestic enterprises and sixth in the overall market in 2018.

Although its performance in the capital markets has not been particularly striking, Sanyou Medical’s innovation capability is worthy of close attention. With a market cap-to-R&D ratio of 812.01, Sanyou Medical ranked first among A-share STAR Market listings in the first half of the year and second among medical device projects. In its prospectus, Sanyou Medical also stated that the proceeds from its IPO are intended for investments in projects such as expanding production capacity for orthopedic implants, establishing an orthopedic product R&D center, and building its marketing network.

Qiming Venture Partners is an early investor in Sanyou Medical and its largest shareholder after a six-year journey. Hu Xubo, Managing Partner at Qiming Venture Partners, stated in an interview with the media that the firm’s initial rationale for investing in Sanyou Medical was its capability to achieve domestic substitution of high-end medical devices. The goal is to leverage high-quality Chinese brands and products to reduce healthcare costs and enhance the accessibility of orthopedic medical services.

However, against the backdrop of long-standing reliance on imports, foreign medical device brands such as Johnson & Johnson, Medtronic, and Stryker still hold over 60% of the market share for orthopedic spinal implant consumables. For Sanyou Medical, the pressing challenge is to ensure that the quality of its flagship products surpasses that of imported counterparts, thereby achieving genuine substitution with domestically produced alternatives.

In the segment of domestically produced high-end medical devices, another target that must be mentioned is Hygeia Healthcare. This project, which listed on the Hong Kong Stock Exchange as China’s largest oncology healthcare group, operates in China through its wholly-owned subsidiary, Gamma Star Medical, a manufacturer of gamma-ray equipment.

Gamma Star Medical’s flagship product, the GyroKnife, utilizes a rotation principle similar to that of aerospace gyroscopes and was independently developed in 2004 by Song Shipeng, then Chairman of Gamma Star Medical Group. According to the prospectus, Hygeia Healthcare’s business can be divided into three segments: hospital operations (accounting for 87% of revenue in 2019), third-party radiotherapy services (with the highest gross profit margin at 64.6%), and hospital management services.

Alongside the development of its proprietary hospitals and intensive acquisitions in recent years, Hygeia Healthcare has established more than 50 chain oncology medical institutions across multiple provinces and municipalities in China, including Shanghai, Beijing, Chongqing, Sichuan, Guangdong, Jiangsu, Hunan, Hubei, Shandong, Liaoning, Henan, Hebei, Jiangxi, Fujian, Heilongjiang, Guangxi, Yunnan, Guizhou, and Shaanxi. These institutions integrate diagnostic, therapeutic, and research functions.

However, half of Hygeia Healthcare’s revenue over the past year came from its self-built Shanxian Hospital and the acquired Suzhou Canglang Hospital. Unlike most domestically produced high-end medical equipment developers that have recently gone public, although Gamma Knife production remains its core underlying technology, the issue Hygeia Healthcare needs to address in its next stage of development is no longer the commercialization of its products, but rather how to optimize its operational sustainability while expanding its hospital management footprint.

Burning Rock Biotech, which listed on the Nasdaq in early June, was another star project of the first half of the year. Under the spotlight of holding the “first license” for tumor genetic testing and being the “first stock” in precision oncology services, Burning Rock Biotech experienced a small surge in its share price after its IPO. By the end of the first half of the year, it maintained a market capitalization of RMB 19.272 billion and an average share price growth rate of 0.49%, becoming the only Chinese medical device company whose stock price remained up among those that listed on the Nasdaq during the period.

Burning Rock Biotech focuses on oncology next-generation sequencing (NGS) services and product development, conducting its business through two models: the central laboratory model, where hospitals send patient samples to the company’s laboratories for testing (accounting for 72.4% of revenue), and the in-house hospital model, where the company assists hospitals in establishing internal laboratories and building NGS testing platforms while providing training and support, followed by recurring sales of its testing products (accounting for 23% of revenue).

In recent years, Burning Rock Biotech has experienced rapid revenue growth, securing the leading position in China’s tumor gene sequencing market with a 26.7% market share. In 2019, the number of tests conducted through Burning Rock’s central laboratory model exceeded 20,000. Furthermore, Burning Rock offers a portfolio of 13 products; in July 2018, its “Human EGFR/ALK/BRAF/KRAS Gene Mutation Combined Detection Kit” became the first product of its kind to receive marketing approval from the National Medical Products Administration (NMPA).

Another oncology NGS company, Genetron Health, went public one week after Burning Rock Biotech. It is understood that Genetron Health primarily operates three major business segments: diagnosis and monitoring, early cancer screening, and pharmaceutical services (drug R&D services). Its glioma panel testing business has long held the largest market share in this niche segment. The IDH1 and TERT gene detection kits for gliomas and the 8-gene detection kit for lung cancer were approved for market launch in 2017 and 2020, respectively.

Beyond its diagnostic reagent products, Genetron Health has been committed to the development of proprietary technology platforms, possessing the Genetron S5, Genetron S2000, and 3D Genetron biochip readers. During the COVID-19 pandemic, despite a decline in revenue from NGS-based LDT services, the company achieved a 15.3% year-on-year increase in total operating revenue compared to the same period in 2019, driven by growth in IVD business revenue.

It was reported that Genetron Health’s sequencer, the Genetron S5, was deployed in hospitals such as Huoshenshan Hospital, and its coronavirus (COVID-19) detection kit, launched in February 2020, rapidly received regulatory approval for market release.

In China, it is an undisputed fact that the tumor gene sequencing market has become a red ocean. Between 2016 and 2018, a large number of tumor gene sequencing service providers emerged in the domestic market. Unwilling to engage in homogeneous competition, these companies sought breakthroughs through innovations in products and service models. In the future, new product developments—such as regulatory approval of tumor immune response prediction kits and independent innovation in sequencing platforms—as well as new service models, such as precision medicine collaborations with pharmaceutical companies for new drug development, will test the sustainable growth capabilities of both Burning Rock Biotech and Genetron Health.

Beyond sheer numbers, when assessed by total market capitalization, innovative drug projects still command the highest aggregate market value among all seven sub-sectors, accounting for 446%. If biologics, traditional Chinese medicine (TCM), and active pharmaceutical ingredients (APIs) are included, the latest market capitalization of biomedical projects accounts for half of the total market value of the 31 projects.

Market Capitalization Distribution of 31 Projects (Data sourced from East Money Choice; market data as of July 15, 2020)

Regarding industry trends. In the first half of 2020, innovative oncology drug projects witnessed a second wave of IPO activity. Unlike the previous IPO boom, which was dominated by large-molecule innovative oncology drug companies such as Junshi Biosciences and Innovent Biologics, the companies that went public in the past six months—namely Zeltex Pharmaceuticals, I-Mab Biopharma, Novalix Therapeutics (InnoCare Pharma), and Kintor Pharmaceutical—have primarily focused their R&D pipelines on small-molecule innovative oncology drugs.

Analysis of Innovative Drug Projects (Data Source: East Money Choice; Market Data as of July 15, 2020)

The second noteworthy industrial trend is that, with the commercialization and market expansion of earlier-stage large-molecule drugs—particularly innovative oncology therapeutics—domestic upstream raw material suppliers and providers of ancillary products for new drug development have achieved new breakthroughs in the capital markets. Companies such as Amoytop Biotech, which specializes in recombinant protein development, and Jet Biofil, which supplies cell culture laboratory consumables, have successfully listed on capital markets and secured favorable valuations.

Third, diabetes drug-related targets continue to attract attention from the capital market. As one of the diseases with the highest prevalence globally, diabetes has always been a key focus of research and development for pharmaceutical companies. Recently, Gan & Lee Pharmaceuticals, one of the three major domestic suppliers of recombinant insulin analogs in China, listed on the Shanghai Stock Exchange, achieving full listing coverage among major Chinese insulin manufacturers.

Fourth, immune cell therapy projects have begun to enter the market and raise capital. Immune cell therapy is one of the few biomedical sectors in China that can keep pace with global leading competitors in terms of technological R&D progress. With numerous participants and many breakthroughs, the field remains subject to significant controversy as specific regulatory policies have yet to be introduced. Legend Biotech has long been a star project in the immune cell therapy sector. From being among the first to enter clinical trials, to facing skepticism over its clinical data, and ultimately becoming the first publicly listed Chinese company specializing in immune cell therapy, Legend Biotech’s story of continuously driving the advancement of domestic immune cell therapy will be remembered by the market, regardless of the project’s own development prospects. In addition, Sinocelltech, which focuses on differentiated novel monoclonal antibody drugs, has also laid out a pipeline for cell therapy.

Gan & Lee Pharmaceuticals, which went public just before the end of the first half of the year, has emerged as another star in the capital market. With a market capitalization of RMB 48.677 billion, it topped the H1 IPO list for innovative drugs, while its average stock price growth rate of 10% was the highest among all IPO projects during the same period.

Gan & Lee Pharmaceuticals has focused on the research and development of third-generation insulin drugs, emerging as a leader in China’s niche diabetes medication market and a long-term portfolio company of Qiming Venture Partners. In fact, domestic biopharmaceutical companies have maintained strong enthusiasm for developing diabetes medications, whether for generic drugs (such as metformin) or innovative therapies (such as DPP-4 inhibitors). Dr. Gan Zhongru, founder of Gan & Lee Pharmaceuticals, participated in the development of China’s first genetically recombinant human insulin and has since remained dedicated to the R&D, process optimization, and industrial-scale production of insulin-based therapeutics.

According to reports, in 2005 and 2007, Dr. Gan Zhongru led a research team in completing the development of China’s first rapid-acting recombinant insulin analog, “Suxiulin,” and long-acting recombinant insulin analog, “Changxiulin,” making China one of the few countries in the world capable of industrialized production of recombinant insulin analogs.

In 2019, the insulin market size in China was approximately RMB 20 billion. Currently, domestic manufacturers of recombinant insulin analogs include three foreign pharmaceutical companies—Sanofi, Eli Lilly, and Novo Nordisk—and three Chinese pharmaceutical companies—Gan & Lee Pharmaceuticals, The United Laboratories, and Tonghua Dongbao. Among them, Gan & Lee Pharmaceuticals’ four recombinant insulin analog products cover three niche market segments based on insulin action profiles: long-acting, rapid-acting, and intermediate-acting. Leveraging its first-mover advantage among domestic enterprises, the company has gained a strategic edge in import substitution.

By the end of 2019, Gan & Lee Pharmaceuticals’ products were sold in nearly 7,700 hospitals at or above the county level across China, including more than 2,400 tertiary hospitals. However, first- and second-generation insulins still dominate clinical practice in China. How third-generation insulins can displace these earlier generations to capture market share may well be the key challenge facing Gan & Lee Pharmaceuticals as it advances its industrialization efforts.

Zelgen Biopharmaceuticals, which went public in January, is the first unprofitable biopharmaceutical company to list on the STAR Market of the Shanghai Stock Exchange. It is an innovation-driven enterprise dedicated to the research and development of novel chemical and biological drugs, focusing on multiple therapeutic areas including oncology, hemorrhagic and hematologic diseases, and hepatobiliary disorders. Its core product, donafenib, is a Class 1 innovative drug indicated for various cancers such as hepatocellular carcinoma, colorectal cancer, and differentiated thyroid cancer. It is also the first domestically developed targeted new drug in China to initiate Phase III clinical trials for the first-line treatment of advanced hepatocellular carcinoma.

In addition, InnoCare Pharma, founded by Professor Shi Yigong, listed on the Hong Kong Stock Exchange in March, emerging as one of the most closely watched star projects among the many innovative drug companies that went public in the first half of the year. With a market cap-to-R&D ratio of 13,779.84, it topped the list for IPOs in the innovative drug sector during this period. InnoCare Pharma is a clinical-stage biopharmaceutical company focused on developing drugs for cancer and autoimmune diseases. Its selection of disease indications bears considerable similarity to those of Zeltzys Pharmaceuticals, Akeso, I-Mab, and Kintor Pharmaceutical, which also went public around the same time.

When evaluated based on the price-to-research ratio, investing in InnoCare Pharma offers better value for money compared to other innovative drug projects in the clinical stage. However, the price-to-research ratio only measures innovation input and does not guarantee innovation output. To analyze the competitiveness of innovative drug projects, it is also necessary to conduct peer comparisons focusing on R&D progress, leading drug candidates, and indications.

Research Progress of Innovative Drug Projects (Data Compiled from Public Sources, as of June 30, 2020)

Zelgen Biopharmaceuticals is known as the “mini-Betta.” Its independently developed novel small-molecule multi-target drug, donafenib, is primarily indicated for first-line treatment of advanced hepatocellular carcinoma. However, this therapeutic area is not devoid of existing clinical options. Currently, two drugs in the same class have been approved globally for this indication: sorafenib from Bayer (Germany) and lenvatinib from Eisai (Japan), which were approved for marketing in China in 2008 and 2018, respectively. Notably, sorafenib was included in the National Reimbursement Drug List in 2017.

Furthermore, following the expiration of the Chinese patents for sorafenib and lenvatinib in 2020 and 2021, respectively, generic versions from companies such as Qilu Pharmaceutical, Chia Tai Tianqing, and Kelun Pharmaceutical are set to enter the market sequentially. Second-line agents like cabozantinib and Keytruda are also gaining traction in the treatment of advanced hepatocellular carcinoma, placing considerable R&D and commercialization pressure on Zeltis Pharma.

InnoCare Pharma’s core product is orelabrutinib, for which clinical Phase II studies targeting relapsed chronic lymphocytic leukemia (CLL), relapsed small lymphocytic lymphoma (SLL), and relapsed mantle cell lymphoma (MCL) have been largely completed. Currently, three drugs in the same class have been approved globally: Johnson & Johnson’s ibrutinib, AstraZeneca’s acalabrutinib, and BeiGene’s zanubrutinib. Among these, only Johnson & Johnson’s ibrutinib has received marketing approval in the Chinese market, while acalabrutinib and zanubrutinib have been approved for marketing in the United States.

From a timing perspective, orelabrutinib does not hold a first-mover advantage; however, its higher selectivity and stability compared to other competitors result in fewer side effects, thereby establishing its own competitive edge. Specifically, while the other three BTK inhibitors all adopt fused bicyclic cores, orelabrutinib features an ingenious monocyclic design. As a result, orelabrutinib significantly reduces off-target effects, with a much lower probability of adverse reactions than the other three marketed products.

At the time of its IPO, Akeso Biopharma saw subscription levels exceed 600 times, making it the “frozen capital king” before Peijia Medical emerged. As the only company among the aforementioned five innovative drug enterprises engaged in PD-1-related development, Akeso Biopharma has pursued differentiated strategies in the PD-1 market, which is increasingly becoming a red ocean. These strategies include combination therapies targeting PD-(L)1/CTLA-4, monoclonal antibodies against the IL-12/IL-23 targets, and bispecific antibodies targeting PD-1/VEGF.

Globally, only one PD-(L)1/CTLA-4 combination therapy has been approved, while five PD-(L)1/CTLA-4 bispecific antibody programs are in clinical development. In China, no PD-(L)1/CTLA-4 bispecific antibodies have yet received marketing approval; only two such candidates—Alphamab Oncology’s KN046 and Akeso’s AK104—are currently in clinical trials.

Akeso Biopharma has developed the first monoclonal antibody targeting IL-12/IL-23 by a Chinese domestic company, which demonstrates superior efficacy, safety, and ease of use compared to the first-generation TNF-α inhibitors. Among similar products in development, the most clinically advanced is AstraZeneca’s briakinumab, for which a New Drug Application (NDA) was submitted to the FDA in 2019 for the treatment of plaque psoriasis. Additionally, Akeso has pioneered a PD-1/VEGF bispecific antibody for the treatment of patients with advanced solid tumors, which is currently undergoing Phase I clinical trials in Australia. The drug received Investigational New Drug (IND) approval from the FDA in June 2019 and is poised to initiate Phase I clinical studies in the United States.

On its official website, I-Mab Biopharma distinctly showcases its China assets and global assets separately, a distinctive approach that reflects its novel drug development strategy, which differs from those of other innovative pharmaceutical companies. The China assets are derived from license-in agreements, covering Greater China rights to drugs targeting CD38, IL-6, IL-7, B7-H3, C5aR1, and other targets; its partners include MorphoSys, MacroGenics, Genexine, and Ferring Pharmaceuticals. The global assets stem from in-house R&D, including drugs targeting CD47, CD73, GM-CSF, CXCL13, and other targets.

This approach not only diversifies I-Mab’s pipeline of investigational drugs and accelerates the market launch of new therapies, but also fully leverages I-Mab’s drug development capabilities to secure a first-mover advantage in commercialization. However, sustaining such an extensive product portfolio over the long term will inevitably require substantial financial investment and support. After all, for pharmaceutical companies, achieving commercialization is the more critical objective in expanding their R&D pipelines.

Kintor Pharmaceutical’s lead investigational drug, proxalutamide, is a potential best-in-class therapy currently undergoing Phase III clinical trials in China for metastatic castration-resistant prostate cancer (mCRPC), as well as Phase II clinical trials in the United States and clinical trials for breast cancer. The company’s pipeline of investigational drugs targets major cancer types with significant market potential and other androgen receptor (AR)-related diseases. According to a Frost & Sullivan report, prostate cancer was the second fastest-growing major cancer type in China in terms of new case growth rate from 2014 to 2018, while breast cancer was the most common cancer among women worldwide in 2018.

For Kintor Pharmaceutical, verifying that prochlorperazine is best-in-class and achieving commercialization remain severe challenges.

Due to space constraints, we are unable to provide a detailed analysis of each individual project. In early July, while we were preparing this manuscript, several healthcare companies—including Tinavi Medical Technologies, Hepalink, Ocumension Therapeutics, Yatai Bio, Hongli Medical Management, and Junshi Biosciences—listed on the STAR Market or the Hong Kong Stock Exchange. We will review these listings in our year-end roundup for 2020. We believe that every project entering the capital markets possesses unique advantages as well as distinct challenges. In an efficient capital market, the interplay between these strengths and weaknesses will ultimately determine market valuation trends. We also hope that every innovative project that has navigated the darkness of early-stage entrepreneurship and overcome the thorny path of startup development, finally stepping into the public eye, will continue to make steady progress toward meeting expectations.