Junshi Biosciences Surges Over 200% on STAR Market Debut; Toripalimab Marks 18-Month Milestone with Expanding Indications and Commercial Progress

Junshi Biosciences

Innovative Drug Developer

On July 15, 2020, Junshi Biosciences successfully listed on the STAR Market, becoming the first company to transfer from the NEEQ (National Equities Exchange and Quotations) to the STAR Market while simultaneously maintaining its listing in Hong Kong. A year and a half earlier, Junshi Biosciences was also the first to benefit from new listing policies, becoming the first biopharmaceutical enterprise with a “NEEQ + H” share structure.

Junshi Biosciences priced its IPO at CNY 55.5 per share, issuing a total of 87.13 million shares. The gross proceeds amounted to CNY 4.836 billion, with net proceeds reaching CNY 4.497 billion, significantly exceeding the originally planned fundraising target of CNY 2.7 billion.

At today’s market open, Junshi Biosciences opened at RMB 216 per share, representing a 289.19% increase over its offering price. As of 9:52 a.m., the stock was trading at RMB 180 per share, up 224.32% from its offering price.

As one of the few innovative pharmaceutical companies in China to have successfully launched its products, Junshi Biosciences has emerged as a leading player in the biopharmaceutical sector. Its stock price on the Hong Kong Stock Exchange has also been on a steady rise over the past six months. By the close of trading on July 14, 2020, the share price of Junshi Biosciences on the Hong Kong Stock Exchange had climbed to HK$62.850, representing a 135.4% increase from its opening price at the beginning of the year.

So, over the past year and a half, have the plans outlined at the time of the Hong Kong Stock Exchange listing been implemented one by one? For Tuoyi, which failed to be included in the National Reimbursement Drug List, did its sales remain robust in 2020? What other blockbusters are in Junshi Biosciences’ pipeline?

Good news from Junshi Biosciences keeps coming in quick succession.

Just before its listing on the Hong Kong Stock Exchange, Junshi Biosciences’ first product, Tuoyi (toripalimab), received approval from the National Medical Products Administration for market launch, becoming the first domestically produced PD-1 monoclonal antibody to be marketed in China. It is indicated for locally advanced or metastatic melanoma after failure of prior standard therapy, positioning it as a direct competitor to Merck’s Keytruda.

On the eve of its listing on the STAR Market, Junshi Biosciences applied to the Hong Kong Stock Exchange under Rule 18A.12 and obtained approval to remove the “B” suffix from its stock code.

The “B” suffix for Hong Kong-listed companies denotes “pre-profit biotechnology listed companies,” serving as a warning to investors that these entities may carry higher risks. With stable management and actual control, a market capitalization of nearly HK$50 billion (as of July 14), and RMB 775 million in revenue in 2019, Junshi Biosciences fully meets the market capitalization/revenue test under Rule 8.05(3) of the Hong Kong Stock Exchange Listing Rules and no longer requires the “B” marker.

Although it merely involved removing a small “hat,” this signifies that Junshi Biosciences has transitioned from its startup phase, which relied entirely on financing for development, into a rapid growth stage driven by stable revenue.

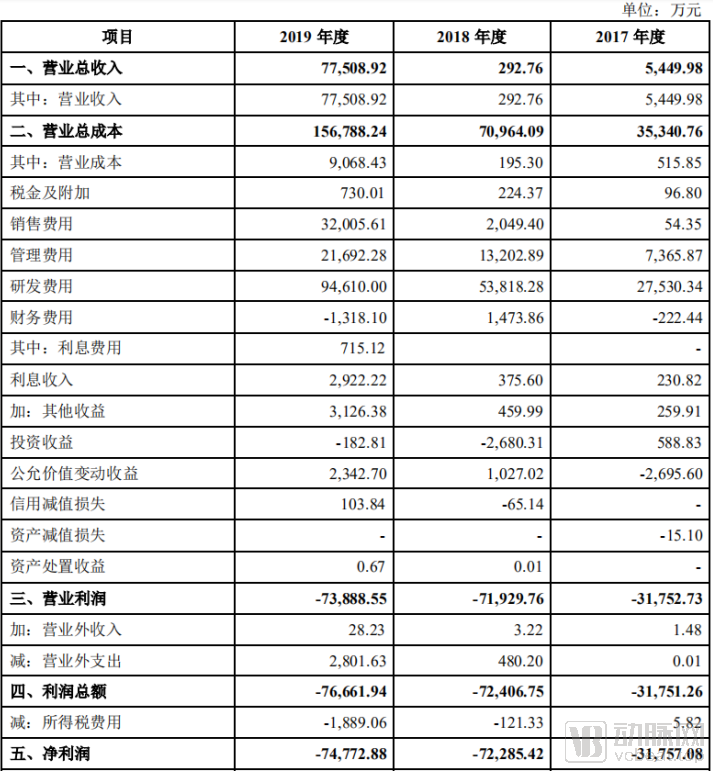

Selected Financial Data of Junshi Biosciences (2017–2019)

Although Junshi Biosciences has generated revenue and removed its “loss-making” label, it remains in a loss position. Due to the concurrent conduct of multiple Phase III clinical trials, the company’s R&D expenditure reached a new high of RMB 946 million in 2019, representing a 75.8% increase from 2018. Despite this rapid growth in R&D spending, Junshi Biosciences managed to contain the scale of its losses. The net loss for 2019 amounted to RMB 748 million, an increase of only 3.46% compared with 2018. The successful containment of losses was primarily attributable to the strong market performance of Tuoyi.

In January 2019, Junshi Biosciences announced the pricing for Tuoyi (toripalimab), with a single 240 mg vial priced at RMB 7,200, resulting in an annual treatment cost of less than RMB 200,000—significantly lower than that of Keytruda (pembrolizumab), which exceeded RMB 600,000 per year. In the subsequent patient assistance program, Junshi Biosciences further demonstrated the cost advantage of its domestically produced PD-1 monoclonal antibody. After accounting for the free-drug provisions, the annual cost of Tuoyi was reduced to only RMB 100,800, less than half the adjusted annual cost of Keytruda. Although Tuoyi failed to be included in the National Reimbursement Drug List during the year-end negotiations, its affordable price has placed it within the financial reach of most patients.

Driven by the strong performance of Tuoyi, Junshi Biosciences achieved total revenue of RMB 775 million in 2019, with a gross profit margin of 88.3%. The company has finally entered its harvest season.

The strong performance of Tuoyi is attributable not only to its pricing and efficacy but also significantly to Junshi Biosciences’ marketing and promotional efforts. Junshi Biosciences has established a 320-member sales team responsible for the commercial promotion of Tuoyi and future products. In 2019, Junshi Biosciences invested RMB 320 million in sales activities, with selling expenses accounting for 41.3% of its revenue. The first year following a new drug’s launch typically requires substantial market education, resulting in an exceptionally high proportion of selling expenses; for instance, Innovent Biologics’ selling expenses reached 66.2% of its revenue in 2019. Junshi Biosciences’ ratio is already at a relatively low level within the industry.

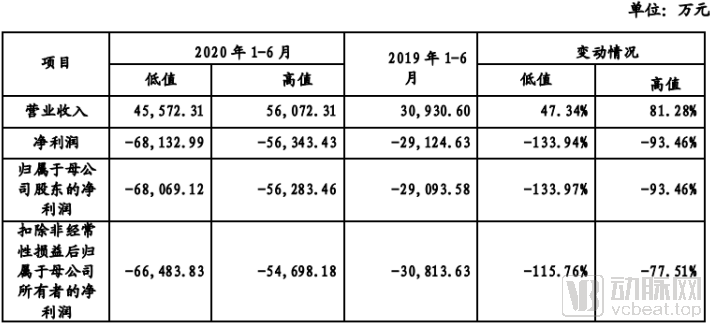

The COVID-19 outbreak in early 2020 had a certain impact on Junshi Biosciences’ clinical trial enrollment, product sales, and production. However, according to the relevant financial data disclosed in its prospectus, Junshi Biosciences still achieved operating revenue of RMB 172 million, the vast majority of which came from sales of Tuoyi. Moreover, R&D investment did not slow down, maintaining a high level of R&D spending at RMB 217 million, resulting in a net loss of RMB 229 million for the first quarter of 2020.

Junshi Biosciences' Performance Forecast for the First Half of 2020

In its latest prospectus, Junshi Biosciences provided a brief forecast of its performance for the first half of 2020. Data indicate that Tuoyi (toripalimab) continued its upward trajectory during this period, generating approximately RMB 500 million in revenue for Junshi Biosciences. On the other hand, after a period of stabilization in 2019, the company’s net loss widened again; Junshi Biosciences projected that its net loss for the first half of 2020 would exceed RMB 500 million, primarily driven by increased R&D expenditures resulting from the concurrent conduct of multiple clinical trials.

It is common for biopharmaceutical companies to burn cash on R&D; the key is that the spending yields corresponding returns. From 2018 to the present, Junshi Biosciences has continuously increased its R&D investment, with the majority of funds raised from its two IPOs directed into the development of corresponding products. So, over the past year and a half, has Junshi Biosciences fulfilled the commitments it made when listing on the Hong Kong Stock Exchange? What is the progress of its pipeline in development?

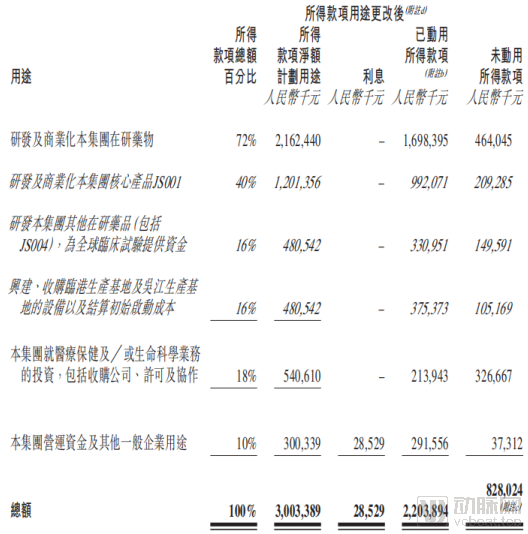

Use of Proceeds from Junshi Biosciences’ HKEX Listing (as of December 31, 2019)

By the end of 2019, Junshi Biosciences had fulfilled the majority of its capital investment commitments made at the time of its listing on the Hong Kong Stock Exchange. In particular, nearly 80% of the funds allocated to new drug research and development have been invested in the original plans, with corresponding outputs already achieved.

Toripalimab remains a key product in Junshi Biosciences’ current pipeline. At the time of its listing on the Hong Kong Stock Exchange, JS001 had just received marketing approval from the National Medical Products Administration (NMPA), with ten additional indications at various stages of clinical trials. Among these, the programs for nasopharyngeal carcinoma and first-line treatment of melanoma were advancing more rapidly and had already entered Phase III clinical trials.

With this launch, the number of key registrational clinical studies being conducted for toripalimab has increased to 15. Upon successful completion of these clinical trials, new indications can be submitted for approval in a phased manner. Toripalimab holds a leading position among domestic peers in indications with high prevalence in China, including non-small cell lung cancer (NSCLC) after failure of EGFR-TKI therapy, neoadjuvant treatment for NSCLC, adjuvant therapy for liver cancer post-surgery, first-line triple-negative breast cancer, and first-line nasopharyngeal carcinoma. New Drug Applications (NDAs) have already been submitted for toripalimab as monotherapy second-line treatment for nasopharyngeal carcinoma and urothelial carcinoma; notably, this represents the world’s first NDA for a PD-1 monoclonal antibody in the treatment of recurrent or metastatic nasopharyngeal carcinoma.

Junshi Biosciences’ other product pipelines are also progressing smoothly. The adalimumab biosimilar has successfully completed clinical trials and is awaiting inspection and approval by the National Medical Products Administration (NMPA). JS002, a PCSK9 monoclonal antibody independently developed by Junshi Biosciences and the first of its kind in China to enter clinical development, has successfully completed Phase II clinical trials and is actively preparing for Phase III clinical trials.

In August 2019, Junshi Biosciences made partial adjustments to the use of proceeds raised on the Hong Kong Stock Exchange, specifically highlighting its independently developed BTLA monoclonal antibody JS004, underscoring its importance in Junshi Biosciences’ pipeline strategy.

BTLA is an important immune checkpoint molecule expressed on activated T and B lymphocytes, possessing a structure similar to that of PD-1 and CTLA-4, as well as comparable signal transduction mechanisms. In vitro studies using cells derived from melanoma patients have demonstrated that simultaneous blockade of the BTLA and PD-1 pathways can significantly increase the quantity and function of tumor-specific cytotoxic lymphocytes. This suggests that combination therapy with anti-BTLA monoclonal antibodies and anti-PD-1 monoclonal antibodies may yield therapeutic efficacy significantly superior to that of anti-PD-1 monotherapy.

More importantly, Junshi Biosciences’ JS004 has received approval from both the NMPA and the U.S. FDA to enter clinical trials, making it the world’s first anti-tumor BTLA monoclonal antibody to reach the clinical trial stage and demonstrating a significant global leadership position.

Selected pipelines with estimated approval timelines disclosed by Junshi Biosciences in its R&D schedule

In its latest prospectus for the STAR Market, Junshi Biosciences also disclosed its current R&D timeline. According to Junshi Biosciences’ plan, ten additional indications for toripalimab are expected to gain approval within the next three years, with nasopharyngeal carcinoma (second-line) and urothelial carcinoma (second-line), for which New Drug Applications (NDAs) have already been submitted, projected to be approved in the second half of 2020.

Given that the first domestic biosimilar of Humira has already been secured by another company, UBP1211, another Humira biosimilar for which a New Drug Application (NDA) has been filed, is also highly likely to gain approval within 2020. JS002, a PCSK9 monoclonal antibody about to enter Phase III clinical trials, also stands a good chance of being approved for market launch in 2022, provided its clinical trials proceed smoothly.

Overall, over the next two to three years, the indications for Tuoyi will continue to expand, including nasopharyngeal carcinoma—an indication not yet addressed by competing products. Other pipeline products will also gradually enter the commercialization stage. As Junshi Biosciences’ product portfolio becomes increasingly comprehensive, its pace of development is expected to accelerate.

Biopharmaceuticals are manufactured using complex fermentation processes, whereby larger production capacity leads to lower per-unit production costs. In 2019, the commercial production and clinical trial supply of Junshi Biosciences’ products relied primarily on its Wujiang production facility. The Wujiang facility has a fermentation capacity of 3,000 liters, and the first batch of Tuoyi produced there was released in February 2019. According to the latest prospectus, the capacity utilization rate of the Wujiang production facility was 76.47% in 2019. Given the ongoing expansion of Phase III clinical trials and the rising sales of Tuoyi, the Wujiang facility’s capacity will be insufficient to guarantee Junshi Biosciences’ product supply in 2020.

Junshi Biosciences has also taken proactive measures. A portion of the funds raised from its listing on the Hong Kong Stock Exchange was specifically allocated to the construction of a new production base in Lingang. Furthermore, as part of the adjustment to the use of proceeds, some funds originally designated for investments and mergers and acquisitions were redirected to the construction of the Lingang production base.

In December 2019, Phase I of the Lingang production base was successfully commissioned, initiating pilot production of PD-1 monoclonal antibodies and PCSK9 monoclonal antibodies. The completed Phase I project covers an area of 80 mu, with a total construction area of 70,000 square meters and a production capacity of 30,000 liters, while also reserving space for future expansion. The Lingang base currently has the largest single-site production capacity among biopharmaceutical companies in China that have disclosed their capacity figures.

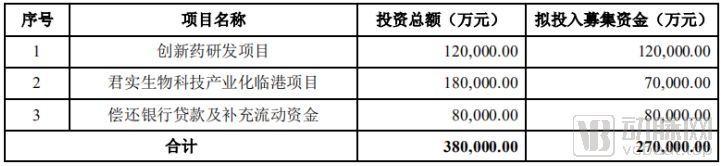

Intended Use of Proceeds from Junshi Biosciences’ STAR Market IPO

From Junshi Biosciences’ planned use of proceeds from this listing, it is evident that, in addition to maintaining its investment in innovative drug development, the company will continue to allocate substantial funds to the construction of its Lingang production base. This capital allocation strategy fully reflects Junshi Biosciences’ strong confidence in the future regulatory approval and market launch of its products, as well as in the expansion of their indications.

Of the proceeds from its listing on the Hong Kong Stock Exchange, Junshi Biosciences also allocated a portion to external collaborations, including outward investments, licensing transactions, and collaborative research. Based on publicly available information, VCBeat has outlined Junshi Biosciences’ strategic initiatives in this area since its IPO.

VCBeat Compiles Selected External Collaboration Activities of Junshi Biosciences Since Its Listing on the HKEX, Based on Public Reports

Overall, Junshi Biosciences’ external investments and collaborations have consistently focused on oncology. Its product portfolio is diversified, with nearly every collaboration exploring a distinct developmental pathway. For instance, in the development of toripalimab combination therapies, the partnerships with I-Mab Biopharma and Harbin Pharmaceutical Group BioPharm Co., Ltd. (Youhe Pharma) involve combinations between immune checkpoint inhibitors, focusing on cancer immunotherapy; the collaboration with Ascentage Pharma investigates the impact of accelerated apoptosis on the efficacy of PD-1 monoclonal antibodies; the partnership with Huiyu Therapeutics centers on combining angiogenesis inhibitors with PD-1 monoclonal antibodies; and the collaboration with Sirnaomics explores the interplay between RNAi therapeutics and PD-1 monoclonal antibodies.

Although PD-1 monoclonal antibodies have demonstrated significant efficacy in most tumor types, their response rates remain suboptimal in certain cancers. Current research suggests that combination therapy may be the key to overcoming the efficacy bottleneck of PD-1 monoclonal antibodies. With ample funding, pursuing more exploratory collaborations can help Junshi Biosciences rapidly identify valuable drug combination regimens and continue investing in this direction to discover new breakthroughs.

In terms of in-licensing, Junshi Biosciences has successively partnered with Runjia Pharmaceuticals and Duoxi Biologics to secure the future commercialization rights to their products. These two in-licensing deals focus on different targets, including CDK, PI3K, and Trop2, thereby enriching Junshi Biosciences’ overall portfolio.

On the eve of its IPO, July 14, 2020, Junshi Biosciences announced a collaboration with U.S. startup Revitope, formally entering the cell therapy field. The two parties will jointly develop “global first-in-class” T-cell chimeric activation cancer therapies targeting dual antigens. These licensed-in products have significantly enriched Junshi Biosciences’ product pipeline, laying a solid foundation for future development.

During the sudden outbreak of the COVID-19 pandemic in 2020, Junshi Biosciences was among the first companies to launch related research. It first participated in the Series A+ financing round of Steady Medicine, a developer of mRNA vaccines for SARS-CoV-2, and then announced on March 20, 2020, a collaboration with the Institute of Microbiology of the Chinese Academy of Sciences to develop neutralizing antibodies against SARS-CoV-2. This move also attracted support from multinational pharmaceutical companies; on May 6, 2020, Eli Lilly announced a partnership with Junshi Biosciences, securing an exclusive license for JS016 (Junshi’s COVID-19 antibody) outside the Greater China region, while committing to subscribe to USD 75 million worth of Junshi’s shares.

The results of animal studies on JS016 have been released and published in the prestigious international journal Nature. In rhesus monkey studies, this antibody significantly inhibited viral infection, demonstrating both therapeutic and prophylactic efficacy, thereby highlighting its potential for clinical translation. Based on these excellent preclinical results, JS016 has entered Phase I clinical trials in China, with subject enrollment already completed. Clinical trials of JS016 in the United States were also initiated in the second quarter, led by its partner, Eli Lilly.

Looking back on Junshi Biosciences’ development over the past year and a half, all the plans outlined at the time of its listing on the Hong Kong Stock Exchange have been fully implemented. Product R&D has progressed smoothly, production facilities have been established, and the company has actively pursued external collaborations. Moreover, during the COVID-19 pandemic, it rapidly launched drug products and successfully advanced them into clinical trials. With substantial funds raised through this latest listing, Junshi Biosciences will continue to serve as a leader in China’s biopharmaceutical industry in the next phase.