GoHealth IPO: How a Health Insurance TPA Giant Achieved a $6.7B Market Cap

This Wednesday, U.S. health insurance TPA giant GoHealth listed on the Nasdaq, currently boasting a market capitalization of $6.679 billion, equivalent to over RMB 46 billion.

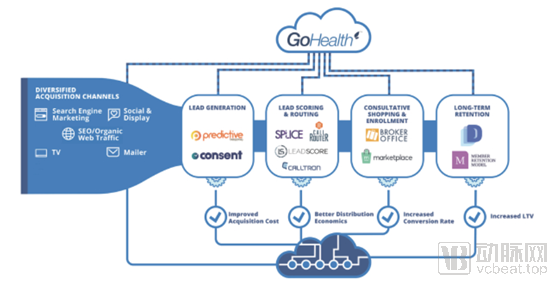

GoHealth’s model connects consumers with insurance companies by leveraging diversified distribution channels, combined with technology, data science, and deep industry expertise. Its revenue is primarily derived from commissions on health insurance policies, with commission income for fiscal year 2019 projected to reach $420 million.

GoHealth’s model resembles that of an insurance brokerage. In China, insurance brokerages primarily rely on the traditional agent-based model, whereas GoHealth leverages technology and data science—specifically, machine-learning algorithms powered by nearly two decades of insurance behavior data—to reimagine optimal processes and help individuals identify the health insurance plans best suited to their specific needs.

In 2001, founder Brandon Clingman found it difficult to obtain suitable health insurance, so he established GoHealth to make it more convenient and simpler to find appropriate insurance products. Since its inception, GoHealth has evolved from a company showcasing insurance quotes and enrollment technologies into a health insurance brokerage firm, and further into a data- and algorithm-driven comprehensive health insurance service provider, successfully listing on the NASDAQ. According to its prospectus, the company’s net revenues reached the $3 billion range in 2019.

How Was GoHealth Built? What Insights Can GoHealth’s Success Offer to Players in China’s Health Insurance Industry?

Next, VCBeat will answer these two core questions for you.

GoHealth’s mission is to improve access to healthcare in the United States. For customers, navigating health insurance options is often confusing and difficult, and minor differences between insurance plans can lead to substantial out-of-pocket costs or even lack of coverage for essential medications.

Since its inception, GoHealth has continuously invested in technology, data science, and business processes, enabling millions of individuals to enroll in health insurance plans while helping carriers expand their product offerings and insurance programs.GoHealth’s platform leverages proprietary technology, machine learning capabilities, data, efficient business processes, and skilled, well-trained licensed agents to connect consumers with health insurance carriers through multiple channels.

GoHealth Platform offers a wide range of health insurance products, including but not limited to Medicare Advantage, Medicare Supplement, prescription drug plans, and individual and family plans, allowing consumers the freedom to choose.

Among the various health insurance plans offered by GoHealth, consumers are encouraged to provide reviews and suggestions to enhance the suitability and transparency of health insurance products. GoHealth has established an internal team called TeleCare to assist users in securing potential government subsidies and simplifying the insurance enrollment process. This team is dedicated to increasing consumer engagement with the GoHealth brand, selling new products and services that help meet consumers’ healthcare needs, and helping consumers maximize the benefits of their health insurance plans to support long-term health.

Furthermore, carriers can also benefit from GoHealth’s platform, particularly those seeking access to a large and rapidly growing population of Medicare-eligible individuals. GoHealth has grown to become the largest external partner for many insurance underwriters in Medicare Advantage plans.

GoHealth’s service model operates such that, after consumers engage with its platform via online or telephone interactions, they enter GoHealth’s data-driven omnichannel marketing funnel, where the company leverages LeadScore—one of its proprietary machine learning technologies—to evaluate consumer leads in real time.

Subsequently, GoHealth’s proprietary technology and business processes transfer qualified leads to agents in real time through internal and external channels. Its technological advantages enable these agents to work either at the company’s sales operations center or remotely from home.

In 2019 alone, the GoHealth platform generated over 42.2 million consumer engagement leads and acquired inquiry data from more than 4 million consumers. In the same year, the platform employed an average of 931 agents, with the total number of insurance agents reaching 1,453 in the Medicare segment alone.

Leveraging consumers’ specific needs and GoHealth’s comprehensive data, agents use GoHealth’s proprietary “Marketplace” technology to identify the best-matching health insurance products from an extensive inventory. The Marketplace then facilitates seamless quoting and enrollment for the consumer-selected health insurance plans by utilizing proprietary and third-party data, as well as direct application programming interfaces (APIs) to connect with carriers.

The accumulation of data has provided significant support to GoHealth in customer acquisition, user education, and facilitating the sale of health insurance products. This has ultimately driven GoHealth toward a data- and algorithm-driven model, digitizing the entire lifecycle of health insurance and delivering direct benefits to all stakeholders within the ecosystem.

As GoHealth recruits more qualified leads through the Marketplace, the power of data enhances the platform’s marketing capabilities. GoHealth’s platform is specifically designed for rapid scalability, with cloud infrastructure featuring information security controls that have been independently audited by multiple third-party firms. Its technology drives compliance with HIPAA, TCPA, and state insurance regulations, and consumers incur no fees for using any of GoHealth’s services.

(GoHealth's Technical System)

Typically, the platform charges operators an initial commission when consumers register their products and become customers. As long as these customers maintain their health insurance plans, GoHealth charges additional commissions. This commission structure encourages collaboration with insurance underwriters to enhance customer satisfaction by selecting health insurance products that best meet customer needs, thereby delivering better outcomes for insurance underwriters, users, and the platform.

As of December 31, 2019, GoHealth’s total commissions receivable (representing such expected future commission streams) amounted to $382.9 million, an increase of 231.5% compared to December 31, 2018.

In essence, GoHealth does not provide insurance to customers, nor does it assume underwriting or medical loss risks associated with customer placements in carrier products on its platform. In addition to commissions, GoHealth partners with certain carriers to charge fees for marketing services provided on its platform.

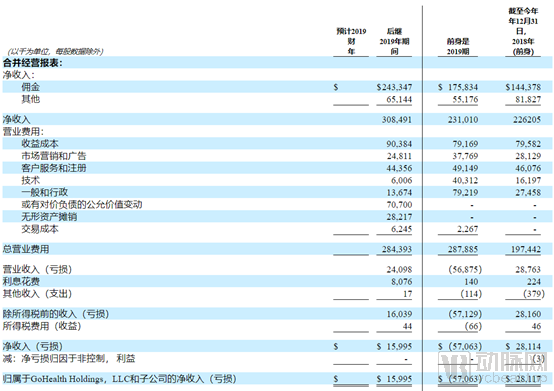

The unique value of the data science-driven, fully integrated platform has fueled GoHealth’s rapid growth.From 2018 to 2019, the company's net income grew by 138.5%, reaching $539.5 million, up from just $226.2 million in 2018.

On the GoHealth platform, the total number of policies generated was 118,000 in 2018, and by 2019, this figure had grown to over 427,000.

GoHealth has established six key technologies with competitive barriers in its health insurance business.

1. Data-Driven Omnichannel Marketing. Leveraging predictive lead scoring and multivariate testing of lead attributes, GoHealth’s data-driven omnichannel marketing approach enhances the identification and matching of prospective customer segments, thereby improving marketing conversion rates.

2. LeadScore Proprietary Technology. LeadScore is one of GoHealth’s proprietary machine learning technologies, built on large-scale end-to-end sales data. It predicts the conversion probability of consumer leads and is used to optimize in real time the customer journey for purchasing health insurance products.

3. Advanced Matching Technology. GoHealth’s proprietary qualified lead allocation, based on LeadScore and agent performance data models, uses prioritization technology to precisely match the best leads with the most suitable insurance agents.

4. Marketplace. GoHealth’s proprietary Marketplace technology features decision-support capabilities and seamlessly integrates with the company’s operational enterprise systems, enabling agents to quickly and efficiently select health insurance plans tailored to each consumer’s specific needs and close sales.

5. TeleCare Team. GoHealth’s in-house TeleCare team is dedicated to enhancing consumer engagement and loyalty toward the GoHealth brand, selling new products and services that help meet consumers’ healthcare needs, and assisting consumers in maximizing the benefits of their health insurance plans.

6. Scalable and Compliant Infrastructure. GoHealth’s cloud infrastructure and compliance technologies ensure the scalability and regulatory compliance of the entire platform.

These six key technologies have established GoHealth’s core competitiveness. They are difficult for competitors to replicate and have increasingly anchored the platform’s value for both agents and consumers. Moreover, as time passes, the data generated by customers and operators becomes ever richer, feeding into machine learning and data-science-driven feedback loops that make GoHealth’s marketing and technology increasingly intelligent.

This creates a positive feedback loop: increasingly intelligent algorithms enhance customer conversion rates, leading to a win-win outcome for insurers, users, and the platform alike.

GoHealth’s product portfolio primarily consists of three major segments: Medicare (government-sponsored health insurance or commercial insurance), IFP (Individual and Family Plans), and Others.

From a segmented perspective, the Medicare segment focuses on selling Medicare Advantage, Medicare Supplement, Medicare Prescription Drug Plans, and Medicare Special Needs Plans through multiple carriers. In addition, the Individual and Family Plans (IFP) and other segments offer individual and family plans—such as dental insurance, vision insurance, and other supplemental coverage—to individuals who are not eligible for Medicare, with many policies having terms of less than one year.

In 2019, among the three major categories of health insurance products, Medicare generated the highest revenue and was the primary contributor to both business growth and profit margin expansion.As disclosed in the prospectus, the Medicare segment accounted for 80.2% of total revenue in fiscal year 2019, while IFP and others comprised 19.8% of total revenue for the fiscal year; in 2018, Medicare accounted for only 49.6% of total revenue, with IFP and others making up 50.4%.

The shift in revenue structure reveals GoHealth’s strategic pivot, with its strategic focus now directed toward the Medicare health insurance segment. To this end, over the past two years, GoHealth has increased the number of multi-carrier channel agents in the Medicare market segment and prioritized placing qualified leads into Medicare insurance products.

This strategic adjustment actually aligns with the industry's development trends.

In the United States, the Medicare program (similar to China’s basic medical insurance, with government involvement in its establishment) has seen a growing proportion of the population eligible for coverage. The number of enrollees is projected to rise from approximately 61 million in 2019 to about 77 million by 2028. In 2019, 38% of Medicare beneficiaries (approximately 23 million people) were enrolled in Medicare Advantage plans (supplementary commercial insurance built upon basic Medicare), representing an increase of roughly 1.5 million from 2018 to 2019. Against this backdrop, GoHealth has increasingly shifted its focus toward Medicare-related products over the past four years, de-emphasizing individual and family health insurance products, which had previously been the company’s core business.

The total addressable market for Medicare Advantage and Medicare Supplement products is estimated at $28 billion, a trend that will drive further market growth in the coming years.

Riding the Medicare market trend has made a clear contribution to GoHealth’s development. Total revenue generated by the Medicare segment grew from $112.2 million for the period ending in 2018 to $432.7 million in fiscal year 2019, representing a year-over-year increase of 285.6%.

GoHealth's Core Operating Data

China's health insurance industry is currently experiencing rapid growth.

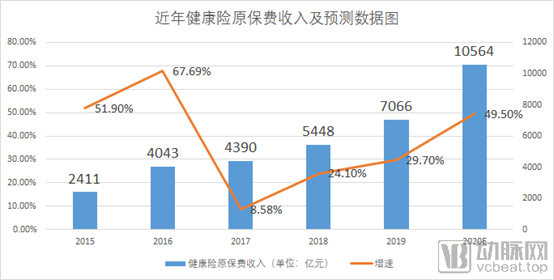

In 2019, China’s original premium income for health insurance reached RMB 706.6 billion, a year-on-year increase of 29.7%. In the first quarter of 2020, despite the impact of the pandemic, health insurance premium income amounted to RMB 264.1 billion, representing a year-on-year growth of 21.6%. Over the past five years, the industry’s compound annual growth rate (CAGR) has approached 30%. Based on this growth trajectory, China’s health insurance market is projected to reach the trillion-yuan level this year.

Against the backdrop of innovative payment models in healthcare, health insurance has been frequently highlighted in policy documents. Over the past year, regulators have introduced multiple policies to vigorously promote the development of health insurance.

On March 5, 2020, in the policy document titled “Opinions on Deepening the Reform of the Medical Security System” issued by the Central Committee of the Communist Party of China and the State Council, with the statement of "establishing a multi-tiered medical security system in which basic medical insurance serves as the mainstay, medical assistance provides the safety net, and supplementary medical insurance, commercial health insurance, charitable donations, and mutual medical aid develop in concert", to provide top-level design for China's healthcare payment system. Driven by policy influence, health insurance is bound to play a significant role in healthcare payments in the future.

Since 2018, the health insurance sector has attracted a surge of players and capital, with frequent announcements of corporate financing. In 2019, more than 20 companies secured funding. Notable examples include Shuidi, which raised RMB 500 million in its Series B round and RMB 1 billion in its Series C round, and Duobaoyu, which completed three rounds of financing in 2019, with its latest Series B round exceeding RMB 200 million and led by Yunfeng Capital.

In 2020, the financing momentum in the health insurance industry remained strong, with eight companies disclosing funding news in Q1 alone. A notable example was Baoxian Jike (Insurance Geek), which secured a $25 million Series C round.

From the overall financing trend, multiple companies in the health insurance sector have reached Series C and Series D funding rounds, suggesting that the industry may be on the verge of an IPO boom.

The author believes that China’s health insurance industry currently faces both opportunities and pain points. To some extent, the entire industry is still in its early stages.

From the perspective of the industry chain, health insurance operations involve multiple segments: “medical care, pharmaceuticals, insurance, and wellness.” Customers receive financial compensation for health protection directly or indirectly from payers; obtain diagnostic, therapeutic, and prescription services from healthcare providers; and access full-cycle wellness services and health incentives from wellness service providers. Payers and providers achieve integration through shared customer bases, data interoperability, and system connectivity. However, the pain points existing in these segments remain far from resolved.

In the operation of health insurance, issues such as information asymmetry, low level of specialization, high claim ratios, and low profitability still stand in the way of the industry.

Can innovative companies in the industry, like GoHealth, empower the sector through digitalization and truly ignite an engine driven by data and algorithms?

Moreover, and more importantly, users do not purchase health insurance products for the sake of claims settlement, but to gain access to corresponding medical services and healthcare coverage. The question is whether current industry operators possess the capability to provide such medical services.

Pain Points and Opportunities Coexist. Only by addressing pain points more thoroughly can the entire industry usher in greater opportunities.