Are China's Clinical Trials Going Global? Analysis of 1,235 Ongoing Phase III Trials

Phase III clinical trials represent the final hurdle before a drug’s market approval. The Phase III clinical trials of investigational drugs essentially indicate the trajectory of drug approvals over the next two to three years, serving as a key barometer for new drug launches.

Although some drugs may receive conditional approval based on Phase II clinical trial results, such cases remain the minority. Furthermore, drugs granted conditional approval must still undergo Phase III clinical trials; if these trials fail, the drug’s marketing authorization will be revoked.

VCBeat conducted a brief statistical analysis of the 1,235 Phase III clinical trials listed as ongoing on the CDE Drug Clinical Trial Registration and Public Disclosure Platform as of July 15, aiming to explore the trends in drug approvals in China over the coming years.

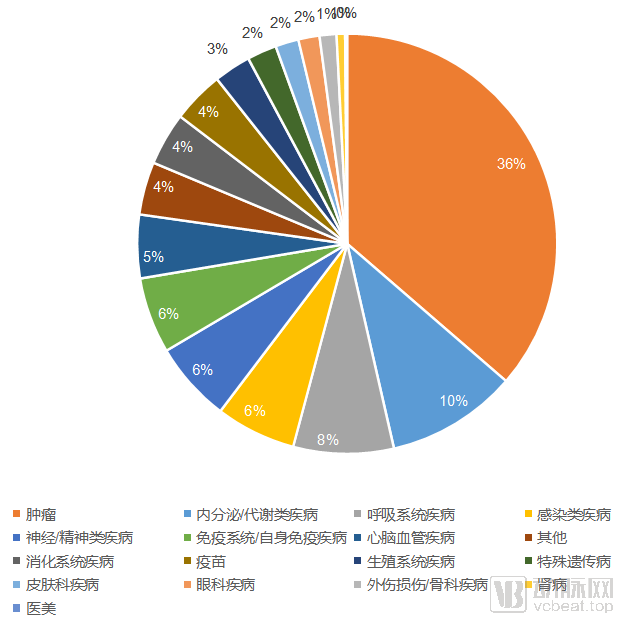

Distribution of Indications for Phase III Clinical Trials in China

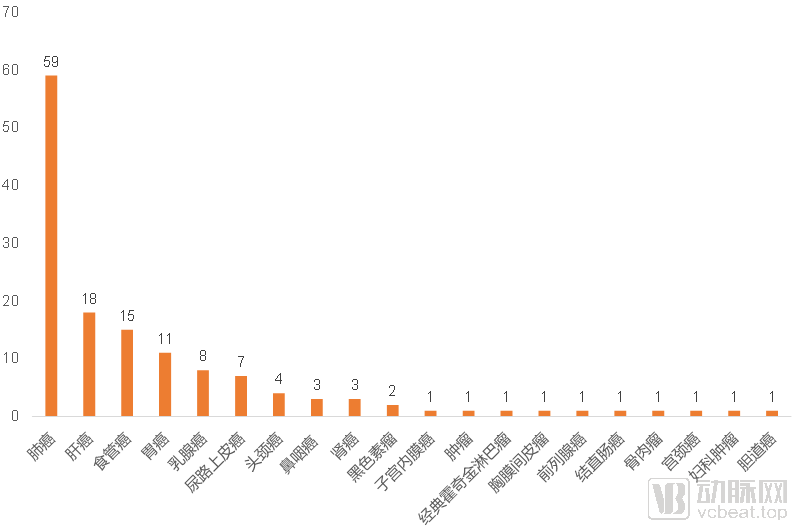

In terms of the distribution of indications in clinical trials, oncology is undoubtedly the most popular field. Among the Phase III clinical trials currently under investigation in China, approximately 36% are focused on oncology, totaling 447 trials.

Following closely are endocrine and metabolic diseases, represented by diabetes; respiratory diseases, represented by asthma and pulmonary hypertension; and infectious diseases, represented by HIV/AIDS, hepatitis B, and hepatitis C.

In July 2019, VCBeat conducted a statistical analysis of all ongoing clinical trials listed on ClinicalTrials.gov. Both in the overall analysis of clinical trials and in the subset of Phase III/IV trials, neurological and psychiatric disorders ranked second, surpassed only by oncology, with their share in Phase III/IV trials reaching as high as 15%. However, among domestic Phase III clinical trials in China, there were only 76 ongoing studies focusing on neurological and psychiatric disorders, accounting for merely approximately 6%.

Neurological and psychiatric disorders, such as Alzheimer’s disease, Parkinson’s disease, and major depressive disorder, have long lacked sufficiently effective clinical treatment options. Although these conditions may not be directly fatal, they significantly impair patients’ quality of life and can ultimately lead to indirect mortality. While highly discussed innovative drugs such as GV971 have emerged in China in recent years, overall domestic R&D investment in neurological and psychiatric disorders—a field severely lacking therapeutic solutions—remains relatively low compared with global levels.

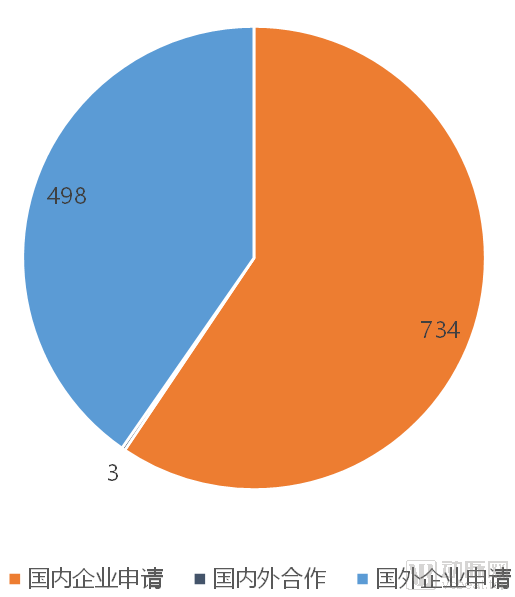

Distribution of Clinical Trial Applicant Types

Regarding applicants for Phase III clinical trials, as China further opens its stance on drug introduction and clinical research, an increasing number of multinational pharmaceutical companies are conducting clinical trials domestically or including China in global multicenter clinical trials. Among the registrational Phase III clinical trials currently under investigation in China, those sponsored by multinational pharmaceutical companies have reached 498, accounting for approximately 40% of the total.

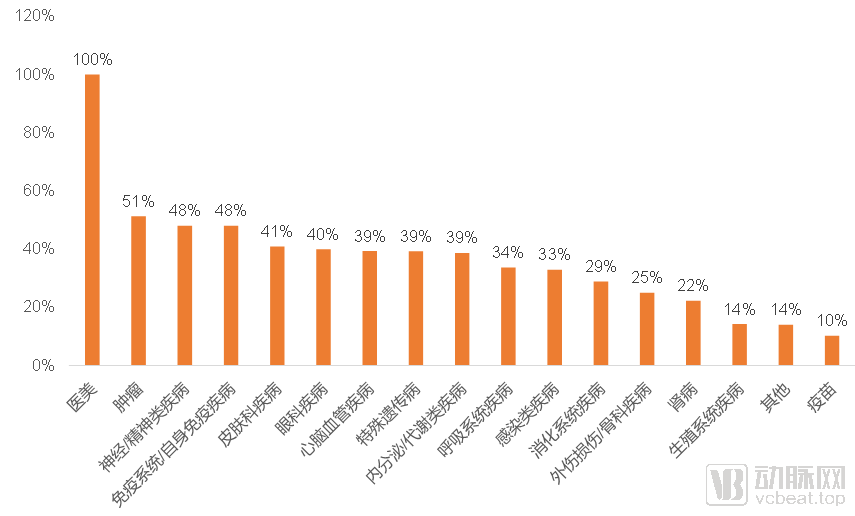

Proportion of Phase III Clinical Trials in the Corresponding Field Conducted by Foreign Applicants

Multinational pharmaceutical companies’ clinical trial portfolios in China are largely aligned with their global strategies. The number of Phase III oncology trials they have launched in China has surpassed that of domestic pharmaceutical companies, and their shares in the fields of neurological/psychiatric disorders and immune/autoimmune diseases each approach 50%. In contrast, domestic pharmaceutical companies have adopted a more aggressive strategy in cardiovascular and cerebrovascular diseases and endocrine/metabolic disorders, which are key focus areas in chronic disease management.

The key therapeutic areas where multinational pharmaceutical companies are strategically positioning themselves in China are precisely those critical fields lacking adequate clinical solutions. In the chronic disease markets, such as hypertension and diabetes, treatment options are already relatively mature. Unless a new drug can deliver a qualitative leap over existing therapies, it is unlikely to become a blockbuster. Broad statistical trends indicate that while multinational pharmaceutical giants continue to invest in these chronic disease areas, they are evidently more attracted to fields with unmet medical needs and an urgent demand for innovative therapies.

Even in their strategic focus on niche segments, multinational pharmaceutical companies are increasingly prioritizing areas with more urgent clinical needs. Taking gastrointestinal diseases as an example, AbbVie, Eli Lilly, and Takeda Pharmaceutical have concentrated their efforts in this field, primarily targeting two indications: Crohn’s disease and ulcerative colitis. Both conditions are characterized by low cure rates and a high tendency for recurrence, representing significant challenges in the management of gastrointestinal disorders. In contrast, very few domestic companies have developed pipelines for these two indications. Instead, a large number of Phase III clinical trials conducted by Chinese firms are focused on indications with favorable prognoses, such as duodenal ulcers and gastroesophageal reflux disease (GERD).

This actually highlights the differences in R&D strategies between domestic and foreign pharmaceutical companies. Products with relatively mature clinical solutions are undoubtedly easier to develop, but they also face more intense market competition after launch. In contrast, while addressing current clinical treatment challenges involves greater R&D difficulties, the resulting products boast stronger market competitiveness and higher returns. Most domestic pharmaceutical enterprises, especially traditional ones, tend to focus on low-risk, low-return R&D approaches; whereas multinational pharmaceutical companies are relatively more bold, adopting high-risk, high-return R&D strategies to tackle more challenging clinical problems.

Clinical trials related to medical aesthetics constitute a special case in these statistics. Currently, the two Phase III clinical studies on medical aesthetics underway in China have both been initiated by multinational pharmaceutical companies: Allergan and Daewoong Pharmaceutical, with both trials investigating BOTOX (botulinum toxin for facial slimming). The Lanzhou Institute of Biological Products in China is also conducting research on botulinum toxin; however, its indications focus not on medical aesthetics but on neurological disorders such as chronic migraine and multiple sclerosis.

Number of Phase III Clinical Trials Led by Top Principal Investigators

In China, 21 principal investigators (PIs) have served as PIs for more than 10 Phase III clinical trials. Professor Qin Shukui, who holds the highest number, has served as the PI for 30 Phase III clinical trials.

Meanwhile, the principal investigators (PIs) handling a large volume of clinical trials are predominantly concentrated in the field of oncology. Among the 21 top-tier PIs, 15 primarily engage in clinical research related to oncology. When examining more specific disease categories, leading PIs in high-prevalence conditions—such as lung cancer, breast cancer, gastrointestinal tumors, and diabetes—are similarly burdened with heavy workloads. Notably, in the field of lung cancer, six PIs—Zhou Caicun, Shi Yuankai, Wu Yilong, Lu Shun, Cheng Ying, and Zhang Li—each oversee more than 10 Phase III clinical trials, with their combined total exceeding 100 trials.

When selecting key opinion leaders (KOLs) for clinical trials, top-tier principal investigators (PIs) across various specialties naturally become the preferred choices for trial implementation. Endorsement by leading KOLs serves as a guarantee of clinical trial quality. This is particularly evident in oncology, where KOL influence is prominent; conducting large-scale Phase III clinical trials requires PIs and their teams to possess extensive experience in managing clinical trials. Consequently, for Phase III clinical trials across most disease areas, efforts are made to invite top-tier KOLs to serve as the principal investigators.

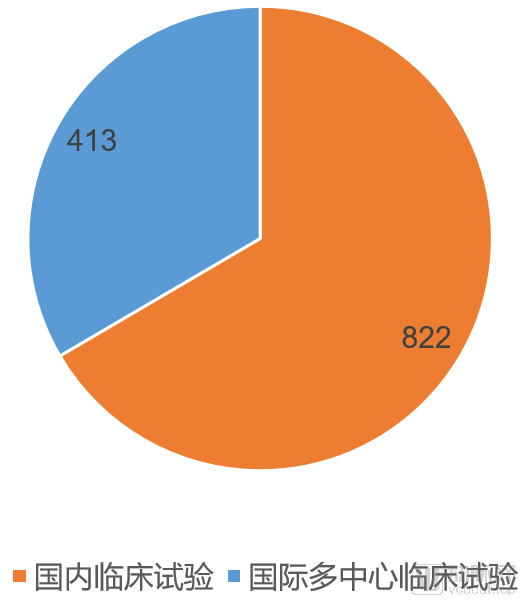

Proportion of International Multicenter Clinical Trials in Phase III Clinical Trials

Among currently ongoing clinical trials, the ratio of domestic clinical trials to international multicenter clinical trials is approximately 2:1. Generally, Phase III clinical trials involve large patient enrollment. Adopting an international multicenter approach not only reduces the specificity of clinical data but also facilitates rapid patient recruitment. Particularly since China joined the ICH and achieved mutual recognition of clinical data, results from international multicenter clinical trials can be recognized globally. This has significantly enhanced the value of international multicenter clinical trials.

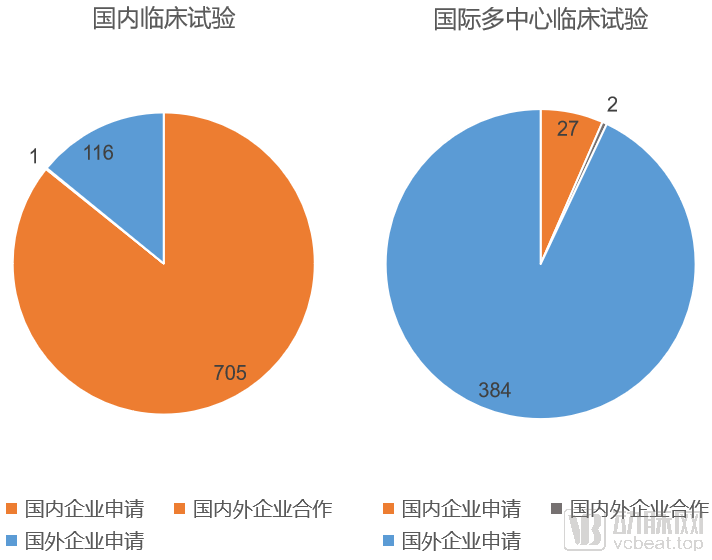

Distribution of Applicants for Domestic Clinical Trials and International Multicenter Clinical Trials

When we categorize Phase III clinical trials into domestic clinical trials and international multicenter clinical trials, and further analyze the applicants involved, we observe significant differences between the two groups. Domestic clinical trials are primarily sponsored by Chinese pharmaceutical companies, whereas international multicenter clinical trials are mainly sponsored by multinational pharmaceutical companies.

Given the high value of international multicenter clinical trials, multinational pharmaceutical companies are significantly more inclined to include China in global multicenter studies as part of their clinical trial programs, rather than conducting complete registration clinical trials domestically.

Domestic pharmaceutical companies primarily conduct clinical trials within China, a trend that aligns with the broader trajectory of drug development in the country. As previously analyzed, Chinese pharmaceutical firms currently focus on therapeutic areas with relatively mature solutions and large market sizes. Consequently, among products in Phase III clinical trials, there is a substantial proportion of generic drugs and follow-on innovative products. Since overseas markets for these products are already well-established, domestic companies find it difficult to penetrate international markets even after completing multinational clinical trials. Therefore, these pharmaceutical enterprises need only complete domestic clinical studies to successfully launch their products in the Chinese market.

For domestic innovative pharmaceutical companies, opting to conduct international multi-center clinical trials is naturally the superior choice. At present, however, a significant number of innovative drug companies still choose to conduct clinical trials within China, primarily due to budgetary constraints. International multi-center clinical trials often require enrollment on the scale of thousands of participants and involve dozens of clinical sites across more than ten countries worldwide, resulting in substantially higher costs across all aspects compared to domestic clinical trials. Consequently, most innovative pharmaceutical companies still opt to complete their Phase III clinical trials domestically first.

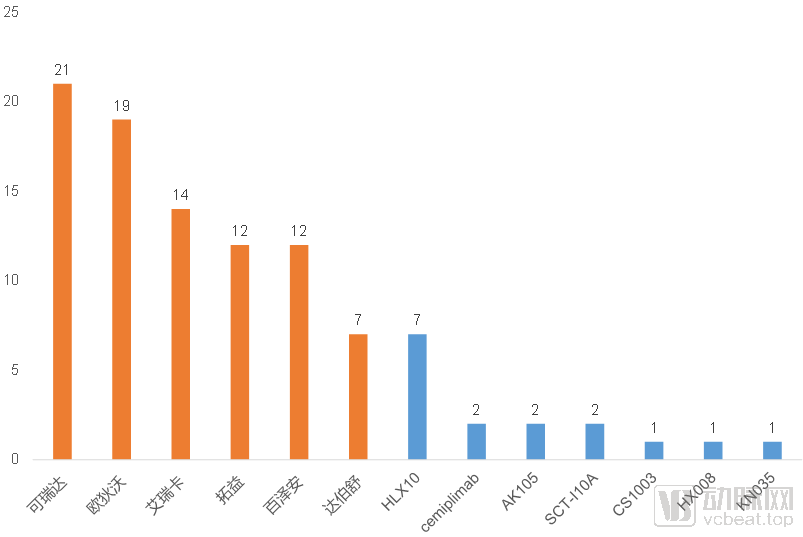

27 Global Multicenter Phase III Clinical Trials Applied for by Domestic Companies Currently Under Investigation

As domestic pharmaceutical innovation capabilities improve, Chinese pharmaceutical companies have begun to deploy pioneer teams toward international multi-center clinical trials. The value of these global clinical trials is gradually being realized. A notable example is BeiGene’s BGB-3111 (zanubrutinib), which has successfully marked the overseas expansion of an innovative Chinese drug.

Henlius, which initiated a global multicenter Phase III clinical trial for trastuzumab as early as 2016 (the trial is currently still listed as ongoing), is likely approaching the approval and market launch of its product in China. Henlius has successfully obtained EU GMP certification, and the Committee for Medicinal Products for Human Use (CHMP) of the European Medicines Agency (EMA) has issued a positive opinion on the marketing authorization of this drug. The regulatory review process in China has also entered the approval stage. Henlius is well-positioned to achieve the sequential market launches of its trastuzumab biosimilar in China and Europe within 2020.

In the realm of PD-1 monoclonal antibodies, which have gained significant popularity over the past two years, several domestically approved PD-1 mAbs are now attempting to expand into international markets through multinational clinical trials. Beigene, Junshi Biosciences, and Hengrui Medicine have all initiated Phase III multinational clinical trials. In selecting indications, they have strategically targeted those for which Keytruda and Opdivo received approval relatively late, or which remain unapproved to date, such as nasopharyngeal carcinoma, liver cancer, and esophageal cancer.

Overall, investing in international multi-center clinical trials for high-value drug product development has gradually become an industry trend. Among the 27 related clinical trials we have currently compiled, 14 were initiated in 2019, accounting for more than half of the total. As domestic investment in innovative drugs continues to increase, international clinical trials are bound to become a major future trend.

Following the sequential approval of six PD-1 monoclonal antibodies that had previously been submitted for market authorization, two PD-L1 monoclonal antibodies gained approval between late 2019 and 2020. Competition over indications for PD-1/PD-L1 monoclonal antibodies has become increasingly intense. Pharmaceutical companies are sparing no expense in funding clinical trials. Meanwhile, several products not yet submitted for market approval are actively seeking differentiated strategic positioning to distinguish themselves from existing offerings.

Phase III Clinical Trial Status of PD-1 Monoclonal Antibody

Among the six PD-1 monoclonal antibodies already on the market, two imported products have conducted extensive Phase III clinical trials in China by incorporating the country into their global clinical studies. In contrast, domestic companies have primarily focused on clinical trials within China, supplemented by a limited number of international trials, seeking breakthroughs overseas by leveraging their competitive advantages in specific indications.

In addition to the already approved products, seven PD-1 monoclonal antibody candidates have entered Phase III clinical trials: Henlius’s HLX10, Sanofi’s cemiplimab, Akeso’s AK105, SinoCellTech’s SCT-10A, CStone Pharmaceuticals’ CS1003, Hansoh Biopharma’s HX008, and Alphamab Oncology’s KN035. Among these, HLX10 and cemiplimab are poised to become the next PD-1 monoclonal antibodies approved for marketing in China.

Henlius’s PD-1 monoclonal antibody, HLX10, as its flagship first self-developed innovative drug, may have slightly lagged in R&D progress, but it remains a highly competitive PD-1 monoclonal antibody product thanks to its exploration of novel biomarkers and combination therapy mechanisms.

Sanofi’s cemiplimab, jointly developed by Sanofi and Regeneron, is the third PD-1 inhibitor approved globally. It was initially approved by the U.S. FDA in September 2018 for the treatment of cutaneous squamous cell carcinoma (CSCC). However, Sanofi’s clinical research strategy in China has not focused on skin cancer but rather on non-small cell lung cancer (NSCLC), an indication that the company is currently prioritizing in overseas markets. This may suggest that Sanofi’s clinical trials of cemiplimab in China are primarily intended to expand the global patient pool for broader indication development, rather than to penetrate the Chinese market.

Status of Phase III Clinical Trials of PD-L1 Monoclonal Antibodies

If 2018 was the inaugural year of cancer immunotherapy in China, then 2020 was the inaugural year of PD-L1 monoclonal antibodies. From late 2019 to the first half of 2020, two imported PD-L1 monoclonal antibody products—AstraZeneca’s Imfinzi and Roche’s Tecentriq—were successively approved for marketing, closely mirroring the sequential approvals of Opdivo and Keytruda in 2018. Following the development trend observed in 2018, domestically produced PD-L1 monoclonal antibodies were expected to rapidly follow suit in 2020, competing alongside imported products.

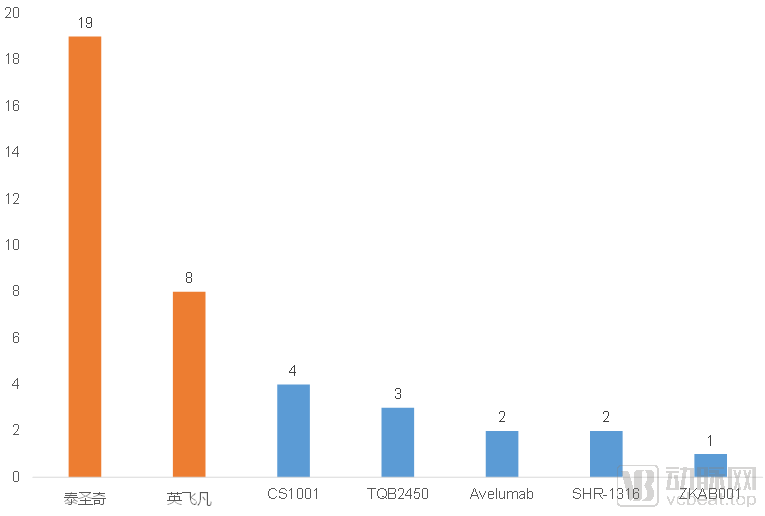

However, based on current progress, no domestic PD-L1 monoclonal antibodies have yet submitted a New Drug Application (NDA), making approval within 2020 unlikely. Nevertheless, since the first Phase III clinical trials for CStone Pharmaceuticals’ CS1001 and Hengrui Medicine’s SHR-1316 were both initiated in 2018, there is a relatively high probability that these trials will be completed and NDAs submitted within 2020. Therefore, domestically produced PD-L1 monoclonal antibodies are expected to officially enter the market in 2021.

In the development of Phase III clinical trials, Roche has equipped Tecentriq with 19 ongoing Phase III clinical trials, a figure that even exceeds the total number of Phase III clinical trials for all other PD-L1 monoclonal antibodies. Based on this substantial investment, Roche appears determined to secure a dominant position in China’s PD-L1 monoclonal antibody market. Infinitus, as the first domestically approved PD-L1 monoclonal antibody, has not extensively rolled out Phase III clinical trials but instead focuses on several core indications, including lung cancer, liver cancer, and cervical cancer.

The third imported PD-L1 monoclonal antibody, avelumab, co-developed by Merck and Pfizer, is also in Phase III clinical trials. However, like cemiplimab, it appears to be more of an extension of global clinical trials, with no clear domestic filing plans emerging.

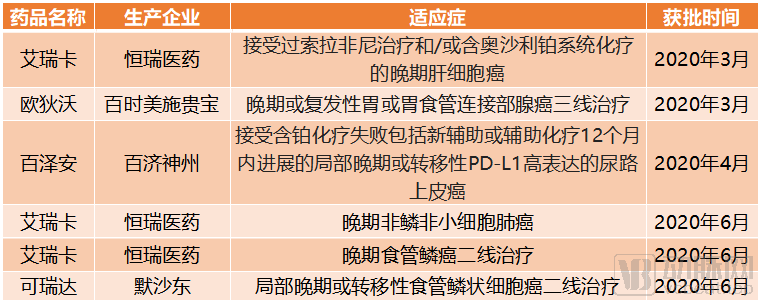

New Indications for PD-1 Monoclonal Antibodies Approved in the First Half of 2020

In the first half of 2020, in addition to the approval of PD-L1 monoclonal antibodies, the indications for PD-1 monoclonal antibodies were significantly expanded. Unlike the substantial overlap seen in previously approved indications, the six indications approved in the first half of 2020 signaled that PD-1 monoclonal antibodies were beginning to expand into new oncology fields. Eligible patients with liver cancer, gastric cancer, esophageal cancer, urothelial carcinoma, and other conditions can now receive treatment with the corresponding PD-1 monoclonal antibodies.

Distribution of Indications in Phase III Clinical Trials of PD-1/PD-L1 Monoclonal Antibodies

Major indications for PD-1/PD-L1 monoclonal antibodies have begun to see product approvals. Nearly all PD-1/PD-L1 monoclonal antibodies are accompanied by Phase III clinical trials related to lung cancer, and to date, five products have sequentially received approval for indications in the field of lung cancer. Approvals have also been granted for most other major indications.

The key indications that will be the focus of future competition are primarily concentrated in four areas: breast cancer, head and neck cancer, nasopharyngeal cancer, and renal cancer.

Clinical Trials of PD-1/PD-L1 Monoclonal Antibodies in Several Indications

In the highly competitive field of breast cancer, Tecentriq holds a near-absolute advantage. In March 2019, Tecentriq received U.S. FDA approval as the first immunotherapy for the treatment of triple-negative breast cancer (TNBC). Its proactive clinical development strategy has further solidified Tecentriq’s leading position. In April 2018, Tecentriq initiated Phase III clinical trials in China for TNBC, followed by the addition of two related clinical trials in 2019. Among PD-1/PD-L1 monoclonal antibodies, Tecentriq was the earliest to launch Phase III studies for breast cancer indications in China and has conducted the largest number of such trials.

In the field of renal cell carcinoma, imported products also hold a dominant position. Opdivo and Tecentriq initiated Phase III clinical trials as early as 2018, whereas Tuoyi has only just begun.

As a tumor type with a particularly high incidence in China, nasopharyngeal carcinoma has attracted three PD-1 monoclonal antibodies, all domestically produced, to target this indication. Among them, Tuoyi (toripalimab) holds a distinct advantage, with its Phase III clinical trials nearing completion. According to the product pipeline disclosed in Junshi Biosciences’ STAR Market prospectus, the New Drug Application (NDA) for the nasopharyngeal carcinoma indication is expected to be submitted in the second half of 2020.

In the head and neck cancer indication, competition is primarily among three PD-L1 monoclonal antibodies; Chia Tai Tianqing’s TQB2450 may have the opportunity to surpass Avelumab and Tecentriq in this indication.