The End of High-Margin Era in Pharmaceutical Retail: The Rise of Omni-channel Expansion in China's Internet+ Healthcare Landscape

Author: CICC April 10, 2020

Analyst: Tu Weiying SAC License No.: S0080516040001, SFC CE Ref: BHM709

Analyst: Zou Peng SAC License No.: S0080513090001, SFC CE Ref: BCC313

Contact: Feng Xipeng, SAC License No.: S0080119030029

The Transformation of the Pharmaceutical Industry from the Perspective of “Internet Plus”: The Pharmaceutical Retail Sector

We believe that “Internet + Healthcare” has accelerated its development under the catalyst of the COVID-19 pandemic, promising to equip local governments with more comprehensive and real-time regulatory capabilities, while granting consumers greater choice and decision-making power. This trend may further hasten the end of the era of high gross margins in traditional retail, paving the way for an era of omnichannel expansion in pharmaceutical retail.

Accelerating Transformation in Pharmaceutical Retail: Omnichannel Retail, the Future Is Here

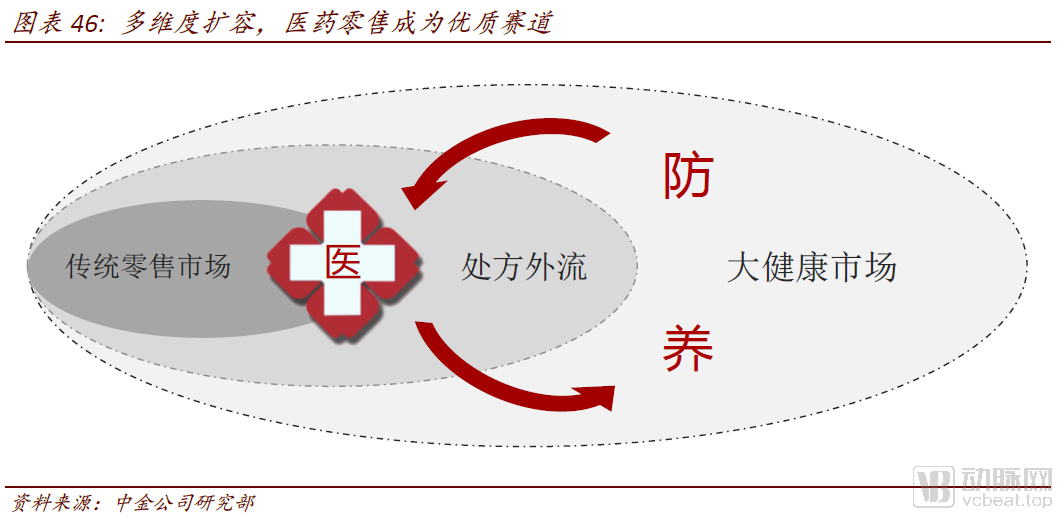

Premium Sector: Pharmaceutical Retail Enters a New Era of Development.In recent years, the pharmaceutical retail market has expanded, driven by escalating health demands and the outflow of hospital prescriptions, while shifts in consumer habits and the breaking down of geographical barriers have spurred a redistribution of terminal traffic. Meanwhile, as Health-tech continues to permeate the pharmaceutical industry, we believe that retail enterprises are poised to undergo a comprehensive transformation toward platform-based business models, with their traditional role as “drug sellers” set to be upgraded into a new role as providers of holistic health “services.”

Challenges and Opportunities Coexist as the Era of High Gross Margins Accelerates Toward Its End.We believe that the accelerated development of “Internet + Healthcare” is posing challenges to traditional retail in several areas: expansion capability (due to insufficient emphasis on “traffic expansion” strategies), service capability (requiring improvements in prescription fulfillment and professional service levels), new scenarios (with stores becoming “warehouses” in F2S/face-to-screen scenarios), and new regulatory landscapes (where health-tech enables an exponential increase in regulatory capabilities). These factors may further accelerate the end of the “high gross margin” era for traditional retail. Furthermore, as the industry’s chain affiliation rate and concentration remain low, diversified expansion strategies based on distinct operational advantages are likely to accelerate industry consolidation, potentially reshaping the competitive landscape.

Omni-channel Retail: The Future Is Here.We believe that pharmaceutical retail enterprises possess stronger expansion capabilities and broader development prospects in the era of “Internet + Healthcare.” In the future, they are expected to adopt a consumer-centric approach and achieve omni-channel expansion across multiple dimensions: omni-entry (integrating “online + offline,” connecting “in-hospital + out-of-hospital,” and exploring “indoor + outdoor”); omni-product (ranging from OTC to prescription drugs, from pharmaceuticals to general health products, and from regionalized offerings to borderless products); omni-service (simultaneously providing “broad-spectrum lifecycle health services” and “deeply specialized disease-specific services”); and omni-payment (striving for inclusion in basic medical insurance while embracing commercial insurance). Meanwhile, these enterprises will leverage data-driven dynamic decision-making to serve consumers more precisely and enhance operational efficiency through intelligence, thereby comprehensively transitioning toward a platform-based development model.

Risk

New entrants are intensifying industry competition; strategic transformation of traditional enterprises is falling short of expectations.

In recent years, the pharmaceutical retail market has expanded, driven by escalating health demands and the outflow of hospital prescriptions, while shifts in consumer habits and the breaking down of geographical barriers have reshaped terminal traffic distribution. Meanwhile, as Health-tech continues to permeate the pharmaceutical industry, we believe that retail enterprises are poised for a comprehensive transition toward platform-based business models. The traditional role of “drug selling” is expected to be upgraded to a new role focused on “health services,” ushering in significant development opportunities for the pharmaceutical retail sector.

Multi-Dimensional Expansion: Pharmaceutical Retail Emerges as a High-Quality Sector

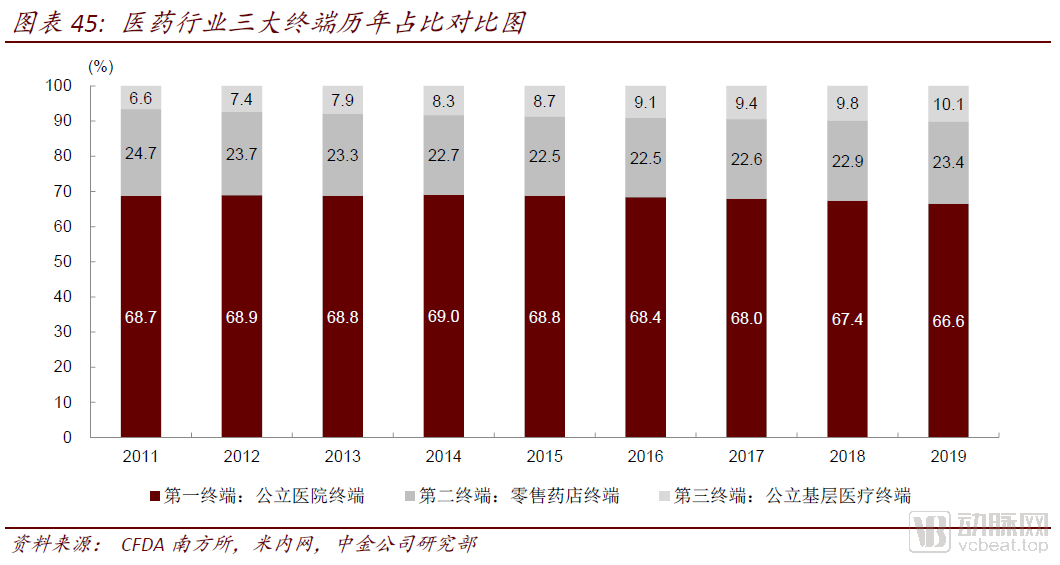

Prescription outflow is becoming a trend.According to data from the Southern Institute of the China Food and Drug Administration (CFDA), sales in China’s terminal pharmaceutical market reached RMB 1.80 trillion in 2019, with the retail segment’s share further rising to 23.4%. Benefiting from healthcare reform policies promoting the separation of prescribing and dispensing, the implementation of measures such as caps on the drug-to-revenue ratio and zero-markup pricing has driven a year-on-year increase in the retail segment’s share in recent years. We anticipate that the advancement of policies such as generic consistency evaluation and volume-based procurement will encourage pharmaceutical manufacturers to seek growth opportunities in the out-of-hospital market.

The demand for comprehensive health and wellness is growing.As health awareness rises and purchasing power increases, consumer demand for big health products and services is shifting from disease treatment to preventive care (encompassing prevention, wellness, and other areas), becoming more diversified and personalized. This trend has created a demand for full-lifecycle big health management, further expanding the growth potential of the pharmaceutical retail market.

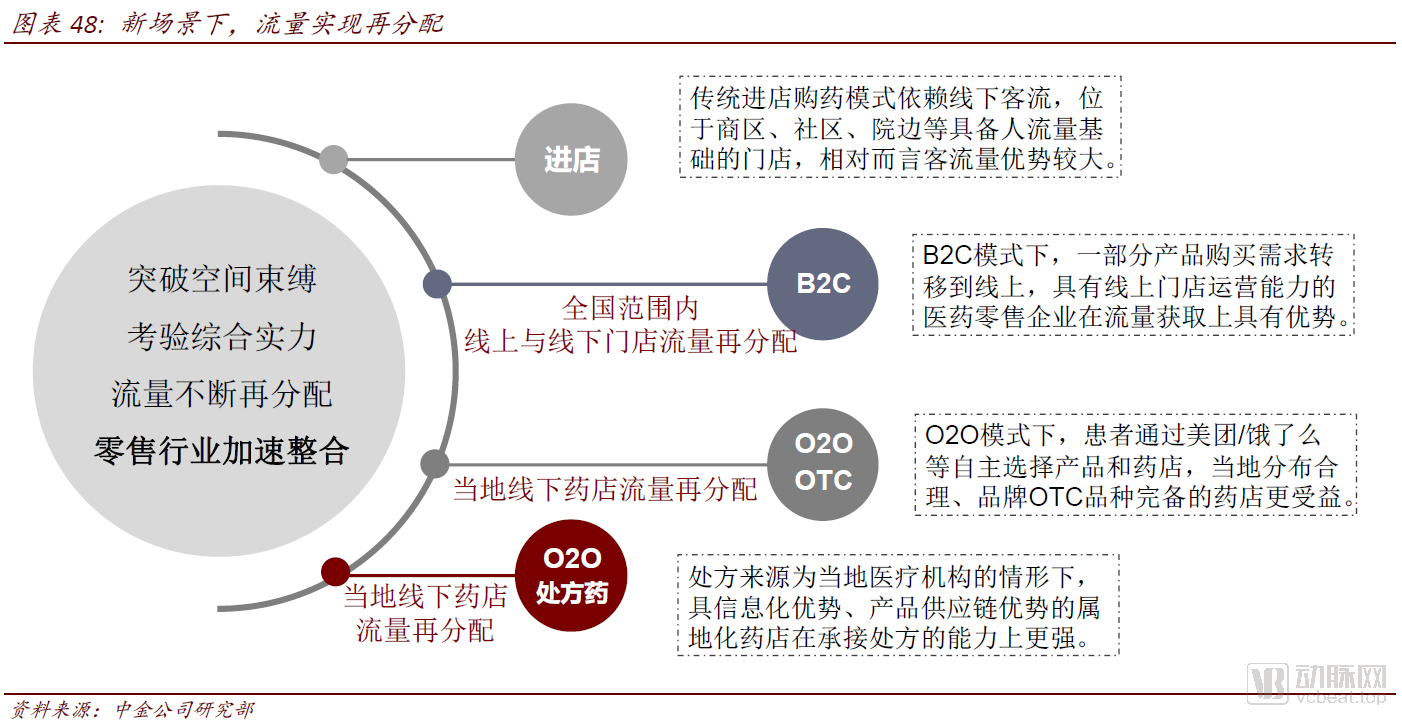

Traffic Redistribution: Industry Concentration to Accelerate

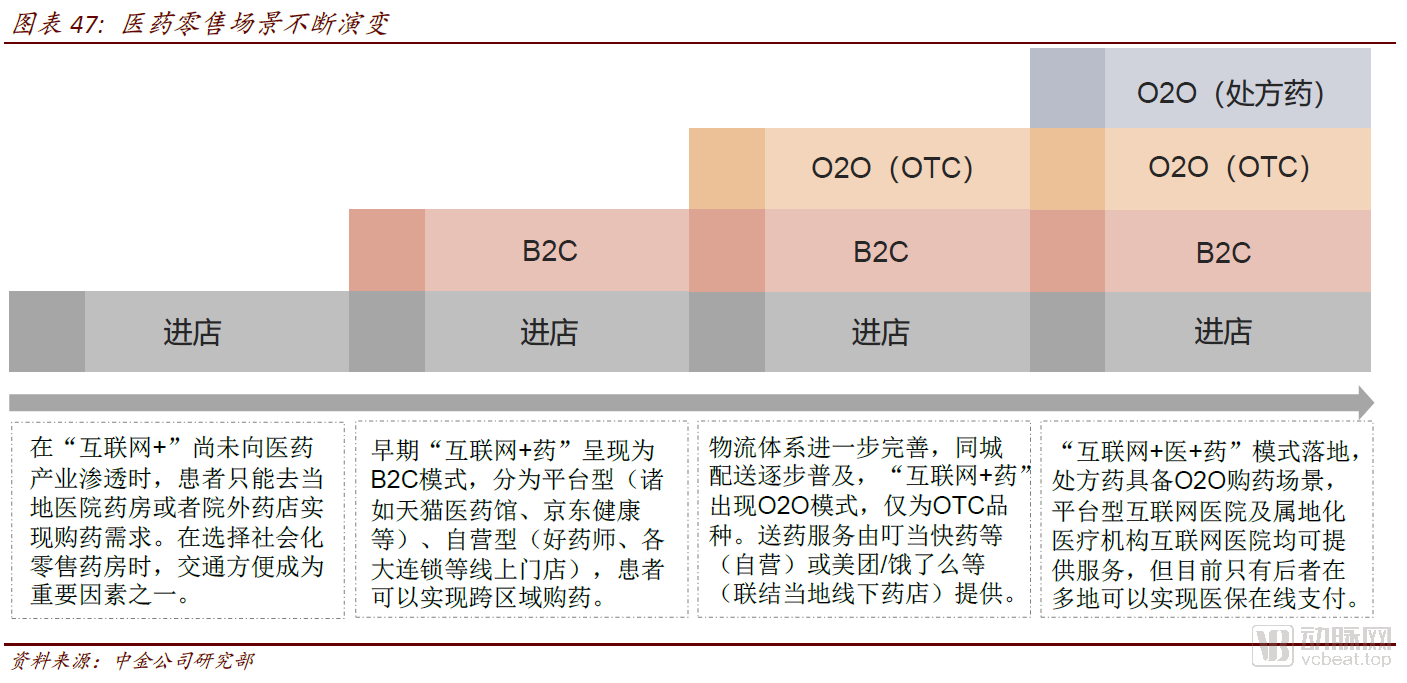

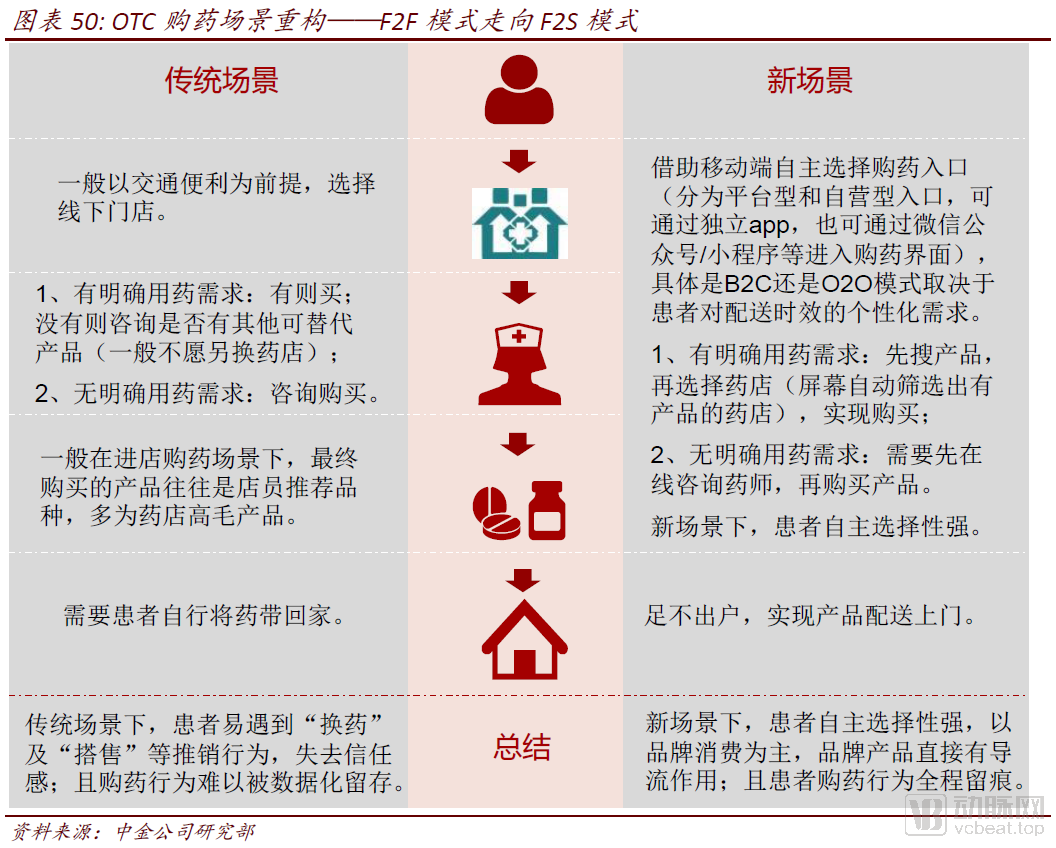

The pharmaceutical retail landscape is continuously evolving.In traditional pharmaceutical retail scenarios, patients could only purchase medications at hospital pharmacies or off-site retail pharmacies, with transportation convenience being a key consideration (particularly crucial when selecting independent community pharmacies). This gave chain stores with “dense distribution networks” a certain advantage in attracting customer traffic. With the continuous penetration of Health-tech into the pharmaceutical sector and the ongoing improvement of China’s logistics infrastructure, patients now have more diversified medication purchasing options and richer consumption scenarios. These have expanded from the most traditional in-store purchases to B2C, and further to O2O models, continuously breaking through geographical limitations. In terms of product categories, patients in the F2S scenario can currently purchase everything from OTC products to prescription drugs (primarily those for common and chronic diseases).

Under new scenarios, the service radius of stores has expanded, leading to a redistribution of traffic.For online stores primarily operating on a B2C model, the service radius can be expanded to cover the entire country; for those mainly based on an O2O model, the service radius is limited to the same-city delivery range of their corresponding offline physical entities. The advantages of traffic allocation vary across different models:

►Under the B2C Model: Across China, there is a reallocation of online and offline traffic, with stores possessing strong online operational capabilities gaining a greater advantage in traffic acquisition;

► Under the O2O model: Within the same city, local offline physical traffic is redistributed; stores with national or localized brand advantages and strong informatization capabilities are better positioned to capture traffic (for prescription drugs, product supply chain considerations also apply).

Meanwhile, new scenarios empower consumers with greater autonomy in decision-making. As geographical constraints diminish and pharmacy information becomes increasingly transparent, online stores accessed via third-party platforms—primarily B2C models such as Tmall Health and JD Health, and primarily O2O models such as Meituan, Ele.me, and JD Daojia—are continually emerging. Traffic redistribution will be consumer-led, with customers deciding which store to transact with. Furthermore, in scenarios where localized internet healthcare platforms serve as entry points, pharmacies with strong prescription fulfillment capabilities and significant local brand influence hold an advantage in traffic redistribution.

Overall, we believe that as the pharmaceutical retail landscape continues to evolve, end-user traffic will be redistributed. Industry consolidation is expected to accelerate with the penetration of Health-tech, and pharmaceutical retailers with strong comprehensive capabilities are more likely to emerge as beneficiaries.

“Internet Plus” Empowerment: Pharmaceutical Retail Poised to Transition Toward a Platform-Based Development Model

Traditional pharmaceutical retail role: “Selling drugs.”The traditional pharmaceutical industry landscape, constrained by physical spatial limitations and information asymmetry, has evolved in a linear, chain-like manner. Strategic formulation by various stakeholders—including manufacturers, distributors, healthcare institutions, and retailers—is based on their respective roles within this industrial chain: manufacturers are positioned as “producers,” distributors as “logistics providers,” and retailers as “sales endpoints.” Consequently, from a strategic perspective, manufacturers tend to be product-centric, distributors focus on warehousing and logistics, and retailers prioritize store networks, all limited by their relatively singular role definitions.

The Role of Pharmaceutical Retail in the New Era: "Service"Health-tech virtualizes and digitizes the physical spaces housing the core elements of the pharmaceutical industry, enabling the separation of terminal scenarios for patients, doctors, information flows, logistics, and capital flows. Consequently, the structure of the pharmaceutical industry is beginning to evolve toward a platform-based development model. Retail enterprises possess abundant upstream and downstream resources: upstream, they connect with numerous pharmaceutical manufacturers and distributors; downstream, they directly serve consumers while also linking with last-mile delivery platforms such as Meituan, Ele.me, and JD Daojia. With the integration of prescription circulation platforms, these retailers further connect with healthcare institutions (including platform-based internet hospitals). Retailers qualified for medical insurance reimbursement also link with medical insurance agencies, continuously breaking through the linear relationships across various segments of the pharmaceutical industry. We believe that the development of “Internet + Healthcare” presents new opportunities for pharmaceutical retail enterprises. In this new era, pharmaceutical retailers are poised to transform into a platform-based development model, upgrading from a role centered on “selling drugs” to one focused on providing “services” within the broader health and wellness sector.

Traditional pharmaceutical retail relies on face-to-face (F2F) in-store purchasing driven by foot traffic, with a “high gross margin” model as its core profitability strategy. As the “Internet + Healthcare” sector accelerates its development, traditional retailers are facing short-term challenges in expansion capabilities, service delivery, new consumption scenarios, and regulatory compliance. Meanwhile, the industry remains characterized by low chain penetration and low market concentration, while diversified expansion models have intensified competitive pressures. We believe that challenges and opportunities coexist, and the era of high gross margins may be drawing to an accelerated close.

Reshaping Traditional Retail Scenarios: The Era of High Gross Margins May Be Coming to an Accelerated End

In the early days, pharmaceutical end-consumer scenarios were entirely constrained by physical space; whether purchasing over-the-counter (OTC) products or prescription drugs, patients were required to visit brick-and-mortar stores. As medication-purchasing scenarios have evolved with the times, patients have increasingly cultivated the habit of buying medicines without visiting physical stores.

OTC Retail Scenario Restructuring

Traditional OTC purchases were primarily made through offline physical outlets in community pharmacies. Since the penetration of health-tech into the pharmaceutical industry, “Internet + OTC” initially emerged in a B2C model. With the continuous improvement of China’s logistics infrastructure, the “pharmacy + delivery” model has enabled O2O scenarios for “Internet + OTC,” achieving last-mile delivery within the same city. Consequently, terminal consumption scenarios have shifted from F2F (face-to-face) to F2S (face-to-screen), predominantly among younger consumers.

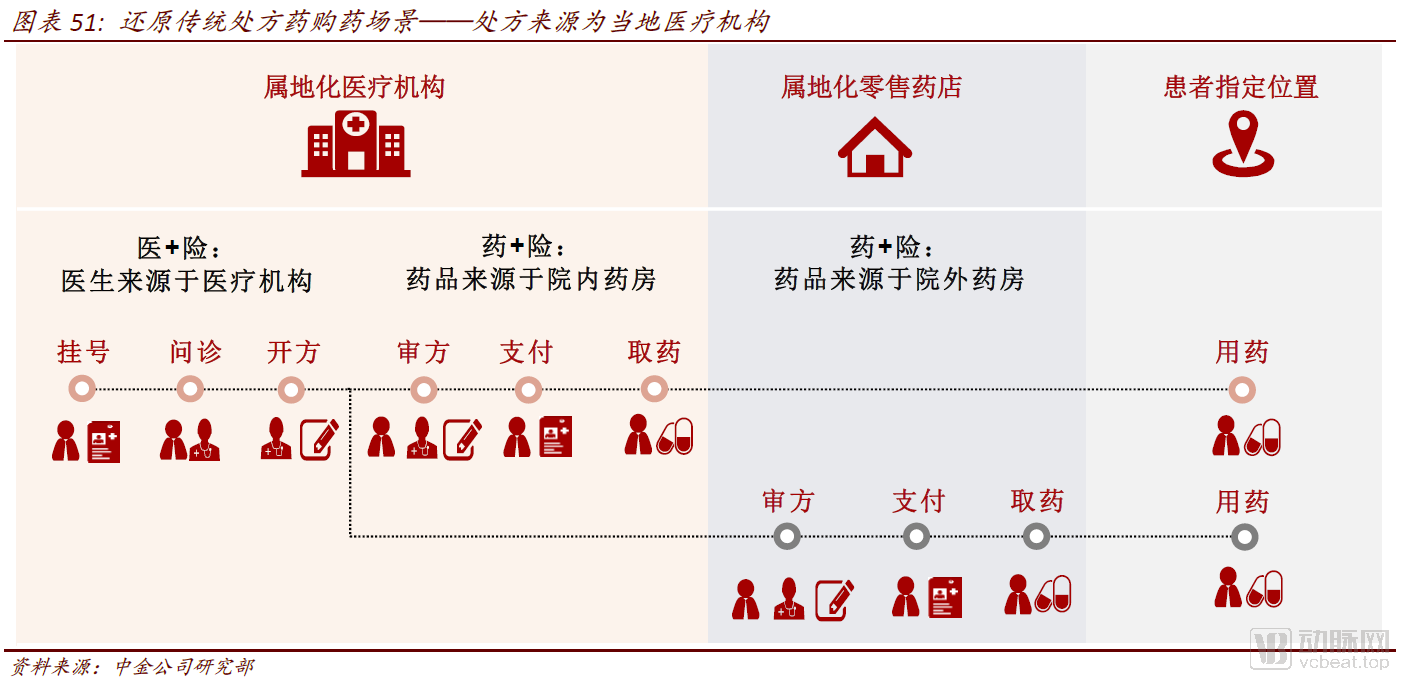

Reimagining the Retail Landscape for Prescription Drugs

Traditional prescription drug purchases occur offline, remaining a face-to-face (F2F) scenario. After obtaining a prescription from a medical institution, patients either pick up their medications at the hospital’s in-house pharmacy or purchase them at an external pharmacy using the prescription.

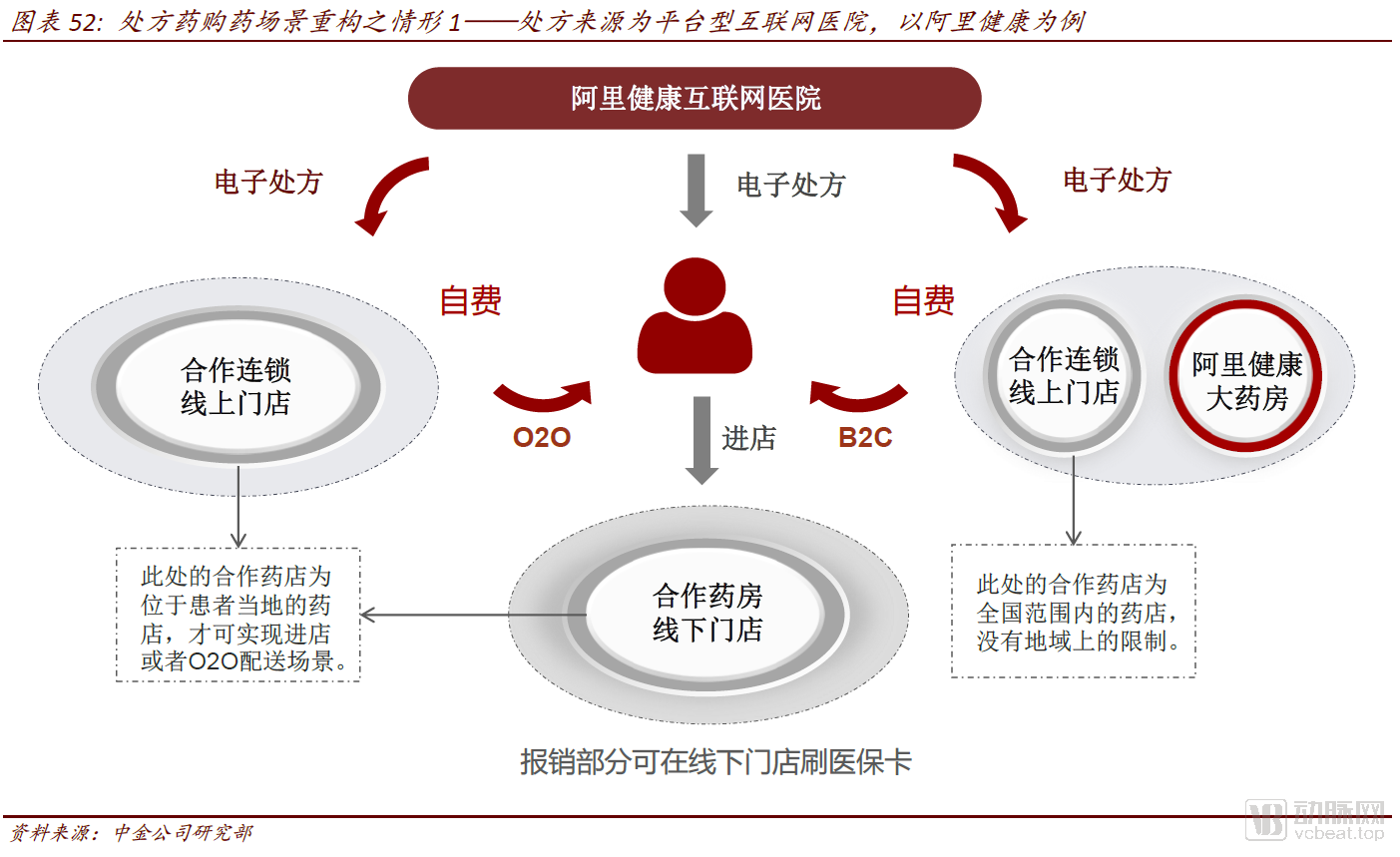

In August 2019, following the introduction of the revised Drug Administration Law, restrictions on the online sale of prescription drugs were relaxed to a certain extent. This led to a restructuring of prescription drug purchasing scenarios and the emergence of the “Internet + Healthcare + Prescription Drugs” model, with prescriptions primarily originating from platform-based internet hospitals:

► Companies represented by Alibaba Health and JD Health transfer electronic prescriptions from their proprietary internet hospitals to online pharmacies, and deliver medications directly to consumers’ doors via B2C models through third-party or in-house logistics networks.

► Companies represented by Alibaba Health, JD Health, and Ping An Good Doctor allocate electronic prescriptions from their proprietary internet hospitals to the online storefronts of brick-and-mortar pharmacies in patients’ local areas, and deliver O2O “door-to-door medication delivery” services through third-party or in-house logistics networks.

In August 2019, following the introduction of the revised Drug Administration Law, restrictions on the online sale of prescription drugs were relaxed to a certain extent. This led to a restructuring of prescription drug purchasing scenarios and the emergence of the “Internet + Healthcare + Prescription Drugs” model, with prescriptions primarily originating from platform-based internet hospitals:

► Companies represented by Alibaba Health and JD Health channel electronic prescriptions from their proprietary internet hospitals to online stores, and deliver B2C “door-to-door medication delivery” services through third-party or in-house logistics networks;

► Companies represented by Alibaba Health, JD Health, and Ping An Good Doctor allocate electronic prescriptions from their proprietary internet hospitals to the online storefronts of brick-and-mortar pharmacies in patients’ local areas, and deliver O2O “medicine-to-doorstep” services through third-party or in-house delivery systems.

During the COVID-19 pandemic, to address the challenge of non-COVID patients—particularly those with chronic diseases—in accessing timely basic medical care, the state actively promoted breakthroughs in the “Internet + Insurance” model. The fully online “Healthcare + Pharmaceuticals + Insurance” integrated model was initially implemented in many provinces and cities. Under this model, prescriptions issued by local healthcare institutions were routed through prescription circulation platforms to local retail pharmacies, primarily serving patients with chronic conditions.

“Non-store” medication purchasing habits continue to take root, accelerating the end of the traditional high-margin era

“Self-interest” as the core: The traditional pharmaceutical retail profit model relies on “in-store visits.”Traditional pharmaceutical retail has relied on operational advantages such as information asymmetry and geographic constraints, adopting a “high gross margin” model as its primary profit strategy. However, this self-serving business philosophy is contingent upon a specific scenario: “customers visiting the store.” In this “in-store” context, retail outlets acquire customers through low prices, promotions, or even non-compliant practices, and then promote high-margin products to achieve profitability.

From “Self-Interest” to “Altruism”: The Era of High Gross Margins May Be Coming to an Accelerated EndCurrently, the end-user medication purchasing scenario is shifting from Face-to-Face (F2F) to Face-to-Screen (F2S). Whether through B2C or O2O models, consumers no longer need to visit physical stores, thereby continuously cultivating the habit of “non-store” purchasing. Apart from certain prescription drug scenarios, consumers can now choose not only medications but also pharmacies, reflecting an enhanced capacity for self-directed decision-making. Looking ahead, we believe that an “altruistic” model centered on user experience will become the core operational philosophy in the new era of pharmaceutical retail, and the era of high gross margins may be coming to an accelerated end.

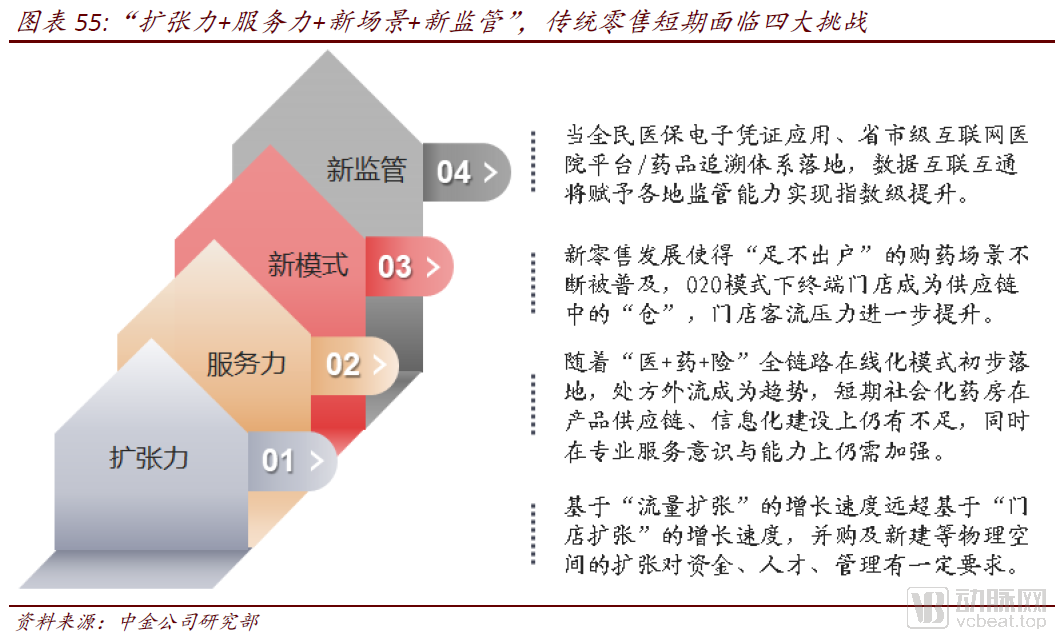

“Internet + Healthcare” Accelerates Development, Traditional Retail Faces Four Major Challenges in the Short Term

As “Internet + Healthcare” accelerates its development, traditional retail faces challenges in the short term across four dimensions: expansion capability (insufficient emphasis on the “traffic expansion” strategy), service capability (the need to enhance prescription fulfillment capacity and professional service levels), new scenarios (stores becoming “warehouses” in F2S/face-to-screen scenarios), and new regulatory landscapes (health-tech enabling an exponential increase in regulatory capabilities).

Expansion Power: Insufficient Emphasis on the “Traffic Expansion” Strategy

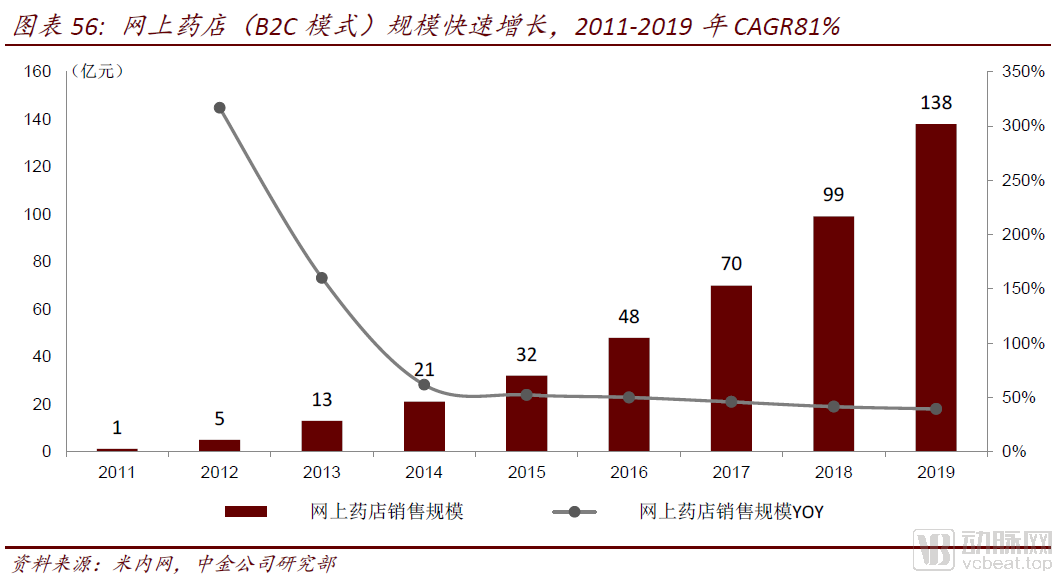

From 2011 to 2019, the market size of online pharmacy terminals under the B2C model achieved rapid growth (with low penetration, accounting for only 3.3% of the total retail terminal market in 2019), registering a CAGR of 81.0%, while the CAGR for the physical retail pharmacy market during the same period was 9.3%.

Traditional retail has placed insufficient emphasis on the B2C development model, with its strategy primarily focused on physical expansion.In terms of traditional retail strategic expansion, the focus has primarily been on “store expansion,” achieving growth in physical space through new store openings or mergers and acquisitions. However, since the emergence of the B2C model, traditional pharmaceutical retail enterprises have varied significantly in their strategic emphasis on online operations. While most chain pharmacies have obtained approval for internet drug trading qualifications and established online pharmacies on third-party platforms such as Tmall Medicine, or even built self-operated platforms, they have not actively explored operational strategies to enhance their ability to expand beyond geographical constraints. Although the current O2O (Online-to-Offline) model has extended the service radius, it mainly facilitates the redistribution of traffic within the same city, remaining constrained by the distribution of offline stores.

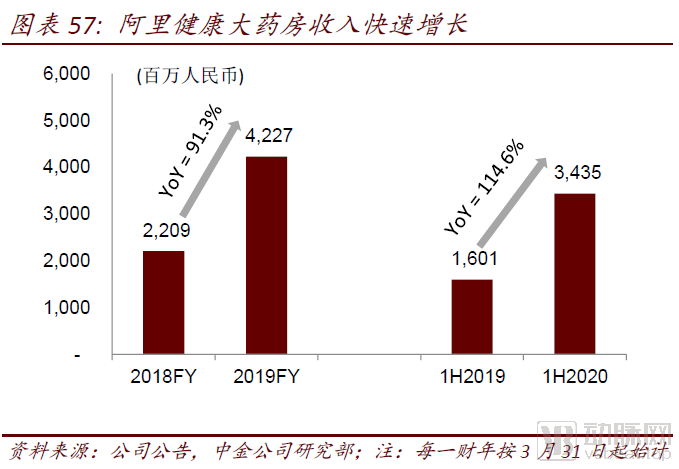

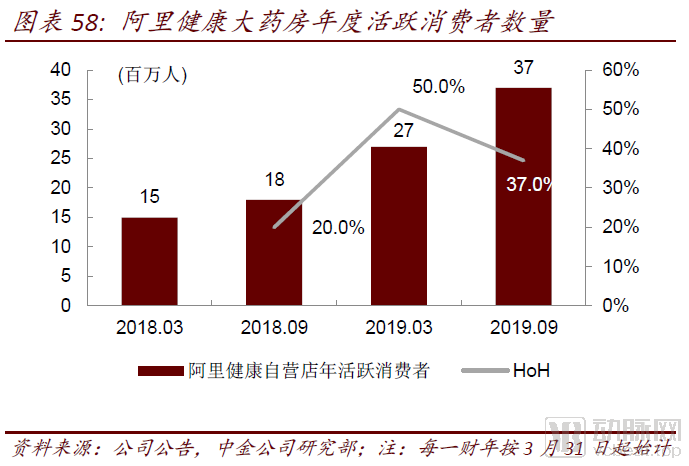

New retail enterprises prioritize a strategy centered on “traffic expansion.”Taking Alibaba Health as an example, the company acquired Guangzhou Wunianqian Pharmaceutical Chain Co., Ltd. in 2016, officially launching its B2C self-operated retail business. Although it entered the market later than competitors, leveraging the ecosystem support of the Alibaba Group and placing high strategic emphasis on the development of its B2C operations, the company has achieved rapid growth in recent years. It has continuously strengthened “traffic expansion,” broken through geographical limitations, and sustained revenue growth driven by an increase in annual active consumers.

Service Capability: Prescription Fulfillment Capacity and Professional Service Levels Need Improvement

During the COVID-19 pandemic, the fully online “medical care + pharmaceuticals + insurance” model was initially implemented in many provinces and cities. We believe that as this model becomes more widespread, it may accelerate the outflow of prescriptions from hospitals and promote the separation of medical services from pharmaceutical dispensing. However, in the short term, socialized pharmacies still face deficiencies in product supply chains and information technology infrastructure, while also needing to enhance their professional service awareness and capabilities.

►Matching Capability Between Prescription Drugs and Medical Institutions: Traditional pharmaceutical retail enterprises primarily rely on over-the-counter (OTC) drug sales, and their product supply chains differ significantly from those of medical institutions. In the short term, there is still room for improvement in their capacity to handle prescription orders. In contrast, retail pharmacies affiliated with local commercial companies that hold integrated wholesale and retail licenses possess stronger advantages in product supply chains and maintain more comprehensive collaborations with local medical institutions;

►Pharmacist Professional Service Level for Prescription Patients: Unlike OTC drugs, prescription drugs have special requirements for usage methods and timing, and must be used under the guidance of a physician; with the outflow of prescriptions, retail pharmacies that accept prescriptions, except

Beyond merely selling medications to patients, if pharmacies wish to strengthen patient communication and provide health management services, they require professional pharmacists to deliver specialized care. This is particularly crucial in brick-and-mortar stores, where face-to-face interactions are leveraged to enhance the warmth and personal touch of service. In such settings, it is essential to elevate professional service awareness and competence, de-emphasize assessments based on high gross margins, and build patient trust.

New Scenario: F2S (Factory-to-Store) Medication Purchase Model, with Retail Stores Serving as “Warehouses”

The development of “Internet + Healthcare” has increasingly popularized the scenario of patients purchasing medications without leaving their homes. Particularly under the fully online model integrating “medical care, pharmaceuticals, and insurance,” collaborative efforts among pharmaceutical manufacturers, distributors, local medical/pharmaceutical/insurance institutions, mobile payment platforms, and last-mile delivery services have further enabled local medical insurance support for the home-based purchase of prescription drugs. Overall, in the B2C model, medications are sourced from offline warehouses linked to online stores and reach patients through cross-regional delivery; in the O2O model, medications are sourced from local brick-and-mortar stores corresponding to online storefronts, with these stores serving as forward stock locations and reaching patients via same-city delivery. Both models intensify the pressure on physical stores due to declining foot traffic.

New Regulation: Health-tech Empowers Regulators with Exponential Capability Enhancement

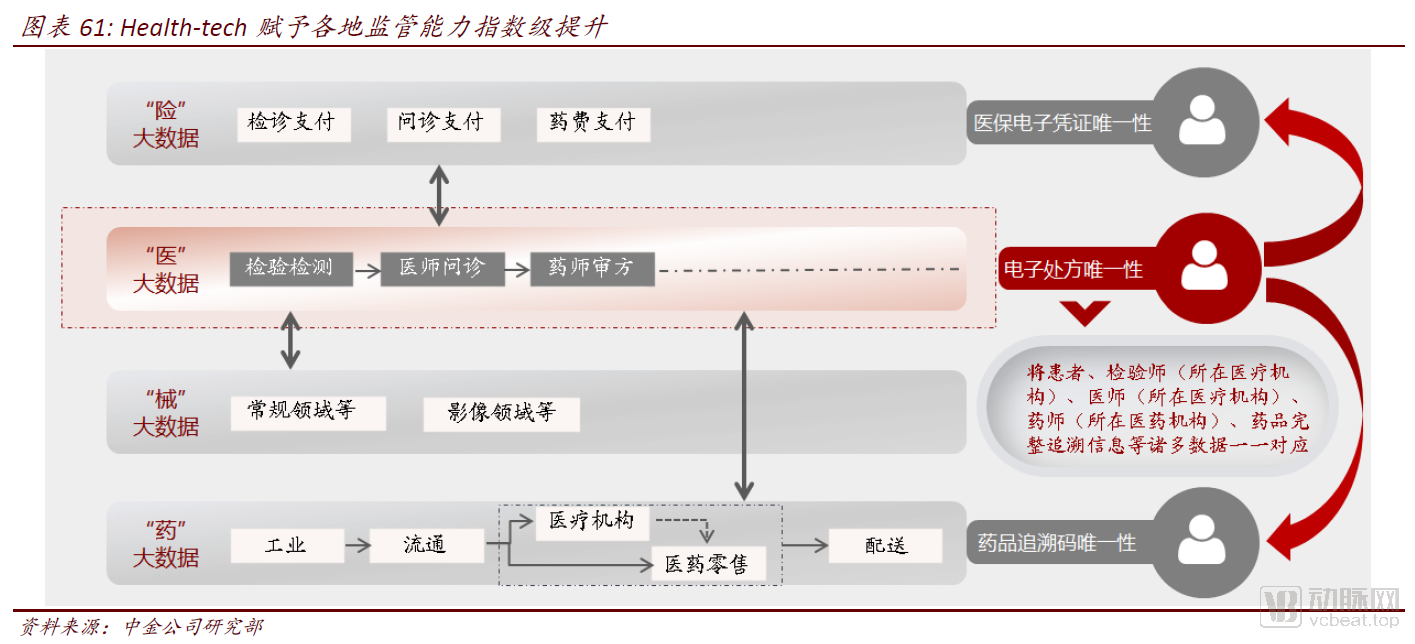

End-to-End Traceability, Empowering an Exponential Leap in Regulatory Capabilities.We believe that the advancement of information infrastructure for China’s healthcare, pharmaceutical, and medical insurance systems will facilitate the widespread adoption of fully online “healthcare + pharmaceuticals + insurance” integrated services in areas such as follow-up visits for common and chronic diseases. Provincial and municipal internet healthcare service regulatory platforms integrate both service delivery and oversight functions. Through prescription circulation platforms, medical institutions achieve data interoperability with pharmaceutical entities, enabling end-to-end traceability of diagnosis and treatment, prescriptions, transactions, and distribution, as well as comprehensive monitoring of information, capital, and logistics flows. This significantly enhances regulatory capabilities by orders of magnitude.

Health-tech continues to penetrate the market, with compliance costs rising steadily.The development of “Internet + Healthcare” has already introduced technologies such as fingerprint recognition and facial recognition. We believe that in the future, it will further incorporate technologies like the Internet of Things (IoT) and blockchain. Every individual has left various types of data in cyberspace, which collectively form user profiles. In particular, mobile payment platforms are further shaping personal credit system profiles (mobile payments transform transactions from “intangible” to “traceable,” making transaction behaviors retrievable, monitorable, and traceable in cyberspace), and these are closely linked to personal identity information. As health-tech continues to penetrate the pharmaceutical industry, we anticipate that national regulatory capabilities will strengthen, and the compliance costs for pharmaceutical retail operations will continue to rise.

The industry remains in a phase of “low chain affiliation rate + low market concentration,” leading to intensified competition.

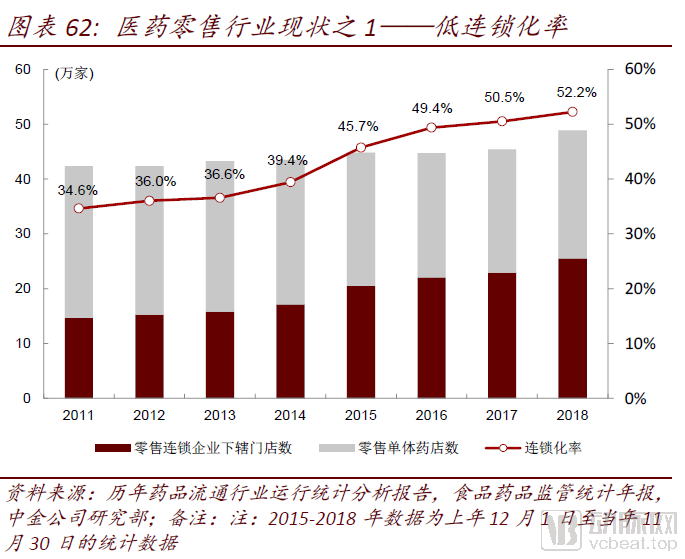

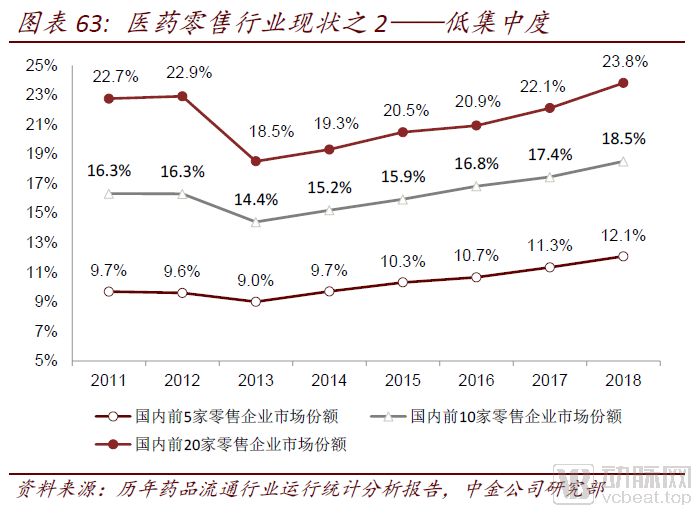

The industry remains characterized by “low chain affiliation rates and low market concentration,” with the final competitive landscape yet to take shape. According to data from the 2018 Statistical Analysis Report on the Operation of the Pharmaceutical Distribution Industry, as of the end of 2018 (with the reporting period ending on November 30, 2018), the total number of brick-and-mortar pharmacies in China reached 489,063. Among these, there were 5,671 chain enterprises (operating 255,467 stores) and 233,596 independent pharmacies, resulting in a chain affiliation rate of 52.2%. In 2018, the revenue share of the top five retail pharmaceutical enterprises in China was approximately 12.1%. We believe that China’s pharmaceutical retail industry is still in a phase of low chain affiliation and low concentration, and the competitive landscape is poised for reshaping.

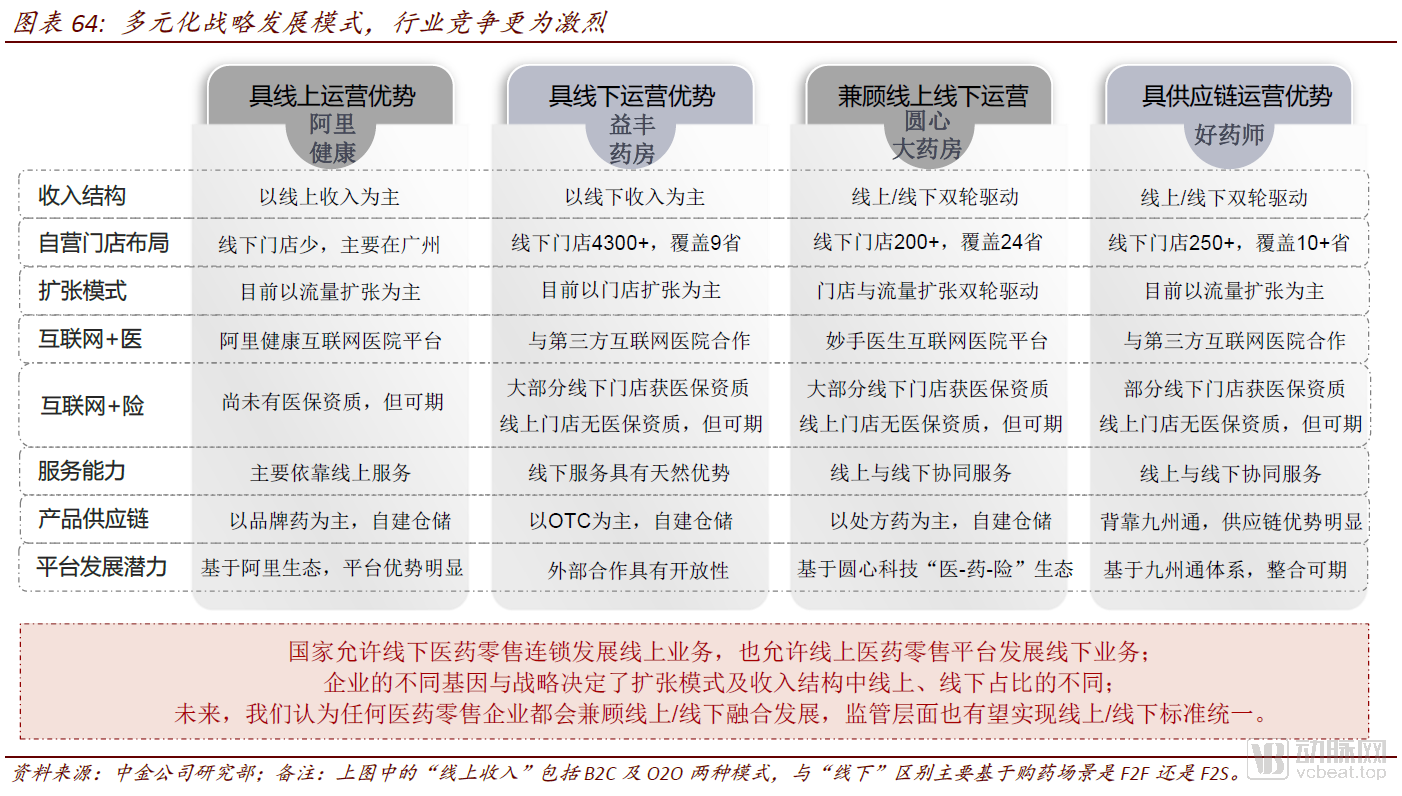

Diversified expansion models have intensified industry competition.“Internet + Healthcare” has evolved to a stage where the state permits offline pharmaceutical retail chains to develop online operations, while also allowing online pharmaceutical retail platforms to expand into offline business. The distinct corporate DNA and strategies of enterprises determine their expansion models and the respective proportions of online and offline revenue. As the industry remains in a consolidation phase, diversified expansion models have intensified competition. We believe that with an increasing number of new entrants and the ongoing transformation of traditional retail, the following four types of enterprises hold advantages in the redistribution of terminal traffic, leveraging their respective operational strengths:

► Strengths in online operations: Represented typically by Alibaba Health and JD Health, these players have few offline stores. At the strategic level, they prioritize online traffic expansion to break through geographical limitations and achieve nationwide coverage across China. Their business models encompass both platform-based and self-operated services, integrating B2C and O2C models. They offer both “Internet + Pharmaceuticals” and “Internet + Healthcare” segments, forming an integrated “Internet + Healthcare + Pharmaceuticals” dual-service ecosystem within their systems. The medication purchasing scenario is primarily “face-to-screen,” where consumers exhibit strong autonomous decision-making capabilities. Consequently, product sales are dominated by branded products, and partnerships focus mainly on pharmaceutical manufacturers with inherent traffic advantages. However, they currently lack medical insurance accreditation, so consumers primarily pay out-of-pocket.

► Advantages in offline operations: Represented typically by Yifeng Pharmacy and Laobaixing, these enterprises operate a large number of physical stores. Their current strategy prioritizes offline store expansion, with coverage primarily focused on provinces and cities where they have established a presence. In the “Internet + Pharmaceuticals” sector, the O2O model is dominant, while the B2C model still holds significant room for operational improvement. In the “Internet + Healthcare” sector, collaboration with platform-based internet hospitals is the primary approach. As the entire “Healthcare + Pharmaceuticals + Insurance” value chain moves online, prescription sources are increasingly channeled through prescription circulation platforms to localized medical institutions. The greatest current advantage of physical stores lies in their medical insurance accreditation and the provision of face-to-face service scenarios, which offer a more personalized and empathetic experience. However, this requires de-emphasizing a “high gross margin” orientation and building trust with patients.

► Balancing Online and Offline Operations: Exemplified by Yuanxin Pharmacy and Dingdang Kuaiyao, these enterprises were established during the growth phase of “Internet + Healthcare.” Strategically, they were positioned from inception to adopt a new retail development model, emphasizing synergistic expansion and development across both online and offline channels. Their operations encompass physical store networks as well as B2C and O2O models, with offline activities primarily driven by the O2O model. Yuanxin Pharmacy further leverages Yuanxin Technology to achieve end-to-end integration of “healthcare, pharmaceuticals, and insurance,” pioneering the continuous incorporation of commercial health insurance into terminal scenarios of the pharmaceutical industry and formulating its development strategy directly around a platform-based model.

► Supply Chain Operational Advantages: Represented by Haoyaoshi (affiliated with Jointown Pharmaceutical Group) and Shanghai Pharma Cloud Health (affiliated with Shanghai Pharmaceuticals), these entities belong to leading national distribution enterprises integrating wholesale and retail operations. They possess significant advantages in healthcare institution coverage and robust product supply chain operations. Particularly in the era of comprehensive online development across the “medical care + pharmaceuticals + insurance” value chain, new opportunities have emerged. We believe that retail enterprises with a wholesale-retail integrated background have the potential to integrate abundant upstream and downstream resources and transition toward a platform-based development model. However, this premise requires unified information systems and seamless data interoperability across regional subsidiaries and business segments, thereby enabling more flexible and efficient maximization of overall competitive advantages.

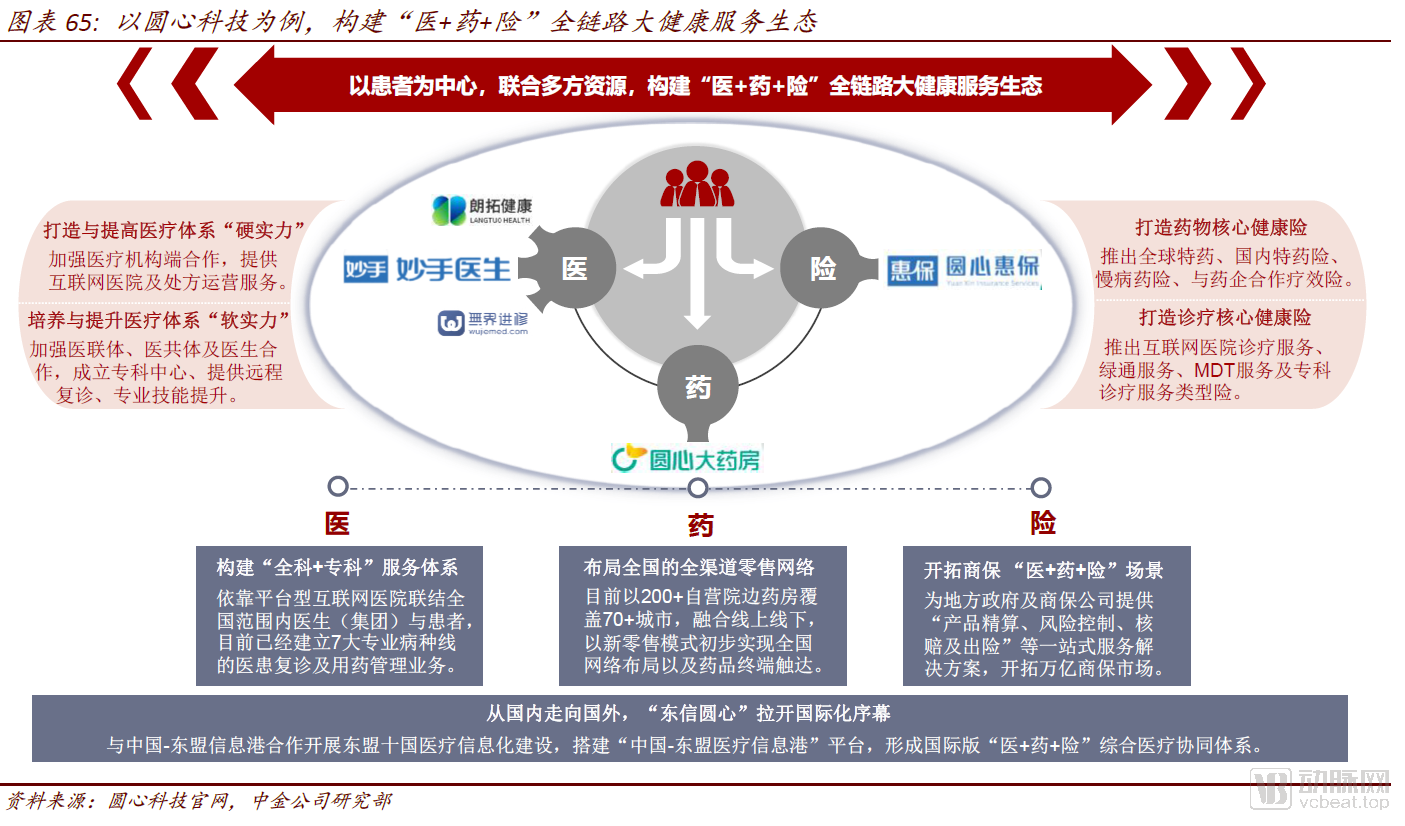

As Yuanxin Technology has not yet gone public, with limited publicly available data, we analyze its strategic layout from the perspective of its business operations:

Founded in 2015, the company has developed its “Internet + Healthcare” services based on “Miaoshou Doctor,” its “Internet + Pharmaceuticals” services based on “Yuanxin Pharmacy,” and its “Internet + Insurance” services based on “Yuanxin Huibao.” Leveraging “Langtuo Health,” it provides medical institutions with informatization construction, as well as the development and operation of internet hospitals. Through a platform-based development strategy, the company connects patients, physicians, pharmaceuticals, and insurance sectors, achieving full-chain integration of “healthcare + pharmaceuticals + insurance.”

By the end of 2019, Yuandian Pharmacy had covered 24 provinces and 70 cities through more than 200 self-operated pharmacies located near hospitals and Direct-to-Patient (DTP) pharmacies, initially establishing a nationwide pharmacy network. Miaoshou Internet Hospital had accumulated over 100,000 registered and contracted specialists in specific diseases, providing professional services for follow-up consultations and medication management in fields such as oncology, hematology, dermatology, hepatobiliary diseases, rheumatism, psychosomatic medicine, reproductive health, and andrology. Yuandian Huibao offers one-stop service solutions to local governments and commercial insurance companies, including product actuarial analysis, risk control, claims assessment, and incident handling. Meanwhile, the company collaborates with the China-ASEAN Information Harbor to advance healthcare informatization in the ten ASEAN countries, building the "China-ASEAN Medical Information Harbor" platform to facilitate pharmaceutical import and export channels and further expand into international markets.

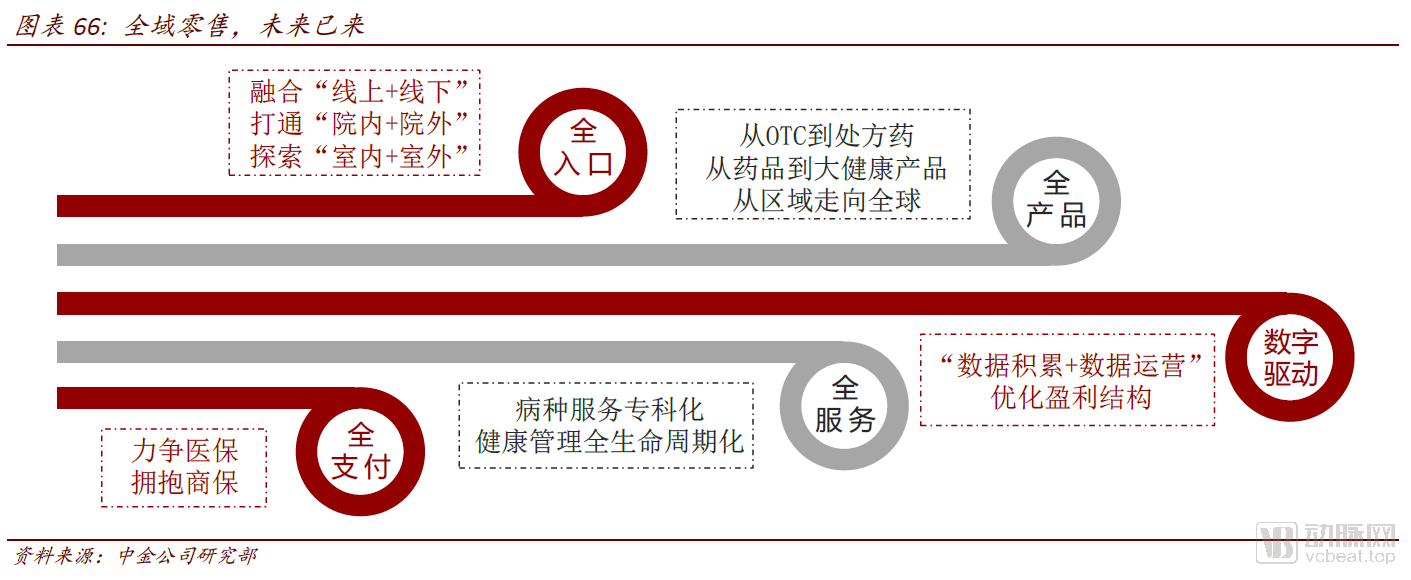

The development of “Internet + Healthcare” has empowered local governments with more comprehensive and real-time regulatory capabilities, granted consumers greater choice and decision-making authority, and simultaneously provided retail enterprises with stronger expansion capabilities and broader development space. We believe that although the industry faces short-term challenges, the pharmaceutical retail sector is comprehensively ushering in new development opportunities in the medium to long term.

We believe that the future of the pharmaceutical retail industry will be consumer-centric, achieving omnichannel expansion across multiple dimensions—including all entry points, product portfolios, service offerings, and payment methods. Meanwhile, driven by data-enabled dynamic decision-making, the industry will serve consumers with greater precision and enhance operational efficiency through intelligence, paving the way for a comprehensive upgrade toward a platform-based development model.

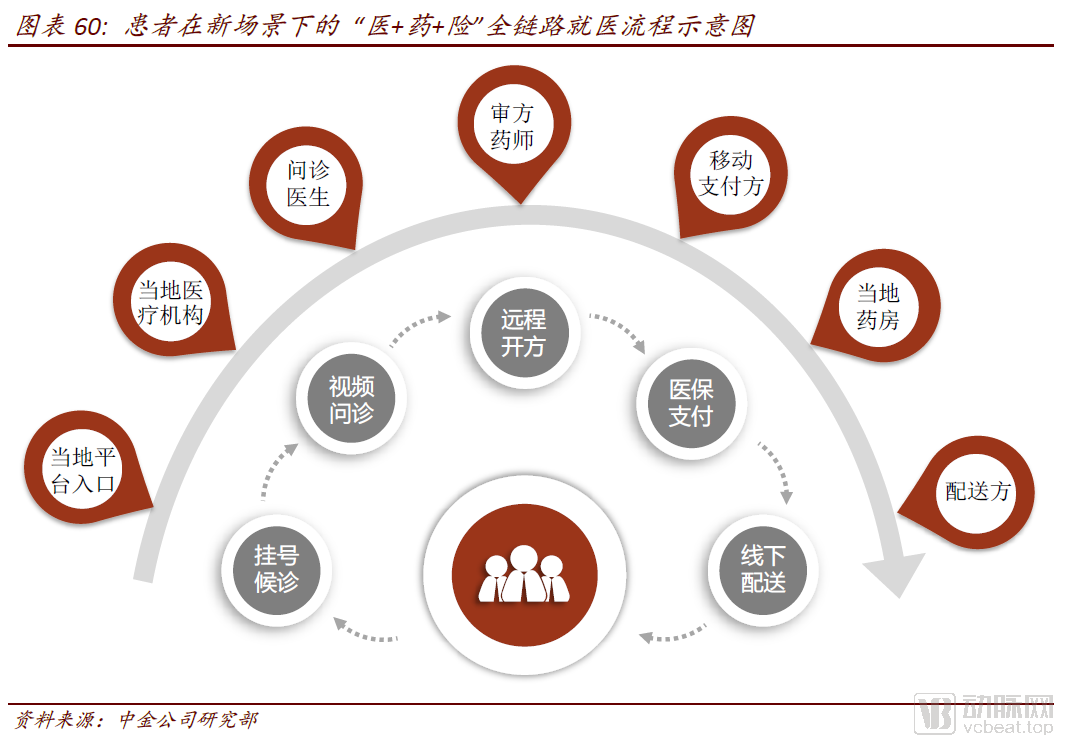

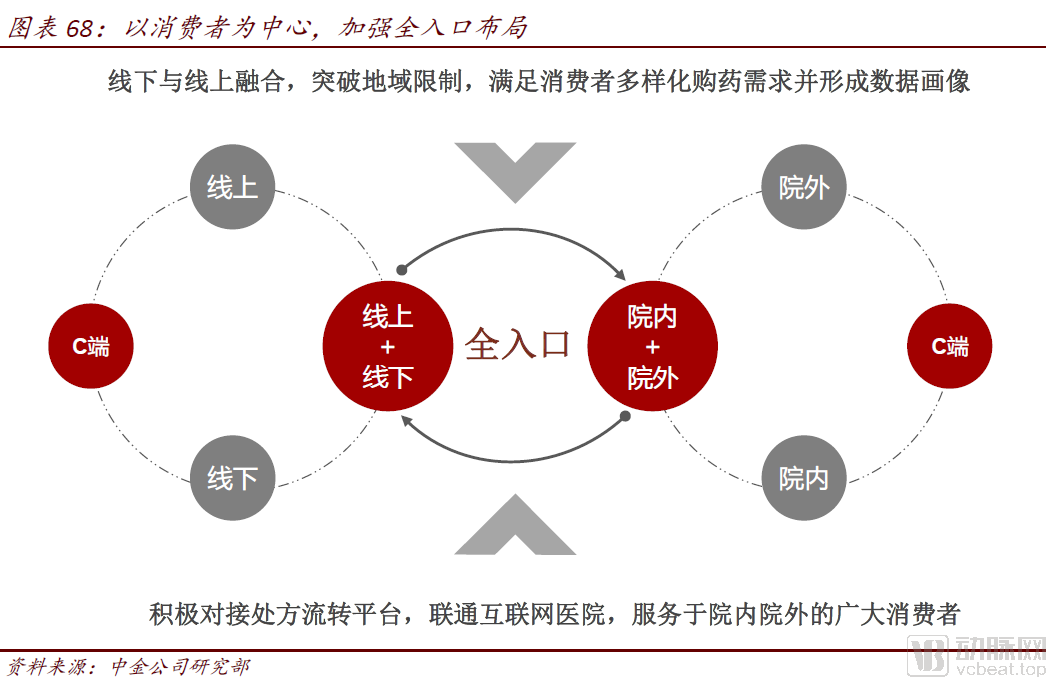

Full-Channel Access: Integrating “Online + Offline,” Connecting “In-Hospital + Out-of-Hospital,” and Exploring “Indoor + Outdoor”

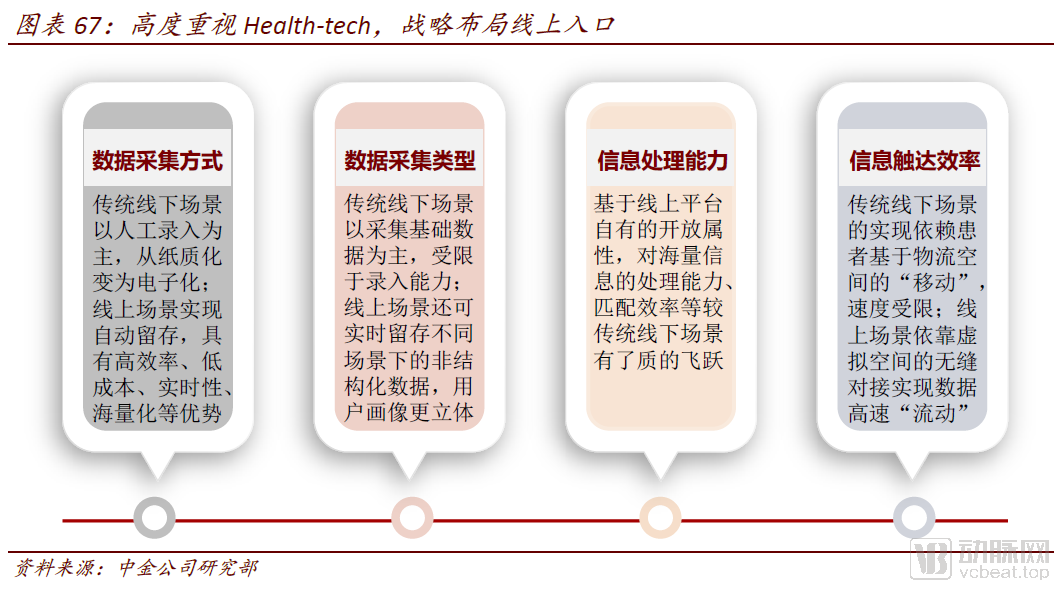

Place high priority on Health-tech and strategically lay out online channels.Health-tech is driving breakthrough transformations in traditional pharmaceutical scenarios by virtualizing and digitizing physical spaces, offering distinct advantages in data collection methods, data types, information processing capabilities, and information delivery efficiency. We believe that establishing a strong online presence holds significant strategic importance. As the pharmaceutical industry enters the data era, the acquisition and accumulation of consumer data are prerequisites for pharmaceutical retail enterprises to manage and monetize their data assets. Only by adopting a consumer-centric approach, integrating online and offline medication purchase scenarios, and continuously accumulating and operating C-end (consumer-side) data can companies deeply uncover health needs, achieve precision marketing, provide more accurate products and services, actively facilitate sales, and enhance monetization capabilities.

The continuous entry of traffic platforms has created a diversified landscape for market access in the pharmaceutical industry.We believe that the broader healthcare sector represents a high-quality market track, characterized by inelastic medical demand and consumer-driven demand for prevention and wellness care. As traffic-heavy platforms such as Alibaba and JD.com deepen their engagement in the broader healthcare industry, we anticipate that other companies with significant platform advantages—including Tencent, Baidu, Meituan, Pinduoduo, Douyin, and Xiaomi—may emerge as potential entrants to consolidate the pharmaceutical industry. This will foster a diversified landscape for pharmaceutical industry development, featuring various entry points such as e-commerce platforms, internet hospitals, mobile payment systems, O2O delivery services, live-streaming channels, and IoT interfaces. Although these entry points differ, each can partially meet consumers’ whole-lifecycle healthcare needs, depending on the comprehensiveness of the products and services integrated by each platform.

As entry points to the big health platform become increasingly diversified, we recommend strengthening our layout across all access channels:

► Integration of “Online + Offline”: In addition to the traditional model of expanding physical stores, strengthen the development of the O2O (Online-to-Offline) model to leverage brand advantages and expand the radius of localized services. Simultaneously, enhance the B2C (Business-to-Consumer) model to further break through geographical limitations and achieve traffic expansion across China.

► Integrate “in-hospital + out-of-hospital” services: Connect with localized internet hospital platforms, actively accommodate outsourced prescriptions, develop a fully online “medical care + pharmaceuticals + insurance” end-to-end model, accumulate more patient resources, and further expand service scenarios centered on patient needs;

► Exploring “Indoor + Outdoor” Scenarios: We believe that with the development of 5G and the Internet of Things (IoT), indoor home environments such as living rooms are poised to become new settings for comprehensive health services. This is particularly relevant for elderly individuals with limited mobility. In the future, retail terminals are expected to leverage these indoor home scenarios to deliver chronic disease management services with certain social attributes for affected populations.

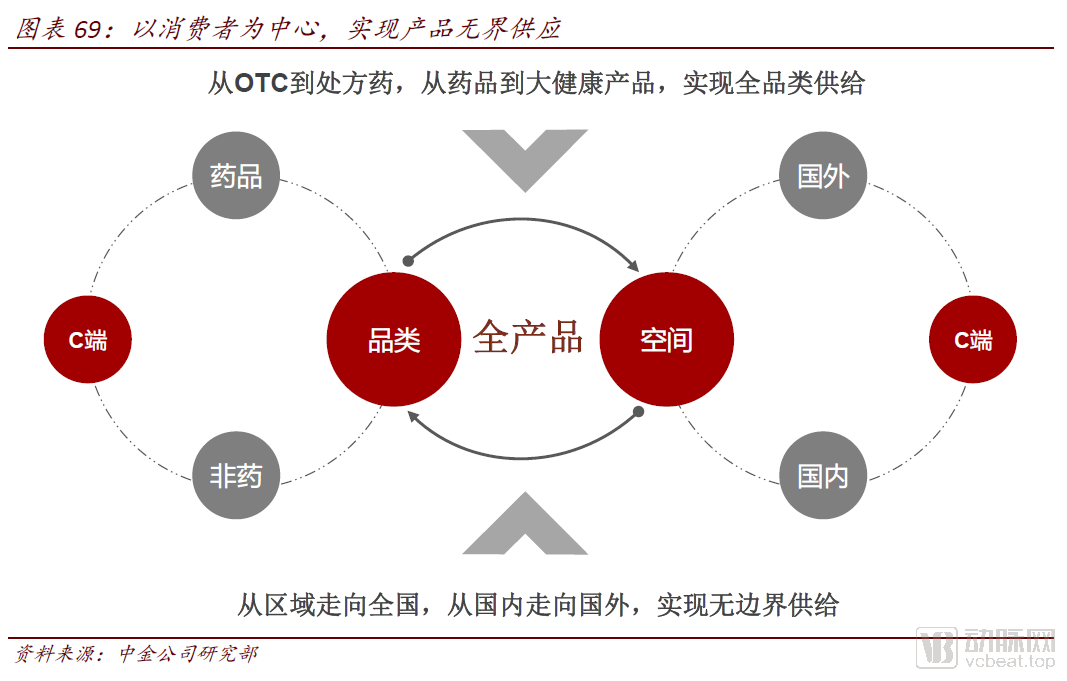

Full Product Portfolio: From OTC to Prescription Drugs, from Pharmaceuticals to General Health Products, from Regionalized Products to Borderless Products

As health awareness strengthens and purchasing power rises, consumer demand for general health products is extending from the basic realm of “disease treatment” to prevention and wellness, expanding into the domain of “preventive care.” We recommend achieving borderless supply of general health products:

►From OTC to Prescription Drugs: Strengthen collaboration with branded OTC partners (leveraging the traffic advantages of branded products) to meet consumer demand for branded products, while simultaneously enhancing the prescription drug supply chain to improve capacity for fulfilling prescription orders;

► From Pharmaceuticals to General Health Products: We believe that the tiered and classified management of pharmacies is likely to be implemented in the future. Health and wellness stores will break through the limitations of pharmaceutical products, comprehensively meeting consumers’ broader health needs. Pharmaceutical retail enterprises can achieve borderless supply of health and wellness products by establishing both offline and online stores, thereby overcoming shelf-space constraints.

► From Regional Products to International Products: The Internet is increasingly empowering consumers to access product information, while a sophisticated logistics system further enhances the ability of products to reach consumers. We believe that consumer demand for cross-border purchases in the general health and wellness sector, particularly for healthcare-related products, is poised to grow steadily.

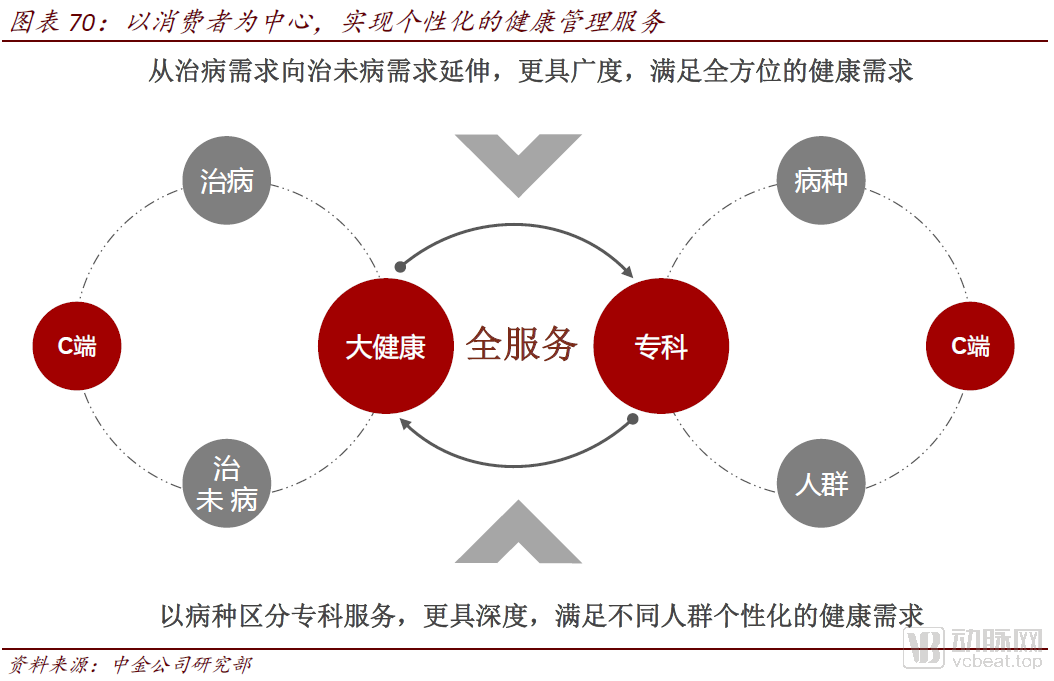

Full-Service: Differentiated User Structure, Specialized Disease-Specific Services, and Full-Lifecycle Health Management

Healthcare services are unique in nature. While online services can enhance accessibility and improve patient experience, offline services such as testing, diagnosis, intravenous infusion, and surgery remain irreplaceable. With the advancement of “Internet + Healthcare,” we believe that, in addition to physical medical institutions, brick-and-mortar retail stores will emerge as one of the core service endpoints. We recommend adopting a strategy that differentiates by target population and specializes by disease category, combining both breadth and depth to provide consumers with personalized, full-lifecycle health management:

►Full Lifecycle Health Management: Greater Breadth: Leverage a platform-based development model to connect with more health and wellness service providers, including physical examinations, traditional Chinese medicine services, medical aesthetics, dentistry, ophthalmology, orthopedics, wellness and elderly care, nursing, and maternal and child care, so as to meet the personalized, full-lifecycle service needs of diverse populations;

►Specialized Disease-Specific Services, Greater Depth: As prescription outflow accelerates, we believe that professional services targeting patients with prescription drug needs are critically important and will become one of the core competitive advantages of offline brick-and-mortar pharmacies. By providing specialized disease-specific services, pharmacies can not only more professionally and comprehensively meet patients’ deeper healthcare needs but also further facilitate integration with commercial health insurance.

Full Payment Coverage: Striving for Medical Insurance Integration, Embracing Commercial Health Insurance

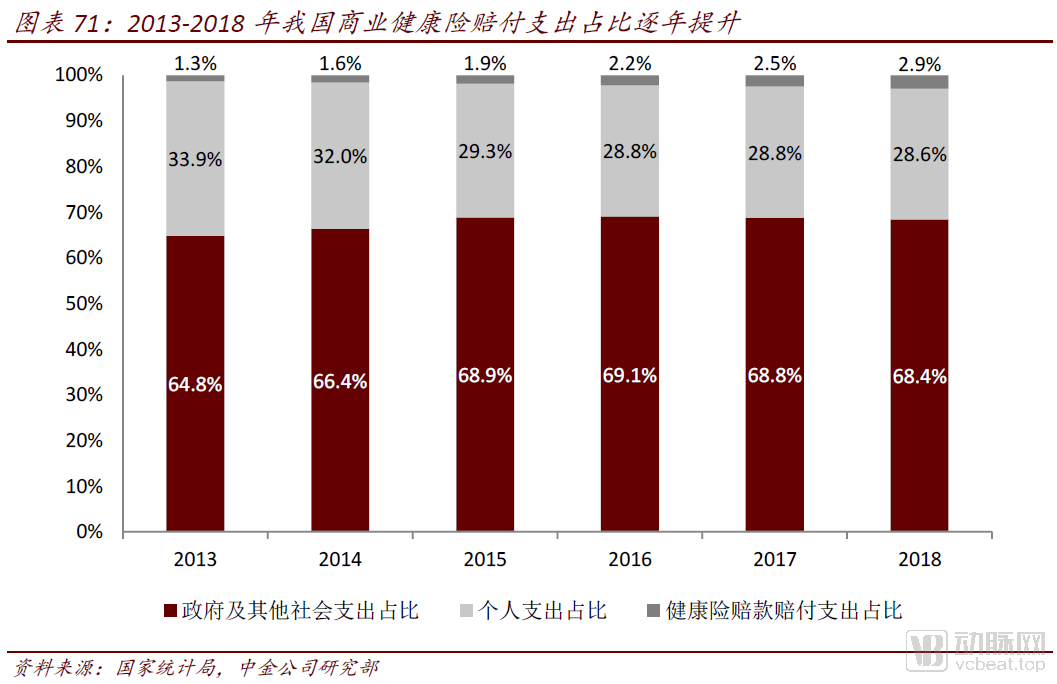

As the development environment for health insurance in China continues to improve, data from the China Insurance Yearbook shows that national health insurance premium income grew from RMB 69.2 billion in 2011 to RMB 544.8 billion in 2018, with a CAGR of 34%, demonstrating a trend of rapid growth. In 2018, China’s total health expenditure was approximately RMB 5.9 trillion, with commercial health insurance claims accounting for about 2.9%. We believe that the penetration rate of commercial health insurance in China remains low and is poised to become a significant payer in the broader healthcare sector in the future. We recommend that, in addition to striving for qualifications within the basic medical insurance system, companies should strengthen cooperation with commercial insurers and explore more scenarios for comprehensive health management.

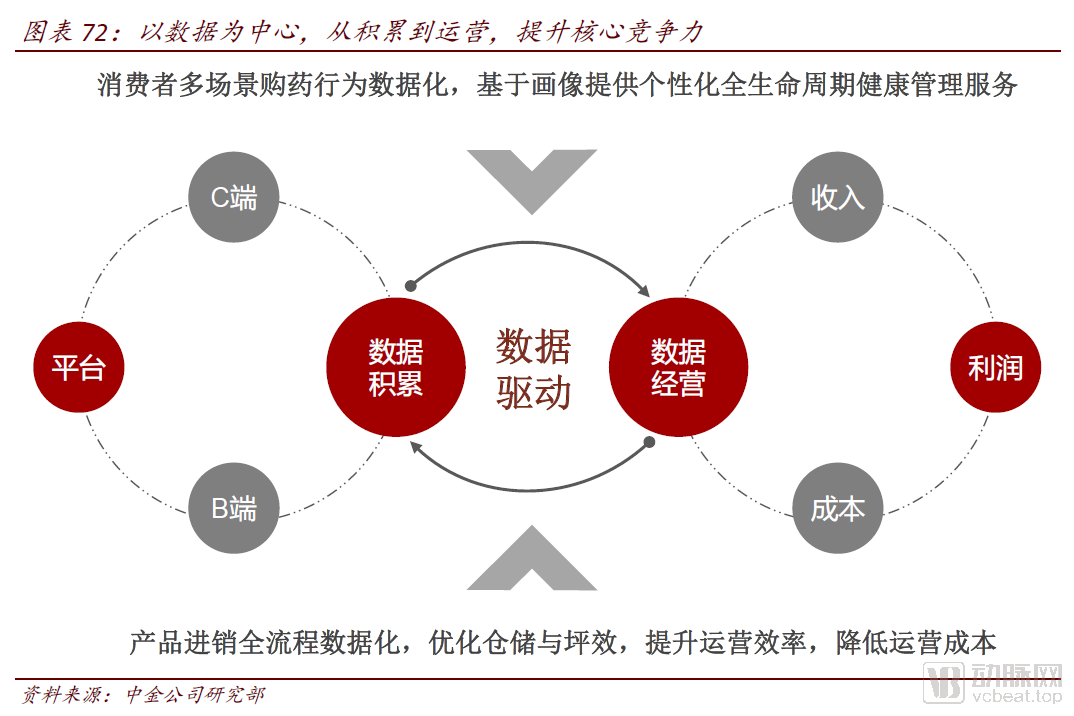

Digital Operations: Integrating “Data Accumulation + Data Operations” to Enhance Core Competitiveness

Acquiring and accumulating consumer-end data is the prerequisite for health management.Consumers are the core element of the pharmaceutical industry. The accumulation of data assets centered on the consumer (C-end) can enhance the granularity of consumer profiling, serving as the foundation for building a “personalized” full-lifecycle health management system. As the layout across all entry points continues to advance, user health data, transaction data, and review data are being retained. We recommend strengthening the construction and operational capabilities of CRM systems, leveraging C-end data profiles to uncover latent demands, continuously iterating and updating the supply of big health products and services, and providing full-lifecycle health management services.

“Data-Driven” Management Decisions Enhance Operational Efficiency.As production, marketing, logistics, and sales become increasingly digitized, we anticipate that enterprises will be able to make dynamic decisions based on real-time feedback data. The subsequent data updates triggered by these decisions are expected to further reinforce a feedback loop, continuously cycling to help companies optimize operational efficiency, reduce costs, and enhance productivity. We recommend integrating internal information systems to achieve seamless interconnectivity of data across all regions, business lines, and entry points, thereby enabling highly coordinated, “data-driven” management decision-making.

Legal Disclaimer

General Disclaimer

This report is solely a summary of previously published reports by China International Capital Corporation Limited (which has obtained approval from the China Securities Regulatory Commission to engage in securities investment consulting business). The information contained herein is derived from publicly available sources that we consider reliable; however, China International Capital Corporation Limited and its affiliates (collectively referred to as “CICC”) make no representations or warranties as to the accuracy or completeness of such information. The information, opinions, and other content set forth in this report are for reference purposes only and do not constitute an offer or solicitation for the purchase or sale of any securities. Such information and opinions do not take into account the specific investment objectives, financial conditions, or particular needs of the recipients of this report and shall not be construed as a personal recommendation to any person at any time. Recipients of this report should independently evaluate the information and opinions contained herein, taking into consideration their own investment objectives, financial conditions, and particular needs, and should consult professional financial advisors regarding legal, commercial, financial, tax, and other matters as necessary. CICC and/or its affiliated personnel shall not bear any legal liability for any consequences arising from reliance on or use of this report.

The opinions, assessments, and forecasts contained in this report represent only the views and judgments as of the date of publication. Such opinions, assessments, and forecasts are subject to change at any time without prior notice. Past performance should not be regarded as an indication or guarantee of future results. CICC may issue research reports with opinions, assessments, and forecasts that are inconsistent with those contained in this report at different times.

This summary of the report may be republished with a delay compared to the formally released version, and may become inaccurate or invalid due to changes in circumstances or other factors after the report’s release date. CICC may issue research reports at different times that contain information, views, or data inconsistent with those presented herein. Sales personnel, traders, and other professionals of CICC may orally or in writing present market commentaries and/or trading views that differ from the opinions and recommendations in this report, based on different assumptions, standards, and analytical methods. CICC assumes no obligation to update inaccurate or outdated information, views, or data, and will not provide separate notice when making changes or updates to such information. CICC makes no express or implied representations or warranties regarding the fairness, accuracy, completeness, reasonableness, or timeliness of the information, views, forecasts, or valuations contained in this report.

This report is provided in Hong Kong by CICC Hong Kong Securities Limited, which is regulated by the Securities and Futures Commission of Hong Kong.

This report is provided in Singapore by China International Capital Corporation (Singapore) Pte. Ltd. (“CICC Singapore”), which is regulated by the Monetary Authority of Singapore, to accredited investors and/or institutional investors as defined under the Securities and Futures Act and the Financial Advisers Act of Singapore. In providing this report to such investors, the relevant financial adviser is exempt from the requirement to make any disclosure under Section 36 of the Financial Advisers Act of Singapore regarding any interest and/or interests in any securities held by it or on its behalf.

This report is provided in the United Kingdom by China International Capital Corporation (UK) Limited (“CICC UK”), which is authorised and regulated by the Financial Conduct Authority. The investments and services to which this report relates are available only to persons who fall within the categories specified in Articles 19(5), 38, 47 and 49 of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005. This report is not intended for retail clients. In other European Economic Area countries, this report is distributed to persons who are classified as professional investors (or equivalent) under their respective national laws.

The contents of this report may be provided in other countries or regions in accordance with the laws, regulations, and regulatory requirements of such countries or regions.

Special Statement

To the extent permitted by law, CICC may hold positions in the securities issued by the companies mentioned in this report and engage in trading activities, and may also provide or seek to provide investment banking services to these companies. Therefore, recipients of this report should take into account potential conflicts of interest that CICC and/or its relevant personnel may have, which could affect the objectivity of the views expressed in this report. This report should not be regarded as a basis for making investment or other decisions.

For disclosures related to the specific companies mentioned in this report, please visit https://research.cicc.com/footer/disclosures, or refer to the recently published specific research reports on these companies.

The copyright of this report is exclusively owned by CICC. Without written permission, no institution or individual may forward, reproduce, copy, publish, distribute, or cite it in any form.