Hillhouse's $17 Billion Healthcare Investment Decoded: Long-Termism Paves an Enduring 'Long Snow Track'

Hillhouse

Long-Term Structural Value Investment Institution

Zhang Lei of Hillhouse has stated that while there may never be a definitive answer to how one identifies exceptional companies, there is one sector Hillhouse will never invest in: areas where its resources and insights cannot create value. Zhang Lei does not believe in zero-sum games; instead, he favors strategies that expand the overall market. Hillhouse seeks out entrepreneurs who aim to achieve great things.

This approach generates substantial impact across any sector. In healthcare, Hillhouse has repeatedly set records for the largest investments in the pharmaceutical industry. With its significant capital commitments and dense portfolio strategy, Hillhouse possesses the power to reshape the industrial landscape.

In the past, mentions of Hillhouse were invariably prefaced by its investments in Tencent and JD.com within the TMT sector; today, however, its prowess in the healthcare sector is equally dazzling.

For a long time, Hillhouse has intensively invested in healthcare companies at various stages, and enterprises backed by Hillhouse, such as MicroPort Medical, Asymchem, Kaili Tai, and BeiGene, have all seen significant surges in their stock prices.

Six years ago, Hillhouse’s first investment in the primary market of the healthcare sector was in BeiGene; since then, Hillhouse has participated in eight consecutive follow-on funding rounds.

Over the past six years, Hillhouse’s interest in the healthcare sector has only grown. To date, Hillhouse has invested in more than 160 companies across biopharmaceuticals, medical devices, healthcare services, and pharmaceutical retail, including over 100 Chinese enterprises. The total investment amount exceeds RMB 120 billion, with the combined market capitalization of its portfolio companies surpassing RMB 2.5 trillion.

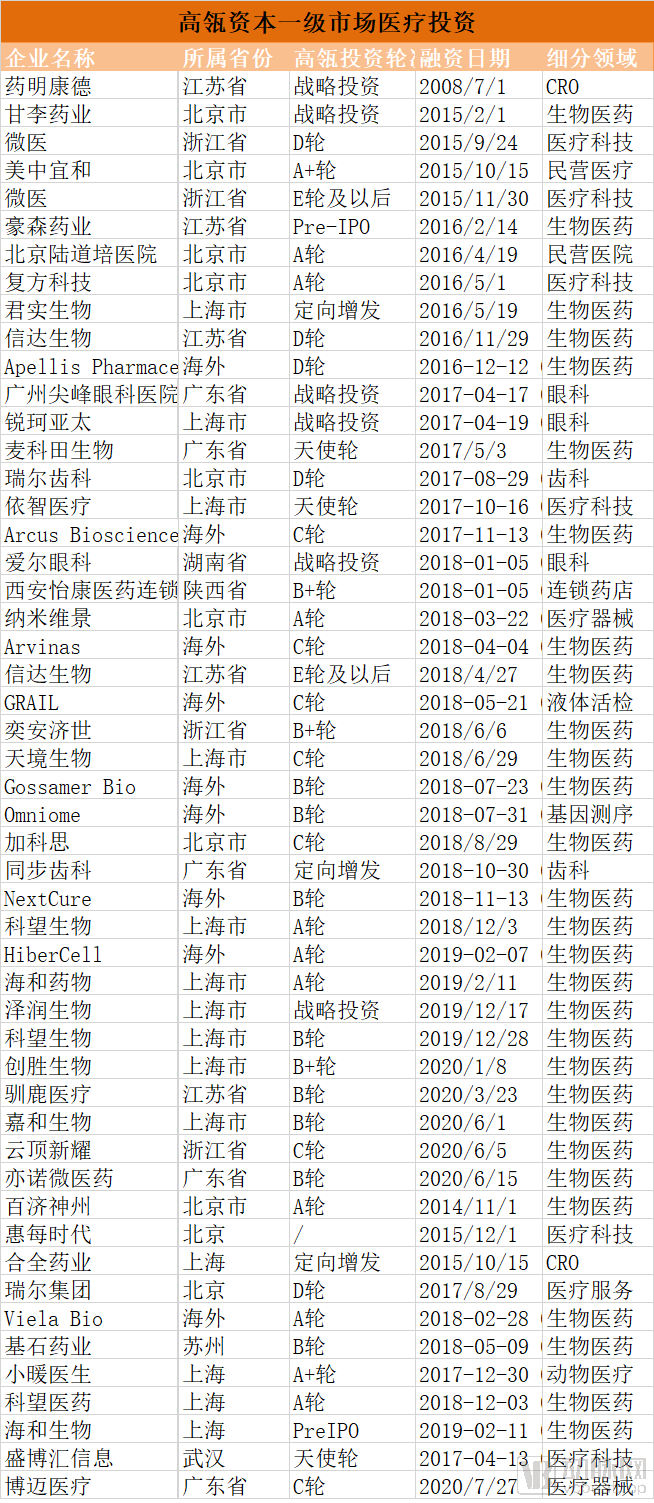

Although bold in its moves, Hillhouse has consistently maintained a low-profile style, rarely disclosing its investment logic and strategic layout in the healthcare sector to the public. Where exactly has Hillhouse’s RMB 120 billion in healthcare investments been allocated? Which 160 companies are included in its portfolio? VCBeat (WeChat ID: vcbeat) collected Hillhouse’s historical primary market investment data from the Artery Orange database and its current secondary market holdings from Choice, identifying over 100 healthcare companies previously invested in by Hillhouse. The article then organizes and analyzes Hillhouse’s investment focus across various healthcare subsectors.

Data sourced from Qichacha & VCBeat Orange Database

(Some of Hillhouse’s portfolio companies have gone public; the data in the table reflects the development stage of each company at the time of Hillhouse’s investment.)

First, let us examine Hillhouse’s investment layout in the primary market. Analysis of the data in the table reveals two most prominent characteristics of Hillhouse’s healthcare investments in the primary market: first, its strong preference for the biopharmaceutical sector, where the number of investments made by Hillhouse far exceeds those in other fields. Judging by subsequent IPO performance, Hillhouse backed multiple companies that went public over a six-year period. Companies in this sector have lived up to Hillhouse’s high expectations; firms invested by Hillhouse in the new drug R&D track—such as Gan & Lee Pharmaceuticals, BeiGene, Innovent Biologics, I-Mab, and WuXi AppTec—have all successfully listed. Gan & Lee Pharmaceuticals, in which Hillhouse invested in 2015, finally listed on the Main Board of the Shanghai Stock Exchange on June 29, 2020. Within just two weeks of its listing, Gan & Lee’s market capitalization surpassed RMB 100 billion.

Second is the comprehensiveness of coverage across sub-sectors. In healthcare, it is difficult to find a sector that Hillhouse has not entered, ranging from medical devices and retail pharmacies to private hospitals. A defining characteristic of Hillhouse is its whole-industry-chain investment approach.

In terms of investment round preferences, Hillhouse has coverage ranging from the angel round to pre-IPO. Hillhouse spans early-stage venture capital, private equity investment, investments in publicly listed companies, and post-listing mergers and acquisitions.

Data sourced from East Money and compiled from public information.

Companies invested in via the primary market are not included in the table.

In the secondary market, Hillhouse’s focus and strategic layout in specific sectors mirror those in the primary market, with a strong bullish stance on biopharmaceuticals.This is primarily attributable to Hillhouse’s strategic choice of long-term investment.. In fact, most of the biopharmaceutical companies in Hillhouse’s portfolio received early-stage investments in the primary market, followed by continuous position increases in the secondary market and long-term support, clearly reflecting Hillhouse’s distinctive approach to full-stage, long-term investment.

Zhang Lei has stated that Hillhouse’s investment approach involves identifying the best business models through research and then seeking out the most suitable entrepreneurs who align with those models. If viable targets can be found in the secondary market, Hillhouse purchases their stocks for long-term holding; if no such companies are available, it turns to the private market; and if suitable opportunities are lacking even there, Hillhouse incubates them itself. This capability is regarded by Hillhouse as essential for long-term investing.

Regarding Hillhouse’s long-termist investment strategy, Yi Nuoqing, Partner and Co-Chief Investment Officer overseeing Hillhouse’s pharmaceutical and healthcare investments, has also stated that in the biopharmaceutical sector, Hillhouse has consistently increased its positions and has hardly ever exited.

Hillhouse Holds Stakes in Leading Companies Across Multiple High-Growth Sectors. When integrating Hillhouse’s investments across both the primary and secondary markets, it becomes evident that Hillhouse has invested in multiple leaders within a given sector. In the CRO sector, WuXi AppTec and Tigermed, the two domestic giants, have both received investment from Hillhouse. In the field of heart valves, Hillhouse has secured positions in the top three players by investing in Venus Medtech, Peijia Medical, and MicroPort Scientific. In the PD-1 sector, Hillhouse has invested inBeiGene, Innovent, Junshibiopharmaceutical companies, etc.

Not every investment institution has the capacity to simultaneously invest in multiple industry leaders. Although leading companies within a given therapeutic area may have overlapping pipelines, they are likely to pursue differentiated development paths in the future, evolving into platform-based enterprises. Furthermore, in the healthcare sector—where mergers and acquisitions are commonplace—there are also opportunities for consolidation among multiple leading firms.

VCBeat will analyze Hillhouse’s investment portfolio across different sectors through data analysis.

Hillhouse has shown a strong preference for the biopharmaceutical sector, both in the secondary and primary markets.

More than a decade ago, Hillhouse already recognized the immense potential of China’s innovative drug sector, believing that China would inevitably give rise to homegrown pharmaceutical companies with independent innovation capabilities.

Zhang Lei once stated that in China’s rapidly changing landscape, one year is equivalent to ten or twenty years in the West. The market indeed evolved as Zhang Lei had predicted: after 2015, a series of policy implementations brought about sweeping changes to China’s pharmaceutical market. Within just a few years, these reforms—spanning drug review and approval policies, national reimbursement drug list (NRDL) access, and capital exit environments—created substantial growth opportunities for innovative drugs. Hillhouse happened to ride this wave at precisely the right time.

In just four to five years, Hillhouse has secured stakes in many of the leading enterprises in China’s innovative drug sector. According to the global Top 50 pharmaceutical companies list compiled by Endpoints News based on market capitalization, six Chinese listed companies made the cut: Hengrui Medicine (ranked 22nd), Hansoh Pharma (29th), WuXi Biologics (33rd), Sino Biopharmaceutical Limited (36th), CSPC Pharmaceutical Group (41st), and BeiGene (47th). Among these, four companies—Hengrui Medicine, Hansoh Pharma, WuXi Biologics, and BeiGene—are either held or have been invested in by Hillhouse.

Based on its investment preferences, Hillhouse’s biopharmaceutical portfolio can be broadly categorized into two areas: first, monoclonal antibody biologics; and second, cancer immunotherapies.

In the field of monoclonal antibody biopharmaceuticals, Hillhouse’s first favored project was BeiGene, which was developing PD-1 inhibitors. In 2013, Zhang Lei personally traveled to Boston to learn about PD-1 therapy. After expressing confidence in BeiGene, Hillhouse also invested in several other biopharmaceutical companies with PD-1 as their core product, including Junshi Biosciences, Innovent Biologics, Genor Biopharma, and CStone Pharmaceuticals, all of which produce PD-1 or PD-L1 monoclonal antibodies.

The leading position of PD-1 stems from its role as a representative of third-generation oncology drugs. Over the past two decades, the application of monoclonal antibody-based large-molecule drugs in cancer and autoimmune diseases has gained momentum worldwide, establishing them as the third generation of anti-tumor and immunological disease therapeutics (with the first generation being chemical drugs and the second generation being small-molecule targeted therapies).

PD-1 inhibitors also hold immense market potential. In 2018, two PD-1 monoclonal antibodies, Keytruda and Opdivo, both ranked among the top 10 drugs globally by sales revenue.

However, PD-1 inhibitors have only partially addressed the challenges in cancer treatment. Hillhouse continues to invest in other monoclonal antibody biopharmaceutical companies, aiming to bet on oncology immunotherapies for the post-PD-1 era. Within Hillhouse’s investment portfolio, companies such as NextCure, Esperance Therapeutics, and HiberCell are all developing monoclonal antibody biologics to benefit patients who do not respond to PD-1 immunotherapy.

Oncology and autoimmune diseases are often the fields where “blockbuster” drugs (those with global sales exceeding $1 billion) emerge. In addition to monoclonal antibody biologics, Hillhouse has also made strategic investments in multiple subsectors of cancer immunotherapy.

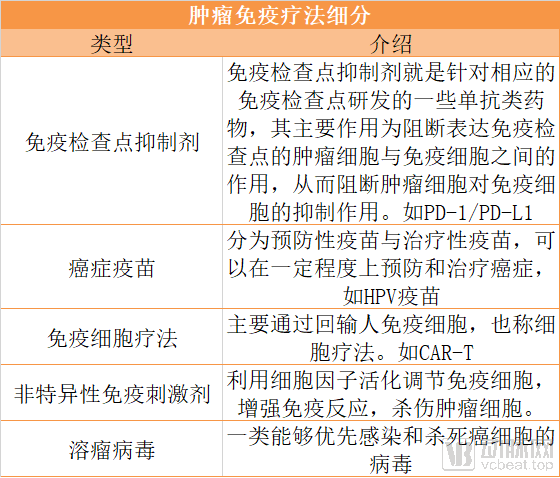

The field of tumor immunotherapy is divided into four major categories: nonspecific immune stimulants, cancer vaccines, immune checkpoint inhibitors, and immune cell therapies. The representative agents of immune checkpoint inhibitors are PD-1/PD-L1 inhibitors; as previously mentioned, Hillhouse has made substantial investments in this area.

Data Source: CNKI

Cancer vaccines can be categorized into preventive and therapeutic vaccines, which can prevent or treat cancer to a certain extent. The HPV vaccine is a representative example. In this niche sector, Hillhouse has invested in Zerun Biologics and Hualan Vaccine. Although Hualan Biological Engineering is not involved in cancer vaccines, Hualan Vaccine is China’s largest production base for influenza vaccines and the first company in China—and the fifth globally—to obtain WHO prequalification for its influenza vaccines. It has garnered significant attention amid the COVID-19 pandemic.

Compiled from public sources

CAR-T therapy is the representative of immune cell therapies. CAR-T, or chimeric antigen receptor T-cell immunotherapy, uses genetic engineering to activate T cells and equip them with a targeting and navigation system known as CAR (chimeric antigen receptor). This transforms ordinary T-cell “warriors” into “super warriors,” namely CAR-T cells. Leveraging their CAR “targeting and navigation system,” these cells specifically recognize tumor cells in the body and release a variety of effector factors through immune responses, thereby efficiently killing tumor cells and achieving the goal of treating malignant tumors. In this field, Hillhouse has invested in Gracell Biotechnologies.

Data sourced from Qichacha and the VCBeat Orange Database, compiled from public information

Medical devices are one of the key sectors targeted by Hillhouse. In particular, Hillhouse’s enthusiasm for the medical device sector has surged in the first half of this year.

In the first half of 2020, Hillhouse increased its stake in MicroPort twice; became a cornerstone investor in Kangji Medical, a company specializing in minimally invasive surgical instruments and accessories; subscribed to HK$640 million worth of shares in Peijia Medical, a prior investment; spent nearly RMB 400 million to participate in the private placement of Kaili Tai; and made a strategic investment of RMB 645 million in Sinocera Material, a company related to dental medical devices.

This series of intensive, high-frequency moves offers a glimpse into how Hillhouse, already a first-tier player in the biopharmaceutical sector, has also secured leading positions with multiple industry giants in the medical device field.

The major segments of the medical device market include in vitro diagnostics, medical imaging, orthopedics, cardiovascular, ophthalmology, and dentistry. Hillhouse has established varying degrees of presence across these segments.

In the field of cardiac interventions, the core products of Peijia Medical, Venus Medtech, and MicroPort CardioFlow—companies invested in by Hillhouse—are all transcatheter aortic valve replacement (TAVR) systems. Although the TAVR market may appear modest in size, it holds the potential to give rise to China’s own Edwards Lifesciences. Edwards Lifesciences is a global leader in heart valve technologies, with annual revenue reaching $4.348 billion and a recent market capitalization exceeding $45 billion.

MicroPort Medical, another cardiovascular-related company heavily invested in by Hillhouse, has three core businesses: coronary stents, orthopedic medical devices, and CRM (cardiac rhythm management). Its domestic market share for cardiac stents in China reaches 23%. MicroPort Medical’s product portfolio is similar to that of Medtronic, giving it the potential to become the “Medtronic of China.”

In the orthopedics sector, Hillhouse has invested in AK Medical, Kaitai Tai, and MicroPort. The orthopedics market comprises four major segments: joints, spine, trauma, and sports medicine, with Hillhouse primarily focusing its investments onJointandSpineTrack.

From a market segmentation perspective, China’s orthopedics market is growing at a rate far exceeding that of the United States. In the trauma segment, import substitution has already been achieved due to relatively lower technical barriers. Meanwhile, joints and spine represent larger and faster-growing subsegments within the orthopedics market, with industry growth rates consistently remaining above 15%.

For companies in the orthopedics sector, China’s orthopedic market is currently experiencing a dual trend of import substitution and rising industry concentration, which will accelerate the market share growth of domestic leading orthopedic implant manufacturers.

In the joint sector, Hillhouse has invested in AK Medical and MicroPort. AK Medical ranks first among domestic manufacturers with a 15% market share in joint implants. MicroPort’s orthopedics business focuses primarily on artificial joints, with its technology and product line derived from the OrthoRecon division of Wright Medical, a U.S.-based orthopedic company acquired in 2014.

In the spine sector, Hillhouse chose Kellytai. As the first domestic enterprise to enter the vertebroplasty market in China, Kellytai leads the industry with the largest market share in minimally invasive spine procedures.

Hillhouse has invested in numerous companies in the therapeutic device sector, but its current footprint in the diagnostics space remains limited.

In the field of medical imaging diagnostics, Hillhouse has invested in NanoVision Imaging in the primary market. Founded in 2014, NanoVision Imaging is a high-tech enterprise dedicated to high-speed, high-precision radiation imaging, with its business primarily covering static CT, X-ray detectors, and X-ray imaging software.

In the in vitro diagnostics sector, Hillhouse has invested in a liquid biopsy company.GRAILand third-party medical testingKingMed Diagnostics.

CROs/CDMOs are an indispensable link in the innovation industry chain for pharmaceuticals and medical devices.

Contract Research Organizations (CROs) are entities or institutions that provide specialized outsourcing services to pharmaceutical companies for drug research and development through contractual agreements. The scope of CRO services is extensive, covering all stages of new drug development, including preclinical CRO services (such as compound research, preclinical studies, safety assessments, and pharmaceutical technologies) and clinical CRO services (such as Phase I to Phase IV clinical trials and drug registration applications).

Hillhouse has invested heavily in numerous innovative drug companies in the biopharmaceutical sector. However, most of these innovators lack fully developed in-house R&D infrastructure, making outsourcing an inevitable choice. As Hillhouse doubles down on China, the rise of the domestic innovative drug industry is inextricably linked to the development of CROs and CDMOs.

Following Hillhouse’s strategy of investing in the top one or two players in an industry, WuXi AppTec and Tigermed are not to be missed. In China, WuXi AppTec and Tigermed are the two leading companies in the CRO sector. WuXi AppTec reported revenue of RMB 12.9 billion in 2019, with a market capitalization reaching RMB 200 billion. WuXi AppTec’s overseas revenue accounts for a significantly higher proportion than its domestic revenue, placing it in a position of absolute leadership in terms of scale. WuXi AppTec is also exploring end-to-end service capabilities across the entire industry chain, from early-stage research to late-stage development and manufacturing.

Zhang Lei once remarked, “Why is there an explosive trend in original innovation within China’s pharmaceutical industry? Because companies like WuXi AppTec exist.”

As a long-term investor and partner, Hillhouse has spared no effort in supporting WuXi AppTec’s development of an integrated R&D service platform from both strategic and operational perspectives. This initiative aims to reduce innovation costs for the growing number of emerging startups, research institutions, and scientists, thereby helping the entire industry shorten the R&D cycles for drugs and medical devices.

TigermedIn 2019, the company’s total operating revenue reached RMB 2.803 billion, representing a year-on-year increase of 21.85%. From 2010 to 2019, the company’s revenue grew from RMB 123 million to RMB 2.803 billion, with a compound annual growth rate (CAGR) of 41.53%, consistently outperforming the growth rate of the CRO industry over the long term. Among the 13 Class 1 new drugs approved in China in 2019, seven were developed with the support of Tigermed or its subsidiaries.

Hillhouse also invested in a subsidiary of Tigermed.PharmaBlock. Pharmaron is a fully integrated contract research organization (CRO) that provides comprehensive product development services to generic and innovative pharmaceutical companies, supporting Investigational New Drug (IND) applications, New Drug Applications (NDA), and Abbreviated New Drug Applications (ANDA). Its service offerings include clinical trial research, biologics, bioanalysis, Chemistry, Manufacturing, and Controls (CMC), and Bioequivalence (BE) studies.

In the first half of this year, Asymchem, in which Hillhouse participated in a private placement, operates in the CMO sector.CMO (Contract Manufacturing Organization), or "Global Biopharmaceutical Contract Manufacturing," primarily accepts commissions from pharmaceutical companies to provide services such as process development, formulation development, clinical trial material supply, production of chemically or biologically synthesized active pharmaceutical ingredients (APIs), intermediate manufacturing, drug product manufacturing (e.g., powders and injections), and packaging.

Asymchem is an industry-leading provider of CMO/CDMO solutions. It is one of the top three companies with the largest domestic market share in the COM sector.WuXi STA, Asymchem, Porton PharmaBoth companies primarily operate in the field of small-molecule chemical drugs and are actively expanding into the biologics sector. The domestic CMO/CDMO industry is highly competitive, with WuXi STA leading at a 6% market share, followed closely by Asymchem with a 4% market share.

In the CMO/CDMO sector, Hillhouse has also invested inWuXi Biologics. WuXi Biologics operates in the field of biologics and is a globally leading “CRO+CMO/CDMO” enterprise. WuXi Biologics is also the only company worldwide offering comprehensive drug substance development services. According to its 2019 annual report, WuXi Biologics reported revenue of RMB 3.984 billion, representing a year-on-year increase of 57.2%.

With the growth of the biologics market and the continuous iteration of products and technologies, large pharmaceutical companies and small to mid-sized biotech firms increasingly require highly specialized biologics research and development service providers such as WuXi Biologics.

Since its inception, Hillhouse has maintained a strategy of making significant investments in China. Amidst the transformative trends in China’s healthcare industry, while the product sector is undergoing import substitution and technological iteration, the healthcare service supply side is also experiencing structural adjustments. In the fields of medical retail and services, Hillhouse has strategically invested in pharmacies and private specialized hospitals.

As early as 2017, Gaoling Healthcare, the healthcare investment and operational platform under Hillhouse, began acquiring and consolidating pharmacy businesses in China. Gaoling Healthcare injected at least $1.5 billion in capital into multiple pharmacy chains, including Chongqing Wanhe, Chengdu Dongsheng, Guangdong Bangjian, Hebei Shicheng Baixing, Sichuan Xinglin, and Xi’an Yikang, rapidly becoming the largest pharmacy chain in China. In October 2019, foreign media reported that Tencent would invest approximately $500 million in Hillhouse’s pharmacy business in China.

From a temporal perspective, 2017 marked the first year in which the separation of prescribing and dispensing and the outflow of prescriptions were truly implemented. The state introduced a series of policies to emphasize and implement specific measures for these reforms. Meanwhile, the outflow of prescriptions will drive structural adjustments in pharmaceutical distribution channels, representing both a reallocation of existing market share and a new growth driver for the market.

In addition to policy adjustments, China’s pharmaceutical retail industry itself has significant room for industrial consolidation. In China, the concentration of the pharmaceutical retail market is far lower than that in the United States, where CVS, a pharmaceutical retail giant, accounts for more than 50% of the retail market sales. In 2019, CVS reported revenue of $256.8 billion.

From the development trajectory of CVS, it is evident that once retail pharmacies reach a certain stage of maturity, they can aggressively integrate the upstream and downstream segments of the pharmaceutical supply chain. Leveraging strong bargaining power, they can reduce healthcare expenditures and expand into businesses such as Pharmacy Benefit Management (PBM) and chronic disease management. In 2018, CVS further expanded its PBM operations by acquiring the insurer Aetna for $69 billion.

Hillhouse’s consolidation efforts in the pharmacy sector target the future market size of consolidated pharmaceutical retail, while also recognizing the potential for integrating the industry chain from the retail end. With Hillhouse’s support, a Chinese counterpart to CVS may well emerge in the future.

Beyond the retail pharmacy end market, another sector in which Hillhouse has made significant investments is private specialized hospitals and research-oriented hospitals. In 2018, Hillhouse invested RMB 1.026 billion to participate in Aier Eye Hospital’s private placement.

Aier Eye Hospital not only operates in a high-growth sector but also stands as the leader in specialized ophthalmic care. By leveraging its early-established strategy of scale and centralization, Aier Eye Hospital has expanded into multiple first-tier cities and taken the lead among other specialized ophthalmic hospitals in completing its layout across second- and third-tier cities, thereby solidifying its position as the industry’s leading player. The revenue structure of Aier Eye Hospital Group has shifted from being primarily driven by its top ten hospitals to achieving profitability across the majority of its hospitals within the group, while significantly shortening the ramp-up period for new facilities.

In the private specialized hospital sector, Hillhouse also invested in Hygeia Medical, China’s largest private oncology healthcare group.

In fact, in addition to the aforementioned specialty leaders, Hillhouse has systematically invested more heavily in the establishment of research-oriented hospitals over the years. Years of research into the innovative drug industry have enabled Hillhouse to recognize earlier that independent research-oriented hospitals have become a critical link in the development of the pharmaceutical innovation industry.

Yi Nuoqing once analyzed in an interview with the media that clinical research is the only method to verify the safety and efficacy of drugs in humans, and it is also the most capital- and time-intensive phase in new drug development. However, the reality is that the number of institutions capable of conducting clinical trials remains limited, plagued by numerous pain points such as insufficient capacity, scarce resources including experts and hospital beds, lack of professionalism, and inadequate attention, leading to an imbalance between the supply and demand of clinical research resources. This was the original intention behind Hillhouse’s strategic investment in research-oriented hospitals.

In March this year, Hillhouse broke ground on the Gaobo Research Hospital in Changping District, Beijing, marking its latest expansion in the research hospital sector following the opening of the Shanghai Artemed Hospital last year.

Having entered the healthcare investment sector over a decade ago, Hillhouse has made life and health investments its area of greatest expertise. After initiating its healthcare investment strategy with PD-1 novel drugs, Hillhouse has deeply cultivated niche sectors including CRO/CDMO, ophthalmology, orthopedics, dentistry, and cardiology. If healthcare investment is akin to a long ski slope, then through sustained commitment and comprehensive value-chain deployment, Hillhouse has worked alongside numerous enterprises to make this slope progressively longer and thicker. VCBeat will continue to track and analyze Hillhouse’s healthcare investment landscape.