Tigermed, a Leading Clinical CRO in China, Surges 19% on Hong Kong Debut

Tigermed

Biopharmaceutical R&D Service Provider

On August 7, 2020, VCBeat learned that Tigermed was listed on the Hong Kong Stock Exchange today, becoming another CRO company listed on both mainland China’s stock exchanges and the Hong Kong Stock Exchange, following WuXi AppTec and Pharmaron.

In this public offering, Tigermed priced its shares at HK$100, at the upper end of the indicative price range. A total of 107 million shares were issued, raising proceeds of HK$10.7 billion.

Tigermed opened today at HK$119, representing a 19% increase over its issue price. As of 9:33 a.m., Tigermed’s share price stood temporarily at HK$115.5, up 15.5% from the issue price.

If WuXi AppTec is the representative enterprise in China’s preclinical CRO sector, then Tigermed is undoubtedly the leader in the clinical CRO field. Some domestic clinical CRO companies that emerged during the same period as Tigermed have fallen significantly behind.

If Tigermed initially gained a head start by leveraging its core competencies, its business logic has undergone significant changes following its expansion and growth. The company is transitioning from providing standalone services to building a comprehensive ecosystem. Therefore, we focus here on its three stages of development to interpret Tigermed’s dual identity as both an industrial operator and a capital investor.

Tigermed, established in December 2004, is currently the largest clinical CRO company in China. Its predecessor was Tigermed Consulting, founded by Ms. Cao Xiaochun and Dr. Ye Xiaoping in 2002. According to the prospectus, Dr. Ye and Ms. Cao, the two founders, remain the largest shareholders of Tigermed (excluding HKSCC Nominees Limited).

Tigermed's Core Business

Honghui Capital, a well-known domestic healthcare investment institution, participated in the anchor investment for Tigermed’s listing on the Hong Kong Stock Exchange. Ms. Jiang Yanye, spokesperson for Honghui Capital, stated to VCBeat: “Honghui Capital remains bullish on China’s CRO sector. As a leading clinical CRO in China, Tigermed will help complete Honghui’s portfolio in the CRO field. Furthermore, Tigermed will achieve greater business synergy with innovative companies invested by Honghui, creating a win-win situation for all parties.”

In fact, when Tigermed was listed on the ChiNext board, some institutions had already reaped substantial rewards from their investments in the company.

When Tigermed was founded, the clinical CRO industry was still a blue ocean. Leveraging the strong capabilities of its founding team, the newly established Tigermed quickly secured a leading position in China’s clinical trial sector. Its rapid growth soon attracted capital market attention. Qiming Venture Partners invested a total of $7 million in Tigermed in two rounds, in June 2008 and March 2010, becoming the sole institutional investor prior to Tigermed’s listing on the ChiNext board. On August 17, 2012, Tigermed officially listed on the ChiNext board at an issue price of RMB 37.88 per share. The stock closed at RMB 50 on its first day of trading, representing a 32% increase, with a market capitalization approaching RMB 2.7 billion. Based on the first-day closing price, Qiming Venture Partners achieved an eight-fold return on its paper exit.

As of December 31, 2019, Tigermed’s clinical professional team comprised nearly 2,500 members, including 840 clinical research associates (CRAs), 1,490 clinical research coordinators (CRCs), and 100 patient recruitment specialists. More than 80% of the over 500 Good Clinical Practice (GCP)-registered clinical trial institutions in China have established collaborative partnerships with Tigermed.

Looking back on Tigermed’s 16-year development journey, its business has long been centered around clinical CRO services. Tigermed’s leading position in the clinical CRO industry is reflected not only in its team size and network of partner institutions, but also in other key metrics such as annual revenue and the number of ongoing clinical trials.

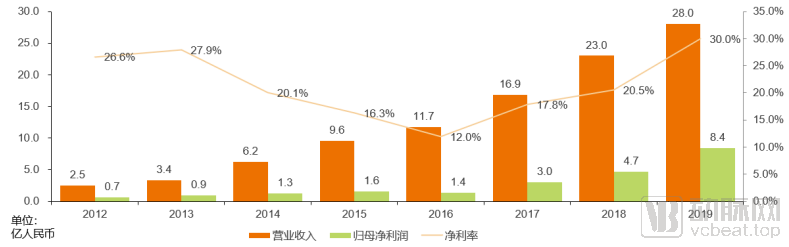

Tigermed's Annual Revenue Trends

Although Tigermed is already a large-scale enterprise with a mature business system and stable revenue, it has maintained rapid growth over the past eight years since its listing on the ChiNext board in 2012. Its revenue increased from RMB 250 million in 2012 to RMB 2.8 billion in 2019, representing an 11-fold increase and a compound annual growth rate (CAGR) of over 40%. This rapid growth has also driven strong profitability. From 2012 to 2019, Tigermed’s net profit attributable to shareholders of the parent company grew in tandem with its operating revenue, reaching a peak net profit margin of 30% in 2019.

According to a report by Frost & Sullivan, Tigermed was the largest clinical contract research organization in China in 2019, with a market share of 8.4%, based on its 2019 revenue and the number of ongoing clinical trials as of the end of 2019.

Tigermed’s ability to achieve sustained high-speed growth hinges on three key factors. First, the continuous deregulation of domestic policies has raised the ceiling for the overall clinical CRO industry in China. Second, the company has a clear strategic focus, prioritizing the consolidation of its foundational capabilities before pursuing globalization. Third, it leverages its capital strength to continuously increase investment in related industries, building a comprehensive pharmaceutical R&D ecosystem through mergers and acquisitions.

As an industry leader, market size is one of the key factors that may constrain Tigermed’s future development.

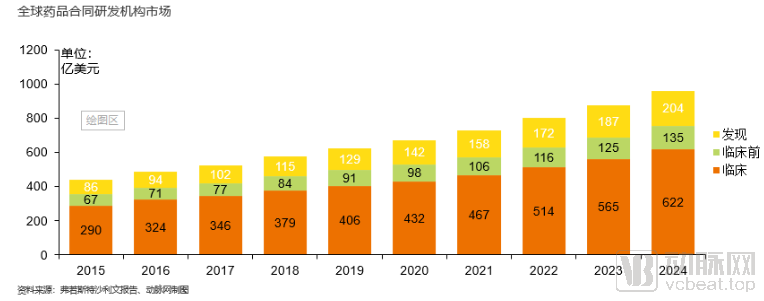

Global CRO Market Size

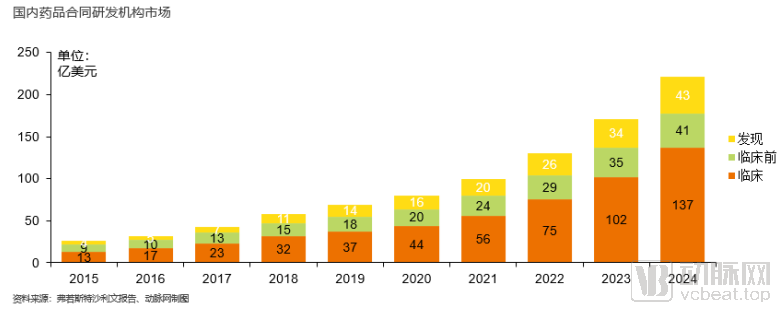

Domestic CRO Market Size

According to relevant reports by Frost & Sullivan, the global contract research organization (CRO) market has maintained steady growth, with the clinical CRO segment accounting for approximately two-thirds of the overall market. In contrast, China’s CRO market is experiencing rapid expansion and is projected to grow exponentially over the next five years. Notably, the clinical CRO segment is expected to further increase its share of the total market, reaching a scale of tens of billions of U.S. dollars by 2023.

In recent years, policy support has significantly boosted the R&D outsourcing industry, particularly the clinical CRO sector. First, domestic policies encouraging the development of innovative drugs have generated a large volume of new drug clinical trials. Second, the demand arising from the ongoing consistency evaluation of generic drugs over the past two years has also been absorbed by clinical CROs. Third, as China’s clinical trial practices have aligned with international standards, a substantial number of international multi-center clinical trials have established sites in the country.

Driven by multi-faceted policy initiatives, both the market potential and size of China’s clinical CRO industry have seen significant expansion. Moreover, R&D expenditures associated with clinical trials are substantially higher than those for drug discovery and preclinical stages. Given that drugs entering clinical trials have already undergone rigorous screening and meticulous design, pharmaceutical companies are willing to incur higher costs in this phase to secure superior clinical trial management.

Jiang Yanye also expressed a similar view: “From the broader perspective, the government encourages innovation. An increasing number of enterprises are prioritizing R&D and continuously ramping up their R&D investments. Moreover, the future trend of the CRO industry will inevitably see rising market concentration driven by integration across the upstream and downstream segments of the industrial chain and intensified horizontal M&A activities. As an industry leader, Tigermed has accumulated substantial successful M&A experience and is well-positioned to further expand its market share and solidify its leading status through future acquisitions.”

Therefore, we generally believe that from the perspectives of policy and industry development, the clinical CRO sector in which Tigermed operates is currently in a phase of rapid growth. As a leading enterprise in China, Tigermed is poised to accelerate its development amidst this trend.

Tigermed has evolved from its origins as a domestic clinical CRO into a global service provider covering the entire new drug R&D lifecycle. In terms of the R&D process, its services have extended downstream to post-marketing studies and upstream to preclinical pharmacokinetics, pharmacodynamics, bioanalysis, and CMC. Meanwhile, in its globalization strategy, Tigermed has expanded its service scope from China to the global market.

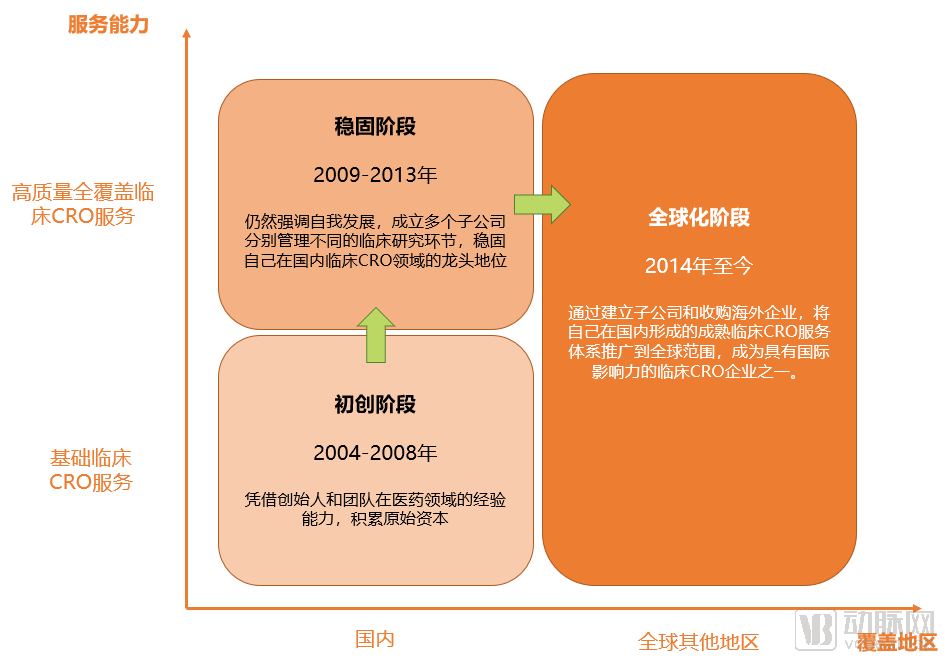

The Three Major Development Stages of Tigermed

Based on Tigermed's development history, we primarily divide its growth into three stages: the startup stage, the consolidation stage, and the globalization stage.

Tigermed’s Milestones in Acquisitions and Subsidiary Development

From Tigermed’s establishment in 2004 to 2009, it was Tigermed’sStart-up Phase. During this phase, Tigermed was in its earliest stage of development. Leveraging the founders’ and team’s expertise and experience in the pharmaceutical industry, the company provided clinical CRO services to clients, thereby accumulating its initial capital and laying a solid foundation for its future growth.

Subsequently, Tigermed, having gradually achieved scale, began to expand the scope of its services.

2009–2013 was a period of development for TigermedConsolidation Phase. During this phase, Tigermed continued to emphasize organic growth, primarily focusing on segmenting its clinical CRO operations by establishing multiple subsidiaries to separately manage different stages of clinical research. At this stage, Tigermed had also begun to selectively engage in investments and mergers and acquisitions to strengthen its capabilities, such as its 2009 acquisition of Medidata to enhance its data management and statistical analysis services.

During this period, Tigermed also accomplished a key milestone in its development. On August 17, 2012, Tigermed was listed on the ChiNext Board of the Shenzhen Stock Exchange, raising over RMB 500 million in total. According to its prospectus that year, the proceeds were primarily intended for the establishment of an integrated clinical trial management platform, a data management center, and an SMO (Site Management Organization) management center. This further corroborates Tigermed’s strategic logic at this stage: first consolidate its competitive advantages and establish a firm foothold in China’s clinical CRO sector, then seize opportunities for further expansion as they arise.

Thus, Tigermed spent five years further consolidating its accumulated advantages in clinical research, firmly establishing its leading position in China’s clinical CRO sector, and then launched a new globalization strategy at the end of 2013.

In November 2013, the establishment of Tigermed Australia Pty Limited, an Australian subsidiary of Tigermed, marked the launch of Tigermed’s global strategy, representing a new phase in the company’s development.Globalization Stage。

From 2014 to 2015, Tigermed made concentrated breakthroughs in its strategic layout across the Americas and other parts of Asia. The landmark events during this period were the acquisition of U.S.-based Frontage Labs in 2014 and the acquisition of DreamCIS, a South Korean clinical CRO company, in 2015. These two acquisitions served as key gateways for Tigermed to expand its operations in the United States and South Korea. Subsequently, from 2018 to 2019, Tigermed further strengthened its presence in the Japanese and European markets. By the time of this listing, the company had achieved comprehensive coverage of major global pharmaceutical markets.

It was also from the globalization stage that Tigermed adopted a more open attitude toward business expansion, more frequently deploying in related fields through acquisitions, collaborations, and investments—a point we will analyze in detail later.

The development across these three stages has laid the foundation for Tigermed’s success and reflects its steady and pragmatic approach.

Benefiting from its continuous deepening expertise in the field of clinical research, Tigermed has accumulated a large base of loyal clients, which has grown year by year. From 2017 to 2019, Tigermed’s client base expanded from 1,570 to 1,898. In 2019, all of the top ten pharmaceutical companies globally by total revenue and the top ten pharmaceutical companies in China by total revenue established cooperative relationships with Tigermed. Meanwhile, the retention rate of Tigermed’s top ten clients during the reporting period reached 100%. Among the top ten clients in 2019, Tigermed provided services to most of them for more than five years, covering multiple service categories.

Long-term customer service has also brought valuable orders to Tigermed. The future service revenue from contracts already signed by Tigermed amounts to RMB 5.3 billion. Based on Tigermed’s 2019 annual revenue of RMB 2.8 billion, the total value of its pending orders reaches approximately 1.9 times its annual revenue. In other words, Tigermed has essentially secured its order backlog for the next two years.

Tigermed’s subsidiaries have now begun to adopt Tigermed’s development strategy.Based on the acquired Frontage Labs, Tigermed established the holding company Fangda Holdings, which was listed on the Hong Kong Stock Exchange on May 31, 2019. In 2019, Fangda Holdings’ revenue exceeded US$100 million, and its net profit margin increased from approximately 14% to 18.4%. The U.S. business accounted for more than half of the total, the China business for about one-third, and the remainder comprised global operations.

As the holding company of Tigermed, Frontage Holdings’ development strategy is fully aligned with that of Tigermed. In 2019, Frontage Holdings invested in expanding its laboratory infrastructure and staffing to strengthen its operational capabilities, while also acquiring RMI and BRI sequentially to continuously enhance its service capacity and business expansion capabilities in the United States.

As Tigermed advances its globalization strategy, the company, backed by substantial capital reserves, has also begun to actively engage in partnerships, mergers and acquisitions, and investments from a strategic investor perspective.

The acquisition of MSTA in 2009 marked Tigermed’s first move in investment and acquisitions. Subsequently, as part of Tigermed’s global expansion, local teams in Europe, the United States, and South Korea were all established through acquisitions.

In addition to mergers and acquisitions, Tigermed has frequently appeared as a primary market investor since 2017. Its external investments include direct investments in startups by the company itself, outward investments made by its subsidiary investment firms, and capital provision to other investment institutions in its capacity as a limited partner (LP).

In summary, Tigermed’s outbound investments have already begun to generate substantial returns. These returns stem from three distinct sources: First, investments in companies within the contract research organization (CRO) and related sectors help Tigermed acquire new clients and strengthen its ecosystem, thereby enhancing stickiness among existing clients. Second, invested innovative drug developers are poised to become Tigermed’s future clients, delivering direct revenue. Third, Tigermed’s equity stakes in these portfolio companies will yield significant financial gains upon their eventual initial public offerings (IPOs).

Investment Events Disclosed by Tigermed Through Public Channels

Based on Tigermed’s publicly disclosed investment activities to date, its investment strategy is entirely concentrated within its areas of expertise. The target companies fall primarily into two categories: the first comprises enterprises directly related to its core business, such as preclinical CROs and CDMOs; the second consists of innovative drug developers.

Investment in Relevant Enterprises, Tigermed is primarily focused on enhancing its ecosystem in contract research outsourcing. These companies may operate at different stages of the new drug development process relative to Tigermed, creating synergies and complementing each other while sharing clients.

Although Tigermed itself still has gaps in the full-process management of pharmaceutical R&D, by building such an ecosystem, it can also provide pharmaceutical companies with a complete one-stop service for drug research and development. Therefore, the key role of this type of investment is to acquire new customers and enhance customer stickiness.

Strategic Layout of Innovative Drug CompaniesTigermed also places significant emphasis on this area, which has even become one of its growth strategies. In the growth strategy outlined in Tigermed’s Hong Kong stock listing prospectus, it is explicitly stated that the company “will continue to invest in and incubate promising early-stage biotechnology and medical device companies to drive their development, thereby acquiring potential clients and business opportunities.”

This means that Tigermed’s investments in innovative drug companies are driven, on one hand, by its professional expertise and precise identification of high-value investment targets; on the other hand, as these companies advance to the clinical stage, they are likely to become Tigermed’s clients, directly driving business growth for the company.

So, how has Tigermed performed in its capacity as a capital entity?

According to the 2019 annual report, Tigermed’s revenue reached RMB 2.8 billion, with net profit attributable to shareholders of the parent company amounting to RMB 840 million. Of this, net profit after deducting non-recurring gains and losses was only approximately RMB 560 million. In other words, the portion of non-operating income attributable to the parent company amounted to approximately RMB 280 million, accounting for more than 30% of the net profit attributable to shareholders of the parent company.

Specifically, the various financial assets held by Tigermed generated a total revenue of RMB 278 million for the company in 2019, among which gains from changes in fair value amounted to RMB 185 million. These gains primarily stemmed from the increase in valuation of enterprises invested in by Tigermed, resulting in corresponding changes in value.

Successful enterprises always share certain common traits. We have previously provided an in-depth analysis of WuXi AppTec, another leading domestic CRO company. These two companies exhibit many shared decision-making characteristics throughout their development histories. For instance, during the mid-stage of their growth, they avoided aggressive expansion and instead dedicated several years to solidifying their core businesses. Additionally, in recent years, both have continuously increased their investments in the healthcare industry through capital deployment.

Use of Proceeds Disclosed in Tigermed’s Hong Kong IPO Prospectus

From the use of proceeds from Tigermed’s IPO, we can also see that in the coming years, Tigermed will continue to adhere to its Phase III strategy, further strengthening its overseas service capabilities and outward investment.

Although the short-term strategic plan is already clear, how will Tigermed continue to move forward after completing its global layout and ecosystem construction? The story of Tigermed is far from over.