Teladoc and Livongo Merge to Form $38 Billion Virtual Care Leader

On the evening of August 5, news of a corporate merger went viral in the healthcare community: Teladoc and Livongo, two giants in the U.S. digital health sector, announced their merger.

This is an unprecedented event in the history of digital health, which will have a significant impact on the industry.

Under the terms of the transaction, each share of Livongo held by its shareholders will receive 0.592 shares of Teladoc and $11.33 in cash, valuing Livongo at $18.5 billion.According to estimates by financial services firm Piper Sandler, the merged entity could be valued at $38 billion, equivalent to approximately RMB 270 billion.

Teladoc, founded in 2002 and publicly listed via an IPO in 2015, established a telemedicine technology platform that enables patients to consult remotely with physicians enrolled on the platform via video. Livongo, founded in 2008 and publicly listed via an IPO in 2019, primarily leverages digital technologies and smart devices to help patients with chronic diseases (mainly diabetes) manage their conditions.

In the newly merged company, Teladoc shareholders and Livongo shareholders will hold 58% and 42% of the shares, respectively. Jason Gorevic, the current CEO of Teladoc, will serve as the CEO of the combined company. Under the leadership of Teladoc Chairman David Snow, the board of directors of the newly merged Teladoc will consist of eight members from the Teladoc committee and five members from the Livongo committee.

How Were Teladoc and Livongo Built, and What Solutions Did They Deliver? What New Possibilities and Myths Will Their Merger Bring to the Industry?

Next, this article will answer your questions one by one.

Looking back at Teladoc’s 18-year development journey, the first major milestone dates back to 2005.

That year, the company launched “TelaDoc Medical Services,” a telephonic medical consultation program. This service primarily aims to provide convenient and affordable healthcare solutions for corporate employees. For just $35 per consultation, members can speak with qualified physicians via phone, a significantly more cost-effective option than visiting an emergency room or hospital outpatient clinic. From its inception, the program has supported payments through Health Savings Accounts (HSAs). Members can complete CMS-1500 claim forms to facilitate insurance reimbursement and tax deduction applications. Upon registration, TelaDoc’s system establishes individual accounts and electronic medical records, enabling physicians to review patients’ chronic medical histories, current medication lists, drug allergies, and other relevant health information prior to future consultations.

After several years of technological evolution, Teladoc’s telemedicine business reached a significant inflection point in 2011, with its growth curve rising sharply. In addition to phone consultations, the company launched web-based online video consultations, accelerating physician response times and reducing average user wait times to 22 minutes, at a price of $38 per consultation.

Thereafter,Teladoc has consistently focused on innovatively addressing core issues such as access to healthcare services, cost, and quality, expanding its service population to include health insurance companies, corporate employers, labor unions, associations, and the general public.Technologically, in addition to leveraging multiple channels such as telephone, online video, and health kiosks to deliver medical services, Teladoc developed separate mobile applications for physicians and members following the advent of the mobile internet era, named “Teladoc Physician” and “Teladoc Member,” respectively.

(The image shows a screenshot of the early interface of the Teladoc user-side app)

In 2015, when mobile health startups in China were booming, Teladoc successfully completed its initial public offering (IPO) in June of the same year.According to the prospectus, the company had more than 300 employees, over 1,100 physicians, 4,000-plus clients, and nearly 11 million members at that time. Revenue was also substantial, with Teladoc reporting turnover of $20 million in 2013 and $44 million in 2014.

In the years following its IPO, Teladoc achieved exponential growth through a combination of rapid expansion in its core business and aggressive investment, acquisition, and M&A activities within the industry. This trajectory ultimately established Teladoc as a leading enterprise in digital health, creating a valuation myth worth tens of billions of U.S. dollars.

For example, earlier this year, prior to the acquisition of Livongo, Teladoc acquired InTouch Health for $600 million in January. InTouch Health is a leader in acute care telemedicine solutions, partnering with more than 450 hospitals and healthcare systems worldwide and serving over 14,500 physician users. Furthermore, InTouch Health supports more than 130 health systems and 2,135 care sites, covers over 40 clinical use cases, and has been ranked by KLAS Research as the world’s leading virtual care platform for two consecutive years.

(Teladoc's Recent Investment and Acquisition Activities)

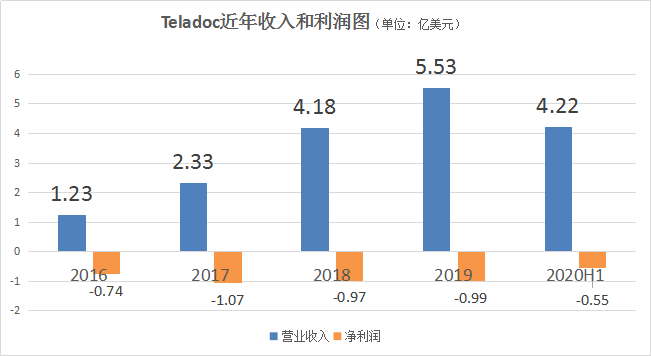

In its core business, Teladoc has seen significant revenue growth in recent years.

In 2015, Teladoc’s revenue stood at only $77 million, rising to $553 million by 2019. In 2020, buoyed by the positive impact of the pandemic, Teladoc reported second-quarter revenue of $241 million, a year-on-year increase of 85.01%.

Livongo was founded to address a glaring pain point in the U.S. healthcare system.

In the U.S. health insurance system, employers purchase commercial insurance for their employees, typically covering 80% of the premium costs. The exact proportion depends on the company’s benefits structure. From the insurer’s perspective, it is always preferable to minimize medical expenditures among corporate employees. Compared with healthy employees, those with chronic conditions represent the largest share of insurers’ payouts. Insurers not only bear the costs of ongoing treatment but also face significantly higher expenses from hospitalizations if these conditions are poorly managed—all of which are covered by the insurer. Therefore, insurers cannot afford to neglect the management of employees with chronic diseases.

To address this, Livongo provides viable solutions to help insurers control expenditures on chronic disease management. Insurers and employers (the policy purchasers) share aligned interests; when insurers are confident that costs are reduced and controllable, they will inevitably pass on a portion of the savings to employers in some form. Furthermore, improved employee health helps employers reduce absenteeism and other productivity losses. Therefore, when Livongo demonstrates its return on investment with compelling evidence, both insurers and employers become willing to recommend its services to employees.

Livongo’s solution is a combination of hardware, software, and human services, encompassing connected devices, system feedback, and personalized coaching. It has currently launched four solutions: Livongo for Diabetes, Livongo for Hypertension, Livongo for Prediabetes and Weight Management, and Livongo for Behavioral Health by myStrength.Among these, the diabetes business accounts for nearly 90% of total revenue.

Among the evaluation metrics for solutions, Livongo effectively addresses three key concerns of payers: “user satisfaction, clinical outcomes, and economic costs.”

Thus, Livongo established a B2B2C business model: its clients are enterprises that purchase health insurance for their employees; insurers and Pharmacy Benefit Managers (PBMs) serve as channel partners that facilitate client referrals; and the ultimate beneficiaries of Livongo’s innovative services are the employees of these enterprises.

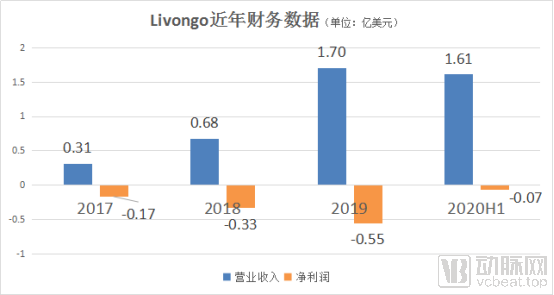

Over the past three years, Livongo has also achieved significant business growth.

As shown in the chart, Livongo’s revenue has been rising steadily, doubling each year. According to the latest second-quarter earnings report released on August 5, Livongo generated $161 million in revenue in the first half of 2020, nearly matching its full-year total for 2019. Losses also narrowed further, with the combined net loss for the two quarters of 2020 amounting to only $7 million.

To date, Teladoc supports 40 languages across more than 175 countries and regions, maintains leadership in 100 virtual care clinical practice guidelines, and has expanded its clinical depth and breadth across over 450 medical specialties, thereby continuing to dominate the public telehealth sector.Livongo, with 328,000 members and 500 million data points on its platform, is considered the market leader among companies providing remote monitoring solutions distributed through employers and payers.As telemedicine has experienced explosive growth over the past few months, the stock prices of Teladoc and Livongo have repeatedly hit record highs.

Supported by advancements in hardware and software technologies for telemedicine and remote patient monitoring, both companies are poised to continue growing and strengthening along their respective paths.

Yet the two companies suddenly announced their merger, catching the market off guard and sparking immense excitement. In U.S. media coverage, executives, investors, analysts, and other stakeholders associated with the two firms offered extensive commentary on the development.

“Livongo CEO Zane Burke stated that this strategic decision will expand Livongo’s solutions into the care domain, ultimately making patients the winners of this merger. ‘By creating unique, consumer-centric virtual care, we have gained the ability to integrate health and care. From the outset, our mission has been to empower people with chronic conditions to live their best and healthiest lives. We recognize that our members will interact with their physicians on many occasions. Livongo’s mandate has always been to meet members where they are and understand their lives,’ said Burke.”

Both parties believe that the opportunity is equally synergistic for Teladoc. “If we can leverage Livongo’s technology to better recruit and engage our existing users, we will be able to outperform competitors lacking such capabilities. Likewise, if Livongo is optimized to deliver favorable therapeutic outcomes for patients, they can also benefit from our established medical practices,” said David Sides, Chief Operating Officer of Teladoc Health.

Burke and Sides believe that the merged entity of Livongo and Teladoc will be able to more comprehensively address patients’ full spectrum of healthcare needs within a single consumer-facing experience. “Livongo offers many advantages, such as consumer experience, artificial intelligence, data science, and other one-to-many scalable solutions, while Teladoc excels in creating unique one-on-one interactive experiences,” said Burke.

There are numerous examples illustrating how Teladoc’s one-on-one solutions benefit Livongo’s one-to-many approach. If a Livongo patient has not yet reduced their hemoglobin A1c to the target level, they can schedule a same-day appointment with an endocrinologist via Teladoc to determine how to optimize their medication regimen. “When Livongo and Teladoc are integrated, you can accomplish certain powerful tasks more rapidly, whereas these initiatives might progress more slowly if the two companies were merely partners,” said Sides.

Furthermore, significant cross-selling opportunities exist between the two companies. Although both Teladoc and Livongo are leaders in the digital health market, their commercial overlap among health plans, employers, and partners is less than 25%. Livongo serves 30% of Fortune 500 companies, while Teladoc serves 40%; thus, the merged entity, “Telavongo,” demonstrates substantial revenue growth potential. “When you look at our momentum and the synergistic opportunities that will be unlocked by merging with Teladoc, this merger becomes undeniable,” said Burke. “To realize revenue synergies, we will begin cross-selling to our existing customers as early as next week,” said Sides.

Given Livongo’s limited business presence outside the United States, while Teladoc has established a business network in more than 175 countries and regions, this merger creates a rare opportunity for Livongo to accelerate the overseas expansion of its chronic disease management system. “In our conversations with national leaders around the world, we found that the concept of digital chronic disease management is virtually nonexistent outside the United States. Moving forward, wherever there are ties to health plans and healthcare systems, we can leverage Teladoc’s international business network to grow Livongo’s operations.”

Many healthcare technology leaders also see synergistic opportunities in the merger of Livongo and Teladoc. John Halamka, President of the Mayo Clinic Platform at Harvard University, stated that the merger between Teladoc (which acquired InTouch) and Livongo addresses too many issues.

“I firmly believe that digital health will be an ecosystem composed of many companies, including device/sensor manufacturers, interoperable platforms, AI/ML companies, and cloud service providers. Although Livongo/Teladoc has become an important part of the digital health industry, they will still need the support of many other companies in the ecosystem,” said Halanka.

As venture capital investment in the digital health industry reaches historic highs, reactions to this consolidation within the sector have been mixed. For the venture capital community, this merger serves as further validation of the entire digital health market, which has grown from $300 million in venture funding in 2009 to $5.4 billion in the first half of 2020.

Previously, the industry remained skeptical of digital health due to a lack of digital medical services; however, over the past 14 months, nine IPOs have emerged, with most performing well in the public markets. Overall, there is a surging understanding and appreciation in the public markets for the power of digital health to transform healthcare. Although these developments occurred prior to the pandemic, it is evident that the pandemic has significantly accelerated the industry’s growth.Prior to the pandemic, the combined market capitalization of Livongo and Teladoc stood at $8 billion; today, it has surged to $38 billion.

Regarding how this merger will impact early-stage investment in the sector, it is certain that more capital will be directed toward and invested in digital health, with increased funding flowing into the industry. This merger may prompt more growth-stage digital health companies to go public or secure substantial financing within the next two years. Furthermore, other competitors in the industry, such as Optum, will undoubtedly vie for other targets in the sector, moving quickly to acquire them.

Overall, this merger came as a surprise to many early investors. Some believed that by leveraging the “digital hospital” narrative, the merged entity could become a company valued at $100 billion. Yet, from one perspective, the digital health industry is only just getting started.

Moreover, the market did not fully endorse the merger. On the day Teladoc and Livongo announced their merger, both companies’ stocks fell sharply. By the close of trading, Teladoc’s shares had dropped 19%, while Livongo’s had declined 11.4%. Some Teladoc shareholders believed that Teladoc had overpaid for Livongo and that Livongo’s business was not entirely synergistic with Teladoc’s core telehealth operations. For instance, just a few days earlier, Siemens acquired Varian (Varian ), as the global leader in oncology radiotherapy, has installed more than 8,000 radiotherapy systems worldwide, capturing over 50% of the global radiotherapy market share.Siemens’ acquisition price was only $16.4 billion.

Has Livongo’s value truly surpassed that of Varian?

This is the key issue that has sparked controversy in this merger and acquisition event.

However, for early-stage digital health companies in the industry, this merger is both a blessing and a curse. The merged entity is a strong potential acquirer for many early-stage digital health companies, but new market entrants will also have to answer the question, “Why couldn’t Livongo and Teladoc do this themselves?”

Following the merger, the combined entity possesses sufficient capital to explore other strategic options. Consequently, in the future, the new entity can acquire solutions for various chronic diseases through mergers and acquisitions.

“We can certainly gain additional capabilities through Livongo that complement our existing work, and I believe this will help us build out more features,” said Sides. One example is the InTouch Health network, which offers an integrated suite of technologies, software, and specialized devices. Through Livongo, Teladoc will be able to add more solutions to better facilitate the transition from hospital to home care, while allowing providers to practice within their scope. This will help reduce overall care costs while increasing the number of patients who can be treated.

According to Teladoc’s CEO, “If we are to rapidly secure more user-beneficial solutions, we will pursue additional acquisitions in the future.”

References:

1.Forbes,《Say Hello To The Largest Virtual Care Company: Telavongo, The $38 Billion Merger Between Teladoc And Livongo》.

2.The Motley Fool,《Why Teladoc and Livongo Stocks Plunged Today?》.