Public Hospitals Tighten Belts Amid 'Year of Economic Management': Non-Core Service Outsourcing Emerges as a Strategic Solution

Under the Background of the New Healthcare Reform, Public Hospital Reform Is Steadily Advancing; Reform Measures Such as the Abolition of Drug Price Markups and the Separation of Medical Services from Pharmaceutical Sales Have Imposed New Requirements on Hospital Operational Capabilities.

Recently, according to the official website of the National Health Commission, ““Public Healthcare Institutions Economic Management Year” will be launched in July 2020, lasting for one year and concluding in June 2021. The initiative aims to better meet the growing demand for medical services among the public and drive public healthcare institutions to accelerate efforts in addressing weaknesses and shortcomings in internal management.

The campaign requires public hospitals (including general hospitals, traditional Chinese medicine hospitals, specialized hospitals, maternal and child health care hospitals, etc.) and primary healthcare institutions (including community health service centers and stations, township health centers, etc.) operated by health administrative departments and traditional Chinese medicine authorities at all levels across China to systematically review prominent issues in economic management and economic conduct identified through prior external regulatory activities such as audits, inspections, and checks, as well as weaknesses and shortcomings in economic management uncovered during internal operational management, and to ensure timely and effective implementation of corrective measures.

“Comprehensive budget management has been advocated for many years, but it has not been effectively implemented. The current low operational efficiency of public hospitals is mainly due to the lack of effective tools in economic operation management,” pointed out Liang Wannian, Director of the Department of Structural Reform at the National Health Commission, at the 8th China County and City Hospital Cloud Forum recently.

2020 was an exceptionally unusual year. Amid the COVID-19 pandemic, the economy faced significant pressure, and industries across the board struggled to operate. According to data released by the National Bureau of Statistics Information Center, the total number of outpatient and emergency visits at medical and health institutions nationwide reached 2.03 billion in January–April 2020, a year-on-year decrease of 26.1%. Of these, public hospitals accounted for 740 million visits, representing a year-on-year decline of 27.1%.

On June 11, the 2020 departmental budget released by the National Health Commission showed that the general public budget allocation for the year amounted to RMB 1,731.98804 million, a decrease of RMB 581.25793 million compared with the actual expenditure in 2019. Notably, the budget for public hospitals declined significantly, with the budget for general hospitals dropping by as much as 41.8%. This nearly 40% reduction in budget has further exacerbated the operational challenges faced by public hospitals.

In light of the introduction of the “Public Hospital Economic Management Year” policy, public hospitals must prioritize economic management and reduce operational costs by “tightening their belts” over the coming year. Under these circumstances, what steps should public hospitals take? What measures can be employed to “cut costs”?

It can be said that, against the backdrop of enhanced economic management in public medical institutions, these institutions are facing significant challenges.

The sustained impact of the multi-pronged healthcare security initiatives has placed immense operational pressure on medical institutions. A series of policies—including centralized drug procurement, adjustments to healthcare insurance policies, reforms in payment systems, crackdowns on insurance fraud, and unannounced inspections—have left many medical institutions struggling to cope. Furthermore, the lack of coordination in the linked reforms of healthcare services, health insurance, and pharmaceuticals, coupled with the stagnation of medical service price reforms, has significantly disrupted the normal operations of medical institutions.

“Promoting the high-quality development of public medical institutions and facilitating the transformation of the development model from scale expansion to quality and efficiency, as well as the transition of the management model from extensive to refined.” This is the key principle proposed in the “Year of Economic Management for Public Medical Institutions” initiative.

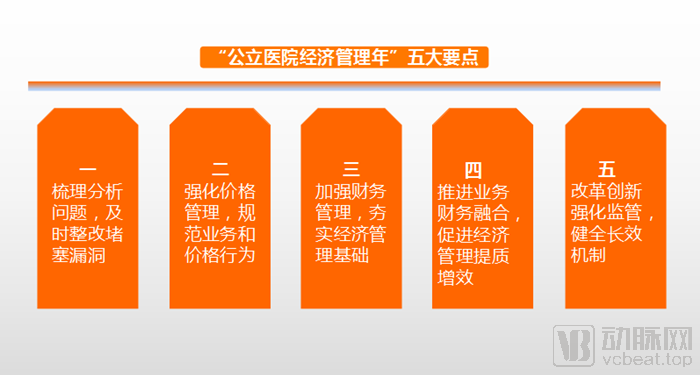

For public hospitals, the "Year of Economic Management for Public Medical Institutions" proposes five key tasks:

First, systematically analyze issues and promptly implement corrective measures to close loopholes. Identify prominent problems in economic management and conduct uncovered by external regulatory activities—such as audits, inspections, and examinations—as well as weaknesses and shortcomings in internal operational management. Ensure timely and effective rectification. Conduct scientific analysis of root causes, establish and improve rules and regulations, and take proactive measures to prevent future occurrences.

Our analysis indicates that the shortcomings in economic management are primarily manifested in the failure to establish a specialized and systematic management framework. Currently, many hospitals have not established dedicated departments to oversee economic management; instead, they merely assign these responsibilities to finance or accounting personnel. The lack of professional management bodies has led to the neglect or even disregard of hospital economic management work.

Secondly, even though some hospitals have established specialized departments for hospital economic management, the personnel responsible for this work in practice often lack professional knowledge in hospital economic management. They are typically transferred temporarily from other departments and do not possess the necessary expertise. Given the heavy workload and demanding tasks associated with hospital economic management, these managers find themselves overwhelmed and unmotivated. As a result, the level of hospital economic management fails to meet expectations, preventing it from contributing effectively to the hospital's development.

Second, strengthen price management and standardize business and pricing practices. Establish and improve self-inspection, self-correction, and internal oversight mechanisms; standardize fee management, medical service delivery, and the management of pharmaceuticals and medical devices; and promptly adjust prices in the hospital’s price management system in accordance with changes in government medical service pricing policies.

Some hospitals exhibit insufficient attention to the management of medical service pricing, inadequate understanding among management personnel, poor alignment with hospital development requirements, and a lack of theoretical foundation for pricing.

These issues have directly led to inadequate adjustments in medical service prices, unclear definitions of medical service items, inaccurate supervision and inspection of medical service pricing, incomplete medical service offerings, untimely updates to medical service prices, and unreasonable price ratios among different medical specialties. These problems directly impact the development of public hospitals.

Third, strengthen financial management, solidify the foundation of economic management, and firmly establish the concept of "living within tight means." Public hospitals must improve their cost accounting systems, operational management policies and measures, and full-process internal control systems, while strengthening procurement and donation management.

Effective financial management helps reduce unreasonable financial costs and ensures the hospital's economic efficiency by supervising and managing financial activities, funds, and resources.

However, there are still some problems in the financial management of hospitals, such as issues with financial budget management, asset accounting, financial supervision, and the team of financial personnel. These issues weaken the quality of financial management and affect the economic benefits of hospitals.

Fourth, promote the integration of business and finance to enhance the quality and efficiency of economic management. Public hospitals may establish independent operational management departments; tertiary hospitals and secondary hospitals with appropriate conditions shall appoint chief accountants to strengthen the development of professional talent in economic management.

“Guiding Opinions of the General Office of the State Council on Establishing a Modern Hospital Management System” (Guo Ban Fa [2017] No. 67) explicitly set forth requirements for achieving standardized, refined, and scientific hospital management, and for basically establishing a modern hospital management system characterized by clear rights and responsibilities, scientific management, sound governance, efficient operations, and robust oversight.

To adapt to the development of the new era, public hospitals need to integrate medical services with financial management. The integration of business and finance in public hospitals refers to the convergence of operational activities—such as medical care, nursing, scientific research and teaching, and pharmaceutical management—with financial activities. Operational activities consume resources, which are a key object of financial management. Improving resource utilization efficiency and enhancing the quality of medical services are shared goals of both business and financial functions. Currently, public hospitals commonly face challenges in integrating business and finance, including low synergy between operational and financial departments, a tendency to prioritize clinical services over financial management, and a lack of synergistic effect between the Hospital Resource Planning (HRP) system and the Hospital Information System (HIS). Promoting the integration of business and finance is highly beneficial for hospital development.

Fifth, strengthen supervision through reform and innovation, and improve long-term mechanisms. Earnestly implement the requirements for deepening healthcare system reform by adopting pragmatic, effective, and practical measures. Public hospitals should advance the establishment of long-term internal management mechanisms for medical service pricing, strengthen internal audit oversight, and enhance regulatory tools.

Strengthening regulatory oversight first requires the establishment of evaluation systems for medical quality, safety, services, and performance, along with the implementation of evaluations, inspections, and supervision of hospitals’ medical quality, safety, services, and financial management. In this context, strengthening internal audit supervision plays a crucial role in helping public hospitals mitigate risks, ensure safe operations, and achieve sustainable development.

Hospital internal audit departments can leverage their inherent advantages to participate in hospital risk oversight, helping identify and evaluate significant risk factors and thereby facilitating the improvement of risk management systems in public hospitals.

In summary, it is evident that under the current policy landscape, management reform in public hospitals is imperative. We believe that, in the process of strengthening economic management, outsourcing non-core business operations represents a viable model for hospitals.

To navigate “tight times” effectively, hospitals must prioritize cost control.

With the deepening of China's healthcare reform,Cost Issues Have Become a Key Focus for Public Hospital Administrators and the Government, cost management is not only a requirement of national policies but also essential for the self-development of public hospitals and an important way to enhance social benefits. However, the current situation of cost management in China's public hospitals is far from optimistic, as it started late and remains at a preliminary stage.Many public hospitals suffer from weak cost management awareness, inaccurate cost accounting, incomplete cost analysis, and inadequate cost control.

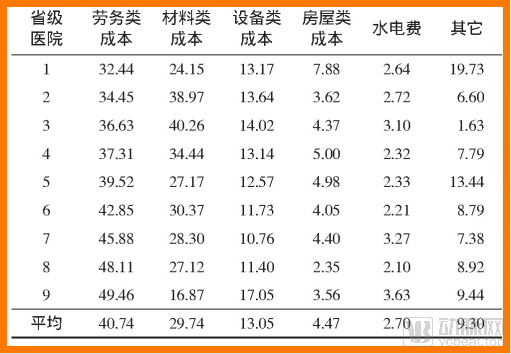

What are the cost components of public hospitals? As stated in "Analysis of Cost Composition in Hospitals at Different Levels Across Five Provinces," a report from the national healthcare service project cost monitoring initiative jointly conducted by the Department of Planning and Finance (formerly under the Ministry of Health) and the Health Management and Policy Research Center of Shandong University,The costs of public hospitals mainly include labor costs, material costs, equipment costs, housing costs, electricity fees, and others.

A survey and comparative analysis of nine provincial-level hospitals revealed that labor-related costs accounted for 32.44%–49.46% of total costs, with a mean of 40.74%, constituting the primary component of hospital expenditures. Material-related costs accounted for 16.87%–40.26%, with a mean of 29.74%. The details are presented in the table below:

Table 1 Cost Composition of Six Categories in Provincial Hospitals (%)

(Figure caption: Composition of six cost categories in nine provincial-level hospitals)

A comparative survey of 14 selected municipal-level hospitals revealed that labor costs accounted for 34.59%–56.17% (mean: 45.74%), while material costs accounted for 14.61%–39.41% (mean: 26.08%).

Table 2 Composition of Six Cost Categories in Municipal Hospitals (%)

(Figure caption: Composition of six cost categories across 14 municipal-level hospitals)

Among the 13 selected county-level hospitals, the composition of six cost categories was as follows: labor costs accounted for 37.88%–64.58%, with a mean of 49.55%; material costs accounted for 11.70%–26.94%, with a mean of 19.35%.

Table 3 Composition of Six Cost Categories in County-Level Hospitals (%)

(Figure caption: Composition of six cost categories in county-level hospitals)

An analysis of cost distribution data across provincial, municipal, and county-level hospitals reveals that labor costs and material costs constitute the majority of expenses at all hospital levels. Notably, the proportion of labor costs increases as the hospital level decreases, whereas the proportion of material costs shows a declining trend with lower hospital levels. The shares of costs for equipment, facilities, utilities (water and electricity), and other items do not vary significantly among the three hospital tiers.

Labor and material costs are primarily concentrated in the core medical operations of hospitals. This implies that, to reduce costs, hospitals must not only strengthen management within their core medical services but also curtail expenditures in non-core medical service areas.

The operational model of outsourcing non-core hospital services is being adopted by an increasing number of hospitals.

Non-Core Medical Operations of Hospitals, refers to administrative and logistical support functions other than core medical services (such as clinical care and nursing) and certain administrative tasks. These include hospital disinfection, cleaning, distribution, linen production, laundering, catering, landscaping, wastewater treatment, medical waste management, facility maintenance, energy supply, building management, parking lot operations, and security management.

Its operational costs, efficiency, quality, and model will directly affect the orderly development of core medical services and the achievement of healthcare reform objectives.

Non-core medical business management can be broadly categorized into three models: self-managed, jointly managed, and outsourced. However, regardless of the model,“Socialization” is considered an essential element for effectively managing non-core medical services.“Socialization” is the inevitable path for non-core medical businesses to break free from high investment, high complaint rates, low efficiency, low quality, and low returns.

“Socialization” is a management philosophy. Merely outsourcing or jointly managing non-core medical services by handing them over to external parties does not constitute true socialization. The core element lies in introducing competitive mechanisms into non-core medical services, benchmarking these services against comparable offerings in the broader market, and aligning service concepts, standards, quality, and pricing with societal norms. This represents a socialized management model—specifically, the socialization of management—rather than simply the socialization of service providers.

Taking the Sterile Supply Department as an example, the Sterile Supply Center is a cost center within a hospital—a department that incurs expenses without generating direct revenue—while also consuming a significant portion of hospital resources, including clinical space and staffing quotas for professional nursing personnel. Generally, the fixed asset investment required for a public hospital to establish its own Sterile Supply Center ranges from RMB 10 million to RMB 20 million, excluding labor allocation and operational maintenance costs.

In contrast, outsourcing sterile supply services through the procurement of third-party medical services represents a viable cost-reduction strategy for hospitals. As specialized entities, third-party sterile processing providers handle these logistical support functions, thereby facilitating the regional sharing of healthcare resources and offering significant advantages.

As a critical platform for supplying foundational medical resources, regionalized sterile supply centers play a significant role in upgrading and supplementing existing healthcare resources. Their characteristics of resource sharing and balanced allocation align closely with the direction of China’s healthcare reforms, such as tiered diagnosis and treatment, private healthcare provision, and the integration of medical resources.

The earliest regionalized sterile supply center in China was the Futian Sterile Supply Center in Shenzhen, established in 2002, which provided services to 24 surrounding medical institutions. Subsequently, hospitals such as West China Hospital, Shenzhen Luohu District People’s Hospital, Liyang People’s Hospital, Guangzhou Huadu District People’s Hospital, Qilu Hospital of Shandong University, and Jining No. 1 People’s Hospital gradually implemented standardized, unified management of regional sterile supply operations, thereby achieving shared healthcare resources within their respective regions. In the same year that China began implementing the “Regulation for cleaning, disinfection and sterilization effect monitoring of central sterile supply department in hospital” (WS 310-2009), New Helix established the first socialized sterile supply center in Suzhou, later expanding its operations to Wuhan and Nanjing.

Subsequently, professional outsourced sterilization service providers such as Julikang, Shandong Dingshengkang, and Sichuan Sinopharm Laoken Medical, along with other enterprises in the sterilization supply chain and pharmaceutical companies, began to enter the regionalized medical sterilization outsourcing industry by leveraging their financial strength, resources, or professional expertise.

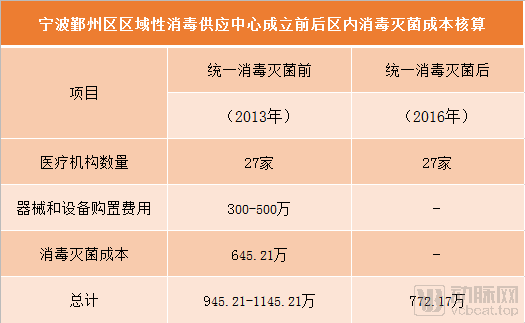

According to a case study released by the Healthcare Service Governance Research Center of the Institute for Hospital Management at Tsinghua University, Yinzhou District in Ningbo established a government-led regional sterile supply center to provide centralized sterilization services for 27 primary and lower-tier medical institutions within the region. Although the sterilization costs for these 27 medical institutions amounted to only RMB 6.4521 million in 2013, prior to the establishment of the regional sterile supply center, superior health authorities conducted centralized tendering and procurement of instruments and fixed equipment, which were then allocated to individual medical institutions. This resulted in annual acquisition costs ranging from RMB 3 million to RMB 5 million, bringing the total cost to between RMB 9.4521 million and RMB 11.4521 million.

Following the implementation of centralized disinfection and sterilization, the total expenditure on disinfection and sterilization across 27 medical institutions in Yinzhou District, Ningbo City, decreased to RMB 7.7217 million in 2016, which was lower than the total cost in 2013.As shown in the table below:

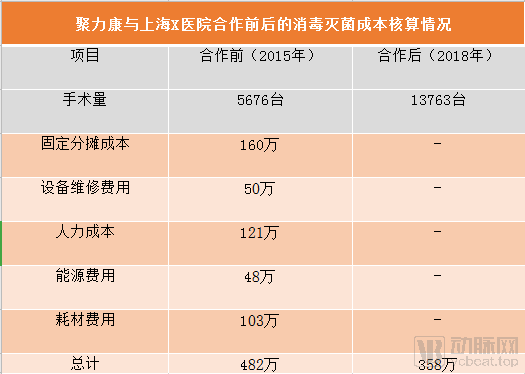

Data shared by Julikang indicates that, following its collaboration with Shanghai X Hospital, sterilization and disinfection costs were significantly reduced.

Juli Kang, established in 2010, is a well-known independent third-party medical service provider specializing in sterile supply services in China. It has currently set up independent third-party medical sterile supply centers in multiple regions.

Shanghai X Hospital has a total of 600 beds and 10 operating rooms. Prior to the collaboration, it was equipped with four washer-disinfectors and five sterilizers, and staffed by 15 personnel. Outsourcing of disinfection and sterilization services was implemented starting in 2016; detailed cost accounting is presented in the table below:

In 2015, Hospital X in Shanghai performed 5,676 surgeries, with a total sterilization and disinfection cost of RMB 4.82 million; in 2018, the surgical volume increased to 13,763 cases, and the total cost for outsourced sterilization and disinfection services was RMB 3.58 million.Despite a more than two-fold increase in surgical volume, the direct costs of disinfection and sterilization in 2018 decreased by 25.7% compared with those in 2015.

In addition to reducing direct costs, outsourcing sterilization services also lowers certain indirect costs for hospitals, including the opportunity cost associated with increased demand for prime medical facility space, upgrade and renovation expenses driven by continuously rising industry standards, and staffing pressures resulting from increased workloads. In summary, for Shanghai X Hospital, implementing outsourced sterilization services has not only effectively reduced financial expenditures but also alleviated challenges related to hospital accreditation evaluations, constraints on medical facility space, and staffing shortages.

A comparison of the above data demonstrates that third-party sterile supply centers can help hospitals achieve cost reduction after outsourcing sterilization services.

Since 2016, with the intensive release of policy documents concerning third-party sterile supply services, the socialization and corporatization of medical sterile supply services have shown a clear acceleration trend.

Outsourcing of Non-Core Medical Services in Hospitals Is Gaining Wider Recognition; Its Key Value Lies in Providing Safe, Effective, Timely, and Cost-Efficient Support for Core Medical Services, Thereby Significantly Promoting the Development of Public Hospitals.

Of course, alsoOnly as more and more hospitals prioritize cost control will the outsourcing of non-core hospital services accelerate.

We have reason to believe that the introduction of the “Public Medical Institutions Economic Management Year Policy” will inevitably accelerate this process, as public hospitals at all levels strengthen their economic management.

References:

Liang Tao. “A Brief Discussion on Problems Existing in Hospital Financial Management and Countermeasures.” 2020

Chen Man. Exploration and Practice of Hospital Economic Management under the New Situation. 2020

Yu Baorong, Liang Zhiqiang, Zhang Xiaoxing, Sun Qiang, Ge Renwei. "Analysis of Cost Composition in Hospitals at Different Levels Across Five Provinces." 2014.

Shen Kui. “Promoting the Socialization of Non-Core Medical Services to Foster the Development of Public Hospitals.” 2013

Zhang Shiru. “Problems and Solutions in Hospital Cost Management.” 2019.