Can Neurointervention Replicate the Success of Cardiovascular Intervention? Insights from a Sector Backed by Hillhouse and Sequoia

“I never imagined that neurointervention would gain such rapid traction; it’s now the hottest trend in the field,” an investor who positioned themselves in the neurointervention space two years ago told VCBeat.

Data from the primary market corroborates his observations. According to financing data from the VCBeat Orange Database, six financing deals were closely clustered in the neurointerventional field between June and August of this year. Among these, five companies secured funding amounts reaching the hundred-million-yuan level, with participation from renowned investment firms such as Hillhouse Capital, Sequoia China, and CITIC Medical Fund. The surge in activity within the neurointerventional sector in the primary market is a ripple effect of the broader positive outlook on the minimally invasive interventional industry.

In the first half of this year, the cardiac intervention sector in the secondary market not only saw multiple companies go public but also experienced a significant surge in stock prices. Since its listing on the Hong Kong Stock Exchange in 2010, MicroPort’s stock price had long hovered around HK$8 per share; however, as of August 16, 2020, it reached HK$35 per share. Meanwhile, Peijia Medical’s market capitalization approached RMB 20 billion following its IPO. Notably, Peijia Medical’s presence in both the cardiovascular and neurointerventional tracks has highlighted new opportunities in the neurointerventional field to the market.

The neurointerventional field, still in its growth stage, is seen as replicating the trajectory of cardiac intervention from a decade ago, with the market expanding rapidly and domestic companies emerging.

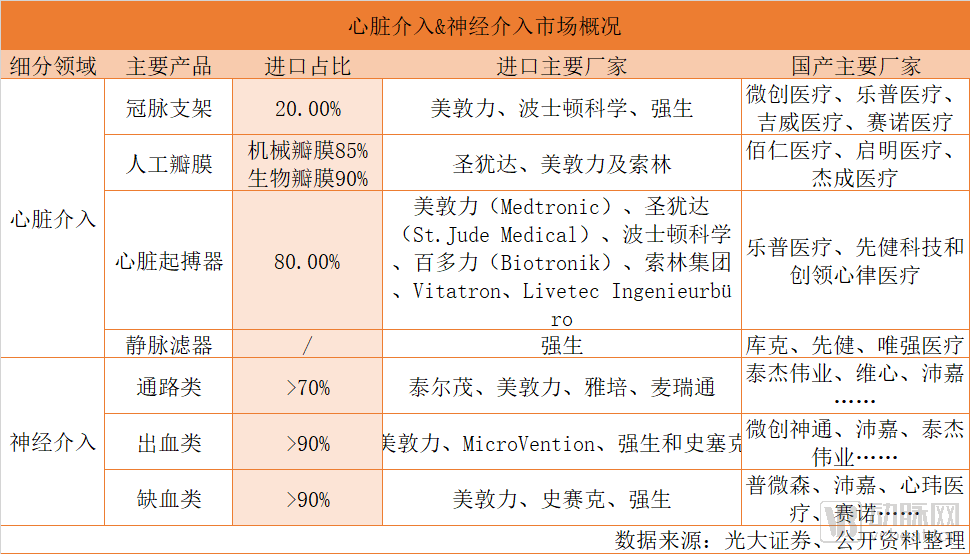

At present, China’s neurointerventional market is dominated by foreign companies such as Medtronic, Johnson & Johnson Medical, and Stryker. Foreign firms account for more than 80% of the market, with Medtronic alone holding over 60%. On the other hand, domestic players including MicroPort NeuroTech, Peijia Medical, Taicore Medical, GeniusMed, and Xinwei Medical are ramping up efforts to build comprehensive product portfolios from the ground up.

We can anticipate that the neurointerventional field will have the opportunity to replicate the success of domestic substitution seen in the coronary intervention sector.

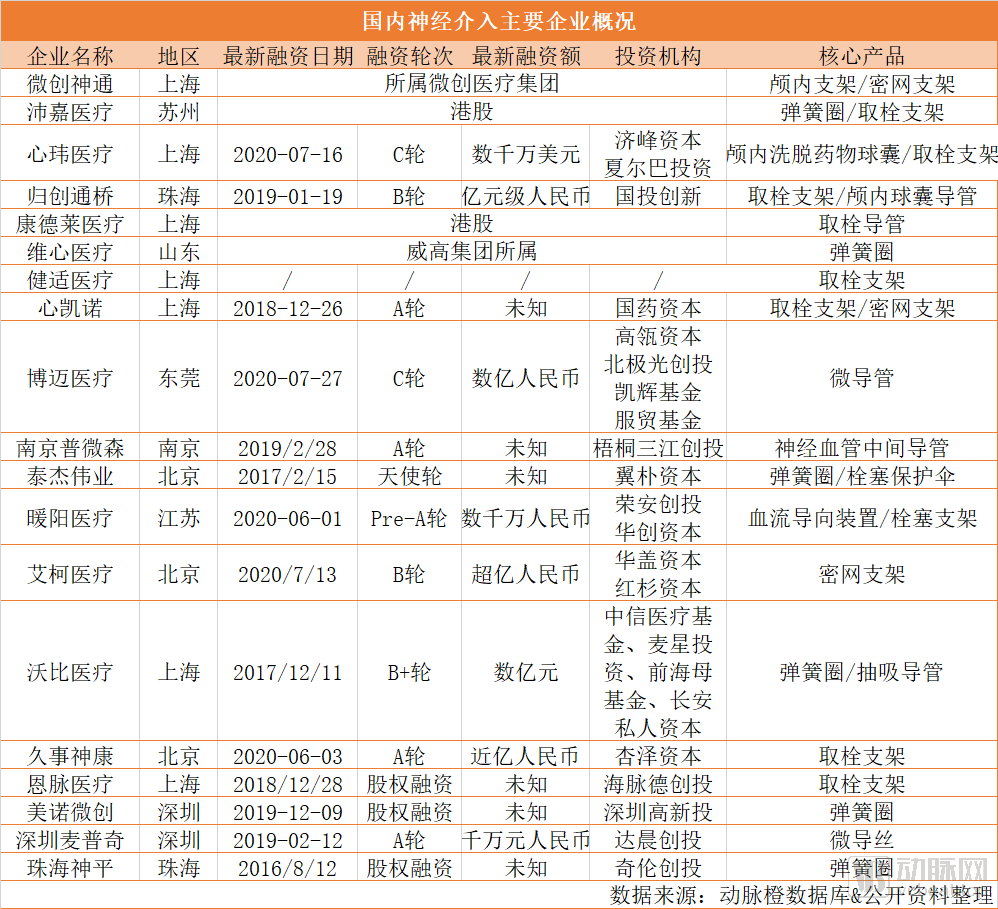

In the field of neurointervention, according to incomplete statistics from VCBeat, more than 20 companies have established their presence. These 20 companies include listed enterprises such as MicroPort Medical, Peijia Medical, and Weixin Medical (a subsidiary of WEGO Group). Among them are also companies that have received support from top-tier venture capital firms and completed several rounds of substantial financing, such as JetMed Medical, Xinwei Medical, and Aike Medical. It can be said that the domestic substitution of neurointerventional products is entering a golden age.

From another perspective, the field of neurointervention features high barriers to entry and technical complexity; domestic substitution is more challenging than in coronary intervention, making the realization of full localization far from straightforward.

Amid the fervor surrounding neurointervention, what industrial transformations are underway, driven by capital? VCBeat has mapped out the neurointervention landscape.

Neurointerventional procedures are primarily associated with cerebrovascular diseases, which have long been a leading cause of death in China. Each year, there are over one million new cases of cerebrovascular disease in the country. According to data from the 2019 Health Statistical Yearbook, an analysis of discharge outcomes for patients from public hospitals in 2018 revealed that 5.67 million patients were discharged with a diagnosis of cerebrovascular disease, accounting for 6.48% of all disease cases.Among them, there were over 720,000 cases of intracranial hemorrhage; 3.73 million cases of cerebral infarction; and 87,000 cases of cerebral artery occlusion and stenosis.. In terms of disease-related costs, the average medical expenditure per patient for cerebral hemorrhage at provincial hospitals was 25,480 yuan, while that for cerebral infarction was 14,117 yuan.

In the field of minimally invasive interventional medicine, neurointervention is hailed as the "crown jewel" of interventional procedures, signifying the exceptionally high level of difficulty in this specialty.

Neurointervention, supported by digital subtraction angiography (DSA) systems, employs endovascular catheter-based techniques to diagnose and treat pathologies involving the human neurovascular system through specific methods such as selective angiography, embolization, balloon angioplasty, mechanical thrombectomy, and drug delivery. Neurointerventional therapy is a method for treating cervical or intracranial vascular diseases by accessing the neck or intracranial vessels via special catheters introduced through femoral artery (or femoral vein) puncture.

Compared with cardiovascular intervention, neurointervention is more difficult to perform. Structurally, there are venous sinuses between the cerebral veins and the jugular veins, which are unique structures within the cranium. Cerebral blood vessels are thinner than cardiovascular vessels; cerebral arteries are slender, long, and highly tortuous, lacking elastic pulsation.

In terms of quantity, the coronary arteries can be divided into three branches: the left anterior descending artery, the circumflex artery, and the right coronary artery. The cerebral vasculature consists of six vessels branching from the aortic arch: the bilateral vertebral arteries, the bilateral common carotid arteries, and the bilateral subclavian arteries.

In terms of disease complexity, cardiovascular intervention primarily utilizes stents to dilate vessels and address stenosis. However, cerebrovascular diseases present with more complex and diverse clinical manifestations. In neurointervention, in addition to managing stenosis, practitioners also treat cerebral aneurysms (often described as "bubbles" formed by cerebrovascular structures) and ischemic stroke.

Therefore, neurointerventional procedures demand higher precision from medical devices, requiring materials that are more refined, flexible, and offer superior trackability. Coronary stents emerged in the 1970s and 1980s, whereas intracranial vascular stents did not appear until 2002.

Although China’s neurointerventional field started late, it has developed rapidly. Before 2015, neurointervention was not highly regarded, but today it is flourishing. Since 2015, China has entered the “Stroke Care 2.0” era, with domestic neurointerventional radiology accelerating its development.

In terms of market size and growth rate, data from the China Medical Device Blue Book, Frost & Sullivan, and the 5th Academic Annual Meeting of the Neurointerventional Branch of the Chinese Stroke Association (CINS 2020) indicate that in 2019, the market size of neurointerventional devices in China reached RMB 6.3 billion, with 40,000 thrombectomy procedures performed. The compound annual growth rate (CAGR) from 2015 to 2019 was as high as 30%, signaling a period of robust development for neurointervention.

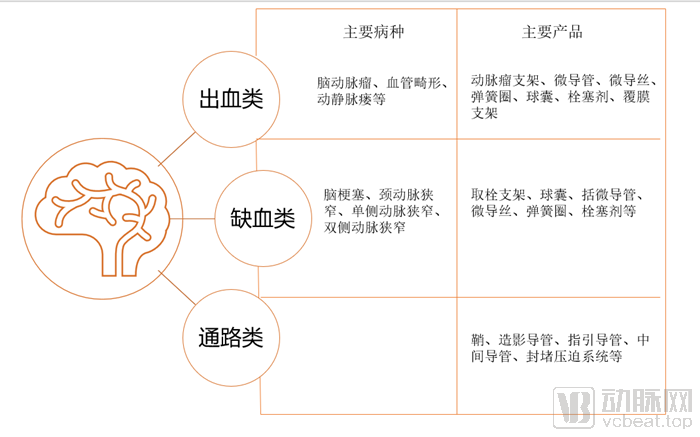

In terms of indications, the major diseases in the field of neurointervention include ischemic stroke, arterial stenosis, and aneurysms; the former two are classified as ischemic conditions, while aneurysms fall under hemorrhagic conditions. In the neurointervention market, products are primarily categorized into three major types.: Pathway-related; Hemorrhagic; Ischemic. The distribution of major products corresponding to disease types is shown in the figure below.

Introduction to Major Diseases and Corresponding Products in the Field of Neurointervention

An industry insider told VCBeat, “Because the incidence of ischemic stroke is higher, the market for thrombectomy products should be larger than that for aneurysm interventional products, with market share even dozens of times greater.”

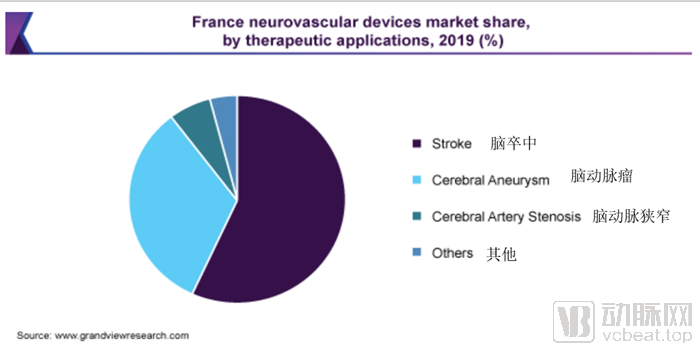

Based on statistical data from France, where neurointerventional techniques are more advanced, stroke accounts for the largest market share, followed by aneurysms and cerebral arterial stenosis. It is anticipated that China will exhibit a similar trend in the future.

Market Share by Disease in the French Neurointerventional Market, 2019

Currently, only foreign-funded enterprises have achieved full coverage across all three major product categories, while some domestic companies have managed to cover the entire product line for a single disease indication. By analyzing the current status of major products in the neurointerventional market, we can gain insights into the distribution and strategic focus of domestic companies in this sector.

Neuroischemic Products

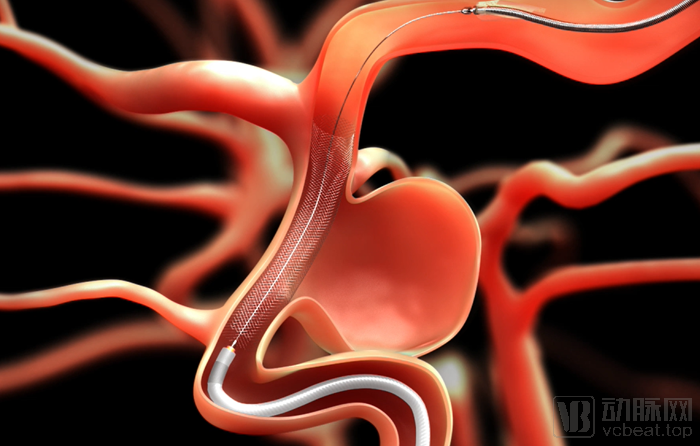

Neuroischemic products are primarily associated with two major categories of diseases: ischemic stroke and cerebral artery stenosis. Products for neurointerventional treatment of ischemic stroke mainly include thrombectomy stents, aspiration thrombectomy devices, and other related products.

Thrombectomy stents for ischemic stroke are delivered via a single microcatheter inserted through an incision in the leg, navigating to the cerebral artery affected by the stroke to remove the occlusive plaque and restore blood flow. In 2015, updated guidelines for the management of acute ischemic stroke in both China and the United States granted this approach the highest level of recommendation.

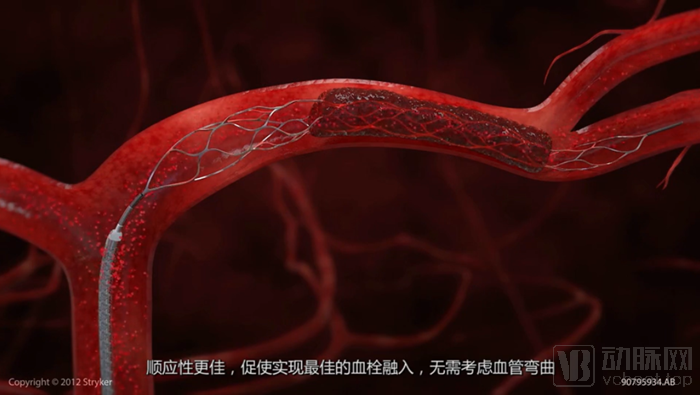

Products from international giants, such as Medtronic’s Solitaire, Stryker’s Trevo stent retriever, Penumbra’s thrombectomy device, and Johnson & Johnson Medical’s Revive SE stent system, are the mainstream offerings in the market. Stryker’s Trevo ProVue thrombectomy device is the first fully visible stent retriever on the market and is hailed as a “thrombectomy miracle.”

Among domestic manufacturers, Nico Medical’s thrombectomy device, now acquired by Jianshi Medical, has already been launched. Thrombite™ (Jiaolong), a thrombectomy stent independently developed by Zhenchuang Tongqiao, received CE certification from the European Union in March this year. “Jiaolong” has also been included in the National Medical Products Administration (NMPA) Class III “Innovative Medical Device” green channel program, completed China’s multicenter randomized controlled registration clinical trials, and is poised for imminent launch in the domestic market.

Peijia Medical’s Jiaqi and Mindray Neurovascular’s thrombectomy stents are currently in clinical trials. Mindray Neurovascular’s thrombectomy system features China’s first multi-point radiopaque thrombectomy technology and is the only long-length thrombectomy stent available domestically. Companies such as Shenyang KaiNuo Medical and Jiushi Shenkang have also entered the thrombectomy stent market.

Stryker Trevo ProVue Thrombectomy Stent: Thrombectomy Procedure. Image source: Stryker official website.

In addition to stent retrievers, aspiration thrombectomy is also an important approach for treating ischemic stroke. The primary tools for aspiration thrombectomy are aspiration catheters or reperfusion catheters, which utilize negative pressure suction to reach the proximal end of the occluded vessel and remove the thrombus. Currently, 80% of interventional treatments for ischemic stroke in the U.S. market initially employ aspiration catheters.

Industry insiders believe that, within the field of interventional consumables, technical difficulty increases progressively from stents to balloons to catheters, with implantation procedures being more challenging than general interventional ones. Therefore, the research, development, and manufacturing of aspiration catheters are more difficult than those of thrombectomy stents.

Major importers of aspiration thrombectomy products include Medtronic, Zeon Medical (Japan), and Penumbra; all three companies have obtained domestic regulatory approval certificates in China. Among domestic manufacturers, Weibo Medical is developing an aspiration catheter. Currently, Weibo Medical’s intracranial thrombus aspiration catheter is applying for U.S. FDA and CE certification, while clinical trials for domestic registration have already commenced at hospitals such as Xuanwu Hospital.

The second most prevalent condition among ischemic diseases is cerebrovascular stenosis, specifically intracranial atherosclerotic stenosis, with the primary therapeutic products being balloons and stents.

For the interventional treatment of intracranial atherosclerotic stenosis, arterial stents are generally delivered to the site of vascular stenosis via balloon dilation catheters, or drug-coated balloons are used directly for treatment. This approach is indicated for patients with ischemic symptoms and stenosis greater than 50%, or for asymptomatic patients with stenosis greater than 70%.

Major domestic manufacturers of intracranial balloon dilation catheters include Sino Medical (which has obtained certification) and Mindray Medical. Sino Medical’s intracranial drug-eluting stent is currently in the late stages of clinical trials.

Neurohemorrhagic Products

Hemorrhagic cerebrovascular diseases primarily include intracranial aneurysms and cerebral arteriovenous malformations. Among hemorrhagic conditions, intracranial aneurysm is a prevalent and major disease. According to clinical statistics, the incidence of intracranial aneurysms ranks third among cerebrovascular diseases, following cerebral thrombosis and hypertensive intracerebral hemorrhage. In China, there are more than 150,000 patients with aneurysms each year.

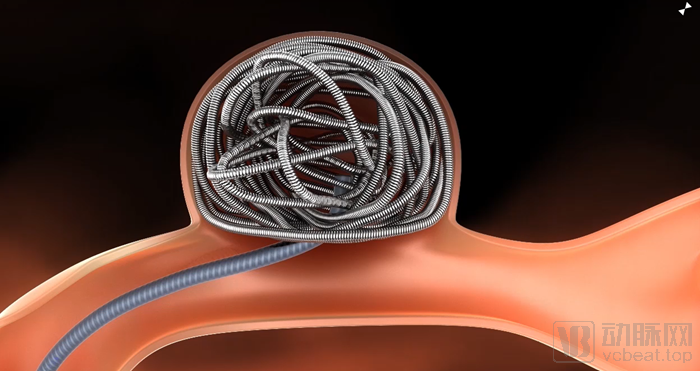

The main products for endovascular treatment of aneurysms are coils and flow-diverting stents.

Medtronic AXIUM™ PRIME Detachable Coils. Image source: Medtronic official website.

Coils are used in embolization procedures, where a microcatheter is inserted into the aneurysm sac, and then the coil is pushed into the aneurysm sac via the microcatheter using a pusher. By leveraging the mechanical occlusion effect of the coil and the subsequent thrombotic occlusion, the aneurysm is isolated from the blood circulation of the parent artery, thereby achieving the goal of preventing aneurysm re-rupture.

Data from Peijia Medical’s prospectus shows that the number of endovascular coil embolization procedures for cerebral aneurysms in China increased from 25,300 in 2014 to 52,300 in 2018, representing a compound annual growth rate (CAGR) of 19.7%. The volume is projected to reach 158,000 procedures by 2025. The Chinese coil embolization market is expected to reach RMB 5.537 billion in 2025, with a CAGR of 14.2% from 2018 to 2025. The market for intracranial aneurysm stents in China is estimated to expand to RMB 812 million by 2025, with a CAGR of 15.% from 2018 to 2025.

In the coil market, major imported brands include Medtronic’s AXIUM, Johnson & Johnson’s coils, and Stryker’s Target coils. The prices of imported coils range from RMB 15,000 to RMB 20,000.

There are currently many domestically approved brands of coils, including Peijia Jiaqi, Weixin Medical, Taijie Weiye, and Wobi Medical, among others that have received approval. The price of domestically produced coils is under RMB 10,000.

In addition to coils, flow diverter stents have also garnered significant attention. Currently, flow diverter stents represent an advanced international approach for treating large and complex aneurysms. By providing a flow-diverting effect, these stents prevent blood from entering the aneurysm sac after deployment, leading to gradual thrombosis and eventual resolution of the aneurysm.

Medtronic PIPELINE™ FLEX Flow Diverter Stent. Image source: Medtronic official website

The most well-known product among flow diverter stents is Medtronic’s PIPELINE. The first-generation PIPELINE device was launched in 2013 and was the earliest flow diversion device applied in clinical practice. It has now been upgraded to the third generation, which features a phosphorylcholine (PC) biocompatible polymer coating to reduce thrombosis risk.

In the field of flow diverter stents, there are also competitive domestically produced products. MicroPort NeuroTech’s Tubridge flow diverter has broken the market monopoly held by imported flow diverters and, together with Medtronic’s Pipeline flow diverter, is regarded as one of the “two giants” in China’s flow diverter market.

The core products under development at start-ups such as XinKaiNuo, Aico Medical, and Nuanyang Medical are also flow diverter stents.

Regarding flow diverter stents, the product category is still undergoing continuous iteration. There is room for improvement in the flow diverter stents currently available in clinical practice; therefore, for startups, there remains market potential if they can address existing issues.

It is reported that the price of flow-diverting stents ranges from RMB 180,000 to 200,000. The use of flow-diverting stents in clinical practice in China is growing, although the initial surgical volume was relatively low. Among hospitals with a higher volume of flow-diverting stent procedures, Beijing Tiantan Hospital is estimated to have performed 300 such cases between 2016 and 2017.

In addition, the third category of neurointerventional products in the neurovascular access field includes distal access catheters, microcatheters, balloon guide catheters, sheaths, angiographic catheters, guide catheters, intermediate catheters, and compression hemostasis systems. These devices are primarily used to establish a vascular delivery pathway from the blood vessel to the target site (lesion) for various indications.

Among access device products with low barriers to entry, the localization process has advanced rapidly. Companies such as MicroPort Medical, Peijia Medical, and Taijie Weiye have achieved independent R&D and manufacturing capabilities for these products. The import share of access devices stands at approximately 70%, significantly lower than the over 90% import reliance seen in hemorrhagic and ischemic product categories, indicating that partial localization has already been achieved in the access device segment.

Based on the preceding introduction to the neurointerventional field, it is evident that the neurointerventional market is characterized by import monopolies, high barriers to entry, and rapid growth. Additionally, a significant feature of this sector is its low penetration rate.

In contrast to cardiac interventions, which are already being performed at county-level hospitals, neurointerventions are generally only available at city-level hospitals. China sees over one million new stroke cases annually, yet the actual number of mechanical thrombectomy procedures performed in 2017 was fewer than 15,000, representing a penetration rate of merely 0.56%, indicating substantial potential for growth.

Compared with countries where neurointerventional procedures are more advanced, China’s neurointerventional field is still in its early stages of development. In France, where neurointervention has matured, 90% of cerebrovascular diseases, particularly hemorrhagic conditions such as aneurysms, are treated with interventional therapies.

The low penetration rate of China’s neurointerventional market is primarily attributable to two factors. First, a shortage of skilled neurointerventional physicians is constraining market growth.

Neurointerventional procedures are no less complex than open craniotomy. Angiography does not visualize all blood vessels, and these interventions demand a high level of neuroanatomical expertise from physicians. The operative field available to the surgeon during neurointerventional procedures is also limited, so intraoperative complications such as bleeding severely test the physician’s ability to respond effectively. Moreover, performing neurointerventional surgery requires multidisciplinary coordination among neurology, interventional radiology, diagnostic imaging, and anesthesiology, placing substantial demands on a hospital’s comprehensive capabilities. Consequently, it is unlikely that neurointerventional procedures will penetrate county-level hospitals to the same extent as cardiovascular interventions in the foreseeable future.

According to expert interview data from China Everbright Securities, as of 2020, there were no more than 300 neurosurgeons in China capable of performing coil embolization for hemorrhagic conditions; only about 20 neurosurgeons in the country were proficient in using flow-diverting stents for aneurysm flow reconstruction surgery.

However, some investors have pointed out that at the current stage, there are few approved domestic products, the number of neurointerventional procedures performed in China is relatively low, and the existing pool of physicians is not yet scarce enough to hinder market growth. Of course, if more products gain approval in the future, the shortage of physicians may become more pronounced.

Second, the high prices of neurointerventional devices.

Renowned neurointerventional specialist Dr. Liu Aihua from Beijing Tiantan Hospital stated in an interview, “In recent years, neurointervention has developed rapidly in China, with most provincial-level hospitals performing well. However, the primary factor constraining the development of neurointervention in China is neither devices nor personnel, but economic conditions. The current prices of products are indeed too high; for the same equipment, domestic prices may be 5–10 times higher than those abroad. While China has made rapid progress in medical device technology, prices have not decreased sufficiently and are expected to drop further in the future. If prices decline, I believe the adoption of minimally invasive neurointerventional therapies will become more widespread.”

How to Reduce Prices: From the Development of High-End Cardiovascular Devices, Localization Is an Inevitable Path. According to reports and statistics from VCBeat, companies have been laying out their strategies in the field of neurointerventional localization since 2012.

However, in the overall neurointerventional market, ischemic and hemorrhagic products are core offerings and hold the majority of the market share. Achieving domestic production of thrombectomy stents, coils, balloons, and other devices is key to realizing substantial price reductions in the field of neurointervention.

VCBeat has compiled and analyzed the current product portfolios of major domestic companies (as shown in the figure below). Based on this analysis, embolization coils are among the most widely marketed domestic products. According to Peijia Medical’s prospectus, Peijia Medical is the first company in China to commercialize embolization coil products. Multiple companies have also entered the markets for thrombectomy stents and flow diverters, resulting in intense competition. At present, only Jianshi Medical has a thrombectomy stent on the market, and only MicroPort NeuroTech has a flow diverter available. However, numerous other companies have products that have either entered or completed clinical trials.

In terms of strategy, domestic startups have adopted two major approaches to product portfolio development: one is to build integrated solutions centered on specific diseases, and the other is to break through the market by focusing on individual products.

From the perspective of team backgrounds, most domestic neurointerventional startup teams originate from leading domestic and international companies such as Medtronic, MicroPort Scientific, Johnson & Johnson, and Lepu Medical, possessing extensive experience in minimally invasive interventional products.

Domestic companies are currently divided into two tiers. Among the listed companies, MicroPort NeuroTech (under MicroPort Scientific), Peijia Medical, and Sino Medical Sciences Technology are the leading enterprises in China’s neurointerventional field.

Leveraging MicroPort’s robust R&D capabilities in the field of minimally invasive interventional medicine, MicroPort NeuroTech has established a comprehensive product portfolio for stroke interventional therapy. The company has commercially launched a range of neurointerventional products, including micro guidewires, vascular reconstruction devices, intracranial covered stents, intracranial arterial stents, and microcatheters. MicroPort NeuroTech supports approximately 40 cerebrovascular stent procedures daily, with its products utilized in over 1,000 hospitals.

MicroPort has not only introduced multiple products to the neurointerventional market, but it can also be regarded as the “Whampoa Military Academy” of China’s minimally invasive interventional field. A review of the resumes of founders of domestic neurointerventional companies reveals that many have previously worked at MicroPort.

In addition to MicroPort NeuroTech, Peijia Medical, which recently listed on the Hong Kong Stock Exchange, has also entered the neurointerventional sector. In the field of cardiovascular intervention, Peijia Medical focuses on transcatheter aortic valve replacement (TAVR) products. The company entered the neurointerventional market primarily through its acquisition of Jiaqi Medical in 2019. Peijia Medical already has marketed products in this space, including coils, microguidewires, and microcatheters. Its current key product under development is a stent retriever, which has now entered the clinical trial phase.

"Among pre-IPO companies, there are also several dark horses in the neurointerventional field."

For example, the merged entity of Zhenjiang Medical and Tongqiao Medical is named Zhenjiang Tongqiao. Zhenjiang Medical primarily focuses on cardiovascular interventions, while Tongqiao Medical specializes in neurointerventions. In terms of team background, Tongqiao Medical was co-founded by several senior overseas medical technology experts who returned to China, bringing together international neurointervention specialists and local elites.

Tongqiao Medical has successfully developed and registered a full portfolio of proprietary intracranial vascular interventional implants, including intracranial thrombectomy stents and intracranial aneurysm embolization coils.

Tongqiao Medical’s flagship product, the Thrombite™ (Jiaolong) thrombectomy stent, features a unique open structure with lateral helical ascending elements that rotate to ensnare thrombi, providing enhanced grip on embedded clots and minimizing the risk of detachment. As a Class III “Innovative Medical Device” approved through the National Medical Products Administration (NMPA) Green Channel, the Thrombite™ (Jiaolong) thrombectomy stent has completed its multi-center, randomized controlled registration clinical trial in China. In these trials, it demonstrated superior product characteristics compared to globally leading benchmark products and is poised for imminent launch in the Chinese market.

Xinwei Medical, which recently completed its Series C financing round, has attracted significant attention. The founding team members of Xinwei Medical all come from leading domestic and international medical device companies such as Medtronic, Johnson & Johnson, and MicroPort, possessing over 15 years of industry experience in the research, development, and sales of cerebrovascular and cardiovascular products. Wang Guohui, the founder of Xinwei Medical, hails from MicroPort Medical. Dr. Li Zhigang, Vice President of R&D and the core technology leader at Xinwei Medical, brings 27 years of experience in the medical device and biomaterials industries. Prior to joining Xinwei Medical, he served as a Senior Principal Engineer at Medtronic, where he was responsible for vascular therapy products.

After four years of development, HeartCare Medical has established five major product lines, including thrombectomy treatment for ischemic stroke, treatment for ischemic stroke with stenosis, hemorrhagic stroke treatment, prevention of cardioembolic stroke, and vascular access products, completing the development of 15–20 products.

Xinkainuo also boasts a relatively comprehensive product portfolio. Zhao Zhenxin, the founder of Xinkainuo, previously served as Co-Founder and Vice President of Technology at Peijia Medical (HK09996). Prior to joining Peijia Medical, he was among the first senior engineers at MicroPort Scientific Corporation.

In the field of neurointervention, XinKaiNuo has three product lines. Among them, the neuro-ischemic products include thrombectomy stents (for treating cerebral infarction thrombi), intracranial balloon catheters (for treating stenotic lesions), and distal protection devices (to prevent intraoperative plaque or thrombus embolization). The thrombectomy stent products are benchmarked against Medtronic’s and Stryker’s thrombectomy devices, with regulatory approval expected in the second quarter of 2021. Neuro-hemorrhagic products include intracranial flow diverter stents and intracranial aneurysm stents. Neuro-access products include distal access catheters, microcatheters, and balloon guide catheters; all access products are currently under registration application, with regulatory approval expected in the second quarter of 2021. XinKaiNuo’s current two core flagship products are the thrombectomy stent for stroke treatment and the intracranial flow diverter stent.

In the field of neurointervention, domestic manufacturers face multiple obstacles in producing products that can truly rival imported ones, due to weaknesses in the industrial chain. For neurointerventional surgeons, product requirements are higher than those for cardiovascular intervention devices. Ensuring that physicians are willing to adopt these domestically produced products and find them user-friendly remains a key challenge for their future development.

Overall, domestic companies are currently in the early stages of development, and their products have not yet entered the phase of large-scale sales validation. There is significant potential for growth in the vast field of neurointervention. An investor stated that the “golden decade” for neurointervention has only just begun, expressing confidence that at least five publicly listed companies will emerge in this sector. This projection is based on a comparison with the orthopedics market, which already boasts more than eight listed companies, despite the incidence of stroke being far higher than that of orthopedic conditions.

Neurointervention has emerged as a hot sector, driven by multiple compelling factors. It represents the next frontier in the domestic substitution of high-value medical consumables within the cardiovascular field. Furthermore, it is an inevitable trend and direction for the development of neurology following the rapid proliferation of minimally invasive interventional technologies. The field of neurointervention is also undergoing revolutionary advancements. We believe that more developments will unfold in the coming years, particularly in procedural optimization and product improvement.

References:

[Issue 89 Exclusive Interview] Liu Aihua of Beijing Tiantan Hospital: The Management of Giant Intracranial Aneurysms—Flow Diverter Stents Show Initial Promise — Neurosurgery Frontier

Neurointervention: The Crown Jewel of Interventional Surgery, a Multi-Billion Blue Ocean Poised for Takeoff — Everbright Securities

Special thanks to the following individuals for their assistance in completing this article:

Wu Yuepeng, Managing Partner of Anlong Fund

Yao Pengfei

Zhou Guanshan

(The above list is in no particular order.)