Investment Opportunities in China's Ascending Healthcare Industry: Focus on Four Key Sectors

In August, Hainan’s scorching sun mirrored the fervor of the pharmaceutical and healthcare industry and the capital markets. The 2020 Westpu Conference Health Industry Capital Summit was held as scheduled at the Boao Forum for Asia Hotel. Centered on “Industrial Development and Investment Trends,” the summit brought together business leaders, investors, and industry experts to comprehensively explore the collaborative development path of China’s pharmaceutical and healthcare industry and capital against the backdrop of “healthcare industry dimension upgrading.”

The Capital Summit focused on in-depth analysis and interpretation of major policies in the pharmaceutical and healthcare sector, a comprehensive review and outlook of the industry landscape, and policy reforms in the capital market. Distinguished experts and investors engaged in open dialogue, sparking a vibrant exchange of ideas.

The Impact of the Chinese Pharmacopoeia 2020 on the Pharmaceutical and Healthcare Industry

Zhang Wei, former Secretary-General of the Chinese Pharmacopoeia Commission, outlined the impact of the 2020 edition of the Chinese Pharmacopoeia on the pharmaceutical and health industries. Following the implementation in 2019 of the newly revised Drug Administration Law, Vaccine Administration Law, and Measures for the Administration of Drug Registration, China’s pharmaceutical sector witnessed another major policy upgrade in 2020 with the official promulgation of the new edition of the Chinese Pharmacopoeia in July. The Chinese Pharmacopoeia establishes quality and specification standards for drugs and their components; together with the standards issued by the National Medical Products Administration (NMPA) and the approved drug registration standards, it constitutes the national drug standards.

Zhang Wei, Former Secretary-General of the Chinese Pharmacopoeia Commission

While ensuring drug quality and safeguarding the baseline of safety, the Chinese Pharmacopoeia establishes scientific and reasonable standards in line with the development level of the pharmaceutical industry, thereby eliminating outdated production capacity, promoting supply-side structural adjustment, and driving overall improvements in quality and technical standards across the pharmaceutical sector. Standards serve as the foundation for innovation, which in turn generates new standards. The Chinese Pharmacopoeia Commission and other health authorities encourage leading enterprises to benchmark against original research standards and align with advanced international standards, so as to enhance drug quality and facilitate China’s transition from a major pharmaceutical producer to a pharmaceutical powerhouse.

The 2020 edition of the Chinese Pharmacopoeia added 319 monographs and revised 3,177, bringing the total number of included items to 5,911. In response to the national volume-based drug procurement programs implemented over the past two years, the new edition has made corresponding adjustments by aligning with international standards for originator drugs and strengthening impurity control. Examples include the export inspections of active pharmaceutical ingredients (APIs) triggered by N-nitrosodimethylamine (NDMA) impurities in valsartan in 2018, and the impact of NDMA impurities in metformin on centralized procurement in 2019. The timely revision and improvement of standards in the new pharmacopoeia will strongly support the consistency evaluation of quality and efficacy for generic drugs, thereby promoting their high-quality development.

In response to the relatively lagging development of China’s pharmaceutical excipients and packaging materials industry, the new edition of the Pharmacopoeia emphasizes the construction of standards systems in these two areas, encouraging and guiding the rapid growth of excipient and packaging material enterprises to match the high-speed advancement of drug research and development in China. The new edition places importance on comparative studies with pharmacopoeias from multiple countries, focusing on international harmonization and convergence of standards, which helps eliminate barriers to import and export trade in pharmaceuticals and promotes the internationalization of China’s pharmaceutical industry.

The Long-Term Impact of New Healthcare Reform Trends on the Structure of the Big Health Industry

Professor Cai Jiangnan, Founder and Executive Chairman of the Shanghai Chuangqi Health Development Research Institute, outlined the long-term impact of new healthcare reform trends on the health industry. Over the past four decades of reform and opening-up, China’s medical and health industry has achieved sustained development. Per capita health expenditure in China rose from RMB 12 in 1978 to RMB 4,148 in 2018, with particularly rapid growth observed after 2000.

The share of health expenditure in GDP rose from 3.0% in 1978 to 6.6% in 2018. Although the health industry has achieved substantial overall growth and healthcare reforms have continued to advance, numerous areas still require improvement.

Cai Jiangnan, Founder and Executive Chairman of the Shanghai Chuangqi Health Development Research Institute

In the healthcare services sector, there is an inverted distribution between the number of medical institutions at various levels and patient resources, resulting in a “medical inverted triangle,” wherein tertiary hospitals, though fewest in number, receive the largest share of patient resources. Medical resources and services continue to concentrate in large hospitals; compared with 2009, when the new healthcare reform was launched, outpatient visits and hospital admissions at tertiary hospitals increased by 169% and 248%, respectively, in 2018—far exceeding the growth rates of other hospitals. The tiered diagnosis and treatment system has not yielded significant results, and primary care has failed to play its intended role in diverting patients.

As the central figures in the healthcare system, doctors in China number approximately 18 per 10,000 people. This figure is lower than that of developed countries but leads among developing nations. However, the educational attainment of Chinese physicians is less than satisfactory, with 45% holding qualifications below a bachelor’s degree. Since academic promotion of innovative drugs and medical devices targets physicians, and their clinical application relies on physicians, the professional competence of doctors significantly influences the development of innovative pharmaceuticals and medical technologies.

Among the three pillars of China’s healthcare reform, the medical services sector still has considerable room for improvement, whereas significant progress has been achieved in recent years in the pharmaceuticals and health insurance sectors. Regulatory reforms by the National Medical Products Administration (NMPA)—such as strengthened verification of clinical trial data, priority review, conditional approval, acceptance of overseas clinical data, and the implementation of the Marketing Authorization Holder (MAH) system—not only resolved the backlog in drug review and approval but also spurred rapid growth in both innovative drug R&D projects and the number of marketed drugs in China. In terms of health insurance, volume-based procurement organized at the national level for generic drugs and high-value consumables, coupled with negotiations to include innovative drugs in the National Reimbursement Drug List (NRDL), have shifted the focus from aggregate cost containment to structural optimization. This approach has enhanced quality and efficiency while minimizing additional expenditure.

Although healthcare reform has made significant progress in the areas of pharmaceuticals and health insurance, these changes have not fundamentally transformed medical services. For instance, they have failed to address the issue of physician compensation and have not truly achieved the “three-medical linkage” (the coordinated reform of medical care, health insurance, and pharmaceuticals). Future healthcare reforms need to place greater emphasis on reforming supply-side stakeholders, such as physicians and public hospitals, while simultaneously shifting from a disease-centered model to a health-centered one, with a stronger focus on health management and disease prevention.

Overview of the Global Innovation Pipeline and Outlook for China

Gang Wang, Chief Scientist for Greater China in the Life Sciences and Pharmaceuticals division of Clarivate, presented an overview of the global innovation pipeline and outlook for China. Globally, the innovative drug industry is characterized by three fundamental trends: accelerated R&D innovation, regulatory frameworks that keep pace with scientific advancements, and a focus on rare diseases.

Wang Gang, Chief Scientist of Clarivate’s Life Sciences and Pharmaceutical Business Unit in Greater China

The application of new technologies, such as DNA-encoded library (DEL) compound libraries for drug screening and AI-assisted drug design, has accelerated the pace of research and development. Technological breakthroughs in innovative drugs are emerging continuously, exemplified by PROTACs overcoming the challenge of targeting previously “undruggable” proteins like KRAS, while cell and gene therapies are advancing rapidly. These technological advances have outpaced existing regulatory frameworks, prompting timely updates to regulations. As drugs targeting common therapeutic areas and well-established targets become increasingly prevalent, the development of superior therapeutics is becoming more challenging. Consequently, the rare disease sector, which still harbors substantial unmet clinical needs, has become a focal point of intense interest for pharmaceutical companies.

From 2013 to 2019, the number of innovative drugs launched globally each year remained relatively stable at approximately 50–60. In 2019, a total of 56 new drugs were approved worldwide, with oncology therapies accounting for the largest share (13 approvals), while only three new drugs were approved for the treatment of infectious diseases. Most infectious diseases are typically acute and non-life-threatening, and the clinical applications for drugs targeting drug-resistant infections are quite limited. These factors have made it difficult to achieve high returns on investment for anti-infective drug development, thereby dampening R&D enthusiasm. The global COVID-19 pandemic has reversed this trend, renewing the industry’s focus on the development of anti-infective therapies.

From 2013 to 2018, the proportion of newly approved drugs led by large multinational corporations (MNCs) steadily declined. Small and medium-sized enterprises (SMEs), being more focused and flexible, were able to accelerate their R&D processes. Furthermore, global policies encouraging the development of orphan drugs helped improve the success rates and time-to-market for SMEs’ R&D efforts. In 2019, the share of newly approved drugs led by large MNCs saw a significant increase, likely because MNCs acquired R&D assets from SMEs through transactions, continued their development, and brought them to market.

In the global distribution of newly added drug pipelines from 2018 to 2020, China surpassed Europe (<2,000 items) and Japan (<500 items) with more than 2,000 new pipeline assets, while the United States maintained an absolute leading position in the first tier with approximately 4,500 items. Regarding the ratio of newly added small-molecule drugs to biologics, the proportions in the United States, Europe, and Japan were all close to 1:1. In contrast, due to its accumulated expertise in small-molecule drug development and relatively lower technical barriers, China’s number of small-molecule drugs significantly exceeded that of biologics.

Turning to global biopharmaceutical financing, although the industry often speaks of a “capital winter,” the COVID-19 pandemic has spurred the development of companies involved in the R&D and manufacturing of epidemic prevention supplies, diagnostic reagents, biological products, and COVID-19 vaccines, causing the sector to leap directly from deep freeze to scorching summer. As of early August 2020, global biopharmaceutical financing reached $81.26 billion, far exceeding the full-year 2019 total of $35.42 billion. In terms of U.S. venture capital distribution by therapeutic area, oncology firmly held the top spot from 2003 to 2018; a notable shift in 2018 was that venture capital investment in technology platforms rose to third place.

The Impact of the Registration-Based IPO System Reform on the ChiNext Board on the Investment Market

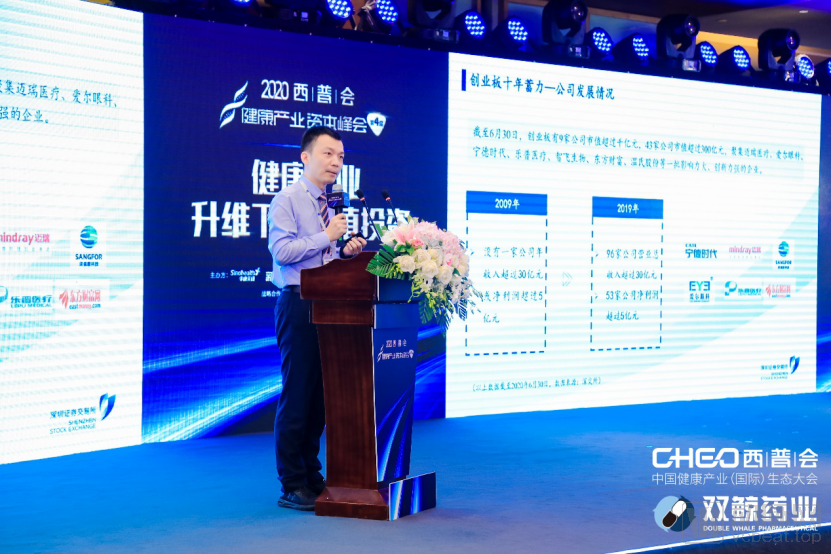

Zheng Wencai, Deputy Director of the South China Regional Office of the Listing Promotion Department at the Shenzhen Stock Exchange, provided an overview of the reforms to the ChiNext board and the pilot registration-based IPO system. His presentation covered the decade-long development and reform of ChiNext, listing review and registration, issuance and underwriting, ongoing supervision, and trading mechanisms. Established in 2009, coinciding with the launch of China’s new healthcare reform, ChiNext has played a significant role in facilitating economic transformation and upgrading over the past ten years. Companies listed on ChiNext have raised RMB 430 billion through initial public offerings (IPOs), with total equity financing reaching RMB 1.0487 trillion. This has provided vital exit channels for venture capital firms and directed substantial social capital toward innovative startups. Statistics show that approximately 500 ChiNext companies received venture capital support prior to their listings, amounting to a cumulative total of around RMB 40 billion.

Zheng Wencai, Deputy Director of the South China Region, Listing Promotion Department, Shenzhen Stock Exchange

The ChiNext board primarily serves growth-oriented innovative and entrepreneurial enterprises, supporting the deep integration of traditional industries with new technologies, new industries, new business formats, and new models, which includes small innovative biotechnology companies. The positioning of the ChiNext board is distinct from that of other market segments, fostering differentiated development to create a virtuous cycle of complementarity and mutual promotion, thereby jointly enhancing the capital market’s ability to serve the real economy and technological innovation, including the innovative drug industry.

On June 12, 2020, the reform of the ChiNext board and the pilot registration-based IPO system were officially implemented. The most significant feature of the registration-based system is that regulatory authorities conduct compliance reviews of application documents submitted by issuers and intermediaries, without assessing the companies’ profitability. Based on full information disclosure, investors independently evaluate corporate value and risks to make their own investment decisions. This has paved the way for early-stage small biotechnology firms to secure financing.

Policy Changes in China's Capital Market and Their Impact on Investment in the Pharmaceutical and Healthcare Industry

Cheng Jie, Managing Director of CITIC Securities and Head of the Healthcare Industry Group within the Investment Banking Management Committee, introduced reforms in China’s capital market policies and their impact on investment in the pharmaceutical and health industries. Since April 2018, when the Hong Kong Stock Exchange amended Main Board Listing Rule 18A—emulating the U.S. NASDAQ—it has allowed pre-revenue, pre-profit biotechnology companies to file for initial public offerings, thereby providing a financing channel for innovative drug developers in urgent need of substantial R&D funding.

Cheng Jie, Managing Director of CITIC Securities and Executive Head of the Healthcare Industry Group under the Investment Banking Management Committee

Following the implementation of Chapter 18A by the Hong Kong Stock Exchange, Ascletis Pharma became the first company to take this pioneering step. It was subsequently followed by BeiGene, CStone Pharmaceuticals, CanSino Biologics, Henlius, and others. By the end of July 2020, a total of 18 unprofitable biotechnology companies had listed on the Hong Kong stock market, eight of which closed below their IPO prices on July 31, 2020.

A characteristic feature of biotechnology companies listed on the Hong Kong Stock Exchange is strong initial post-IPO performance, followed by a decline due to insufficient R&D data or delayed product launches. As early speculative capital exits, stock prices fall further. In contrast, companies with robust R&D data and product portfolios—such as Innovent Biologics, Junshi Biosciences, Henlius, and BeiGene—closed at prices higher than their IPO prices on July 31, 2020, to varying degrees. CanSino Biologics, driven by its leading-position adenovirus-vector COVID-19 vaccine concept, saw this ratio exceed 12.

Although the Hong Kong Stock Exchange’s Chapter 18A rules have relaxed listing restrictions, the degree of leniency remains insufficient. In particular, the requirement that biotechnology companies must have at least one core product that has progressed beyond the conceptual stage to demonstrate profit potential is stringent. Additionally, companies must have secured substantial third-party investment from at least one sophisticated investor at least six months prior to the proposed listing date, with such investment remaining in place until the initial public offering (IPO), which serves as an endorsement.

In 2019, the STAR Market was established, introducing five sets of listing standards that further relaxed listing requirements. For instance, Standard V stipulates an estimated market capitalization of no less than RMB 4 billion; major businesses or products must have achieved phased results, and pharmaceutical companies are required to have at least one core asset approved to initiate Phase II clinical trials. This demonstrates that the STAR Market has set relatively reasonable thresholds while accelerating the development of pharmaceutical enterprises of a certain scale.

Investment Opportunities in the Context of the Upgraded Development of China’s Pharmaceutical and Healthcare Industry

As public health concepts shift from a treatment-centric model to full-lifecycle health management emphasizing prevention, treatment, and rehabilitation, China’s pharmaceutical and healthcare industry has gained development opportunities across all segments and dimensions. Against the backdrop of this industrial upgrading and driven by the COVID-19 pandemic, various subsectors have exhibited distinct development characteristics and investment opportunities.

1. The global antibody drug market has experienced rapid development, reaching $129 billion in 2019, whereas the Chinese market remains relatively limited at only RMB 27.9 billion. Nevertheless, the number of antibody drug applications in China continues to grow rapidly, indicating substantial potential for market expansion.

2. Traditional large pharmaceutical companies (“big pharma”) tend to have lower valuations relative to innovative biotechnology companies (“biotech”). However, once a blockbuster drug is successfully developed, they can rapidly scale up commercialization by leveraging their accumulated resources, as exemplified by Sino Biopharmaceutical and Hengrui Medicine. Big pharma companies with rich and well-structured R&D pipelines also represent attractive investment opportunities.

3. In the medical device sector, domestically produced mid-to-high-end medical equipment has benefited from import substitution and expansion into primary healthcare markets, while the market for home-use medical devices related to chronic diseases is experiencing rapid growth driven by consumption upgrades.

4. Early screening, diagnosis, and treatment of cancer are critical strategies for transforming cancer into a chronic disease within the next 5–10 years. Leading enterprises in comprehensive, lifecycle cancer management will enjoy broad development prospects.