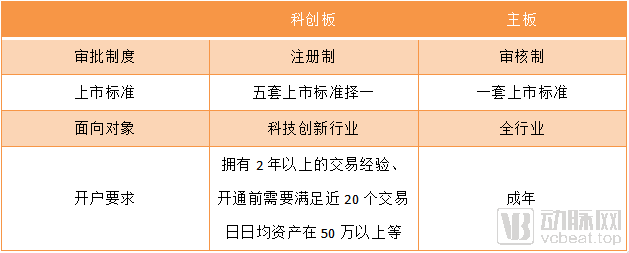

Sci-Tech Innovation Board Propels Medical Industry Forward with Over RMB 900 Billion Market Cap and 41 Breakthrough Enterprises

Unlike fast-moving consumer goods, finance, and food service, healthcare is a “slow” industry. From inception to initial public offering, a healthcare company must withstand tests related to products, policies, and technology. This is particularly true in the two subsectors of drug development and high-end medical device manufacturing, where the entire process—from product design and clinical trials to regulatory approval and market launch—often spans several years. Risks such as product iteration challenges, clinical trial failures, and market uncertainties are prevalent; any one of these risks alone can deplete a startup’s cash flow and lead to its demise.

Therefore, to develop the healthcare industry and encourage competition between emerging enterprises and established companies, it is essential to allow them a certain degree of tolerance for trial and error, enabling them to recover from setbacks when facing risks. However, the stringent market access requirements of China’s A-share market have previously forced many companies with R&D achievements but lacking market data to seek overseas listings. After all, innovative pharmaceutical companies have relatively weak risk resilience and limited financing channels in the primary market; consequently, some have begun to pursue listings on the Hong Kong or U.S. stock markets, where market access requirements are relatively more lenient.

The emergence of the STAR Market has provided a solution to this problem. By introducing capital and enhancing liquidity, small and medium-sized pharmaceutical and medical device companies can adopt a longer-term perspective and engage in more strategic product line planning. Meanwhile, in today’s increasingly intensified geopolitical landscape, retaining top talent and technology within China holds significant strategic value.

More than a year has passed since the launch of the STAR Market, whose establishment has brought about earth-shaking changes to the healthcare industry. Nevertheless, which enterprises have benefited from this development? To what extent have these companies transformed? And where is the STAR Market headed in the future? Perhaps only by delving deeply into data can we find answers to these questions.

As of August 15, 2020, more than 150 stocks had been listed on the STAR Market, with none trading below their initial public offering (IPO) price. The 41 constituent stocks focused on the healthcare sector also demonstrated remarkable performance. Among them, 3SBio Inc., which recorded the smallest price increase relative to its IPO price, was trading at 1.38 times its offering price. Meanwhile, Orient Gene Biotech saw its share price surge by 854% above its IPO price (peaking at 1,060%). The average price increase across the entire sector reached as high as 306.4%.

According to data from Choice, the total market capitalization of these 41 stocks has reached RMB 929.4 billion, with an average market cap of RMB 22.6 billion per company. The free-float portion accounts for approximately one-tenth of each company’s total market value. To date, the market capitalization of certain STAR Market companies has approached the average level of A-share companies.

Let us further examine the price-to-earnings (P/E) ratio, an indicator used to assess the reasonableness of stock price levels. Excluding five unprofitable companies—Bio-Thera Solutions, Junshi Biosciences, Zelix Pharmaceuticals, Tinavi Medical Technologies, and SinoCellTech—the remaining 34 enterprises show a static P/E ratio ranging from a low of 54.0 for Xiangsheng Medical to a striking high of 1,365.84 for Chipscreen Biosciences. Overall, nearly half of these companies have static P/E ratios falling within the 100–200 range, with a median value of 122.4. In comparison, as of March 2020, the average P/E ratios for the Shanghai Composite Index and the CSI 300 Index were in the 11–12 range, while those for the Dow Jones Industrial Average and the S&P 500 reached 16.

However, for the STAR Market as a new testing ground, the initial surge was not irrational. He Bingyu, an analyst at Zhongtai Securities, stated: “In the past, the valuation digestion period for new listings was around two years. Since the equity interests of certain shareholders of companies listed on the STAR Market are frozen and not subject to reduction, various metrics tend to be relatively higher.”

Therefore, although all stocks on the STAR Market have thus far demonstrated strong performance across key metrics, these indicators will eventually revert to a reasonable range over time, and the relative strengths and weaknesses of individual stocks will become more clearly differentiated.

Grouping the aforementioned 41 companies by region and core business also yields some interesting findings.

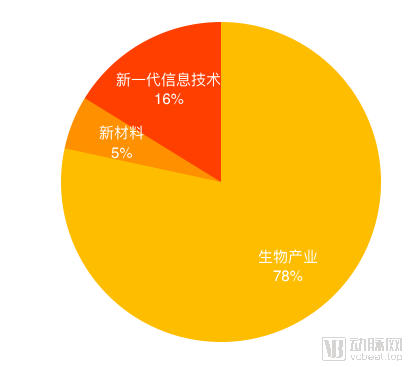

According to the industrial classification outlined in the "Classification of Strategic Emerging Industries," only two companies—Haohai Biological Technology and Bloomage Biotechnology—are categorized under new materials. Six companies fall under next-generation information technology, while the remaining 33 are classified within the bio-industry sector. Notably, among the six companies in the next-generation information technology sector, only Shanda Dadiwei and Zeda Yisheng have established a substantial presence in healthcare, with related businesses accounting for a significant share of their total revenue. The other four companies primarily provide data security solutions across various industries; although they have healthcare-related operations, these remain relatively marginal.

Industrial Distribution of Healthcare Companies on the STAR Market

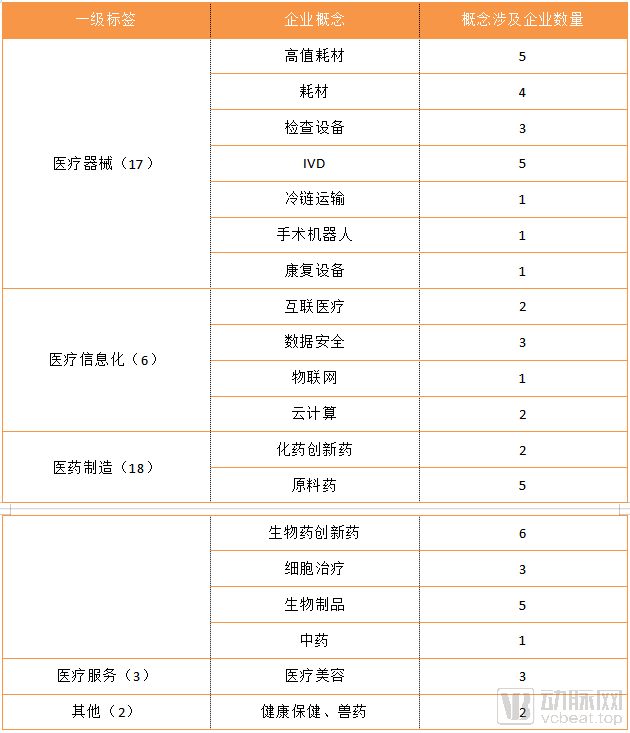

However, the classification of strategic emerging industries has certain limitations in terms of business scope. For instance, companies such as Haohai Biological Technology and Bloomage Biotechnology also fall under the category of pharmaceutical manufacturing, with their medical aesthetics operations classified under new materials representing only one segment of their business. Therefore, VCBeat reviewed the specific business activities and conceptual classifications of 41 companies and re-categorized them accordingly.

Categorization of the 41 companies on the STAR Market based on corporate concepts

Note: Some enterprise tags are duplicated.

To encourage more high-value enterprises to go public, the STAR Market allows companies to list under the fifth set of listing criteria. Specifically, even if a company is not yet profitable, it may apply for registration on the STAR Market as long as it meets the following requirements: “an estimated market capitalization of no less than RMB 4 billion; and at least one core product has been approved to enter Phase II clinical trials.” This listing standard is virtually tailor-made for innovative drug developers. Nevertheless, only a handful of companies have gone public via this route, with just five firms—including Junshi Biosciences and Bio-Thera Solutions—listing on the STAR Market under the fifth set of criteria.

Nevertheless, innovative drugs and medical devices have remained the biggest beneficiaries since the launch of the STAR Market. Since the reform of innovative drugs and medical devices began in 2015, the domestic market has undergone significant changes. China’s accession to the ICH, global acceptance of clinical data, and the shift from an approval-based to a filing-based system for clinical trial registration are among the many factors driving the rapid development of innovative drugs and medical devices in China. According to Yu Wenxin, an analyst at Haitong Securities, this trend is expected to continue for at least the next three to five years.

Data shows a significant increase in the number of pharmaceutical companies listed on the STAR Market after 2020, with all five “A+H” dual-listed concept stocks centered on pharmaceutical manufacturing. Among these 18 companies, those engaged in innovative biologics, active pharmaceutical ingredients (APIs), and biological products are the most numerous. The emergence of COVID-19 has indirectly accelerated the development of pharmaceutical manufacturing enterprises.

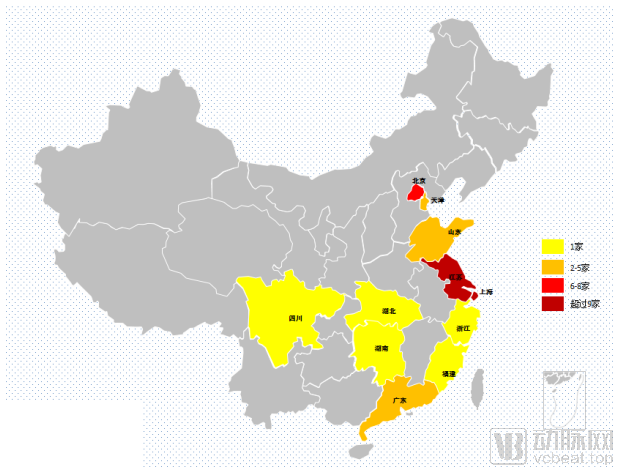

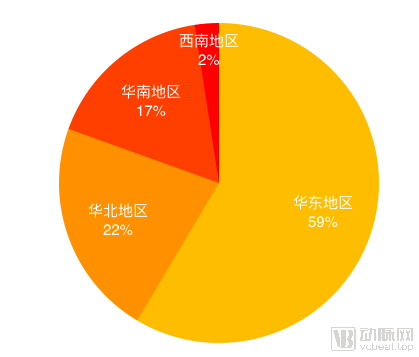

In terms of geographic distribution, Shenzhen, renowned for its high-tech industry, failed to secure Guangdong Province the top spot for the highest number of healthcare companies listed on the STAR Market. Instead, Shanghai and Jiangsu Province took the lead, each producing more than nine listed companies. Beijing followed closely with six listed companies; Guangdong had five; Shandong and Tianjin each had three; while Fujian, Hubei, Hunan, Zhejiang, and Sichuan each had one company listed.

Geographic Distribution of STAR Market Healthcare Companies

The industrial distribution map provides a clearer view of the landscape of the high-tech medical technology industry, with the overall trend shifting toward East China. The Yangtze River Delta region has undoubtedly made significant efforts in this regard; leveraging its industrial park advantages and policy support, numerous pharmaceutical and medical device companies have established operations in Zhangjiang, Pudong, and the Northern Jiangsu Industrial Park.

Taking Jiangsu’s BioBAY as an example, this industrial park was established with government support to integrate the upstream and downstream segments of the biotechnology supply chain within the park. It has set up BioTOP, a smart platform offering services such as financing and independent third-party analytical testing, and has partnered with enterprises like Xinjianyuan Holding Group to establish funds, further addressing the capital needs of companies within the park.

Geographic Distribution of STAR Market Healthcare Companies

In contrast, the development of medical technology in western China has been relatively sluggish, with HitGen, a CRO company based in Sichuan, standing as the sole flagship enterprise in the entire region. This situation is also partly attributable to the uneven development of the healthcare industry.

Yu Wenxin believes that policy implementation and support from regional governments are key drivers behind the growth of medical enterprises in these areas. “Many factors influence the distribution of listed companies, with industrial park planning and construction being one of them. Shanghai Zhangjiang High-Tech Park and Suzhou Industrial Park have nurtured numerous medical industry clusters, which streamline and expand resources for individual companies. Coupled with policy subsidies supporting the innovative drugs and medical devices sector, it is no surprise that these two regions have produced so many companies listed on the STAR Market. However, due to the short time frame involved, these figures do not fully reflect the current state of regional development in China’s high-tech medical sector. Medical industrial parks and policies in Beijing, Shenzhen, Wuhan, and Chengdu are also highly prominent, but it will take more time for their impact to materialize.”

While no definitive conclusions have been reached, factors such as regional atmosphere, industrial clustering, and policy support indeed play a significant role in driving the development of medical technology capabilities. If western regions aim to accelerate the advancement of related technologies, they require more than just policy incentives, funding, and corresponding healthcare infrastructure construction; the cultivation of relevant talent must also be expedited.

Prior to the establishment of the STAR Market, the Hong Kong Stock Exchange and NASDAQ were the preferred choices for many innovative pharmaceutical and medical device companies, while information technology firms were keen on listing on the New Third Board. Within one year of the STAR Market’s launch, this landscape underwent a certain degree of change.

Let us first discuss the informatization sector. To date, all six companies listed on the STAR Market had previously been listed on the New Third Board, possessing certain IPO experience; however, no new enterprises have directly entered the STAR Market. This indicates that in recent years, a new batch of informatization companies still remains some distance away from going public.

He Bingyu told VCBeat, “In 2015 and 2016, the concept of the New Third Board was at its peak. At that time, there were rumors that companies listed on the New Third Board would have the opportunity to transfer to the main board after several years. Therefore, many IT companies that did not meet the listing requirements for the Shanghai or Shenzhen stock exchanges jumped on the bandwagon and listed on the New Third Board, hoping to use it as a springboard.”

Regarding the lack of new enterprises, he noted that the healthcare informatics market is highly fragmented. Apart from leading companies, a significant share is held by small local informatics firms. While these companies are able to survive, their limited scale and growth prospects do not meet the listing requirements of the STAR Market.

“Although the industry is fragmented, businesses in mainstream sectors—such as Hospital Information Systems (HIS), Picture Archiving and Communication Systems (PACS), electronic medical records, and anesthesia information management systems—are already quite mature. With limited room for incremental growth, it is difficult for new companies to emerge as strong contenders. Meanwhile, next-generation enterprises focused on AI and Clinical Decision Support Systems (CDSS) are struggling to generate sufficient revenue, leading to valuation concerns. This is the primary reason for the current situation.”

Nevertheless, a small number of companies still have the potential to list on the STAR Market, with Yidu Cloud, Senyi Intelligence, Huimei Technology, and Jiahe Meikang being among the leading candidates. Therefore, from the current perspective, the timing for IPOs in the healthcare informatics sector is not yet fully mature. As initiatives such as smart hospital development, medical consortiums, and accreditation-related infrastructure construction continue to advance, a new generation of informatics enterprises may witness a peak in IPO activity.

Turning to pharmaceutical and medical device companies. Data from the STAR Market shows that the cumulative fundraising amounts of listed companies range from RMB 300 million to RMB 3 billion. Among them, 23 companies raised less than or equal to RMB 1 billion; 8 companies raised between RMB 1 billion and RMB 3 billion; and only three companies raised more than RMB 3 billion (two raised RMB 3.1 billion each, and one raised RMB 5.2 billion). Kangxinuo, which recently went public, stands out with an initial fundraising of RMB 5.2 billion, becoming the company with the highest fundraising amount in the healthcare sector on the STAR Market.

Medical device manufacturers with relatively short R&D cycles and more stable revenue streams have long been a major focus of domestic investment, a trend that is also reflected on the STAR Market. Data show that the STAR Market has provided effective financing opportunities for many small- and medium-sized medical device companies. While firms specializing in high-value consumables and in vitro diagnostics (IVD) previously often chose to list in Hong Kong, the STAR Market has kept a large number of such enterprises within the A-share market.

Overall, the establishment of the STAR Market has, to some extent, facilitated the repatriation of capital. Many companies that had initially planned to list on NASDAQ or the Hong Kong Stock Exchange have shifted their strategies and turned to the STAR Market for financing. Furthermore, as mentioned above, numerous companies already listed in Hong Kong have not abandoned the STAR Market as a source of capital, opting instead for dual listings in both Hong Kong and mainland China’s A-share market. Among them, Junshi Biosciences has traversed three platforms—the New Third Board, the Hong Kong Stock Exchange, and the A-share market—maximizing its access to funding.

Answering this question is not difficult; an analysis of the company’s first-quarter financial report reveals some clues.

Comparison of Q1 Revenue and R&D Expenditure for STAR Market Healthcare Companies (Data Source: Choice)

As shown in the table above, among the 36 companies with complete data, only 14 experienced a decline in revenue during the first quarter. The remaining 22 companies did not halt their development due to the pandemic and achieved varying degrees of revenue growth, with top performers recording year-on-year revenue increases exceeding 100%.

Unlike other sectors, technology companies require continuous R&D investment before generating substantial financial revenue; therefore, R&D expenditure data serves as an indicator of a company’s technological sophistication. Among the 40 companies with comparable data in the table above, only five reported a slight decline in R&D spending, while the remaining 35 demonstrated growth. Specifically, the average R&D investment per company in the first quarter of 2020 was RMB 23.465 million, representing a 13.54% year-on-year increase compared to 2019. Thus, for healthcare companies listed on the STAR Market, the pandemic did not have a significant negative impact on the industry; on the contrary, some companies accelerated their R&D and commercialization processes as a result.

Net profit also reflects this trend to some extent. Data show that the metric rose for 23 companies and declined for 15, with the overall performance outperforming that of the Main Board.

Therefore, even during the pandemic, market fluctuations did not significantly impact companies in the healthcare sector listed on the STAR Market. Today, stock prices have rebounded across both the Main Board and the STAR Market, reflecting to some extent the overall strong fundamentals of companies listed on the STAR Market.

In addition to rigorous financial data and corporate information, we have also identified non-real-time metrics such as employee compensation and headcount, aiming to provide an indirect portrayal of the current status of companies listed on the STAR Market.

Among the 32 STAR Market-listed healthcare companies with publicly available data, 14 reported chairman compensation of less than RMB 1 million. Tebao Bio offered the lowest compensation at just RMB 120,000. None of the remaining companies provided excessively high cash compensation to their chairmen; the highest was paid by Micro-Tech (Nanjing) Co., Ltd., which awarded its chairman RMB 5 million. Across the entire survey, the median compensation was RMB 1.1687 million, and the average was RMB 1.5218 million. Additionally, the median per-employee compensation at these companies stood at RMB 198,200.

In addition, we sampled 64 A-share listed companies, where the average annual compensation for chairmen was RMB 1.96 million, with a median of RMB 1.05 million, while the median annual compensation per employee was RMB 150,500.

From this perspective, companies listed on the STAR Market not only offer high salaries to executives but also provide substantial benefits to employees. Therefore, joining a STAR Market-listed company may have been a quite attractive option during the pandemic year.

Although the aforementioned data can reflect, to some extent, the current state of the STAR Market, a one-year time span is hardly substantial; the limited number of companies fails to clearly delineate the competitive advantages and disadvantages among them.

Furthermore, AI-driven enterprises and next-generation information technology firms in the medical technology sector have yet to find their place on the STAR Market, resulting in a relatively homogeneous mix of healthcare companies listed there. However, with the entry of broad-based chip manufacturers such as Cambricon and SMIC into the STAR Market, downstream AI application companies should accelerate their efforts to seize this opportunity.

Elevated valuations represent another characteristic of the current STAR Market; under such conditions, a company’s public data may not accurately reflect its intrinsic value. However, over the coming year, as shares held by institutional investors gradually become tradable, stock prices of companies with previously high P/E ratios and market capitalizations are likely to move toward more rational levels.

However, regardless of how the market evolves, the launch of the STAR Market has tangibly injected vitality into medical technology enterprises. Events such as the pandemic, new infrastructure development, and innovative medical devices have created boundless opportunities for this sector. How well companies navigate this landscape ultimately depends on their own strategies and execution.