Regional Breakthrough Strategies of Three Newly Filed IPO Eye Care Chains Amid Aier Eye Hospital's Dominance

Amid the rising tide of privately operated healthcare, Aier Eye Hospital stands as one of the most prominent and shining waves.

Not to mention its 30-fold surge over the decade since its listing on the ChiNext board, which has brought its current market capitalization to nearly RMB 200 billion, the intense industry discussion it has sparked has remained consistently high. Don’t believe it? A Baidu search for “Where is the next Aier Eye Hospital?” yields approximately 712,000 results.

Everyone hopes to see the next Aier Eye Hospital emerge. For instance, whenever a specialized medical institution goes public or secures financing, Aier Eye Hospital is frequently cited by media outlets and investment firms as a benchmark for comparison.

However, over the past decade, no other private specialized healthcare enterprise has demonstrated such stable and outstanding performance as Aier Eye Hospital. Taking “golden eyes and silver teeth”—a phrase referring to the high-quality segments of ophthalmology and dentistry in the private specialized healthcare sector—as an example, Topcare Medical, a leading player in the dental field, has only established a chain network within Zhejiang Province, whereas Aier Eye Hospital has achieved nationwide coverage across China and expanded its operations to Europe and the United States. Although significant differences exist among various market segments, making direct comparisons inappropriate, these indicators nonetheless underscore Aier Eye Hospital’s leading position in the specialized healthcare chain sector.

Turning our attention back to the sector of ophthalmology chains, Aier Eye Hospital stands in a league of its own. Its total number of clinics is far ahead, leaving other ophthalmology chains struggling to keep pace. The “first wave” has already crossed the horizon; do the “next wave” players in the ophthalmology chain market (with “waves” defined by market size rather than founding date) still have opportunities?

Let’s keep you in suspense for now; this is what the main text will discuss.

Many investors and healthcare professionals invariably mention Aier Eye Hospital when discussing specialized medical institutions. Are they merely discussing this company?

No. For instance, the ChiNext board recently accepted IPO applications from three private ophthalmic hospital groups. The news sparked considerable buzz within the industry, with Aier Eye Hospital once again becoming a frequently mentioned topic.

What are people discussing at this time?

First, whether the ophthalmic medical services sector can still produce more companies with market capitalizations of tens of billions, or even hundreds of billions.. As the saying often goes in the investment community, the Pacific Ocean is vast enough to accommodate numerous aircraft carriers. According to the “In-Depth Report on the Ophthalmology Industry” released by VBInsight, the ophthalmic medical services market, which constitutes the largest segment of the ophthalmology market, is valued at approximately RMB 124 billion. In a large and dynamic market, besides the share captured by Aier Eye Hospital, the industry leader, nearly three-quarters of the market remains unconsolidated. For other ophthalmic chain enterprises, whether they can successfully replicate Aier Eye Hospital’s growth trajectory and compete on par with it has always been a key concern within the industry.

Second, whether more new business models will emerge among ophthalmic chain enterprises.As is well known, the core of Aier Eye Hospital’s chain expansion lies in its tiered diagnosis and treatment system. Within this structure, Aier’s Tier 1 hospitals focus primarily on academic research, Tier 2 hospitals serve as the main operational hubs, Tier 3 hospitals facilitate two-way patient referrals between upper and lower tiers, and Tier 4 hospitals reach deep into grassroots communities, thereby forming a relatively complete closed loop for both clinical care and expansion. If another ophthalmic chain giant emerges, will it follow Aier Eye Hospital’s model, or will a new model arise?

Third, what trends will the ophthalmic services sector evolve toward under the current competitive landscape?The larger the market size, the more participants enter, and the fiercer the competition becomes. The current state of the ophthalmic services sector is that most eye hospitals are still operating on a regional level. As more companies go public in the secondary market, raise additional capital, and continuously expand their chain hospital networks, whether the industry will evolve into a fragmented landscape characterized by “multiple competing powers” or gradually form a structure dominated by “one superpower and several strong players” has become a topic of widespread concern.

Fourth, for investors, are there still attractive investment opportunities in the ophthalmic services sector?Over the past decade, Aier Eye Hospital’s strong performance on the ChiNext board has drawn significant investor attention to ophthalmology as a “golden track,” leading to continuous capital allocation in the sector. Although there are currently other listed “small but beautiful” ophthalmology targets besides Aier Eye Hospital, such as C-MER Eye Care (3309.HK) and EuroEyes (1846.HK), the market still anticipates the emergence of more high-quality investment opportunities.

In summary, the core concerns are the market ceiling of the ophthalmic services sector, the future direction of the industry’s competitive landscape, and what opportunities remain for other ophthalmic chains.

Let’s first examine what opportunities remain for other ophthalmology chains in the eye care services sector.

Recently, the ChiNext board has accepted IPO applications from three private ophthalmic hospital groups: Huaxia Eye Hospital, He Eye Hospital, and Purui Eye Hospital. The prospectuses of all three companies indicate that they have met the ChiNext listing requirements over the past two years, specifically achieving positive net profits with cumulative net profits of no less than RMB 50 million.

As news of the IPOs broke, the ophthalmic services sector once again came into the spotlight. The reason why three ophthalmology chain enterprises chose this particular timing for their listings,First, the listing threshold has been lowered following the implementation of the registration-based IPO system on the ChiNext board. Second, the current bull market in the stock exchange facilitates investor exits. Third, compared with the STAR Market, the ChiNext board offers better liquidity.。

In terms of business revenue, the three major ophthalmology chains primarily focus on three core services: optometry (eyeglass dispensing), refractive surgery (myopia correction), and cataract surgery. According to their prospectuses, in 2019, He Eye Hospital’s optometry services accounted for 30.07% of its main operating income, refractive surgery for 20.84%, and cataract surgery for 20.39%. For Purui Eye Hospital, optometry services represented 15.37% of main operating income, refractive surgery 45.54%, and cataract surgery 23.13%. Huaxia Eye Hospital did not provide a detailed breakdown; its prospectus indicated that ophthalmic medical services accounted for 90.04% of main operating income, while eyeglass dispensing accounted for 9.18%.

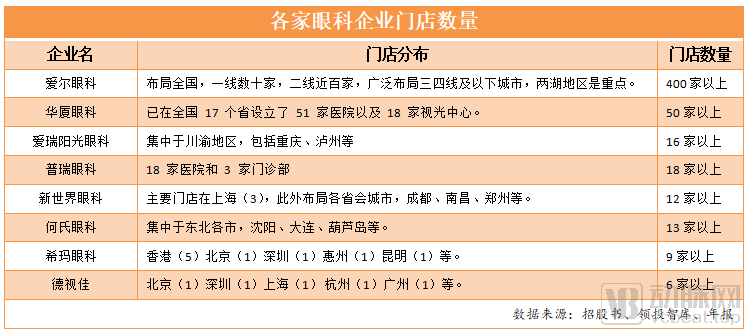

As of December 31, 2019, Huaxia Eye Hospital, founded in 2004, operated 51 ophthalmic hospitals; Purui Eye Hospital, established in 2006, had 18 ophthalmic hospitals; and He’s Eye Clinic, founded in 2009, adopted a three-tier eye health service model, currently comprising 3 tertiary eye care institutions, 30 secondary eye care institutions, and 56 primary eye care institutions.

Interestingly,All three ophthalmic hospitals exhibit distinct regional characteristics.Huaxia Eye Hospital has deeply cultivated the Southeast region, He Eye Hospital has focused on Liaoning Province, and Purui Eye Hospital has established its base in the Southwest. Starting from their respective regional strongholds, these three ophthalmic hospital groups have now expanded their presence across China. AndFor this listing, the three companies are primarily allocating the raised funds to build new hospitals or expand existing ones.。

According to the prospectuses, He Eye Care intends to allocate half of the funds raised to the expansion project of Shenyang He Eye Hospital, as well as the establishment of new hospitals in Beijing and Chongqing. Huaxia Eye Care plans to invest its proceeds into the Tianjin Huaxia Eye Hospital project. Meanwhile, Purui Eye Care will use its funds for the construction of a new Changchun Purui Eye Hospital and the renovation of the Harbin Purui Eye Hospital.

It is not difficult to see that,The three ophthalmic hospitals have chosen an expansion path of building their own facilities, continuing to pursue the goal of expanding from regional markets to a nationwide presence in China.. The reason for expanding from specific points to the entire country,In addition to expanding market share, companies also consider the need to mitigate risks such as policy uncertainties arising from geographic concentration of their operations.。

He Shi Eye Hospital’s prospectus indicates that although the company has implemented a strategic layout nationwide, its current business operations are primarily concentrated in Liaoning Province. Future changes in laws and regulations governing medical institutions in Liaoning Province, as well as shifts in the province’s economic development, will significantly impact the company’s business operations. Should there be major adverse changes in regulatory policies in Liaoning Province, or should economic downturns lead to a decline in population, the company’s operating performance will be adversely affected.

Thus, to safeguard its core business and achieve greater growth, nationwide expansion has become the company’s optimal choice at present. In this process,Three Hospitals Will Face Management Risks Brought by Expansion. For instance, as the scale of operations continues to expand, the company will face significant challenges in resource integration, medical management, financial management, talent management, and market development. The complexity and difficulty of management will gradually increase. If the company fails to enhance its management standards and service capabilities in the future, it will have an adverse impact on its business operations.

Based on Aier Eye Hospital’s past development experience, it has also undergone a strategic transition from a regional presence to a nationwide footprint. Because for chain enterprises,Expanding into external markets will create greater growth potential for the company’s revenue. Behind this lies a significant test of the enterprise’s replicability., including management capabilities, quality control capabilities, brand capabilities, and other aspects.

Can the three ophthalmology chains that have long been deeply rooted in regional markets successfully expand beyond their regions and establish a firm foothold in the national market?

To determine whether the three major ophthalmology chains still have an opportunity to capture a share of the national market, it is essential to examine where the growth ceiling for ophthalmology chains lies.

In the healthcare industry, the adage “golden eyes, silver teeth” has seemingly become a default consensus. As the primary conduit for approximately 90% of human sensory input, vision exerts a significant impact on quality of life. Consequently, eye health has garnered widespread public attention. In medicine, ophthalmology is also a major branch of clinical medicine.

Unlike the diagnosis and treatment of general diseases, most ophthalmic conditions require surgical intervention, with only a small subset of eye diseases amenable to medical or physical therapy alone. Consequently,The market in the field of ophthalmology is primarily concentrated in medical service institutions.above. However, due to the long-standing lack of adequate development of ophthalmology within general hospitals, coupled with the relatively low proportion of ophthalmology revenue in the overall income of general hospitals, specialized eye hospitals have gained more opportunities. Among them,Private ophthalmology chains hold the most significant competitive advantage.。

This competitive landscape has emerged because, although large public specialized hospitals benefit from government endorsement and substantial equipment investment, they continue to suffer from significant issues such as poor service attitudes and long waiting times. In contrast, private ophthalmology hospital chains are more effective at attracting patients due to their heavy investment in technology, aggressive marketing strategies, flexible personnel incentives, and superior service attitudes.

Specifically,Private specialized hospital chains benefit from the economies of scale inherent in their chain operations, giving them an advantage in equipment investment.. As is well known, major ophthalmic equipment involves high costs and significant entry barriers. Therefore, for eye care service providers, adopting a chain model to amortize equipment and marketing expenses is highly feasible.

From the physician’s perspective, private ophthalmology institutions offer better career advancement pathways and higher compensation compared to public hospitals.. In private ophthalmic hospitals, doctors can not only earn higher salaries thanks to their excellent technical skills and service attitude, but also share in the dividends of the hospital’s rapid growth through partnership programs.

In terms of operational efficiency, private ophthalmology chains demonstrate higher operational efficiency.. As private ophthalmology chains are responsible for their own profits and losses and face significant operational pressures, they can offer slightly lower prices than public hospitals while providing consumers with better equipment and superior services, resulting in a distinct competitive advantage.

From a policy perspective, private ophthalmology hospitals have strong momentum for expansion.In recent years, the continuous issuance of national policies encouraging private hospitals has created opportunities for the development of private ophthalmic hospitals. In addition, public ophthalmic hospitals are constrained by staffing quotas and fiscal funding, making it difficult for them to arbitrarily open branch hospitals for expansion. Seizing this opportunity, private ophthalmic hospitals face lower barriers and have strong incentives to pursue chain operations.

Given these advantages, the chain ophthalmology sector is undoubtedly a high-quality track within healthcare services. However, after more than two decades of rapid development, has the market for chain ophthalmology services reached its peak?

From the perspective of demand,There is still significant room for growth in China's ophthalmology market, and the ophthalmic services sector will continue to expand rapidly.According to the "National Visual Health Report" released by Peking University, the incidence of cataracts among elderly people aged 60 to 89 is 80%, and it can exceed 90% in those over 90 years old. Due to the large base of cataract patients in China but a relatively low surgical rate, there is significant potential for growth in cataract surgery.

Due to modern lifestyle habits such as excessive use of electronic devices, physical inactivity, and unbalanced dietary intake, the incidence of ophthalmic diseases like dry eye syndrome and glaucoma has risen. Among these, the number of myopia patients is projected to reach 700 million by 2020. Consequently,The future market potential for ophthalmic services, coupled with the rising prevalence of eye-related diseases, forms an upward growth trajectory.。

In summary, the ceiling for the ophthalmology chain industry still has room for continued growth.

The market is substantial, and opportunities for ophthalmology chain enterprises will continue to grow. However, competition will also become more intense. Therefore, in the process of expanding from regional markets to a nationwide presence, ophthalmology chain enterprises need not only capital but also a robust moat built on technology, business models, and other key aspects.

As a pioneer in the chain ophthalmic hospital industry, while Aier Eye Hospital’s success cannot be entirely replicated, certain aspects of its experience offer valuable insights.

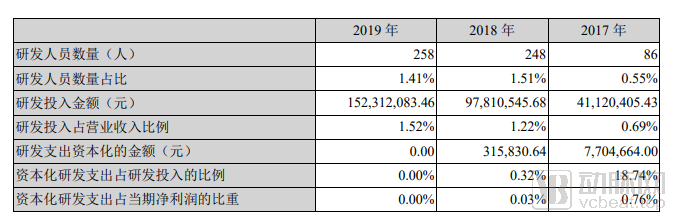

First, prioritize the research and development of medical technologies.. Although the proportion of R&D expenditure in the medical services industry differs significantly from that in other healthcare subsectors, as companies scale up, possessing unique and industry-leading medical technologies has become a critical factor for sustainable growth. According to Aier Eye Hospital’s 2019 annual report, the company has established an integrated system for medical care, education, and research comprising “three hospitals,” “seven institutes,” and “two stations,” and has founded the Aier Eye Hospital Affiliated to Wuhan University, the Aier Eye Clinical College of Wuhan University, and the Aier Eye Research Institute of Wuhan University.

Furthermore, numerous experts at Aier Eye Hospital have published academic papers in prestigious global journals. They have initiated and undertaken multiple research projects at international, provincial-ministerial, and municipal-bureau levels, achieving significant breakthroughs in national-level projects and provincial key R&D programs. Notably, Aier Eye Hospital’s integrated platform for medical practice, education, and research complements its tiered chain model, providing robust support for corporate resource synergy, group-wide medical technology assistance, and the development of talent training systems.

A comparison of the three ophthalmology chain enterprises applying for IPOs reveals that He Eye Hospital’s R&D expenditure as a percentage of revenue has declined year by year, standing at 0.22% in 2019; Huaxia Eye Hospital’s R&D intensity was 0.78% in 2019; and Purui Eye Hospital did not disclose this figure. Aier Eye Hospital’s R&D expenses accounted for 1.52% of its operating revenue in 2019, showing a year-on-year upward trend. It is evident that,Three Ophthalmology Chain Enterprises Have Not Paid Enough Attention to R&D。

(Image source: Aier Eye Hospital Group Co., Ltd. 2019 Annual Report)

Second, skillfully leverage capital instruments to ensure the company’s steady performance growth.. As a publicly listed company, particularly in the healthcare services sector, it is especially critical to strike a balance between sustaining growth in operational performance and maintaining stability in the quality of medical services. One approach adopted by Aier Eye Hospital is external incubation through merger and acquisition funds.

Specifically, since 2014, Aier Eye Hospital has cultivated eye hospitals outside its listed entity by establishing multiple merger and acquisition (M&A) funds. In 2017, Aier Eye Hospital integrated nine mature eye hospitals into the listed company. Thus, Aier Eye Hospital established a dual-drive development model of “listed company + M&A funds.” By the end of 2019, the hospitals under the M&A funds in which Aier Eye Hospital held equity interests totaled 275, with 37 outpatient clinics.

This model not only empowers Aier Eye Hospital in the management, technology, and talent development of its affiliated off-balance-sheet eye hospitals, accelerating their maturation, but also enables Aier to gain control over these hospitals once they are fully matured by repurchasing the shares of the M&A fund held by social capital or directly acquiring equity stakes held by other shareholders of the off-balance-sheet hospitals.The advantages of this model are twofold: first, it ensures the performance stability of Aier Eye Hospital Group, the listed company; second, it alleviates the financial pressure on the listed company for fundraising and expansion, thereby creating a virtuous cycle.。

Third, ample equity incentivesAt Aier Eye Hospital, technically or managerially skilled professionals with core competencies can become partner shareholders and jointly establish new hospitals with Aier Eye Hospital, including newly built, expanded, or acquired facilities. To incentivize talent, Aier Eye Hospital has implemented various incentive programs, such as equity incentives under its partnership model, to enhance management efficiency and accelerate expansion. The partnership and equity incentive plans have provided the company with a robust pipeline of hospital assets suitable for consolidation. While boosting the motivation of core talent, these initiatives also address the challenges of medical talent shortages and turnover associated with the company’s rapid expansion.

According to the prospectuses of three ophthalmology chain enterprises applying for listing,Except for Puri Eye Care, which has four employee stock ownership platforms, the other two companies currently do not have any equity incentive plans or other institutional arrangements that have been formulated or implemented.。

Based on the above analysis, it is evident that significant opportunities remain in the ophthalmic services sector. Some ophthalmic chain enterprises have reached a critical juncture in their expansion from regional to national operations. Regardless of whether any company will emerge to rival Aier Eye Hospital, the rise of an increasing number of medium-to-large ophthalmic chain enterprises has become an irreversible trend.

Therefore, for ophthalmic hospital chains, maintaining long-term competitiveness is essential to achieving greater stability in this “competition.” How can long-term competitiveness be maintained? Jiang Xiaodong, Managing Partner at Changling Capital, believes thatFirst, a company must ensure its survival by maintaining adequate cash flow; second, to sustain long-term viability, it must possess enduring value, built upon accumulated strengths in technology, management, brand, and other areas.

Specifically,Enterprises can secure profitability through a comprehensive ophthalmic diagnosis and treatment layout, then capture the high-end market with innovative products and technologies, thereby ensuring cash flow and cultivating long-term value.According to Aier Eye Hospital's 2019 annual report, the company has gradually expanded its optometry business in recent years. Focusing on medical optometry and prescription glasses, this segment covers conditions such as myopia, strabismus, amblyopia, and presbyopia, with a particular emphasis on enhancing optometry services for adolescents. This business initiative aims to broaden the reach of medical services and ensure stable corporate cash flow.

On the other hand, Aier Eye Hospital screens patients through optometry services, thereby uncovering a larger patient base for excimer laser surgery, cataract surgery, and anterior and posterior segment surgeries, achieving business synergy. Underpinning this success is Aier Eye Hospital’s accumulated technological expertise. In 2019, the revenue from its refractive surgery, cataract surgery, and optometry businesses reached approximately RMB 3.5 billion, RMB 1.76 billion, and RMB 1.93 billion, respectively (representing year-on-year increases of 25.56%, 13.97%, and 30.67% compared to 2018), with gross profit margins remaining largely stable at high levels.

The essence of healthcare lies in returning to its true purpose of saving lives and healing the wounded, as well as embracing humanistic care. Therefore, for the three ophthalmic hospitals applying for IPOs, as well as the emerging ophthalmic chain enterprises that are flourishing,Going public is not the end goal, but the starting point for becoming a great company.

We firmly believe that,As more practitioners join the field, co-opetition within the industry will become increasingly frequent., the ophthalmic chain industry will also see an influx of more “fresh capital.” And this,It will also provide patients with ophthalmic diseases more options, as well as superior medical outcomes and experiences.