New Frontiers in China's Thriving Health Insurance Market: Policy Support, Rising Health Awareness, and Integrated 'Insurance + Health Management' Innovations

In recent years, health insurance has emerged as one of the most prominent segments within the healthcare industry, driven primarily by three key factors.

First, from the perspective of social consciousness,Amid the sudden outbreak of the novel coronavirus (COVID-19) pandemic this year, health risks have garnered greater public attention.. As a result, in the first quarter of 2020, health insurance became the second-largest insurance category in the market and also emerged as the primary insurance type addressing the insurance coverage gap.

Second, from a market perspective, data from the China Banking and Insurance Regulatory Commission (CBIRC) shows that in the first quarter of 2020, the health insurance business achieved original premium income of RMB 264.1 billion, a year-on-year increase of 21.6%. Moreover,Over the past five years, statistical data shows that the compound annual growth rate (CAGR) of health insurance has been approximately 30%.。

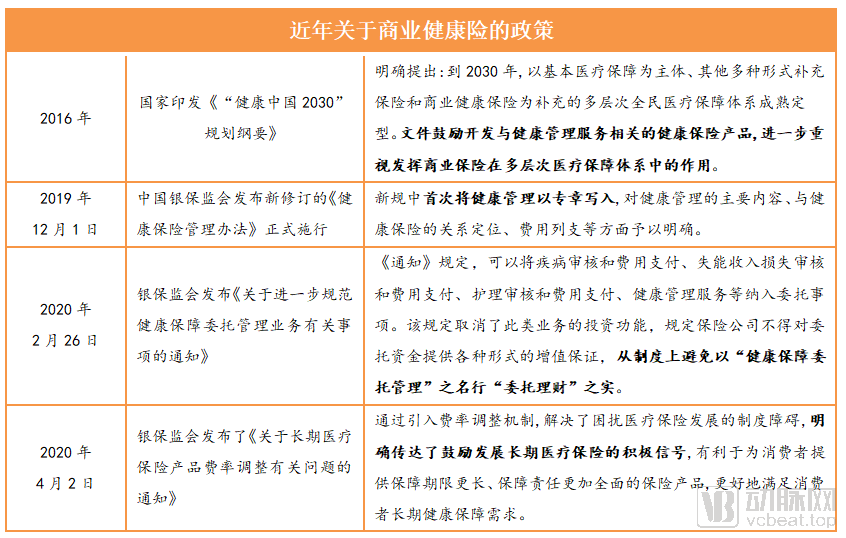

Third, from a policy perspective, since the General Office of the State Council issued the “Several Opinions on Accelerating the Development of Commercial Health Insurance” in November 2014,Policies related to commercial health insurance have been continuously improved.。

Like a speeding train, the health insurance industry has been racing along the track of rapid growth. The pain points and bottlenecks currently facing the industry are also very apparent:Health insurance has long failed to bridge the core gap between medical care and medical insurance, while its existing operational capabilities struggle to keep pace with the industry’s nearly 30% growth rate.Thus, it appears that there exists an insurmountable and ineffable bottleneck and divide between the healthcare industry and the health insurance industry. It remains uncertain when this divide and fragmentation will be bridged by policy or technology.

Looking ahead, we cannot help but ponder: What challenges remain to be addressed on the journey of the health insurance industry? Are there greater possibilities for the future?

Exploring New Models of Health Insurance: Breakthroughs and Attempts by Typical Institutions

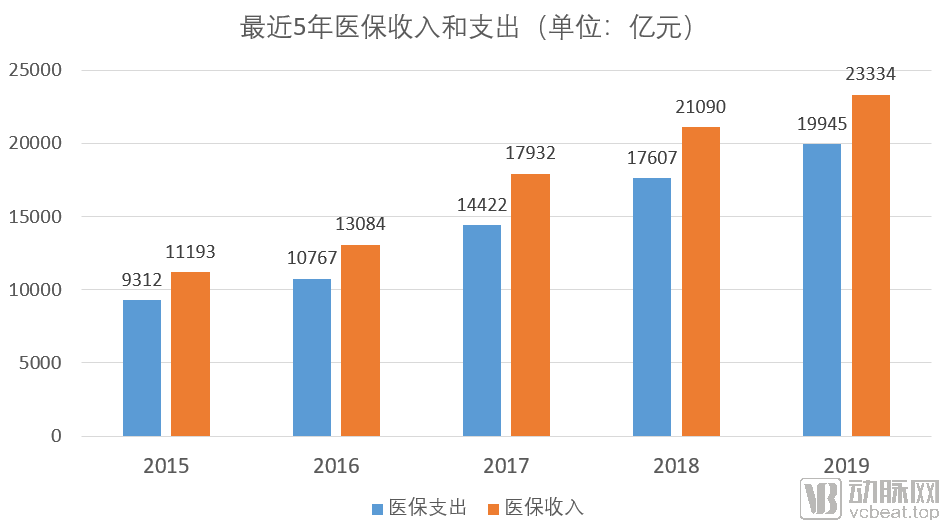

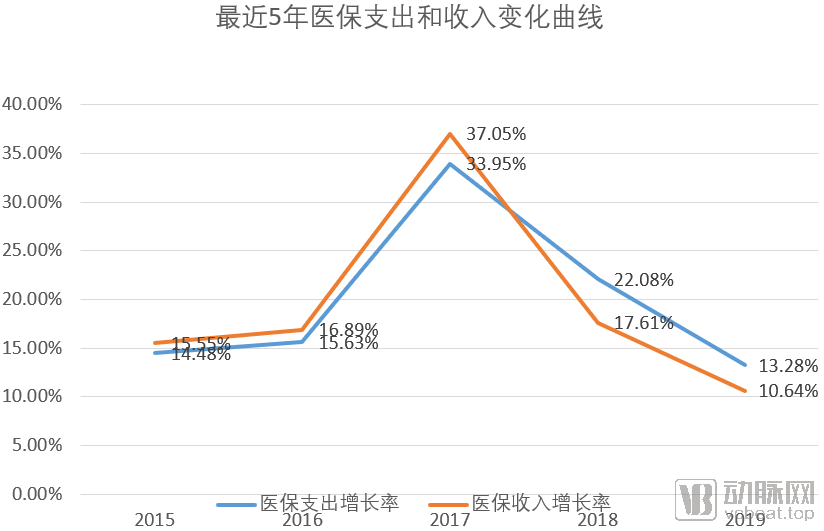

In recent years, with the rise in medical costs, health insurance has been under tremendous pressure. As shown in the figure, since 2018, the growth rate of health insurance expenditures has exceeded that of revenues."If this trend continues, the medical insurance fund will face the risk of deficit."Thus,The State is placing increasing emphasis on disease prevention, while also expecting commercial health insurance to assume a portion of the burden on public medical insurance.

Behind the Rapid Growth of Health Insurance Lies a Persistent Burden of Losses. As premium income surges, health insurance claim payouts have also risen sharply.According to data from industry exchanges, health insurance claim payments in the first half of the year amounted to RMB 29.758 billion, a year-on-year increase of 16.78%. Meanwhile, property and casualty (P&C) insurers’ health insurance business incurred an underwriting loss of RMB 2.221 billion in the first half of the year, making it the line with the largest underwriting deficit, while the underwriting profit margin decreased by 4.96 percentage points year on year.The lack of policyholder health data and insufficient post-underwriting health management resources and services have posed significant challenges for health insurance companies across product design, underwriting, and risk control, directly leading to increased loss ratios.

It is against this backdrop thatInsurance companies are also placing greater emphasis on user health management. On one hand, they aim to reduce the incidence rate and claims ratio of insured individuals during their coverage period through precise health management. On the other hand, they hope to design insurance products that meet market demands by collaborating with enterprises in the health management sector.,Refine and innovate health insurance products and related services, promote the deep integration and development of insurance with health management, and meet the growing and evolving service needs of enterprises, families, and individuals.

In light of the above, numerous insurance companies have continuously pushed boundaries and experimented, undertaking proactive and beneficial initiatives in areas such as integrated protection products, application of innovative technologies, expansion of outsourced health management services, development of health management platforms, and construction and integration of the health service industry chain.

For example, the collaboration between Pacific HealthCare and CPIC Life has led to the development of multiple practical tools for individual insurance underwriting, claims processing, and extended services, leveraging technologies such as big data analytics. Another example is Ping An’s early launch of its mobile health protection platform, the Ping An Health App, which focuses on providing users with one-stop intelligent services integrating “insurance coverage, medical care services, and health management.” Reportedly, the platform continues to be refined and innovated.

Recently, a central state-owned enterprise-controlled insurance company also launched a systematic health protection service platform centered on core service modules such as “screening, wellness, pharmaceuticals, medical care, and insurance.” The launch of this platform marks the insurer’s leading position in the industry in accelerating the implementation of the national “Healthy China 2030” strategy and advancing the innovative integration of insurance and healthcare services.The platform’s primary objective is to leverage insurers’ high-quality service resources, partners’ innovative IT health systems, extensive medical service resources, and seasoned operational capabilities to provide insurers, as well as their corporate and individual clients, with a comprehensive, end-to-end health service ecosystem encompassing insurance, health screenings, medication purchases, medical consultations, health management, consumer healthcare, and employee benefits. Additionally, the platform uniquely offers customized enterprise health management portals for served companies, utilizing modular service entitlement configurations to facilitate the implementation of personalized employee benefits and outsourced health management programs, while also supporting corporate client acquisition.

It is reported that the health protection platform took only a few months from planning to implementation, demonstrating such rapid and efficient development speed.On the one hand, this is driven by the insurer’s robust capabilities in strategic planning, resource integration, and operations; on the other hand, it is also attributable to the company’s partnership with Shicheng Yijiankang, a long-established industry leader in China’s public medical health checkup and health assurance services sector, which serves as the provider of its underlying core systems and core operational support.

With the aid ofShicheng Yijian boasts a service network of over 1,500 health check-up centers in public hospitals across China, a pool of more than 200,000 clinical specialists covering over 30 medical departments, and its independently developed Hongkang Integrated System—a comprehensive platform integrating prevention, physical examinations, health management, and medical care, refined over many years. This health assurance platform delivers a robust, full-scenario, end-to-end health management service system for enterprises, families, and individuals, enabling seamless, one-click access to comprehensive health management.

Although insurance companies are striving to closely integrate insurance with health management, the absence of a public healthcare system makes market entry time-consuming and labor-intensive. Furthermore, the high incidence rates of certain critical illnesses have already impacted insurers’ financial performance. Consequently,For insurance companies, there is an urgent need for products that excel in front-end control, back-end management, and loss ratio reduction.

andShicheng Yijiankang’s health protection platform can help insurance companies comprehensively optimize their insurance products and reduce related premium rates by accessing data from medical examination reports, health consultations, and advisory services. Furthermore, the health protection platform launched by Shicheng Yijiankang has established an integrated service chain and data chain encompassing insurance, medical examinations, health management, medical services, consumer services, and product sales, thereby laying the foundation for insurance business development, customer retention, and reduction of claim incidence rates.

As is well known, the public healthcare system constitutes a core underwriting threshold for insurance companies.Shi Cheng Yi Jiankang’s service foundation, spanning more than 1,500 hospitals, is built on its integration with public medical examination center systems, enabling insurance companies to rapidly expand their coverage in the public healthcare services sector.

Among them, in the area of public medical health checkups and services, benefiting from systematic integration and interoperability,The platform features a structured system of health checkup data labels and the capability to track various types of historical examination data, including years since onset, disease types, referrals, and records of critical illnesses. Leveraging core underlying algorithms and more than 3,000 disease database models, these authorized health checkup data effectively assist insurance companies in analyzing historical data and calculating risk control models. Furthermore, they enable insurers to establish comprehensive, multi-dimensional user data profiles encompassing insurance, health, examinations, and medical care. This significantly enhances insurers’ core competitiveness in areas such as product design and loss ratio reduction.

The “Outline of the ‘Healthy China 2030’ Plan” explicitly states that people’s health needs have shifted from a primary focus on treating acute diseases to comprehensive, full-chain, and whole-life-cycle health services. In the realm of health insurance, insurers must not only ensure convenient claims processing but also provide end-to-end services spanning disease prevention, health promotion, and health education to rehabilitation and post-discharge care, thereby achieving the integration of medical care with elderly care and of nursing with long-term care.

Undoubtedly, under this trend,The “Health Management + Insurance” model, designed to safeguard users’ life and health while reducing medical expenditures, will gain increasing recognition., as this modelIt not only helps users promote health, enhance the national health quality, and alleviate the challenges of chronic diseases and population aging, but also conserves medical resources, controls healthcare costs, and reduces insurance claim ratios, thereby returning insurance to its fundamental role of providing protection.

According to a report by 21st Century Business Herald, an increasing number of enterprises and public institutions are providing health protection services beyond basic medical coverage for their employees, entrusting insurance companies to manage these services. This trend has promoted the development of insurers’ entrusted management business for health protection. By the end of 2018, 26 insurance companies had launched such entrusted management services, covering 66.7 million people and providing payment services to a cumulative total of 10.77 million individuals. The scale of funds under entrusted management reached approximately RMB 34 billion, with management fees totaling RMB 720 million, accounting for about 2.1% of the entrusted fund size.

In this process, as a new player in the social security system, “Health Management + Insurance” should pay attention to the following four points.First, it is essential to clarify the position and role of commercial health insurance within the healthcare system, thereby establishing a commercial health insurance framework that seamlessly integrates with basic medical insurance.

Second, it should focus on playing a complementary role in the healthcare security system in terms of services., such as further improving top-level design and refining the adjustment of detailed policies—including market access mechanisms and the upgrading of settlement systems—during the process of co-locating commercial insurance institutions with social security agencies.

Third, in the process of health interventions by commercial insurance institutions, a mechanism should be established for health insurers to supervise medical practices and control healthcare costs. A payment formulary for commercial health insurance should be developed, seamlessly aligned with the basic medical insurance formulary, with differentiated reimbursement scopes and rates set for hospitals at different tiers., thereby achieving the goal of “seeking care for minor illnesses at primary hospitals and for major illnesses at tertiary hospitals,” promoting tiered diagnosis and treatment, and facilitating the decentralization of high-quality medical resources.

Fourth, improve the standard system construction for the entire industry and establish an industry information and data exchange platform., enabling interconnectivity and information exchange among commercial insurance companies, social security, health authorities, and healthcare institutions to better meet the public’s healthcare needs and support the “Healthy China” strategy.

For health management institutions, development can proceed in three directions. First, health management services should transition from mere physical examinations to comprehensive health management. Second, the physical examination model should shift from standardized packages to personalized assessments. Third, greater emphasis should be placed on health data collection, health risk assessment, and health guidance, with the implementation of a “1+X” personalized physical examination program.

As health management becomes an increasingly important component in the development and innovation of health insurance,“Insurance + Health Management” is becoming the new trend in the innovative development of commercial health insurance. The participation and deep empowerment by platform suppliers have boosted this trend, thereby accelerating the development of the entire big health industry.

We have every reason to believe that, through the concerted efforts of the government, insurance companies, platform vendors, and other stakeholders, China’s health insurance industry will surely “ride the wind and cleave the waves” in this vast blue ocean.