Third Round of China's National Drug Volume-Based Procurement: Fierce Price Cuts, 95% Max Reduction, and Intense Competition Among 194 Pharma Companies

On August 20, pharmaceutical companies once again faced a “major test”—the bid opening for the third round of China’s National Volume-Based Procurement of drugs.

Unlike the widespread anxiety that marked the initial implementation of centralized drug procurement, pharmaceutical companies—having already navigated three rounds of national-level procurement, namely the “4+7” pilot, the expansion of the “4+7” pilot, and the second round of national centralized drug procurement—are clearly mentally prepared for the “exam format.”

Compared with previous times,This round of procurement has further expanded the scope of products, covering 56 varieties, a quantity approaching the combined total of winning products from the previous two centralized procurement rounds. There are 82 product specifications, with a total procurement value of RMB 22.6 billion. A total of 194 companies participated in the bidding, including approximately 50 listed companies.Among them, Yangtze River Pharmaceutical Group, CSPC Pharmaceutical Group, Qilu Pharmaceutical, Shanghai Pharmaceuticals, Hengrui Medicine, and Kelun Pharmaceutical are the companies with the largest number of products involved in this centralized procurement, and they are also the leading domestic generic drug manufacturers.

As is well known, the purpose of centralized drug procurement is to explore and improve the mechanism for centralized drug procurement and a market-driven drug pricing formation mechanism, reduce the public’s burden of medication costs, standardize the order of drug circulation, and enhance the safety of medication use among the public. Therefore,The outcome of this “exam” not only affects the billions in commercial interests at stake for pharmaceutical companies in market competition, but also bears on the livelihoods of millions of doctors and healthcare professionals, as well as the well-being of hundreds of millions of patients.

Upon reviewing the bid results of this procurement round, all 55 drugs had successful bidders, except for the antiviral medication lamivudine tablets, which failed to secure a winning bidder (resulting in a failed tender). In light of this centralized drug procurement outcome, VCBeat provides an analysis from the following perspectives.

In each round of centralized drug procurement, the most eye-catching aspect is the fierce price competition among pharmaceutical companies.

According to the broadcast data from CCTV's Xinwen Lianbo,The average price reduction for the proposed winning products in the third round of China's National Centralized Drug Procurement was 53%, with the highest reduction reaching 95%.

Among them, what has attracted much attention isMetformin, hailed as the “wonder drug” for lowering blood glucose, recorded a procurement amount of RMB 1.305 billion, ranking third in this volume-based procurement round by total value.. As is well known, metformin is widely used in clinical practice, with a market size exceeding RMB 5 billion in China, and it is a commonly prescribed medication throughout the course of treatment for over 100 million patients with type 2 diabetes in the country. However, there are numerous domestic manufacturers of generic metformin, and foreign pharmaceutical companies also hold a significant share of the market. Consequently,As many as 44 companies participated in this centralized procurement, resulting in exceptionally fierce competition.

The proposed award results indicate a significant price reduction for awarded metformin products, with some manufacturers reducing prices by more than 80%. Among them, Chongqing Kerui Pharmaceutical (Group) Co., Ltd. (hereinafter referred to as “Chongqing Kerui”) submitted the lowest bid for Metformin Hydrochloride Tablets at less than two cents per tablet, specifically RMB 0.0154 per tablet.

Captopril, an antihypertensive medication, has also entered the era of pricing in cents., the three proposed winning specifications were all priced below 0.1 yuan per unit. Chongqing Kerui’s bid was as low as 0.014 yuan, while the prices of Captopril tablets from Huazhong Pharmaceutical and Shanghai Xudong also did not exceed 0.02 yuan.

The major upset revealed this time is“Viagra” Sildenafil, with Qilu Pharmaceutical, which had received approval just days prior, being the sole winner of the bid. The company’s quoted price for a 25 mg tablet was RMB 1.748,Compared to the highest effective bid of RMB 28.3414, the price reduction exceeds 93%.. Additionally, for those with larger procurement volumesMoxifloxacin Sodium Chloride Injection Also Sees Significant Price Reduction, with Tianjin Hongri and Hainan Aike ultimately obtaining the proposed winning bid status; among them, Hainan Aike quoted a price of 35.27 yuan,Decline of Over 80%。

It is evident that the overall price reduction in this round of centralized drug procurement remains substantial, with the intensity surpassing that of the previous three rounds. The prices of certain drugs have dropped to what can be described as “rock-bottom” levels. This outcome is attributable to the increasing sophistication of mechanisms such as centralized procurement rules and negotiations.

Significant reductions in drug prices have alleviated the pressure on medical insurance expenditures, making the benefits to the public increasingly evident. In terms of product selection for centralized procurement, this round covers medications for chronic and major diseases—including diabetes, hypertension, cardiovascular conditions, infections, and cancer—which typically entail a substantial long-term medication burden.Volume-based procurement has significantly reduced drug prices, substantially alleviating the financial burden on patients. This enables greater access to high-quality medications for patients, thereby addressing the issue of treatment accessibility.。

Compared with the second batch of centralized procurement, the rules for the third batch were only slightly adjusted and optimized, with the maximum number of selected enterprises increasing from 6 to 8. Among them,The agreed procurement volumes for antibiotics such as amoxicillin, cefdinir, cefaclor, and clarithromycin, as well as injectable formulations, have been reduced relative to other categories to curb the clinical use of antimicrobial agents and promote the rational use of medicines.。

Among the 56 varieties included in this round of centralized procurement,Lamivudine Tablets, an antiviral drug, did not announce any winning manufacturers, becoming the only product that failed to secure a bid in this volume-based procurement.

According to public reports, GlaxoSmithKline’s (GSK) lamivudine tablets have experienced a significant market decline since the expiration of their patent, driven by two main factors: the lower prices of domestically produced generic drugs and the emergence and widespread adoption of newer-generation hepatitis B medications. Data show that in 2018, entecavir accounted for 52% of the hepatitis B drug market, interferons for 17%, tenofovir disoproxil fumarate for 13%, while lamivudine tablets and other drugs collectively made up the remaining 18%.

In light of the above, GlaxoSmithKline (GSK) formally divested its lamivudine product line in 2019. Chongqing Yaoyou, a subsidiary controlled by Fosun Pharma, acquired the drug registration approval for lamivudine tablets (strength: 0.1 g; brand name: Heptodin), along with the production license and GMP certificate for the associated manufacturing facilities, for no more than RMB 250 million. Overall, neither GSK nor Fosun Pharma had high expectations that this drug would be included in the volume-based procurement program.

On the day of the centralized procurement, the original research product Lamivudine Tablets 0.3g from GlaxoSmithKline (GSK) and Fosun Pharma was quoted at RMB 904.2 per box, with virtually no price reduction. The Lamivudine Tablets 0.15g from Shijiazhuang Dikang Longze were quoted at RMB 11.94 per box, which also did not reach the maximum valid declaration price.

According to the proposed selection results, CSPC Ouyi and Qilu Pharmaceutical, leading domestic generic drug manufacturers, emerged as the two companies with the highest number of selected products in this centralized procurement round, each having eight varieties chosen.

The products from CSPC Ouyi Pharmaceutical that are proposed for selection include Montelukast Sodium Chewable Tablets, Celecoxib Capsules, Memantine Hydrochloride Tablets, Ibuprofen Granules, Captopril Tablets, Metformin Hydrochloride Extended-Release Tablets, Metformin Hydrochloride Tablets, and Ticagrelor Tablets. Among these, the first three products secured the top priority status with the lowest “unit comparable price.”

Qilu Pharmaceutical’s provisionally selected products include capecitabine tablets, sildenafil citrate tablets, apixaban tablets, olanzapine orally disintegrating tablets, montelukast sodium chewable tablets, tofacitinib citrate tablets, vildagliptin tablets, and etoricoxib tablets, with seven of these products winning the bid as the first-ranked candidates.

Interestingly,Huahai Pharmaceutical Wins Bids for All Three of Its Volume-Based Procurement Products, namely Valsartan Tablets, Olanzapine Orally Disintegrating Tablets, and Sertraline Hydrochloride Tablets,As soon as the news broke, the company's stock price rose significantly in the afternoon trading session.. Additionally,Huadong Medicine, which failed to be selected in the second batch of volume-based procurement, won bids for two products in this centralized procurement., namely Anastrozole Tablets (1 mg) and Domperidone Tablets (10 mg).

Notably, the current national volume-based drug procurement has become a competitive arena for domestic generic pharmaceutical manufacturers, raising concerns about Chinese companies that trade lower prices for higher sales volumes.The industry’s current focus is on the fact that, as centralized procurement prices are significantly lower than the original drug prices, pharmaceutical companies’ profit margins have been squeezed, imposing higher requirements on quality control. On the other hand, reduced profitability also poses certain challenges to how pharmaceutical companies can sustain their investment in the research and development of innovative drugs in the future.

From a more granular perspective, the winning bid price in centralized volume-based procurement represents the delivery price of pharmaceuticals to hospitals. When drug prices were high, costs associated with packaging, distribution, and storage accounted for a relatively small proportion. However, under the deeply discounted bottom prices—often just 10% or 20% of the original prices—these factors have become significant and non-negligible components of overall drug costs.

Furthermore, from the perspective of the drug development and production cycle, generic drugs currently must pass the consistency evaluation to obtain marketing approval, with costs reaching millions.In this volume-based procurement round, several pharmaceutical companies’ products had only just passed the consistency evaluation in the past two months and currently have no sales revenue. How these companies will recoup their costs poses a significant test to their subsequent operational capabilities.

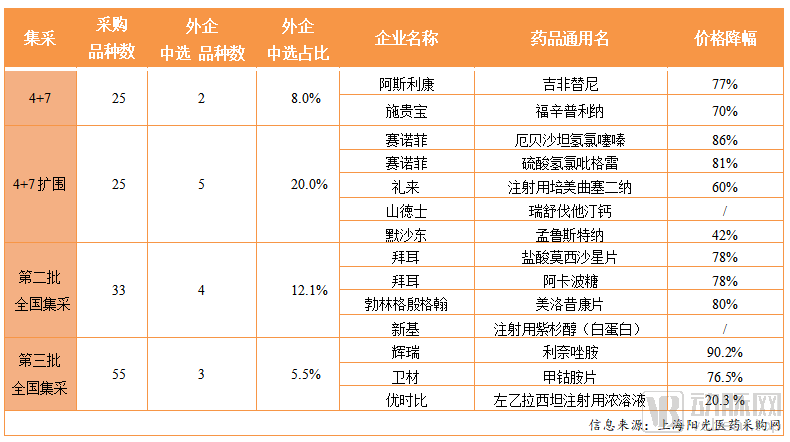

In this round of centralized drug procurement, unlike domestic companies that frequently submitted rock-bottom bids, many products from foreign pharmaceutical companies were offered at high or current market prices, with only a small fraction symbolically reducing prices by approximately 10%. According to the publicly announced list of proposed winning bidders, only three foreign pharmaceutical companies—Pfizer, UCB, and Eisai—have been shortlisted.

Among them, products such as AstraZeneca’s anastrozole, Merck & Co.’s desloratadine, Roche’s capecitabine, Eli Lilly’s orally disintegrating olanzapine tablets, GSK’s (GlaxoSmithKline) lamivudine, Novartis’s letrozole, and Pfizer’s sertraline were all quoted at prices far exceeding the maximum effective bid price, effectively amounting to a direct withdrawal from the volume-based procurement market.

Taking the antiviral drug lamivudine as an example, GlaxoSmithKline (GSK), the originator company, has basically not reduced its price, quoting 904.2 yuan per box, which is not significantly different from the original market price. In contrast, Shijiazhuang Dikang Longze, a domestic generic manufacturer, quoted 11.94 yuan per box, resulting in an exceptionally large price disparity between the two.

Moreover, for capecitabine, the highest valid quoted price per 500 mg tablet was just over RMB 7, whereas the originator’s quote was RMB 298 for 12 tablets, equivalent to RMB 24.8 per tablet. Similarly, for letrozole 2.5 mg tablets, the highest valid declared price per tablet was just over RMB 9, while the originator company quoted RMB 36.3. These volume-based procurement candidates were eliminated early because their bids exceeded the ceiling prices.

In fact, in this round of centralized drug procurement, the number of original research pharmaceutical companies participating was not small, as the variety of drugs involved reached a new high. For example, Merck & Co. and Pfizer were involved with 5 varieties, Eli Lilly, Novartis, AstraZeneca, and UCB were involved with 3 varieties, and Astellas and Bristol-Myers Squibb were involved with 2 varieties. ButBased on the results, only three original research products have won the bid: UCB’s levetiracetam injection, Pfizer’s linezolid tablets, and Eisai’s mecobalamin tablets.。

The starkly different bidding strategies adopted by domestic pharmaceutical companies and foreign enterprises may be partly attributable to market feedback following the first three rounds of national centralized drug procurement.. According to Bayer’s first-half 2020 performance report, global sales of its diabetes drug Glucobay (generic name: acarbose) fell by 73.8%. This decline was driven by the fact that, in the second round of China’s national centralized volume-based procurement in January of this year, Bayer submitted an ultra-low bid of RMB 0.18 per acarbose tablet. Although the bid was successful, it directly resulted in a sharp drop in Glucobay’s sales revenue.

In contrast to Bayer, Pfizer’s first-half 2020 performance report benefited from favorable market sales of its drugs that had not won bids. Although Pfizer’s Lipitor and Norvase failed to win bids in the initial “4+7” volume-based procurement program at the end of 2018 and in the September 2019 expansion of the “4+7” program, the report showed that sales of these two drugs grew against the trend.

Beyond market sales performance, the “withdrawal” of foreign enterprises may also be driven by considerations of global price uniformity., because once prices in China drop significantly due to centralized volume-based procurement, it may cause substantial fluctuations in the company’s pricing strategies in markets outside China. On the other hand, since originator drugs from foreign pharmaceutical companies have already established brand advantages in the market, even if they fail to win bids, they can still target the out-of-hospital market and the self-pay market.

According to a report by Caijing, the latest requirements for coordinating medical insurance payment standards with procurement prices state that for non-winning drugs whose prices at the end of 2018 were more than twice the winning bid price, the payment standard in 2019 shall be set at no less than a 30% reduction from the original price, and adjusted to align with the winning drug’s price as the payment standard in 2020 or 2021. This means that,There is still a certain buffer period for the medical insurance reimbursement of high-priced original research drugs that did not win the bid. After squeezing out the artificially inflated prices through centralized procurement, drug prices will be regulated through medical insurance payment standards.

After four rounds of national centralized procurement “major tests,” volume-based procurement has gradually become normalized, currently showing trends in three main areas.

1. The substitution effect of originator drugs is beginning to emerge, and the concentration of the generic drug industry will continue to rise.It is evident from this volume-based procurement (VBP) round that most originator drugs were excluded, while the substitution by generic drugs is on the rise. As VBP becomes normalized, if foreign pharmaceutical companies continue to forfeit the VBP market in future rounds, this will inevitably accelerate consolidation within the generic drug industry. For domestic generic manufacturers that secure winning bids, this trend will further stabilize their market share.

Second, quality supervision of selected drug varieties will become increasingly important.. To secure inclusion in the volume-based procurement (VBP) list, many generic drug manufacturers have significantly reduced their prices. While this has largely squeezed out the “bubble” in drug pricing and enabled companies to gain hospital formulary access and rapidly expand their market share, enterprises ultimately need to remain profitable to ensure sufficient funding for future development. Consequently, the market is highly concerned about drug quality, making post-award quality supervision of winning bids particularly critical.

Third, the distribution landscape of the pharmaceutical market will undergo changes.. The strategy of exchanging price for volume is reshaping market shares among pharmaceutical companies. Given the substantial decline in drug prices, a number of originator drugs will withdraw from the hospital market. As the primary channel for prescription drug sales, the role of hospitals will gradually diminish, with the main sales channel shifting from hospitals to specialized pharmacies. Therefore, actively exploring markets outside the volume-based procurement (VBP) framework—such as retail terminals and online sales channels—will become a key strategic focus for pharmaceutical companies whose products were not selected in VBP bids.

The outbreak of the novel coronavirus disease (COVID-19) this year has led people to place increasing emphasis on health and to hold life in greater reverence. As an industry dedicated to maximizing the physical and mental well-being of all individuals, the healthcare sector will continue to advance further, driven by the concerted efforts and active promotion of the government, healthcare providers, society, and other stakeholders.