WeDoctor Tops CB Insights' Global Digital Health 150 for Second Consecutive Year, Spearheading China's Leadership in Digital Health Innovation

Recently, the globally renowned data intelligence platform CB Insights released its list of the Top 150 Digital Health Companies. Seven Chinese digital health startups made the list, with the total number second only to that of the United States, ranking China second worldwide. WeDoctor, a digital health enterprise based in Hangzhou, China, has once again topped the list as the unicorn company with the highest publicly disclosed valuation, having secured the top spot last year. It is reported that as early as 2017, CB Insights had already recognized WeDoctor as China’s leading healthcare technology unicorn.

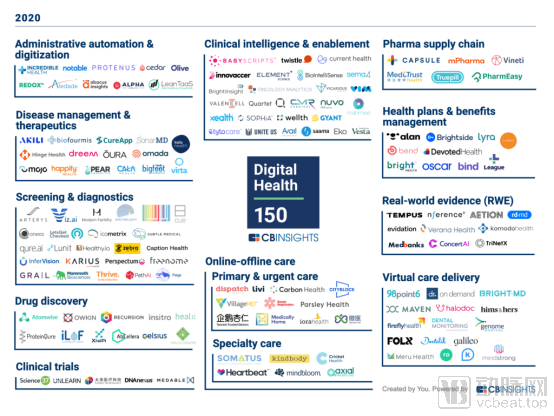

CB Insights’ Global Digital Health 150, the world’s first list dedicated to the concept of “digital health,” is globally recognized as the most authoritative ranking in the digital health sector. This year marks the second time CB Insights has released the list, which selects 150 innovative technology companies from over 8,000 enterprises worldwide that provide solutions for the transformation of the healthcare industry through digital technologies. The list covers 12 sectors, including smart clinical care, screening and diagnosis, new drug development, and pharmaceutical supply chains.

Top 150 Digital Health Companies of 2020: Listed Enterprises and Categories (Data Source: CB Insights)

In 2018, the World Health Organization (WHO) redefined “digital health,” subsuming concepts such as e-health, medical informatics, health informatics, telemedicine, telehealth, and mHealth under the umbrella of “digital health.” The outbreak of the COVID-19 pandemic in 2020 posed severe challenges to the global public health system, during which digital health played a significant role in epidemic control. This has established digital health as an indispensable component of the global healthcare system and has strongly driven the overall digital transformation of the health industry.

The list shows that, spurred by the COVID-19 pandemic, digital healthcare services have experienced rapid growth, with companies offering telemedicine services accounting for 41% of those listed. Taking WeDoctor as an example, at the outset of the outbreak, WeDoctor leveraged its digital capabilities to launch the WeDoctor Real-Time COVID-19 Assistance Platform and the WeDoctor Global Anti-Epidemic Platform. These platforms provided services within China, including real-time epidemic updates, free online consultations, psychological counseling, follow-up visit prescriptions, and medication delivery. Simultaneously, they shared China’s epidemic control experience internationally, supporting overseas Chinese and individuals worldwide. WeDoctor’s innovative initiatives opened up an “aerial battlefield” for epidemic prevention and control. By mid-August, the Real-Time COVID-19 Assistance Platform had served a cumulative total of 2.18 million people, with over 150 million visits; the Global Anti-Epidemic Platform was recommended by more than 170 Chinese embassies and consulates abroad, providing services to 3.26 million people in over 220 countries and regions.

While digital health is deeply integrating into the public healthcare system, it is also playing an increasingly important role across all segments of the entire health industry chain. Anand Sanwal, CEO of CB Insights, stated that digital health companies featured in 2020 are driving comprehensive innovation across every link of the value chain, benefiting biopharmaceutical companies, hospitals, patients, insurance providers, and other stakeholders.

As a digital health platform covering the entire industry chain, WeDoctor’s core business spans eight of the 12 sectors featured in the rankings, encompassing healthcare services, pharmaceuticals, medical diagnostics, health insurance, and healthcare big data. Compared with companies focused on a single segment, WeDoctor more comprehensively reflects the value of digital health, which has been a key reason for its long-term favorability among capital market investors.

It is understood that WeDoctor has helped comprehensively enhance regional medical service capabilities and residents' health levels, while slowing the growth rate of medical insurance expenditures, by building a Health Maintenance Platform (HMP) supported by digital platforms and aimed at improving health. Currently, WeDoctor has initiated the construction of digital health communities in multiple provinces and cities, including Tianjin, Shandong, Ningxia, Fujian, and Hubei. By connecting more than 7,200 hospitals, over 250,000 doctors, and more than 200 million real-name registered users in China, WeDoctor continues to explore and enhance the value of data elements, thereby fully empowering the digital transformation of the healthcare industry.

Notably, since the beginning of this year, China has continuously rolled out policies to encourage the development of the digital health industry. Among these, the opening up of medical insurance payment policies is expected to unlock a trillion-yuan payment market for the digital health sector. However, only two companies on the list have achieved breakthroughs in reimbursement through national medical security systems: WeDoctor from China and Doctor On Demand from the United States. It is understood that Doctor On Demand began gradually integrating with the U.S. federal Medicare program in May of this year, while WeDoctor started exploring this field as early as 2015 and has already implemented online medical insurance payments in multiple regions across China. Further policy liberalization will accelerate the integration of digital health platforms with the medical security system, gradually forming a business landscape where the national medical security system and commercial insurance systems mutually reinforce and complement each other.

The ranking report shows that as of August 10, the 150 listed companies had raised a total of over $20 billion in financing across more than 600 transactions, with participation from over 900 investors. These companies include well-funded mature enterprises, startups that have secured a market foothold, and research-focused early-stage ventures. All demonstrate strong growth potential and promising market prospects, while the pandemic has further accelerated the momentum of digital health companies.