Futu Drives Billion-Dollar IPO Subscriptions for Chinese Biotech Stars: A Surge in Healthcare Listings

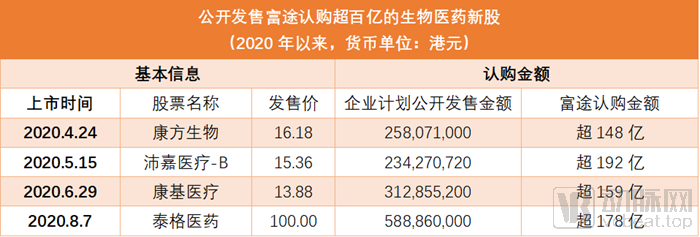

On August 6, 2020, Tigermed listed on the Hong Kong Stock Exchange, with its share price opening 19% higher. As the leading domestic clinical CRO, Tigermed’s IPO in Hong Kong, amid the booming biopharmaceutical R&D sector, was regarded by the secondary market as a phenomenal event from the outset, making the high opening on the first day of trading entirely expected. On the morning of the Hong Kong IPO, Tigermed announced the placement results, revealing that the public offering segment received subscriptions 414.39 times over, triggering an 11.5% clawback of shares from the international placement. In the grey market trading on Futu Securities the previous day, Tigermed’s shares also closed up 18.2%, with a turnover of HK$186 million, ranking second highest in the history of Futu’s grey market transactions.

Notably, several other star mainland Chinese biopharmaceutical companies listed in Hong Kong have also delivered impressive performance on the Hong Kong Stock Exchange, from issuance through trading. As one of the most active and highest-volume internet brokers for US and Hong Kong stocks, Futu has reported that, since the beginning of this year, multiple biopharmaceutical companies have achieved subscription volumes exceeding HK$10 billion on its platform.

(Data source: Futu)

Among them, Peijia Medical once became the “King of Frozen Funds” as its public offering was oversubscribed approximately 1,183 times, with over RMB 277 billion in frozen funds, surpassing Alibaba, which returned to Hong Kong for its listing at the end of 2019. On May 15, 2020, the day Peijia Medical listed on the Hong Kong Stock Exchange, its closing price was 67.97% higher than the offer price. Another minimally invasive surgical device company, Kangji Medical, saw its shares rise 98.85% on the first day of trading, with turnover exceeding HK$3.3 billion. In the grey market trading on Futu Securities the afternoon before the first trading day, Kangji Medical’s share price closed up 85%, with grey market turnover reaching HK$138 million.

For a company’s shares to transition from the private equity market to the public capital markets, they must undergo an extensive preparation and issuance process before becoming eligible for trading. Activities during the issuance phase—including sponsorship, underwriting, roadshows, share placement, and even grey market trading—can all influence the subsequent public trading price of the stock. On the highly market-oriented Hong Kong Stock Exchange (HKEX), retail investors are the primary source of market liquidity. Consequently, subscription results for the public offering tranche have a more significant and easily quantifiable impact on both the IPO performance and post-listing liquidity.

Over the past year and a half, the Hong Kong Stock Exchange has almost become the world’s busiest capital market, with one of the most important reasons being its new listing rules introduced in April 2018.

The securities market under the Hong Kong Stock Exchange (HKEX) comprises two trading platforms: the Main Board and the Growth Enterprise Market (GEM). In December 2017, HKEX announced the addition of two new chapters to its Main Board Listing Rules: first, to allow listings of companies with weighted voting rights structures; second, to permit listings of biotechnology companies that are not yet profitable or have no revenue. At the end of April 2018, the HKEX formally released the “Listing Regime for Emerging and Innovative Companies,” incorporating the aforementioned provisions. This marked the most significant listing reform undertaken by HKEX in 25 years.

Since then, biotechnology companies that fail to meet the financial eligibility criteria of the Main Board have been allowed to list with a “B” suffix, marking the first time that the door to public financing has been opened to unprofitable biopharmaceutical companies.

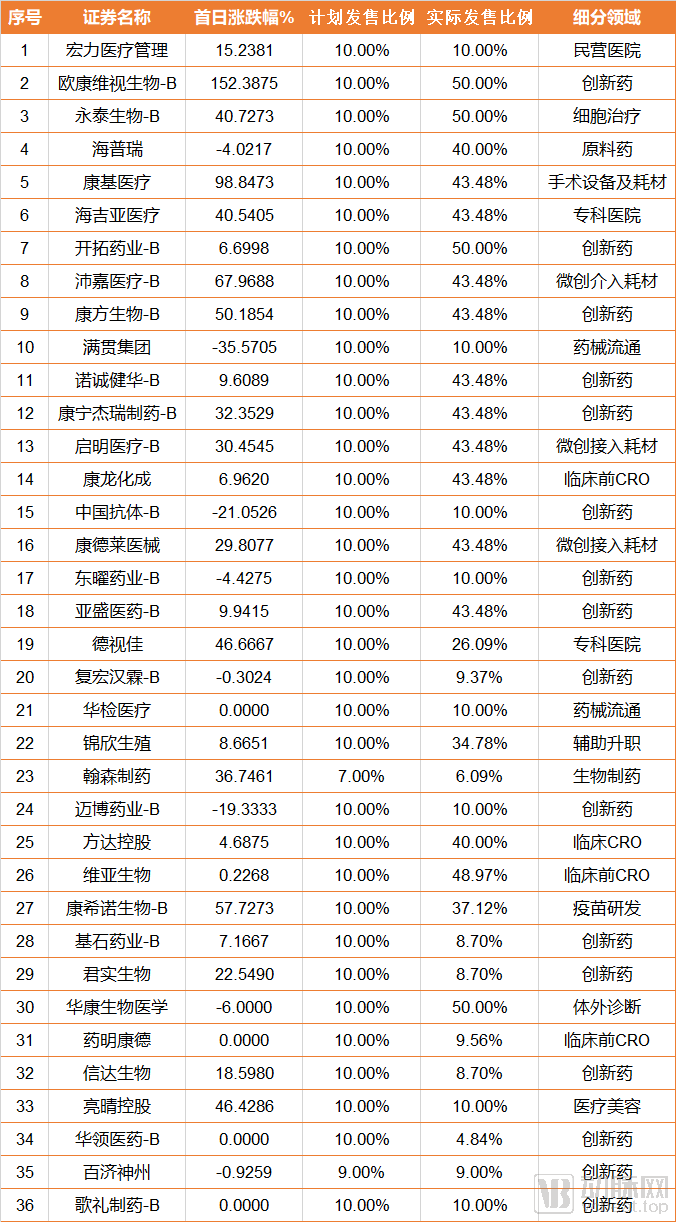

On May 8, 2018, Ascletis Pharma, the first pre-revenue biotechnology company to list under the Hong Kong Stock Exchange’s new listing regime, filed its prospectus and subsequently listed on the HKEX on August 1. According to statistics from VCBeat, a total of 36 biopharmaceutical companies had gone public by July 2020. The new listing rules ushered in a wave of IPOs for biotechnology firms on the Hong Kong Stock Exchange.

(Listing Performance of 36 Biopharmaceutical Companies | Data Source: Compiled by VCBeat from public information )

The Hong Kong Stock Exchange (HKEX) is a highly market-oriented capital market, where it is not uncommon for companies listing via an initial public offering (IPO) in Hong Kong to see their share prices fall below the offer price on the first day of trading. Among the 36 biopharmaceutical IPOs, 24 companies experienced a rise in their share prices on the first day, with Ocumension Therapeutics posting the largest gain at 152.38%. Four companies closed at their offer price, while eight saw their share prices decline. A further analysis of the correlation between first-day price fluctuations and the planned versus actual offering ratios reveals some interesting patterns.

(Comparison of Clawback Mechanisms and First-Day Performance for 36 Biotech IPOs | Data Source: Compiled by VCBeat from Public Information)

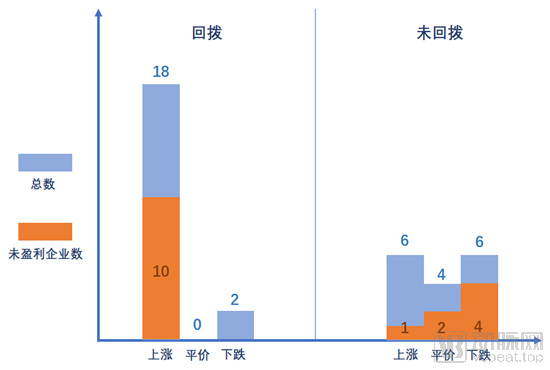

Among the 36 biotech companies, 20 clawed back a portion of their international placement shares during the issuance phase. Of these, 18 saw their stock prices close higher on the first day of listing. Notably, all 10 unprofitable companies that executed such clawbacks recorded first-day closing price gains.

The first-day performance of 16 biotech companies that did not trigger the clawback mechanism was relatively muted: six rose, four remained flat, and six fell, including the three companies with the largest first-day declines. Among the non-clawback stocks that declined, two-thirds were unprofitable enterprises.

This statistic clearly demonstrates a significant correlation between the level of retail investor participation and the post-listing price fluctuations of new stocks. Furthermore, during an initial public offering (IPO), the offer price is primarily determined by institutional investors. Apart from hedge funds, most institutional investors are long-term funds with low trading frequencies. Consequently, once the stock enters the secondary market, its price volatility is largely influenced by the trading activity of retail investors. In the Hong Kong stock market, which is rife with penny stocks, capital tends to concentrate in leading enterprises. If companies fail to achieve a reasonable allocation between retail and institutional investors at the time of listing, or if they do not maintain continuous and efficient investor relations thereafter, they are likely to face liquidity issues.

When a company lists on the Hong Kong Stock Exchange, its share offering is divided into two parts: placement and public offering. Placement refers to the targeted sale of shares to institutional investors such as global funds, while public offering denotes the open sale to retail investors. The typical allocation ratio between placement and public offering in a Hong Kong IPO is 9:1.

When the subscription amount for a public offering is tens or even hundreds of times the number of shares offered, underwriters will reallocate 10% to 50% of the shares originally allocated to institutional investors to retail investors. Based on our analysis of the issuance and listing performance of 36 biotechnology companies listed on the Hong Kong Stock Exchange, we can basically conclude that whether or not a clawback mechanism is applied during the share issuance stage will, to some extent, affect their initial post-listing performance.

A critical factor influencing the initial public offering (IPO) of new stocks is the distributor’s promotional capability. This capability is closely tied to the distributor’s user base, asset volume, and user experience, directly impacting the enthusiasm for public subscription and, consequently, shaping distinct trading patterns on the first day of listing.

FUTU I&E is the corporate services brand under Futu. As an internet investment bank aggregating tens of millions of investors, one of its core businesses is providing U.S. and Hong Kong stock IPO distribution services to corporate clients, having successfully assisted dozens of companies in listing on the U.S. and Hong Kong stock markets.

The head of Futu Anyi’s business division stated that in early 2019, the enthusiasm for subscribing to new Hong Kong stock listings was not as intense as it is today. Some companies preparing for IPOs in Hong Kong were deeply concerned that their business models would not be understood by investors and felt significant pressure regarding public offerings. By providing tools such as “Infographic Prospectus Summaries” and online roadshow platforms, Futu Anyi helped expose these companies’ investment value to a broad investor base. This approach not only facilitated their successful listings but also helped sustain investor interest post-IPO.

(Selected Hong Kong Stock IPO Distribution Cases by Futu Anyi | Data Source: Futu)

According to Futu’s Q2 financial report just released, the company’s revenue in the second quarter reached USD 88.7 million, a year-on-year increase of 165%. Gross profit amounted to USD 68.9 million, up 172% year on year, while net profit hit USD 31.3 million, surging 310% year on year. Latest statistics show that Futu NiuNiu has over 10 million users, and Futu Securities’ client base has exceeded one million, making it one of the largest internet brokers for US and Hong Kong stocks in terms of user scale and investor density. As of the end of Q2, Futu’s client assets totaled HKD 142.4 billion (USD 18.4 billion), with total trading volume reaching USD 83.1 billion (approximately HKD 643.9 billion). As previously mentioned, Futu has completed multiple biopharmaceutical IPOs with subscription scales exceeding tens of billions this year, achievements primarily attributed to its substantial asset base and active investor community.

Leveraging Futu’s large, active user base and comprehensive financial licenses, Futu IPO Plus has gained widespread market recognition, providing IPO distribution services to companies such as Beike, Genetron Health, Xiaomi Group, and Meituan Dianping. “In addition, there have recently been two major IPO cases in the U.S. and Hong Kong stock markets, respectively. With Futu Securities serving as an underwriter for XPeng Motors’ listing, the company attracted subscriptions from over 46,000 Futu clients, with subscription amounts exceeding USD 2.21 billion. In the Hong Kong market, Nongfu Spring attracted subscriptions from Futu clients totaling more than HKD 35.1 billion, setting a new record.”

“In recent years, mainland Chinese biotech companies have shown strong enthusiasm for pursuing initial public offerings (IPOs) in the U.S. and Hong Kong, and we have provided services to the majority of them,” said the head of Futu’s AnYi business unit.

Notably, Futu has not only facilitated the successful listings of numerous biopharmaceutical companies on the U.S. and Hong Kong stock markets, but also serves as the contracted ESOP equity incentive service provider for many such firms. Companies including Akeso, Peijia Medical, Ocumension Therapeutics, and InnoCare Pharma have all selected Futu Anyi as their contracted ESOP equity incentive service provider.

(Selected ESOP Service Cases by Futu Anyi | Data Source: Futu)

ESOP, or Employee Stock Ownership Plan. To better align core employees with the company’s long-term development, most companies establish equity incentive plans at an early stage. During the IPO process, companies must address various considerations, including the maximum percentage of total share capital allocated to equity incentives as stipulated by different stock exchanges, the implementation of equity incentives post-listing, the determination of exercise prices for equity incentive shares, and the sources of funds for exercising these options. It is evident that a successful public listing requires more than just executing the IPO; pre-IPO trust and tax planning, as well as exercise arrangements, are equally critical. For founders and senior executives, well-structured trust designs and tax planning can facilitate risk segregation and reasonable tax optimization, underscoring their significant importance.

Under traditional solutions, equity incentive services are relatively fragmented, with various service stages disconnected from one another. Data management also suffers from weaknesses such as inadequate data governance, lack of client-side (C-end) services, poor customer support capabilities, and slow response times. Leveraging its product capabilities derived from leading internet companies, Futu Anyi provides a one-stop, end-to-end service for ESOP (Employee Stock Ownership Plan) equity incentives. It seamlessly integrates with professional partners to deliver comprehensive management covering incentive plan design, trust and tax planning, data management, and exercise implementation. “After adopting Futu Anyi’s ESOP services, companies no longer need to coordinate with multiple vendors, significantly reducing their workload,” said the head of this business unit. “Furthermore, Futu Anyi’s ESOP product places particular emphasis on data security, employing encryption and secondary storage for sensitive data. Its security capabilities have been rigorously tested by large enterprises such as Tencent, ensuring the safety of user data.”

“Futu Anyi has provided ESOP equity incentive services to over 100 companies, accumulating extensive practical experience. We are well aware of the potential compliance and tax risks throughout the entire process. We have also observed cases where companies neglected trust structures and tax planning arrangements prior to their IPOs, resulting in a significant increase in employees’ exercise costs after listing,” said the head of this business unit. “For companies, directly coordinating with various service providers and stakeholders across the end-to-end ESOP process can incur substantial time costs and trial-and-error expenses. Therefore, they chose Futu Anyi as their one-stop ESOP equity incentive service provider.”

In recent years, the continuous improvement of China’s biopharmaceutical innovation ecosystem has enabled startups to navigate their early-stage rapid growth more swiftly, with an increasing number of companies facing IPO decisions. In practice, whether choosing to list on A-shares or pursuing initial public offerings in Hong Kong or the United States, a thorough understanding of the differentiated rules across these capital markets is essential for ensuring a smoother listing process.