Three Chinese Cell Therapy Companies File for IPO: How Close Is CAR-T to Full Commercialization in China?

2020: The Year CAR-T Cell Therapy Rose in China

As of 2020, two companies, Fosun Kite and WuXi Juno, have had their New Drug Applications (NDAs) accepted; Legend Biotech, Yatai Bio, and WuXi Juno have successively applied for market approval, with Yatai Bio and Legend Biotech having successfully listed on the Hong Kong Stock Exchange and NASDAQ, respectively; additionally, the U.S. FDA has once again approved the third CAR-T cell therapy product for marketing through the Fast Track designation.

Since the consecutive market launches of Novartis’s Kymriah and KITE’s Yescarta in 2017, although enthusiasm for China’s cell therapy sector in the primary market has continued to rise, there have been few breakthroughs in product approvals. After three years of dormancy, the industry finally reached its tipping point in 2020.

With JW Therapeutics’ application for listing on the Hong Kong Stock Exchange as a starting point, we once again examine three Chinese cell therapy companies that have filed for IPOs to assess the industry’s direction and identify the remaining obstacles on the path to commercialization.

In April 2016, WuXi AppTec and Juno Therapeutics announced a partnership to establish JW Therapeutics, leveraging Juno’s chimeric antigen receptor (CAR-T) and T-cell receptor (TCR) technologies alongside WuXi AppTec’s R&D and manufacturing platform and extensive experience in the Chinese local market, with the joint aim of building China’s leading cell therapy company.

When discussing JW Therapeutics, it is impossible not to mention Fosun Kite, another highly similar company. In January 2017, following the collaboration between JUNO Therapeutics and WuXi AppTec, KITE Pharma also entered into a partnership with Fosun Pharma, establishing the joint venture Fosun Kite to introduce KITE’s Yescarta (then unapproved, under the code name KTE-C19) to the Chinese market.

The rivalry between JUNO and KITE has persisted throughout the entire development history of CAR-T products. The two companies followed remarkably similar trajectories, from their founding and fundraising efforts to product development, culminating in their respective acquisitions by Celgene and Gilead Sciences.

In 2016, JUNO was also a strong contender for the first CAR-T product. However, in July 2016, one of JUNO’s lead candidates, JCAR015, caused the deaths of two leukemia patients due to neurotoxicity during its Phase II clinical trial, leading the FDA to halt the study.

Although there has been no further update on JCAR015, JUNO still maintains other product pipelines that are competitive with similar offerings. In the Phase II clinical trial data for JCAR017 presented at the 2017 ASH Annual Meeting, among the 15 patients treated at dose level 2, the overall response rate (ORR) was 80% (12/15), and the complete response (CR) rate was 73% (11/15).

From 2018 to 2019, JUNO continued to update data on JCAR017; however, it has yet to file for marketing approval. Meanwhile, its long-time rival KITE has already launched its first product, Yescarta, in markets including Europe and Japan, and its second product has also received U.S. FDA approval for market entry.

Adverse reactions associated with early products may have, to varying degrees, impacted JUNO’s regulatory approval pathway. In the European and American markets, JUNO has clearly fallen into a disadvantaged position.

While the European and American markets are large, the Chinese market cannot be underestimated. On their development trajectories in China, JUNO and KITE have once again intersected.

Fosun Kite and JW Therapeutics, two joint ventures, have consistently remained in the top tier of China’s cell therapy industry, leveraging their substantial strengths and maintaining closely matched R&D progress. In June 2018, JW Therapeutics’ relmacabtagene autoleucel injection (Relma-cel, JWCAR029) received approval for its Investigational New Drug (IND) application; in September of the same year, Fosun Kite’s fucikabtagene autoleucel injection (FKC876) also obtained IND approval.

By 2020, Fosun Kite’s NDA for ciltacabtagene autoleucel injection was the first to be accepted by the CDE in February and subsequently entered the priority review pathway; JW Therapeutics also demonstrated strong momentum, with its NDA for relmacabtagene autoleucel injection being accepted by the CDE in June.

It remains uncertain which company will secure approval for China’s first CAR-T therapy. However, it is evident that JUNO Therapeutics, having fallen behind in the European and American markets, has reignited its competition with Kite Pharma, driven by the continuous progress of WuXi Juno.

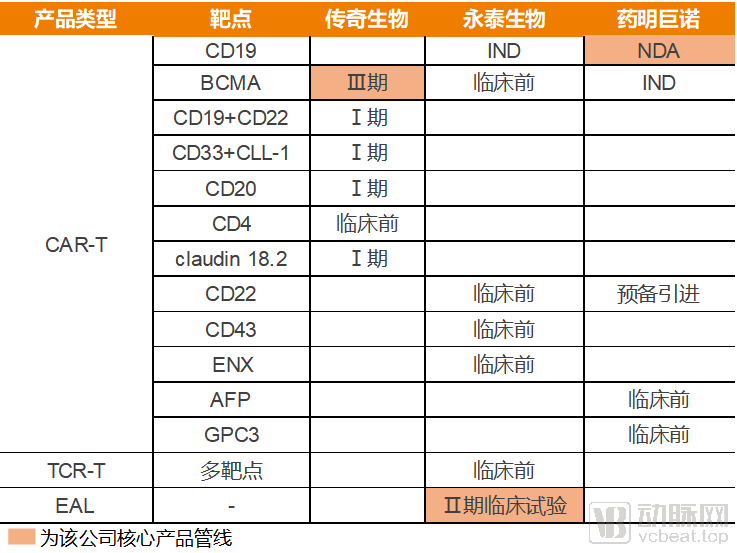

JW Therapeutics' Pipeline in Development

Returning to JW Therapeutics, the company’s current pipeline is entirely derived from in-licensed assets. This includes CD19- and BCMA-targeted products licensed from JUNO Therapeutics, as well as several AFP- and GPC3-targeted products licensed from Eureka Therapeutics.

Among the products targeting hematologic malignancy indications, most originate from JUNO Therapeutics, with the core product being Relma-cel (JWCAR029), which is JUNO’s JCAR017. Although JUNO completed a relatively comprehensive development process for this product abroad, it never received regulatory approval for marketing in overseas markets. WuXi Juno has carried out corresponding localization adaptations and advanced multiple domestic clinical trials. Currently, the New Drug Application (NDA) for this product has been submitted and accepted in China, suggesting that WuXi Juno’s first product may be the first to reach the Chinese market through its efforts.

Relma-cel is currently seeking marketing approval for third-line treatment of diffuse large B-cell lymphoma (DLBCL). In the completed Phase I and II clinical trials, Relma-cel successfully met the predefined primary endpoints, with an overall response rate (ORR) of 58.6% at three months. Regarding best overall response, the ORR and complete response (CR) rates reached 75.9% and 48.3%, respectively.

In addition, the relevant clinical trials for follicular lymphoma and mantle cell lymphoma have entered pivotal trial stages. Although JW Therapeutics did not disclose the early clinical trial results for these two indications in its prospectus, based on the previously released data from JUNO, their clinical value is no less than that of several already marketed products.

JW Therapeutics’ solid tumor pipeline was licensed-in from the innovative company Eureka.

Eureka Therapeutics, a cell therapy company founded by Chinese entrepreneurs, shares a significant history with JUNO Therapeutics. In January and June 2016, Eureka Therapeutics licensed the development and commercialization rights for two of its products to JUNO, targeting BCMA and MUC16, respectively. One of the three flagship products that WuXi Juno licensed from JUNO targets BCMA, which likely originated from Eureka Therapeutics.

JW Therapeutics’ Pipeline Candidates Potentially Subject to Further In-Licensing in the Future

JW Therapeutics holds the right of first refusal for the research, development, and commercialization in China of T-cell products constructed by JUNO. Consequently, as its product pipeline advances, JW Therapeutics may continue to license additional drug pipelines from JUNO. Currently, products targeting popular antigens such as CD22, HER2, and MUC16 are under consideration by JW Therapeutics.

According to the prospectus disclosed by JW Therapeutics, the primary use of proceeds is focused on product registration filings and clinical development, with a portion of the funds allocated for future in-licensing opportunities. Therefore, it is estimated that JW Therapeutics will continue to advance at a steady pace consistent with its current development trajectory over the next few years.

From the development of the three companies that filed for IPOs in 2020, we can observe certain trends in the cell therapy industry.

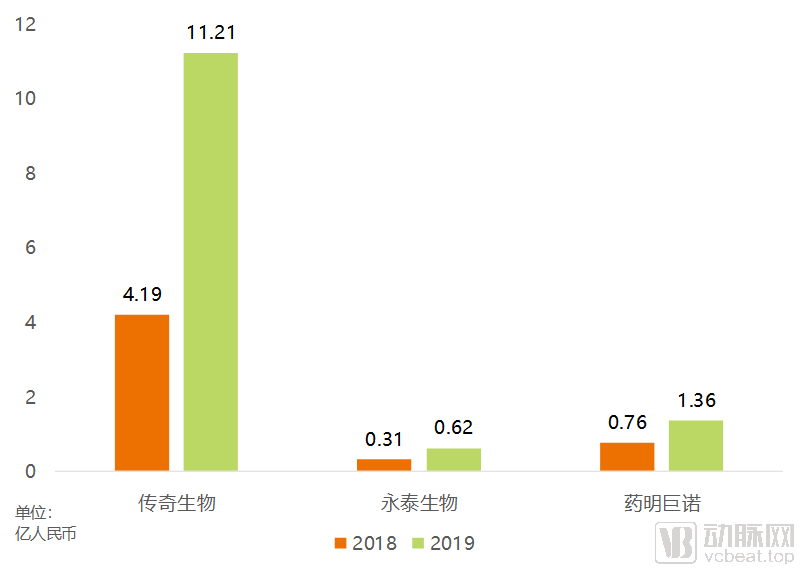

R&D Expenditures of Three Domestic Cell Therapy Companies Applying for IPO

In terms of R&D expenditure, among the three companies that have already gone public, Legend Biotech’s 2019 R&D spending, which exceeded RMB 1 billion, was far ahead of its peers. In contrast, Yatai Bio and WuXi Junuo had significantly lower R&D expenditures.

Yongtai Biopharma presents a unique case, as its CAR-T pipeline remains entirely in the preclinical stage. In terms of clinical trials, only its core product, EAL, is currently under development. This therapy primarily involves isolating, culturing, and reinfusing the patient’s own CD8+ T cells. Given its relatively low manufacturing cost, the associated clinical trial expenses are also easy to control. Consequently, this case lacks broad generalizability or reference value for the industry.

Legend Biotech’s substantial R&D expenditures stem not only from the development costs of the products themselves but, to a greater extent, from the extensive conduct of clinical trials. Its core product, LCAR-B38M, has one Phase III, three Phase II, and one Phase I clinical trial currently underway, while other pipeline candidates have also entered Phase I clinical studies. The simultaneous execution of more than 10 clinical trials inevitably results in significant R&D spending.

Legend Biotech has the confidence to make substantial investments in R&D, backed by its parent company GenScript and Janssen Pharmaceuticals. As Legend Biotech’s holding company, GenScript has consistently provided financial support to Legend Biotech in recent years. Meanwhile, Janssen Pharmaceuticals has entered into an agreement with Legend Biotech to jointly develop, manufacture, and commercialize LCAR-B38M. This collaboration alone included an upfront payment of $350 million, which was sufficient to cover Legend Biotech’s R&D expenditures for 2018–2019.

Turning to JW Therapeutics, first, the number of clinical trials is limited, with only a few studies on its core product, JWCAR029, currently underway; second, its products exhibit a high degree of maturity, as the core product has undergone extensive long-term development by JUNO Therapeutics; third, it benefits from the backing of WuXi AppTec, whose support as a top-tier CRO naturally helps JW Therapeutics further control costs. Under the influence of these multiple factors, JW Therapeutics’ R&D expenditures have consistently remained at a low level.

The situations of these two companies highlight the business model of cell therapy enterprises. The development of innovative drugs requires substantial capital investment.Given the massive capital investment required, reliance on VC/PE support alone is insufficient; startups must also seek greater support from the industry sector.Whether partnering with pharmaceutical giants to accelerate commercialization or collaborating with CROs/CDMOs to further control costs, both strategies represent optimal choices for innovative enterprises to mitigate risk. Eureka Therapeutics serves as a prime example: several products in its pipeline have been licensed out to JUNO Therapeutics and WuXi Juno, with upfront payments and future milestone payments providing the financial impetus for Eureka’s continued development.

Pipeline Overview of Three Companies Filing for IPO

Among the three companies with products currently on the market, their pipelines are notably diversified, with target overlap limited to only CD19, BCMA, and CD22.

This is precisely the situation currently facing CAR-T cell therapy. The first round of competition among Novartis, KITE, and JUNO around the CD19 target has so far resulted in the market approval of three products, attracting a large number of companies to enter the field of CAR-T cell therapy product development. However, there is limited clinical data available to guide target selection; apart from CD19, which has been clinically validated, most other targets are being explored through trial and error.

During the “crossing the river” phase, the BCMA target has begun to emerge as a standout through multi-party validation, with JUNO, Bluebird, and Legend Biotech successively announcing clinical trial results for their respective products. Notably, Legend Biotech’s LCAR-B38M achieved complete response (CR) rates exceeding 70% in multiple myeloma clinical trials conducted in both China and the United States, demonstrating strong commercial potential. Consequently, it is evident that the three companies that have filed for IPOs have all made substantial strategic investments in BCMA-targeted therapies.

However, there is no consensus on which target will become the next major hotspot after BCMA. Some believe that there is still significant room for development in the treatment of hematologic malignancies, others argue that new targets for solid tumors should be explored, while still others contend that product costs should be controlled to develop off-the-shelf UCAR-T products.

In such an environment, even industry giants like KITE appear somewhat uncertain. Although KITE’s newly approved product has demonstrated favorable clinical trial results in both mantle cell lymphoma and acute myeloid leukemia, it still targets established antigens, thereby limiting its long-term growth potential.

For startups, such an industry environment represents opportunities.At a time when established companies are grappling with uncertainty, startups have an opportunity to carve out a niche in the industry.Legend Biotech’s early strategic focus on the BCMA target for priority development has enabled its current position as a global leader.

Although CAR-T cell therapy products have entered the market phase in China, affordability remains a major hurdle for domestic patients seeking timely access to these treatments.

The high price tags of $475,000 for Kymriah and $373,000 for Yescarta in the United States impose a significant financial burden on patients. However, the U.S. commercial insurance system possesses sufficient financial strength to provide healthcare coverage for patients. Additionally, the Centers for Medicare & Medicaid Services (CMS) has already provided comprehensive coverage for CAR-T cell therapy.

However, in China, the payment aspect proves far more challenging. Although domestically listed products are priced lower than their foreign counterparts, they still represent a significant financial burden relative to the average per capita income in China.

We can estimate the pricing of CAR-T cell therapy products to be launched in China by drawing analogies with other innovative drug products. The per-vial price of the PD-1 monoclonal antibody Keytruda in China is half that in the United States; furthermore, with its “buy three, get three free” patient assistance program, the actual out-of-pocket cost for Keytruda in China is approximately one-quarter of its U.S. price.

Based on this ratio, the price of CAR-T cell therapy products to be launched in China in the future will also exceed 500,000 yuan.

So, who will bear this substantial cost? If patients are required to pay out-of-pocket, such a price would undoubtedly exacerbate the financial burden on their families. Conversely, if covered by medical insurance, it would impose a significant additional burden on the national healthcare insurance system.

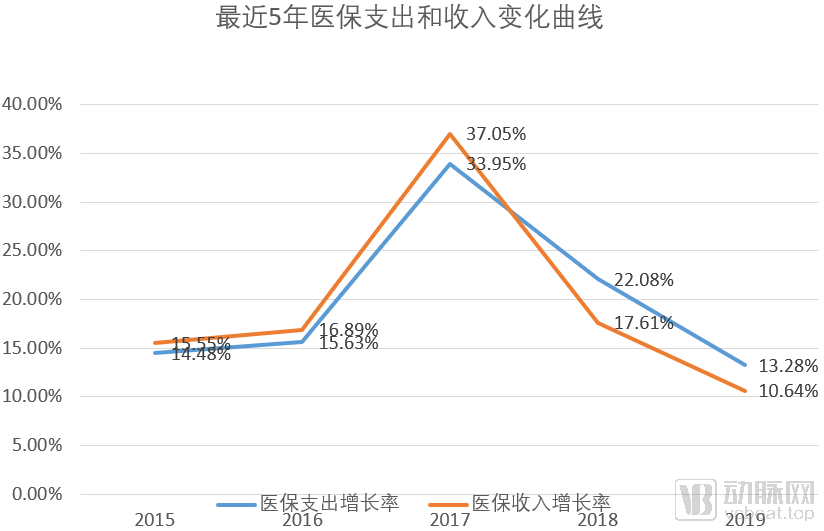

Changes in the Revenue and Expenditure of Medical Insurance in Recent Years

In recent years, the National Healthcare Security Administration (NHSA) has incorporated a large number of innovative drugs into its reimbursement list through price negotiations. Although expenditures have been curtailed through measures such as volume-based procurement and the “Two-Invoice System,” the growth rate of NHSA expenditures still exceeded that of revenues in 2018–2019. Under these circumstances, the NHSA is bound to exercise greater caution when adding new drugs to the reimbursement list in the future.

Payment for products is an issue that must be resolved as China’s pharmaceutical industry integrates with international standards.The Challenges Facing CAR-T: A Microcosm of the Current State of China’s Pharmaceutical Industry

Over the past two years, driven by policy initiatives, new drugs from around the world have accelerated their entry into the Chinese market, while an increasing number of domestically produced innovative drugs have received regulatory approval. However, the high prices of these innovative therapies have placed health insurance authorities in a difficult position. This year, nusinersen injection, a new drug for spinal muscular atrophy (SMA) priced at RMB 700,000 per dose, suddenly became a trending topic on social media. According to relevant responses from the National Healthcare Security Administration (NHSA), the NHSA had engaged in negotiations with Biogen shortly after the drug’s market launch but failed to reach an agreement.

For new drug products that address patients’ essential needs, the bargaining power of the national medical insurance scheme is very limited, and it must also comprehensively consider its own payment capacity.

Overall, it remains challenging to rely on medical insurance to address the reimbursement of high-priced innovative products for the time being.

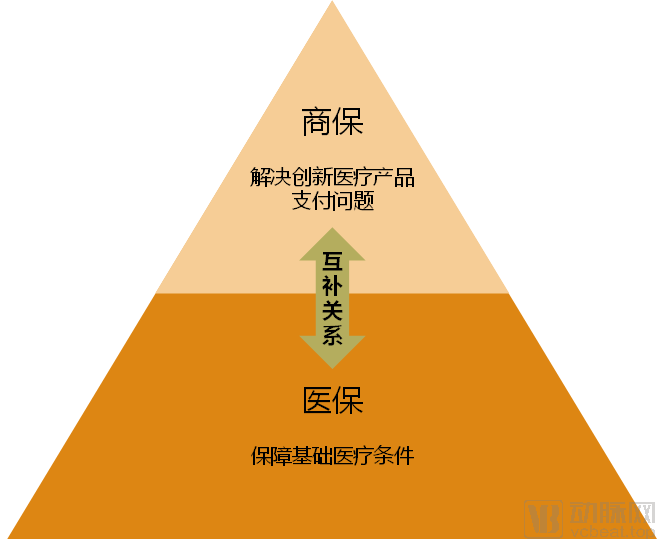

In the past two years, basic medical insurance has also begun to encourage the rapid development of commercial health insurance.

The Complementary Relationship Between Commercial Health Insurance and Public Medical Insurance

Public health insurance and commercial health insurance are not in competition with each other, nor is their relationship purely collaborative; rather, they primarily serve as complementary forces. The key role of commercial health insurance lies in covering medical products that public health insurance cannot afford to reimburse, particularly addressing payment issues for high-cost innovative medical products. Through this synergy, where public health insurance provides basic coverage and commercial health insurance covers “premium” services, comprehensive coverage across the healthcare industry can be achieved.

We have seen the emergence of many high-quality insurance products for specialty drugs, critical illnesses, and oncology medications, which are gradually addressing the limitations of basic medical insurance in covering patients with serious and rare diseases. Once CAR-T cell therapy is approved, it is highly likely to be included in these critical illness and major medical insurance plans.

Although the road ahead will still be bumpy, we are encouraged by the achievements made by the cell therapy industry over the past six months. We believe that with the transformation of China's healthcare industry, the challenges facing CAR-T in research and development and reimbursement will also be resolved.