Sansure Biotech Debuts on STAR Market with Over RMB 50 Billion Valuation, Reports 11-Fold H1 Revenue Surge Driven by Pandemic Response

As Sansure Biotech has shouldered a significant portion of the production of nucleic acid diagnostic reagents for SARS-CoV-2 during the COVID-19 pandemic, its path to listing on the STAR Market has attracted considerable attention. Driven by sales of SARS-CoV-2 nucleic acid detection reagents, Sansure Biotech’s performance surged in the first half of 2020, with revenue exceeding RMB 2.1 billion, representing a year-on-year increase of 1,159.39%. By contrast, the company’s total annual revenue in 2019 was only RMB 360 million.

On January 28 this year, Sansure Biotech’s COVID-19 nucleic acid diagnostic kit received regulatory approval. Two months later, while the domestic epidemic was still at its peak, Sansure Biotech filed for an initial public offering (IPO) on the STAR Market. Now that the global pandemic has entered a stable phase and COVID-19 nucleic acid testing has become a routine demand, will the “first stock of the anti-epidemic era” gain recognition in the secondary market?

Today, investors in the STAR Market have provided their answer.

Sansure Biotech’s IPO price was RMB 50.48 per share, with an opening price of RMB 151. As of press time, the stock price stood at RMB 136.66, representing a gain of 170.72%, and its total market capitalization exceeded RMB 50 billion. According to the prospectus, Sansure Biotech publicly issued 40 million shares in this offering, bringing the total share capital to 400 million shares post-issuance. The funds raised willFor three projects: the construction of a production base for a precision intelligent molecular diagnostics system, the upgrade and construction of an R&D center, and the upgrade and expansion of the marketing network and information technology infrastructure.

Since its establishment in 2008, Sansure Biotech has evolved into a comprehensive provider of in vitro diagnostic (IVD) solutions, with nucleic acid reagents as its core business, complemented by instruments and third-party medical diagnostic services. Sansure Biotech’s greatest strength lies in nucleic acid reagents; it holds a leading market share in hepatitis prevention and control diagnostic reagents and has established a solid market foundation in other areas, including reproductive tract infections and genetics, as well as respiratory tract infections. Sansure Biotech’s products are used in more than 2,000 medical institutions across China and have reached over 120 countries and regions worldwide.

Sansure Biotech is also actively expanding into other niche segments of molecular diagnostics, extending its reach into areas such as early cancer screening, personalized oncology medication, chronic disease management, public health, animal disease prevention and control, and scientific research services.

Among the numerous domestic nucleic acid reagent manufacturers, how did Sansure Biotech emerge as a vital force in the fight against the pandemic? Beyond its COVID-19 nucleic acid diagnostic kits, what other notable achievements has Sansure Biotech made in the field of molecular diagnostics? VCBeat (WeChat ID: vcbeat) has compiled an overview.

From RMB 300 million to RMB 2.1 billion: Sansure Biotech Achieved a Performance Leap in Just Six Months. This was because Sansure Biotech was a leading domestic producer of COVID-19 nucleic acid diagnostic reagents in the first half of the year. From January to September 2020, COVID-19 nucleic acid test kits directly generated RMB 1.73 billion in net profit for Sansure Biotech.

As of June 30, 2020, Sansure Biotech had supplied a total of nearly 38.8513 million person-tests of COVID-19 nucleic acid testing kits domestically and internationally (of which approximately 13.8024 million person-tests were supplied to the international market). This means that the number of COVID-19 nucleic acid testing kits supplied by Sansure Biotech to the domestic market was 25.0489 million tests.

What does this data mean? VCBeat estimates that Sansure Biotech accounted for nearly one-quarter of China’s market share for COVID-19 nucleic acid diagnostic reagents in the first half of the year.

In the first half of the year, there is no publicly available accurate data on the number of COVID-19 nucleic acid tests conducted in China. However, KingMed Diagnostics stated that as of June 30, 2020, it had completed more than 10 million COVID-19 nucleic acid tests, accounting for approximately one-tenth of the national total during the same period. It can be estimated that the volume of COVID-19 nucleic acid testing in China during the first half of the year was around 100 million.

Meanwhile, Sansure Biotech’s domestic shipments of COVID-19 nucleic acid test kits reached approximately 25.04 million units. Based on this estimate, Sansure Biotech alone accounted for one-quarter of the market share in the lucrative COVID-19 nucleic acid testing kit sector.

Sansure Biotech’s performance during the COVID-19 pandemic was also relatively outstanding compared to its peers. Taking Orient Gene as an example, in the first half of 2020, driven by a surge in nucleic acid testing demand for epidemic prevention and control, Orient Gene recorded revenues of RMB 828 million, a year-on-year increase of 388.05%, with net profit attributable to shareholders soaring by 1,477.45% year on year to reach RMB 524 million.

Sansure Biotech’s Financial Data in Recent Years

Sansure Biotech’s rapid emergence during the pandemic response is closely tied to its long-standing R&D capabilities and its production and marketing network.

Following the outbreak of the COVID-19 pandemic, Sansure Biotech rapidly developed a nucleic acid detection kit for the novel coronavirus, becoming one of the first six companies in China to obtain market approval for its novel coronavirus testing products.

During the COVID-19 pandemic response, Sansure Biotech leveraged its established production, marketing, and service networks to rapidly supply its products to the front lines of epidemic prevention and control in more than 30 provinces, municipalities, and autonomous regions across China, including Hubei, Hunan, Beijing, and Shanghai.

Both in China and overseas, Sansure Biotech has seized the first-mover advantage in COVID-19 nucleic acid testing. However, the performance growth driven by the pandemic is incidental; currently, it appears that Sansure Biotech may struggle to sustain the same high growth rate in the second half of the year as it did in the first half.

First, the peak of the domestic epidemic has passed, and multiple companies have launched novel coronavirus testing kits. Currently, there are 43 novel coronavirus testing kits registered in China (including 21 nucleic acid testing kits). Meanwhile, multinational corporations such as Roche and Abbott are expanding the production capacity of their novel coronavirus testing products to meet market demand.

In addition to intensifying competition, provinces have begun implementing centralized procurement for COVID-19 testing products, which will also compress the profit margins of COVID-19 test reagents. Moreover, Sansure Biotech has not yet won any bids in these centralized procurement programs across various regions.

Sansure Biotech participated in the centralized procurement bidding for COVID-19 testing reagents in provinces such as Heilongjiang, Fujian, Guizhou, Shanxi, Gansu, and Henan. However, due to the need to protect international market prices, Sansure Biotech’s bid prices were relatively high, resulting in its failure to win bids in the domestic centralized procurement. Consequently, the sales of Sansure Biotech’s COVID-19 testing reagents are expected to be somewhat affected in the second half of the year.

In response, Sansure Biotech’s solution is to shift the sales focus of its COVID-19 testing reagents to overseas markets.From January to September this year, one-third of Sansure Biotech's COVID-19 diagnostic reagents were sold to overseas markets.In overseas markets, Sansure Biotech’s COVID-19 nucleic acid diagnostic reagents have been primarily exported to dozens of countries and regions worldwide, including Italy, Spain, and the Philippines. Sansure Biotech’s COVID-19 nucleic acid diagnostic reagents have also obtained Emergency Use Authorization (EUA) from the U.S. Food and Drug Administration (FDA), making it the sixth Chinese company to receive FDA EUA certification. In certain countries globally, the pandemic is still in a phase of spread; while overseas sales may support the continued growth of Sansure Biotech’s performance, they are unlikely to sustain explosive growth.

Had the COVID-19 pandemic not occurred, Sansure Biotech’s push for a listing on the STAR Market would have been more noteworthy for its leading position in the viral hepatitis market.

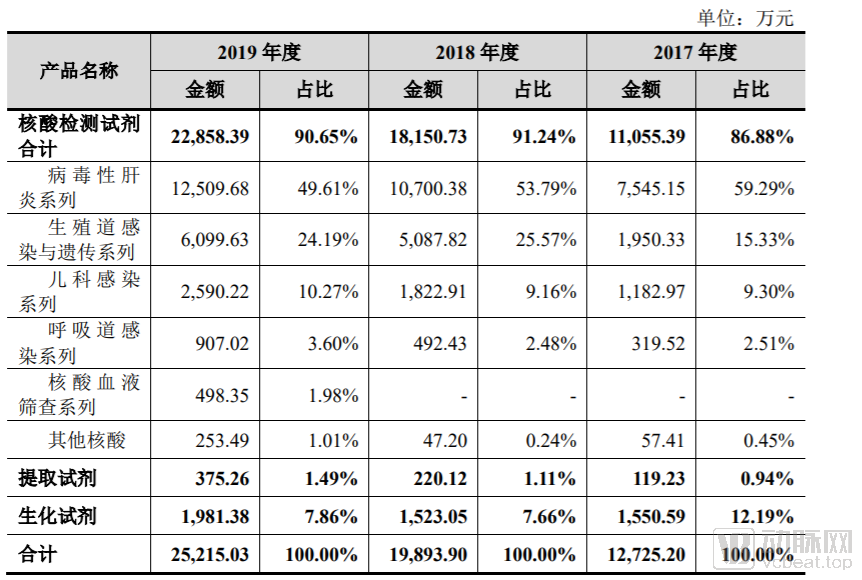

In terms of core revenue composition, Sansure Biotech’s primary income is derived from nucleic acid testing reagents, instruments, and testing services. Among these, nucleic acid reagent services account for over 60%. The markets where Sansure Biotech holds a dominant position in nucleic acid reagents includeViral Hepatitis, HPV Testing, Pediatric and Respiratory Tract Infections, Blood Screening.

In the field of viral hepatitis, Sansure Biotech’s series of nucleic acid testing products for hepatitis viruses are widely used in major tertiary hospitals across China, holding a leading market share in the industry. As the first domestically produced high-sensitivity quantitative diagnostic product for hepatitis launched in China, its detection sensitivity is significantly higher than that of similar domestic products at the time, driving the overall performance improvement of hepatitis virus nucleic acid quantitative testing products in China.

According to data disclosed in the prospectus, the revenue from the viral hepatitis series of reagents amounted to RMB 75.4515 million, RMB 107 million, and RMB 125 million in 2017, 2018, and 2019, respectively, accounting for 59.29%, 53.79%, and 49.61% of the total reagent revenue in those years. Based on overall operating revenue, the viral hepatitis series of reagents alone contributed nearly one-third of Sansure Biotech’s total income.

Revenue from Sansure Biotech's Reagent Products

In addition to the field of viral hepatitis, Sansure Biotech’s advantages in the reagent market also include HPV testing and respiratory infection testing.

In the fields of reproductive health and genetic testing, Sansure Biotech’s “High-Risk Human Papillomavirus Nucleic Acid (Genotyping) Detection Kit” has been progressively deployed in the “Two-Cancer Screening” programs across multiple provinces and municipalities, including Xinjiang, Yunnan, Gansu, Shanxi, and Shaanxi, and is currently utilized in hundreds of clinical hospitals nationwide. Leading multinational corporations in the HPV testing market include Roche, Hologic, Qiagen, and BD, while prominent domestic companies include Da An Gene, Hybribio, and ZJ Bio-Tech.

In the field of pediatric infections and respiratory tract infections, Sansure Biotech has developed nucleic acid detection reagents for hand-foot-and-mouth disease enteroviruses, Epstein-Barr virus (EBV), cytomegalovirus (CMV), Mycoplasma pneumoniae, Mycobacterium tuberculosis, and influenza A virus.

In fact, within the overall market landscape of molecular diagnostic reagents, the sector in which Sansure Biotech operates is characterized by intense competition. Molecular diagnostic kits, including nucleic acid extraction kits and nucleic acid detection kits, have largely been localized in China. The number of domestic manufacturers producing nucleic acid detection reagents for common viruses such as hepatitis B virus (HBV), hepatitis C virus (HCV), and human immunodeficiency virus (HIV) far exceeds that of foreign manufacturers. Nucleic acid detection kits for common diseases such as influenza A, B, and C are relatively mature, with numerous competing manufacturers, and are almost exclusively domestic brands.

Another major battleground for Sansure Biotech is molecular diagnostic instruments. In the domestic market, main products include nucleic acid extractors, PCR amplifiers, nucleic acid molecular hybridization instruments, gene chip analyzers, and gene sequencers.

In the mid-range instrument sector, where technical barriers are relatively easier to overcome, domestic alternatives such as nucleic acid extractors, PCR amplifiers, nucleic acid molecular hybridization instruments, and gene chip analyzers have matured, with domestically produced products capturing the majority of the market.

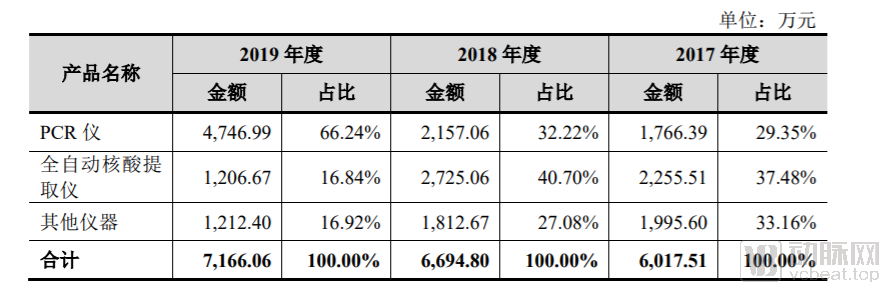

However, Sansure Biotech’s competitive edge in the instrumentation segment is not particularly prominent. According to revenue data from its instrument business, PCR instruments account for the largest share; yet, Sansure Biotech’s PCR products are primarily real-time quantitative PCR instruments sourced externally from Life Technologies, a subsidiary of Thermo Fisher Scientific.

In contrast, Sansure Biotech’s self-manufactured instrument products comprise a series of automated nucleic acid extraction systems, available in two models: Natch S and Natch CS. The main components of the Natch S fully automated nucleic acid extractor produced by Sansure Biotech are imported from TECAN, resulting in a higher price point, and the product is primarily targeted at large public hospitals.

In terms of operating revenue, the revenue from Sansure Biotech’s automated nucleic acid extraction instruments has slowed down. Sansure Biotech attributes this to the gradual saturation of demand from its existing customer base after two years of sales.

Revenue from Sansure Biotech's Instrument Products

It is evident that Sansure Biotech’s influence in the instrument sector lags behind its standing in the reagent market. However, the company has essentially established an integrated business model encompassing reagents, instruments, and testing services, laying a foundation for its future development into a comprehensive platform.

Sansure Biotech’s testing services primarily consist of two business segments: third-party medical laboratory services and scientific research services. The revenues from 2017 to 2019 were RMB 32.1068 million, RMB 31.8626 million, and RMB 35.5242 million, respectively. Among Sansure Biotech’s three business lines, testing services generated the lowest revenue.

Dr. Dai Lizhong, founder of Sansure Biotech, was born in Ningxiang, Hunan Province. After completing his postdoctoral research at the Massachusetts Institute of Technology (MIT), he served as Chief Scientist of the core R&D team at Gen-Probe, the world’s largest nucleic acid reagent company. In this role, he engaged in the development of nucleic acid reagents, addressed key technical challenges related to enzyme-based reagents, and led and participated in the technological development and upgrading of multiple major nucleic acid diagnostic products.

In 1993, Dai Lizhong graduated with honors from Peking University with a major in Chemical Engineering and went on to Princeton University in the United States amid the wave of overseas study. Years later, he chose to return to China to start a business, focusing on biological detection technology for infectious diseases, with hepatitis B as the first targeted disease for application.

This marked the starting point for Sansure Biotech, which was founded in 2008 by its returnee entrepreneur as a nucleic acid reagent company; however, the company encountered numerous difficulties.

Dai Lizhong, founder of Sansure Biotech, stated in an interview that after leaving his position as a core R&D researcher at Gen-Probe, the world’s largest nucleic acid reagent company, to return to China and start his own business, he gained a profound understanding of the differences between the in vitro diagnostic (IVD) industries in China and the United States. He noted that the regulatory framework for biological reagents abroad is well-defined, allowing many factors to be accurately predicted. For instance, developing an infectious disease reagent typically takes about five years and requires an investment of $100–200 million. The situation in China was different; at that time, the industry was still immature and faced numerous challenges.

During the development of Sansure Biotech, the most significant negative incident involved former shareholder Li Chikang, who privately forged company seals and fabricated the signature of legal representative Dai Lizhong. In the name of Sansure Limited, he executed a Guarantee Contract with Chang’an Trust regarding a trust loan for Boya Eye Hospital, with Sansure Limited serving as one of multiple parties providing mortgages and guarantees. Furthermore, Li Chikang, in the names of his affiliated companies such as Boya Eye Hospital and Xiangyu Food, borrowed hundreds of millions from the Hunan Branch of Bank of Communications and the Yuhua District Sub-branch of Agricultural Bank of China in Changsha (hereinafter referred to as “Agricultural Bank”).

To resolve the RMB 113 million in debts owed to Bank of Communications and Agricultural Bank of China, as well as the RMB 110 million debt owed to Chang’an International Trust, and to eliminate the adverse impact of these liabilities on the Company, Sansure Biotech initiated two debt restructuring programs in May 2017.

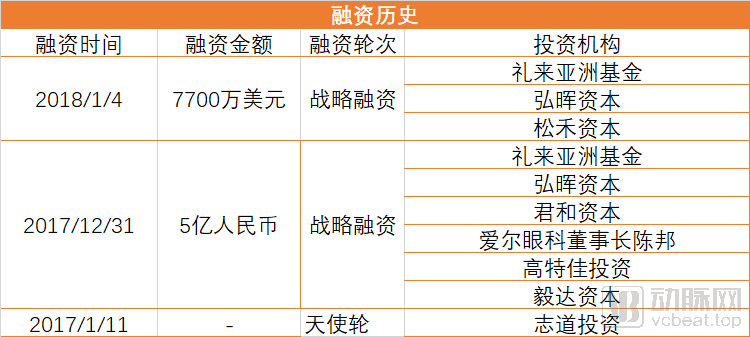

After 2017, Sansure Biotech also began to secure external financing, putting its development on the fast track.

Jiang Yanye, spokesperson for Honghui Capital, stated that when the firm decided to invest in Sansure Biotech, the company was still in the early stages of rapid growth. In that year, it reported operating revenue of RMB 225 million and a net loss of RMB 10.65 million. However, Honghui recognized the substantial growth potential in the molecular diagnostics sector, driven by significant unmet clinical needs and considerable room for improvement and enhancement of existing products.

“We believe the molecular diagnostics sector has significant growth potential, with its applications and scenarios continuously expanding. Founder Dai Lizhong possesses an outstanding professional background, ambitious entrepreneurial vision, and pragmatic execution capabilities. Honghui was deeply attracted by the team’s technological innovation and execution prowess, the differentiated competitiveness and quality advantages of its products, as well as the synergy and diversity of its product portfolio,” added Jiang Yanye, spokesperson for Honghui Capital.

Yu Jianlin, Executive Partner at GTJA Investment, recalled:“At the time of investing in Sansure Biotech, the domestic market share for molecular diagnostics was only 5%, significantly lower than the 20% seen in developed countries in Europe and the United States. The high-end molecular diagnostics segment was devoid of Chinese manufacturers, being dominated by foreign companies such as Roche, Qiagen, bioMérieux, and Abbott. Insufficient technological capability was prevalent at that time, positioning molecular diagnostics firms with advanced technologies to break through this barrier.

Gao Te Jia observes that among domestic PCR companies, Sansure Biotech holds a leading position as an industry frontrunner, with relatively high barriers to entry. Molecular (nucleic acid) diagnostics represent a more advanced segment within the overall IVD field, offering greater reliability and precision compared to traditional biochemical and immunodiagnostic methods. Molecular diagnostics entail higher technical thresholds, imposing stricter requirements on both manufacturing processes and the technical proficiency of operators. Generally, the technological complexity in the IVD sector increases progressively in the order of biochemistry, immunodiagnostics, nucleic acid testing, and sequencing.

Sansure Biotech possesses world-class nucleic acid extraction technology (kits), with its magnetic bead method demonstrating sensitivity and precision approaching the international leading level (Roche). Its “one-step” detection assay is on par with the magnetic bead methods employed by other domestic manufacturers. Sansure Biotech has achieved room-temperature nucleic acid extraction, eliminating the boiling step required in traditional nucleic acid lysis and extraction processes. Its independently developed “nucleic acid release agent” holds fully independent intellectual property rights and is unique within the industry.”

After a comprehensive assessment of the market potential for molecular diagnostics and the technologies possessed by Sansure, GaoTeJia invested in Sansure Biotech.

Yu Jianlin, Executive Partner at GTJA Investment, stated, “During the COVID-19 pandemic this year, Sansure’s technological platform and rapid response further validated this point. The Novel Coronavirus (2019-nCoV) Nucleic Acid Detection Kit (Fluorescent PCR Method), developed and manufactured by Sansure Biotech, received support from the Ministry of Science and Technology’s emergency special project. Leveraging Sansure Biotech’s proprietary ‘One-Step RNA’ technology, the product is adaptable to various scenarios, easy to operate, and delivers results within 30 minutes. It was among the first batch of products in China to obtain market approval and has been progressively launched into global markets.”

Sansure Biotech Financing History

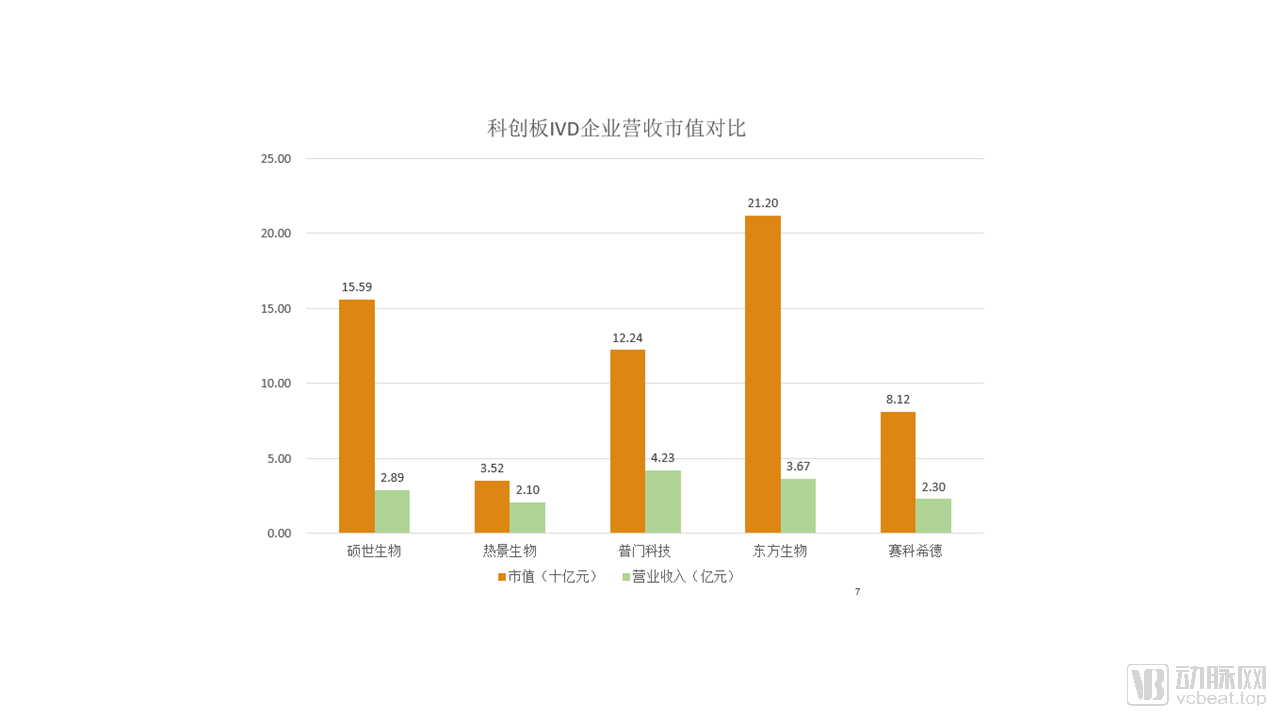

Since the launch of the STAR Market over a year ago, multiple companies in the in vitro diagnostics (IVD) sector have gone public, including Shuo Shi Biotech, Hotgen Biotech, Pumen Technology, Orient Gene, and Succeeder. In terms of market capitalization, Orient Gene exceeds RMB 20 billion; Shuo Shi Biotech surpasses RMB 15 billion; Succeeder stands at approximately RMB 8 billion; and Hotgen Biotech is valued at around RMB 3.5 billion. (Data as of August 21, 2020)

Data as of August 21, 2020

From the perspective of business distribution, the in vitro diagnostic (IVD) companies listed on the STAR Market are primarily engaged in molecular diagnostics and point-of-care testing (POCT). Based on differences in the technical principles and methods used for clinical laboratory tests, IVD products can be categorized into various types, including biochemical diagnostics, immunoassay diagnostics, molecular diagnostics, hematology diagnostics, and microbiology diagnostics. Among these, biochemical diagnostics, immunoassay diagnostics, and molecular diagnostics currently constitute the three major segments of the IVD industry.

In recent years, China’s in vitro diagnostics (IVD) market has been dominated by three major segments: immunoassay diagnostics (approximately 38%), clinical chemistry diagnostics (approximately 19%), and molecular diagnostics (approximately 15%). Together, these three categories account for over 70% of the total market share. Among them, immunoassay diagnostics currently represents the largest segment, while molecular diagnostics is the fastest-growing segment, with its market share continuing to rise rapidly.

From a segment-specific perspective, Hotgen Biotech’s core business is point-of-care testing (POCT), with its main products being blood gas analysis assays. In 2019, Hotgen Biotech reported operating revenue of RMB 210 million, representing a year-on-year increase of 12.45%; the company’s net profit attributable to shareholders of the parent company amounted to RMB 33.88 million, a year-on-year decrease of 29.6%.

Bioperfectus Technologies’ core business focuses on infectious disease testing and HPV detection. Its main products include nucleic acid test kits for Influenza A virus, respiratory panel assays, and an HPV genotyping and quantitative detection system. In 2019, Bioperfectus Technologies reported operating revenue of RMB 280 million.

Oriental Gene’s primary sources of revenue and profit are POCT (point-of-care testing) diagnostic reagents, with infectious disease testing and drug abuse testing constituting its two core product lines. In 2019, Oriental Gene reported operating revenue of RMB 367 million.

Sysmex's primary market is in vitro diagnostics for thrombosis and hemostasis, with Sysmex generating RMB 220 million in revenue in 2019.

It is evident that most in vitro diagnostic (IVD) companies listed on the STAR Market are leaders in their respective niche segments. Early-stage startups often achieve breakthroughs in a single niche, and it takes time for them to evolve into comprehensive platforms. The STAR Market has expanded listing opportunities for the IVD industry, enabling these niche segment leaders to access the secondary market.

Regarding the significance of the STAR Market, Jiang Yanye, spokesperson for Honghui Capital, also stated that the emergence of the STAR Market has accelerated the listing process for “hard” tech and innovative enterprises. It has provided strong support for these companies to enter the secondary market as soon as possible, enhance their brand influence and R&D investment, and thereby achieve leapfrog development.

Yu Jianlin, Executive Partner at GTJA Investment, stated, “In vitro diagnostics (IVD) have garnered significant attention during the current epidemic, with unprecedented enthusiasm from the capital market toward IVD companies. Sansure Biotech is the fifth IVD company listed on the STAR Market, and there are currently 10 other IVD enterprises in the process of applying for listing on the board.”The STAR Market shows a stronger preference for companies in the field of technological innovation that achieve breakthroughs in detection accuracy, speed, cost, and automation, thereby improving detection efficiency while offering greater convenience and cost-effectiveness.

As China’s in vitro diagnostics (IVD) industry rises rapidly, it also faces intense competition. It is common for IVD companies to offer relatively simple products with low revenue and thin profit margins. The STAR Market has provided a breakthrough and implementation path for the Shanghai Stock Exchange to enhance its inclusivity, enabling IVD companies that previously did not meet listing standards to cross the threshold for public listing.

IVD companies with strong technical capabilities and stable products can significantly narrow the current gap in per capita diagnostic spending between China ($7) and the United States ($70) by leveraging capital markets to increase R&D investment and expand market presence. The dividends brought by the STAR Market have only just begun to unfold.