Arterio Intelligence Releases '2020 Global Digital Health Industry Development Outlook' Ahead of IPO Filing

From August 21 to 23, 2020, the “2020 Inaugural China Internet Hospital Conference,” hosted by the Internet Hospital Branch of the Chinese Research Hospital Association, was held in Zhuhai. Hot topics included the development of internet healthcare in the post-pandemic era, medical insurance and commercial insurance payment mechanisms, as well as artificial intelligence, medical big data, and information security.

VBInsight released the “2020 Outlook on Global Digital Health Industry Development Trends” at the forum. Below is the transcript of Liu Hui, General Manager of VBInsight’s speech at the event.

Key Milestones in the Development of Global Digital Health

Mobile healthcare, e-health, m-health... Over the past few years, we have witnessed multiple iterations of these concepts.

The term “Digital Health” emerged around 2010, supplanting earlier concepts such as E-health and M-health. In the same year, the renowned U.S. incubator and investment firm Rock Health was established.

In 2016, the concept of Digital Health abroad gradually became clearer and more unified, largely due to the World Health Organization (WHO) introducing the term "Digital Health" in its official documents for the first time.

In 2017, the U.S. FDA released its Digital Health Innovation Action Plan for the coming years, established a dedicated section, and launched a specialized certification pathway for digital health products.

After years of development, a broad consensus on Digital Health has been reached within the industry. In 2018, the World Health Organization (WHO) released guidelines for digital health, aiming to standardize the terminology and context used in describing and implementing digital technologies in the healthcare sector.

VBInsightThis paper traces the evolution of relevant concepts, synthesizes descriptions from various organizations, and defines “Digital Health” as an industrial ecosystem that collects, stores, analyzes, and transmits diverse data from consumers and patients in both daily life and clinical settings, thereby providing users with health and medical products and services across their entire lifecycle.

VBInsight has established an industry information monitoring system that tracks and records nearly 1,000 industry events daily. We have observed:

I. One of the 2020 Trends in Global Digital Health: Capital Pulse

In terms of the overall trend of global venture capital investment in the healthcare sector over the past decade, 2014–2016 marked the first upswing, coinciding with the nascent stage of telemedicine. Investment peaked in 2018 before declining sharply.

In 2020, impacted by the pandemic, investment and financing in the healthcare sector showed signs of recovery, with numerous large-scale funding rounds occurring. However, the overall number of deals struggled to match the high levels seen in previous years. This indicates that, on one hand, a significant number of startups are fading from view. On the other hand, leading companies demonstrate a pronounced ability to attract capital, most being in the later stages of financing or even already listed, which signifies that their business models have been proven viable and gained market recognition.

The digital health sector is the second most active area, after biopharmaceuticals.

In the first half of 2020, the global digital health industry completed 309 financing deals, totaling RMB 44.5 billion. The objective impact of the global COVID-19 pandemic, coupled with the strong performance of telemedicine companies in the secondary market since the outbreak, has further accelerated innovation and financing activities in the digital health sector, suggesting that a new wave of digital health investment may be underway.

By analyzing the relevant data of the companies in the figure,VBInsightKey Findings:

1. The top 10 companies are distributed across various healthcare services, with the commonality of centering on digital capabilities as their core and providing services centered around digitalization.

2. Most of them were established between 2013 and 2015, have progressed beyond Series C financing, secured single-round investments exceeding USD 100 million, and joined the ranks of unicorns.

3. Traditional services, augmented with digital capabilities, offer greater potential for innovation. For instance, Alto, ranked second, is a digital pharmacy based in California, USA, whose core business revolves around providing medication services and personalized delivery to patients.

4. Telemedicine, spurred by the pandemic, is poised for another wave of rapid growth. For instance, American Well, a long-established player, has secured a new round of financing after gaining favor from pharmaceutical corporate venture capital (CVC) arms after many years. Another notable recent development is Teladoc’s acquisition of Livongo.

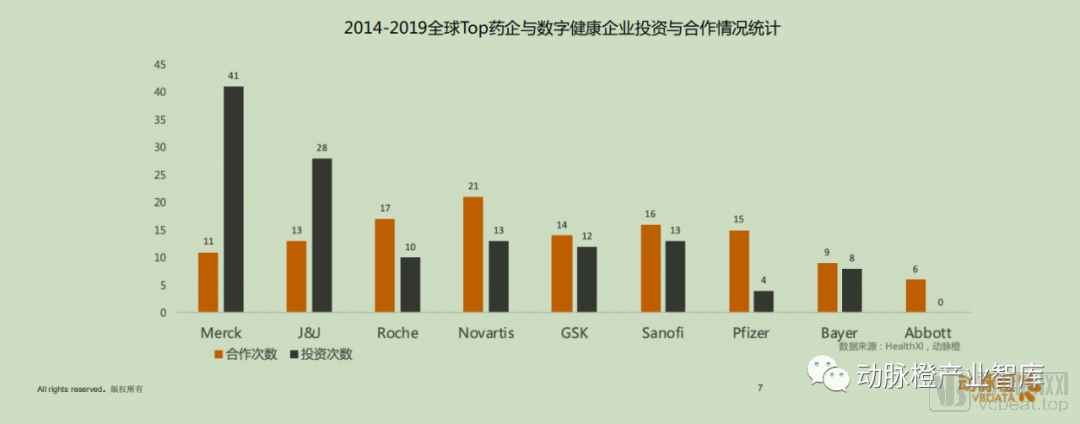

II. The Second Trend in Global Digital Health 2020: Pharmaceutical Innovation

Annual reports from the world’s leading pharmaceutical companies have all highlighted digital transformation in recent years.

By counting the number of collaborations or investments with digital health companies worldwide by the top-ranked pharmaceutical companies globally over the past five years,VBInsightFindings:

1) Major global pharmaceutical companies are entering the digital health sector through R&D collaborations, commercial partnerships, and investments and mergers and acquisitions, with a focus on digital therapeutics products and services for specific disease subtypes.

2) The number of collaborations between pharmaceutical companies and digital health enterprises has increased fivefold.

3) Over the past five years, pharmaceutical companies have cumulatively invested in more than 100 digital health enterprises, with total investments exceeding $4 billion.

VBInsightIt is believed that:

1) In the future, pharmaceutical companies will undergo a significant paradigm shift in their product strategies, evolving from a traditional model of standalone drug sales to an integrated “drug + services” approach, with a focused emphasis on specific patient populations and disease areas.

2) The participation of pharmaceutical companies and related technology enterprises has also driven the development of digital therapeutics.

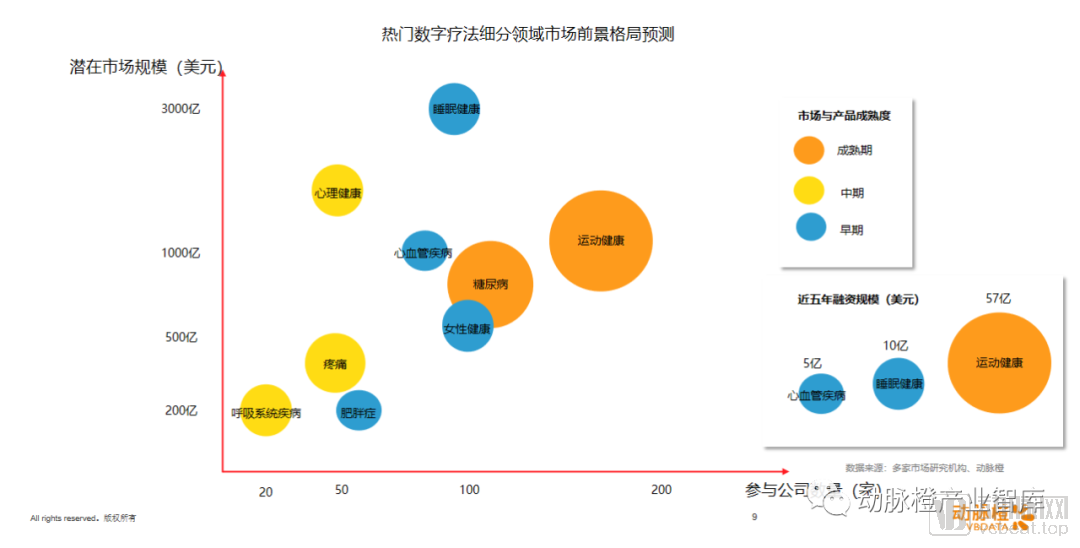

VBInsightAn analysis of data across four dimensions—corporate participation, financing status, product approval status, and research progress—yields the following conclusions:

1) The most mature areas of digital therapeutics currently are physical fitness and diabetes. Products, services, and even business models have been largely validated in these fields.

2) Digital therapeutics that have gained significant traction in the past two years, such as those for pain management, mental health, and asthma, have seen digital products achieve certification. Areas including women’s health, sleep disorders, and cardiovascular care remain in the early stages and may require approximately five years to reach maturity.

III. The Third Trend in Global Digital Health 2020: Cross-Industry Expansion by Tech Giants

VBInsightObserved:

1) IT companies, e-commerce platforms, and retail chain giants are actively expanding into the digital health sector.

2) The frequent cross-industry expansion by tech giants signals a shift in the balance of power within the traditional healthcare value chain.

The above-mentioned tech giants’ cross-industry forays into healthcare can be categorized into three major strategic approaches:

The first category, exemplified by Apple, possesses comprehensive capabilities in both hardware and software. Its engagement with payers and healthcare providers is primarily through technical collaborations. On the product side, it mainly relies on investing in and acquiring related companies to launch its own hardware products. The Apple Watch added ECG functionality last year and may introduce blood oxygen and sleep monitoring features this year. Notably, the two companies acquired by Apple specialize in respiratory and sleep monitoring.

The second category, exemplified by Google and Microsoft, primarily focuses on exporting technological capabilities. These companies collaborate with the largest U.S. chain healthcare groups or hundreds of hospitals to achieve data integration and advanced analytics. In comparison, Google has taken more aggressive steps, particularly through its acquisition of Fitbit, integration of DeepMind, and establishment of Google Health, suggesting a likely shift toward a hardware-software integrated model similar to Apple’s approach.

The third category involves comprehensive layout across the entire healthcare industry, with Amazon being a key player to watch. Since 2018, Amazon has significantly accelerated its moves in the healthcare sector: it co-founded Haven Healthcare with JPMorgan Chase and Berkshire Hathaway, acquired the pharmacy benefit manager (PBM) PillPack, and launched its own Amazon Care clinics last year. Downstream information technology vendors primarily adopt collaborative strategies. Walmart is also rapidly establishing primary care clinics, planning to operate around 20 locations by 2021. From logistics and distribution to payments and services, these efforts are all driven by their respective digital capabilities. In the future, we should not be surprised if Amazon and Walmart emerge as major healthcare brands.

IV. The Fourth Trend in Global Digital Health in 2020: Policy Breakthroughs

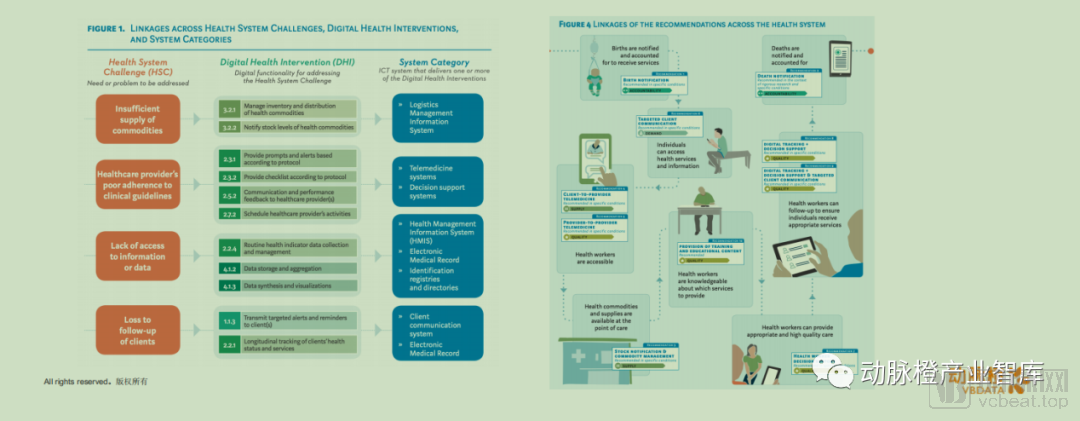

In 2018, the WHO released *Classification of Digital Health Interventions v1.0*, which clarifies how digital technologies can be leveraged to transform healthcare processes from four distinct perspectives: patients, healthcare providers, healthcare institutions, and data services.

In 2019, the WHO released the “Guideline: Recommendations on Digital Interventions for Health System Strengthening,” advocating for a correct understanding of the challenges facing existing healthcare systems and the rational application of corresponding digital technologies to ultimately establish a robust digital health system.

Data sourced from the VBInsight database.

*End of text

Through in-depth research on leading global digital health companies, VBInsight has mapped out the industry landscape covering 32 sub-sectors across three major domains of digital health, compiled a list of top enterprises, and provided a comprehensive analysis of industry trends from multiple perspectives, including policy, market dynamics, investment and financing, and product development. The institutional version of our product is now live; we welcome you to sign up for a trial.