The Future of Mutual Aid Platforms: Insights from Ant Group's White Paper on Network Mutual Aid Industry

In recent years, with the rapid development of health insurance, online mutual aid platforms, as a beneficial supplement to basic medical insurance and commercial health insurance, have also entered a period of rapid growth.

The “Opinions on Deepening the Reform of the Medical Security System,” issued by the Central Committee of the Communist Party of China and the State Council on February 25, 2020, stated that “by 2030, a medical security system will be fully established, with basic medical insurance as the mainstay, medical assistance as the safety net, and supplementary medical insurance, commercial health insurance, charitable donations, and mutual medical aid developing in concert,” thereby incorporating “mutual medical aid” into the medical security system framework.

So, where is the future for online mutual aid platforms that integrate innovative digital technologies such as the internet and fintech? This article will predict their future trends by analyzing the current status and data of these platforms.

Online mutual aid refers to a protection model that leverages the internet’s information-matching capabilities and digital technologies to address information asymmetry and trust issues among members. It brings together individuals with homogeneous risks and similar protection needs, who mutually assist one another and share each other’s health-related financial losses through formal agreements.

The defining feature of online mutual aid is leveraging digital technologies for platform user acquisition and infrastructure development. By utilizing the internet, big data, and other digital tools to reduce operational costs, these platforms charge users only a 6%–10% management fee, thereby lowering the cost barrier for health protection products and ultimately fulfilling the original intent of pure mutual assistance.

In 2011, with the emergence of Kang’ai Mutual Aid Society (formerly the Anti-Cancer Mutual Aid Society), China’s online mutual aid industry began to take root.

Since 2018, tech giants such as Ant Financial, Meituan, Didi, Baidu, and 360 have successively entered the market, bringing about a qualitative transformation to the online mutual aid industry. Leading platforms like Xianghubao (Mutual Treasure) and Shuidi Mutual Aid have gradually developed relatively mature operational models.

By the end of 2019, dozens of online mutual aid platforms in China had attracted 150 million participants, providing assistance to approximately 40,000 individuals throughout the year, with total mutual aid funds exceeding RMB 5 billion. In November 2019, Xianghubao became the first platform in the industry to surpass 100 million members.

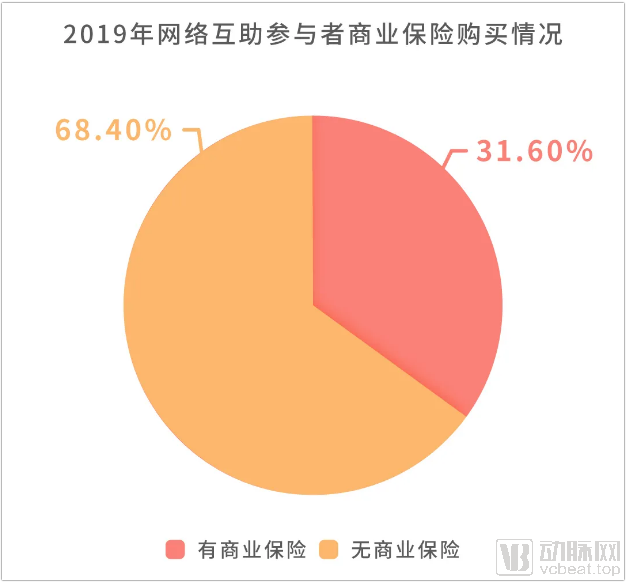

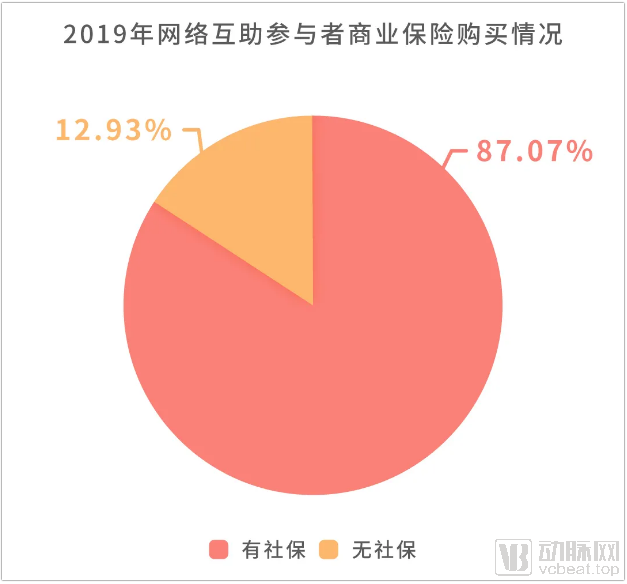

First, online mutual aid serves as a beneficial supplement to both social medical insurance and commercial health insurance. According to the "Report on the Development Index of Commercial Health Insurance in China," the forms of coverage for health risks among Chinese residents are relatively singular. The majority still rely primarily on basic medical insurance and out-of-pocket payments, with these individuals predominantly concentrated in third-tier cities and below, as well as rural areas. This lower-income demographic in lower-tier markets constitutes the primary "base" for online mutual aid platforms. By providing an additional layer of protection for vulnerable populations facing critical illnesses, online mutual aid demonstrates significant inclusive value.

Secondly, the online mutual aid industry has fully leveraged digital technologies to reduce costs and improve efficiency, offering valuable insights for traditional offline insurance models. Currently, online mutual aid platforms utilize internet channels to precisely reach users, implement real-name registration and big data-driven online risk control, facilitate online contracting, and enable online cost-sharing—all of which serve as excellent examples of how traditional offline models can achieve cost reduction and efficiency gains. Furthermore, during business operations, these platforms accumulate vast amounts of medical data that can be analyzed by the industry and the government to assess disease incidence probabilities and medical behaviors, thereby supporting the development of China’s healthcare and health industries.

Finally, the online mutual aid industry has effectively enhanced residents’ awareness of protection. The strong interactivity between online mutual aid platforms and their members, along with periodic disclosures of mutual aid cases and cost-sharing arrangements, encourages members to pay greater attention to their personal health, thereby converting them into a substantial pool of potential customers for commercial health insurance.

As of the end of 2019, the mutual aid platform had approximately 150 million members (after adjusting for a 30% user overlap rate). Based on projections using the internet penetration rates from the Statistical Report on China’s Internet Development, the number of participants in the mutual aid industry is expected to reach 450 million within five years, covering approximately 32% of China’s total population.

Data from various sources are summarized as follows:

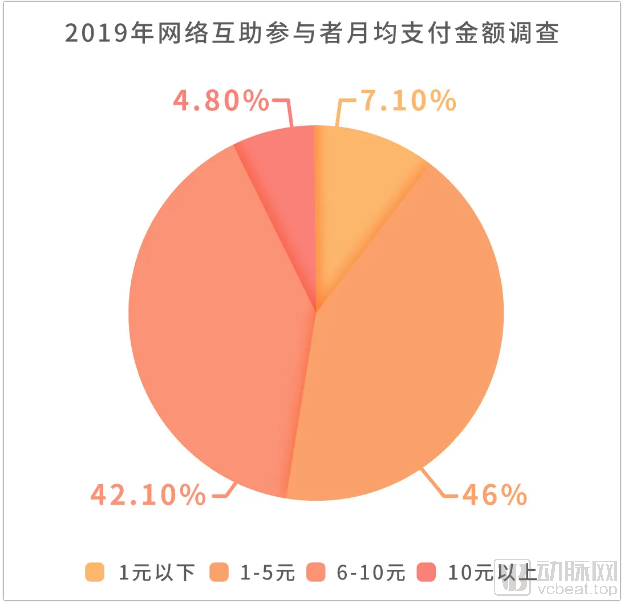

Data shows that over 90% of users pay an average of less than 10 yuan per month, a cost affordable for the vast majority of households. Low-income families can join mutual aid plans without significant financial burden, while also gaining health coverage.

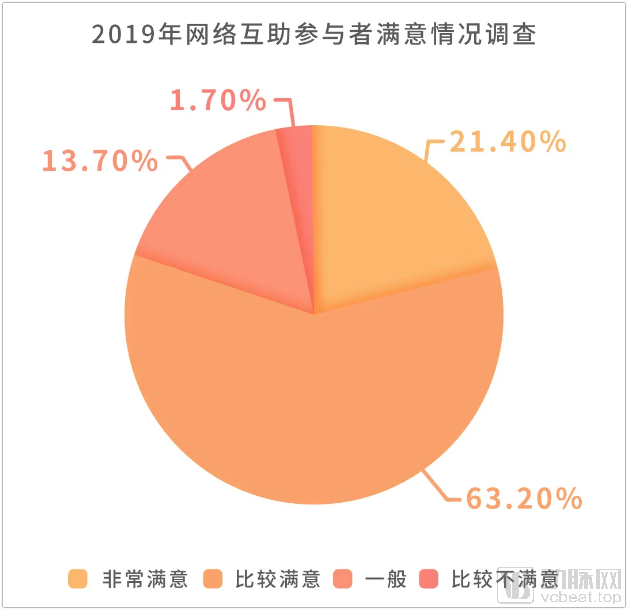

Data show that over 80% of users expressed satisfaction with online mutual-aid platforms, while only 1.7% voiced dissatisfaction. Online mutual aid not only provides medical security for beneficiaries but also enables participants to experience the inclusive spirit of “aiding society and ensuring public well-being,” thereby yielding a strong sense of fulfillment for both parties.

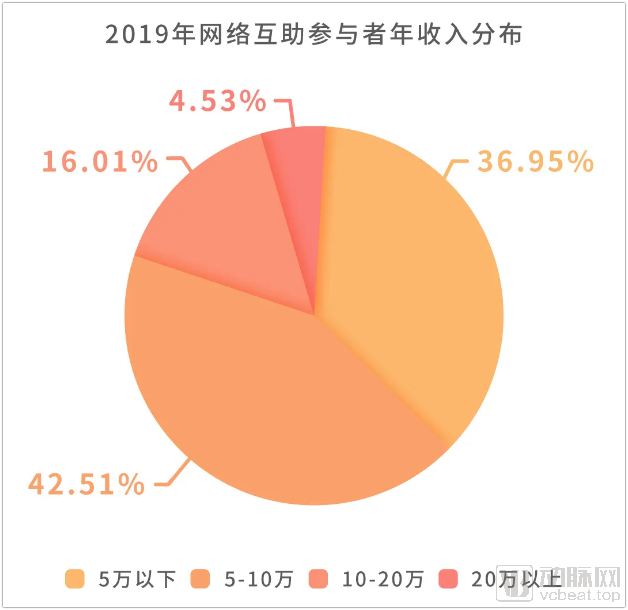

In mid-March 2020, the Ant Group Research Institute conducted a questionnaire survey among members of China’s online mutual aid industry via the Alipay questionnaire platform. The survey collected 58,721 valid responses. Analysis of the questionnaire data reveals that the member base of this industry primarily consists of individuals with middle-to-low incomes, relatively insufficient insurance coverage, and limited financial capacity to bear the costs of critical illnesses.

Due to the low barriers to entry and low costs associated with online mutual aid, it is able to attract more participants from lower-tier cities and low-income populations. According to the data mentioned above, this group purchases commercial insurance less frequently and has inadequate coverage under basic medical insurance. Therefore, achieving broad coverage of online mutual aid within this population can serve as a crucial component of their healthcare security.

With a current membership of 150 million, online mutual aid is poised to rapidly become a valuable complement to basic medical insurance and commercial health insurance as its coverage continues to expand. This development will help establish a more comprehensive healthcare security system, better addressing the diverse healthcare needs of populations at different levels.

The educational effect of online mutual aid on insurance coverage will drive large-scale customer acquisition for commercial insurance. As major traffic platforms, online mutual aid schemes boast a vast user base with significant demand for protection. Meanwhile, commercial insurers possess strong capabilities in designing commercial insurance products, ample financial resources, and the ability to meet diverse needs. The collaboration between these two sectors can fully leverage their respective strengths, providing users with more comprehensive and in-depth protection services.

The Application of Digital Technologies in Online Mutual Aid Will Drive the Transformation of Commercial Insurance. The scaled customer acquisition, online process reengineering, and in-depth application of key technologies within online mutual aid platforms—these insurtech innovations will inevitably accelerate the digital transformation of commercial insurance.

Currently, Xianghubao has applied key digital technologies such as big data, knowledge graphs, and blockchain to various scenarios, including case review, risk control, member services, member experience assurance, and public information disclosure. This has significantly improved industry efficiency, reduced operational costs, and enhanced process precision. In the future, digital technologies will become more precise, claims settlement will achieve a higher level of intelligence, and the industry will further reduce costs and increase efficiency.

No rules, no order. The online mutual aid industry has a short development history and is gradually entering a phase of expansion, while also facing numerous risks, such as compliance in publicity, sustainable operations, and oversight of capital pools.

Author: Kou Dantong | Reposted from the WeChat Official Account “Ping An Health Insurance Medical Insurance”