Healthcare Investment under ChiNext’s Registration-Based System: Smoother Exit Mechanisms and Stronger Confidence in Medical Innovation

On June 12, the Shenzhen Stock Exchange (SZSE) officially released the business rules and supporting arrangements for the reform of the ChiNext board and the pilot registration-based IPO system. Starting from June 15, the SZSE began accepting applications for initial public offerings (IPOs), refinancing, and mergers and acquisitions from companies under review on the ChiNext board. On August 24, the first batch of 18 companies rang the bell to list on the exchange.

The first batch of 18 companies to go public has attracted significant attention and high expectations. Judging by their performance on the first day of listing, all 18 companies lived up to expectations, delivering outstanding results.

Data showed that the ChiNext Index rose 1.98% on August 24, with all 18 stocks in the first batch of new listings closing higher. A total of 10 stocks surged more than 100%. Among them, Kangtai Medical led the gains, with its intraday peak increase nearing 3,000% before closing up 1,061.42%. Kaibei Yi jumped 743.27%, and Tianyang Technology soared 258.62%.

Among the 18 companies that went public, three were related to the healthcare industry: Contec Medical Systems, Weikang Pharmaceutical, and Huisun Biotech. Contec Medical Systems, which focuses on the research and development of electronic medical devices, saw the highest first-day stock price surge, briefly approaching 3000% before closing with a gain of 1061.42%. Weikang Pharmaceutical, a manufacturer of both traditional Chinese and Western medicines, rose by 96.03% on its debut. Huisun Biotech, specializing in animal health, increased by 84.02% on its first day of listing.

Regarding the phenomenon of newly listed companies on the ChiNext board under the registration-based IPO system experiencing strong first-day gains (“opening red”), Liu Daozhi, Executive Partner at Shanlan Capital, believes that the first-day performance is “overheated.” He advises investors to exercise caution, noting that stock prices will inevitably revert to normal levels in the future. Song Gaoguang, Executive Director at Northern Light Venture Capital, stated that a company’s value should not be judged solely by its one-day performance; instead, its development should be observed over a longer time horizon.

The launch of the registration-based IPO system on the ChiNext board is undoubtedly a major event for China’s venture capital and private equity (VC/PE) industry, one that will profoundly influence and reshape the country’s VC/PE ecosystem. For healthcare investment firms and healthcare startups focused on the primary market, what is the significance of the official implementation of the registration-based system on ChiNext? What opportunities and challenges does it bring?

In October 2009, the ChiNext board was officially launched. More than a decade has passed since its inception. On June 12, the ChiNext board ushered in significant reforms as the Shenzhen Stock Exchange (SZSE) officially released the relevant business rules and supporting arrangements for the reform of the ChiNext board and the pilot registration-based IPO system, marking a step toward the full implementation of the registration-based system.

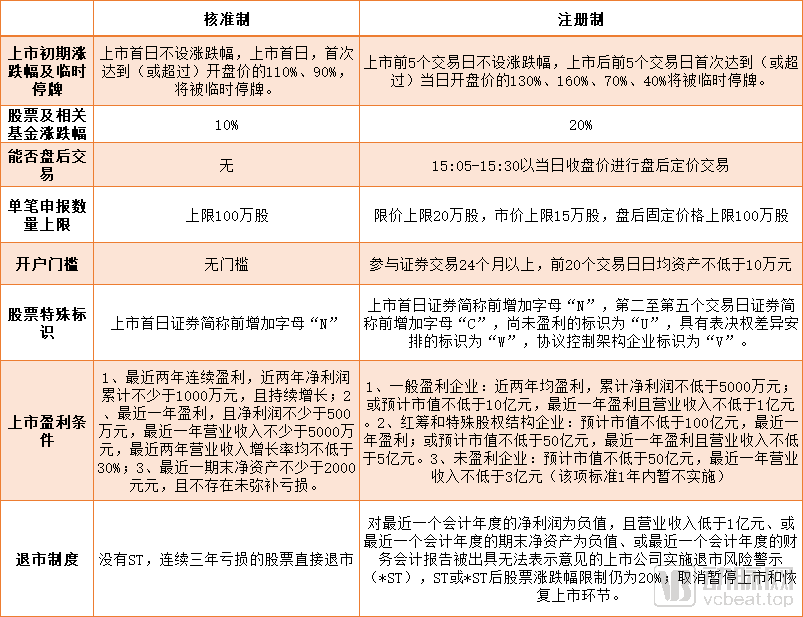

The core distinction between the registration-based system and the approval-based system, which had been in operation for over a decade, lies in the devolution of review authority from the China Securities Regulatory Commission (CSRC) to the stock exchanges. Under the previous regime, the reviewing body was required to ensure that all data in a company’s application documents complied with the issuance conditions established by regulatory authorities and to assess the company’s value. Under the registration-based system, the issuance review body conducts only a formal review of the registration documents, ensuring that the materials provided by the enterprise are authentic, complete, and compliant, while leaving the assessment of corporate value to the market.

In other words, going public does not equate to success; companies should leave the assessment of their value to the market. After listing, they should proactively drive their own development and strive to gain market recognition.

Under the registration-based system for the ChiNext board, a series of rule changes have also been introduced. Compared with the approval-based system, the specific rule changes are as follows:

Differences Between the Registration-Based System and the Approval-Based System on the ChiNext Board

The profitability requirements for listing on the ChiNext Board under the registration-based system stipulate that generally profitable enterprises must have been profitable in each of the past two years, with cumulative net profit no less than RMB 50 million; or have an estimated market capitalization of no less than RMB 1 billion, be profitable in the most recent year, and generate operating revenue of no less than RMB 100 million. For red-chip companies and those with special voting rights structures, the estimated market capitalization shall be no less than RMB 10 billion with profitability in the most recent year; or no less than RMB 5 billion, with profitability in the most recent year and operating revenue of no less than RMB 500 million. Unprofitable enterprises must have an estimated market capitalization of no less than RMB 5 billion and operating revenue of no less than RMB 300 million in the most recent year (this standard will not be implemented within one year).

Companies need to meet only one of the listing criteria mentioned above. It is reported that the first batch of 18 listed companies successfully went public by meeting the criterion of “being profitable in each of the past two years, with cumulative net profits of no less than RMB 50 million.”

Compared with the previous system, the listing threshold on the ChiNext board has been significantly lowered after the implementation of the registration-based IPO system. Although there are certain profitability requirements, the listing conditions are relatively more favorable. Many healthcare companies that were previously ineligible for the ChiNext board now have new opportunities, allowing more high-potential, high-value healthcare enterprises to shorten their listing cycles, go public quickly, and secure greater capital support. “It provides a viable listing channel for small and medium-sized enterprises,” said Song Gaoguang.

Song Gaoguang believes that the launch of the registration-based IPO system on the ChiNext Board can, to some extent, stimulate the development of the healthcare sector, benefiting medical device and biopharmaceutical companies with established revenue streams and growth potential.

“Developing innovative drugs and biotechnologies requires substantial capital investment and involves lengthy R&D cycles, which far exceed the investment horizon of Phase I funds managed by venture capital firms. This mismatch has long resulted in poor capital liquidity in these two sectors. With the implementation of the registration-based IPO system, more capital is inevitably poised to flow into the biopharmaceutical and biotechnology fields, thereby invigorating the entire industry.”

However, among the first batch of listed companies, the three firms involved in the medical sector (Contec Medical Systems, Weikang Pharmaceutical, and Huisheng Biology) do not fall under the category of biopharmaceutical or biotech enterprises mentioned above. In this regard, Liu Daozhi stated, “The initial cohort of listed companies should not be regarded as a benchmark; in the future, a large number of medical enterprises with higher technological content will undoubtedly list on the ChiNext board.”

Under the delisting regime, following the implementation of the registration-based system on the ChiNext board, listed companies are subject to a delisting risk warning (*ST) if they meet any of the following criteria: negative net profit for the most recent fiscal year and operating revenue below RMB 100 million; negative net assets at the end of the most recent fiscal year; or an auditor’s report issued with a disclaimer of opinion for the most recent fiscal year. The daily price fluctuation limit for stocks designated as ST or *ST remains at 20%. The procedures for suspension and resumption of listing have been abolished.

Following the shift to a registration-based system, the ChiNext Board has abolished the long-standing procedures for suspension and resumption of listings. Financial metrics are no longer the sole criteria for delisting; indicators such as excessively low market capitalization and violations in information disclosure have been incorporated, resulting in a more comprehensive and robust delisting framework.

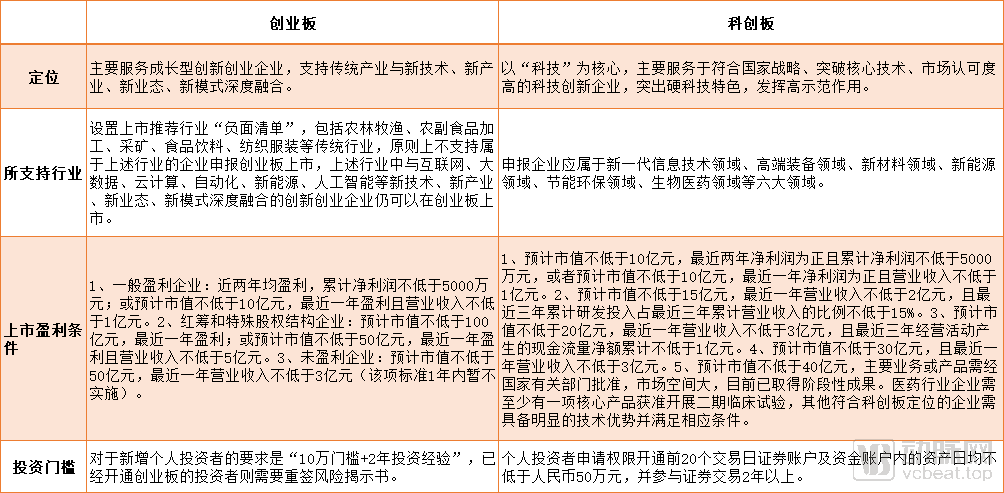

Both the ChiNext and the STAR Market serve innovative enterprises. Previously, domestic medical innovation companies were more inclined to list on the STAR Market. For example, this year, CanSino Biologics, Junshi Biosciences, HitGen, Tinavi Medical Technologies, and Aier Eye Hospital Group all listed on the STAR Market.

Liu Daozhi stated, “With the implementation of the registration-based IPO system on the ChiNext Board, it will become the preferred listing channel for medical innovation enterprises.” It is foreseeable that the number of medical innovation companies applying for listings on the ChiNext Board will gradually increase in the near future.

Meanwhile, many people compare the ChiNext board with the STAR Market. So, how should healthcare companies choose between the two? VCBeat has compiled a summary of their respective positioning, supported industries, and profitability requirements for listing.

Profitability Differences Between Listings on the ChiNext and the STAR Market

In terms of supported industries, the ChiNext board demonstrates greater inclusivity regarding enterprise sectors, while maintaining clear regulations for unsupported industries. In contrast, the STAR Market explicitly outlines its supported industries. Nevertheless, both boards have opened their doors to medical innovation enterprises; in particular, the STAR Market explicitly stipulates that listed companies should belong to one of six key sectors, including biopharmaceuticals.

“From the perspective of profitability requirements for listing, there is no fundamental difference between the ChiNext Board and the STAR Market. Consideration should be given more comprehensively to factors such as the company’s own circumstances, shareholder composition, foreign ownership ratio, corporate structure, and market scope,” said Liu Daozhi.

The choice between the STAR Market and the ChiNext Board should not be based solely on a comparison of listing thresholds. Although the profitability requirements for listing are similar, Song Gaoguang believes that the ChiNext Board and the STAR Market differ in their attributes and positioning, making them suitable for different types of enterprises. The STAR Market primarily serves technological innovation enterprises that align with national strategies, achieve breakthroughs in core technologies, and enjoy high market recognition, emphasizing "hard tech" characteristics and playing a leading demonstrative role. The ChiNext Board mainly serves growth-oriented innovative and entrepreneurial enterprises, supporting the deep integration of traditional industries with new technologies, new industries, new business formats, and new models.

“Simply put, the STAR Market imposes higher requirements on companies’ ‘innovation’ and ‘technology’ attributes. Healthcare companies with relatively stable revenue, strong growth potential, and moderate sci-tech innovation attributes are more suitable for listing on the ChiNext Board.”

As can be seen, during the initial phase of reform, the ChiNext board imposed profitability requirements on companies seeking listing, which posed certain challenges for R&D-intensive enterprises. This issue was particularly prominent for high-end medical device manufacturers, as “advanced medical device companies often remained unprofitable for a considerable period, making it difficult to meet the ChiNext listing criteria.”

Although unprofitable companies can list after one year by meeting the criterion of “an estimated market capitalization of no less than RMB 5 billion and annual operating revenue of no less than RMB 300 million in the most recent year,” Song Gaoguang stated that R&D-intensive enterprises will inevitably undergo a transition from being R&D-focused to sales-oriented. However, not every company’s transformation proceeds smoothly, and difficulties in sales and revenue generation are more or less inevitable.

The STAR Market has, to some extent, relaxed profitability requirements. For companies that are not yet profitable, the STAR Market stipulates that they may list if their “estimated market capitalization is no less than RMB 4 billion, their core business or products have been approved by relevant national authorities, they address a large market opportunity, and they have already achieved phased results.” Recently, Zeltis Pharma, which had no profits, no commercialized products, and virtually no revenue, successfully listed on the STAR Market. Other still-unprofitable companies, including Junshi Biosciences, Sinocelltech, and Bio-Thera Solutions, have also listed on the STAR Market. However, Song Gaoguang believes that “it is still challenging for high-end medical device companies to meet the STAR Market’s RMB 4 billion valuation requirement.”

Addressing the current challenges in bringing high-end medical devices to market, Song Gaoguang expressed his hope that relevant enterprises will actively engage with the China Securities Regulatory Commission (CSRC) and related agencies. He also urged decision-making bodies to take into account the unique circumstances of R&D-intensive companies with high investment costs, and to establish new pathways for such enterprises.

Exit difficulties have long plagued investment institutions.

Following the introduction of the registration-based IPO system on the ChiNext board, the most significant benefit for investment firms lies in a smoother and more predictable exit mechanism. Song Gaoguang remarked, “The R&D cycle for innovative drugs is approximately 10 years. As investors, we often accompany these companies throughout this decade-long journey, which poses a substantial challenge to capital liquidity.”

“Following the introduction of the registration-based IPO system on the ChiNext Board, the listing timeline for companies has shortened, leading to a corresponding reduction in institutional investment cycles and greater capital flexibility. Meanwhile, listed companies can leverage raised funds to sustain growth and expansion, thereby driving up valuations and generating higher returns for institutional investors.”

Song Gaoguang has observed that since the implementation of the registration-based IPO system, many investment institutions that previously focused on early-stage projects have shifted their attention to mid- and late-stage ventures. “Under the favorable impact of the registration-based system, investors will concentrate more on late-stage investments in the coming years.” However, he believes that “the short-term rush toward late-stage projects within the venture capital community is a normal phenomenon driven by capital dividends. In the long run, investment activities are bound to return to a normal pace and equilibrium.”

Liu Daozhi noted, “Previously, investors were quite cautious about early-stage projects, fearing prolonged exit timelines, and thus preferred investing in later-stage ventures. Following the implementation of the registration-based IPO system on the ChiNext Board, listing requirements have been slightly relaxed, allowing companies without net profits to apply for listings. This has significantly bolstered investors’ willingness and confidence in funding early-stage healthcare projects.”

Combining the perspectives of both parties, the launch of the registration-based IPO system will strengthen investment institutions’ willingness to invest in early-stage, growth-stage, and late-stage projects, thereby significantly promoting the balanced development of China’s venture capital and private equity ecosystem.

Under the registration-based IPO system, the investment sectors and stages that institutional investors focus on are also undergoing changes.

From an investment perspective, sectors aligned with the characteristics of the ChiNext Board—such as biopharmaceuticals, biotechnology, high-end medical equipment, high-value cardiovascular consumables, surgical robots, and minimally invasive medical devices—are more favored by investment institutions.

From the perspective of investment stages, venture capital firms will appropriately broaden their stage coverage, making fundraising smoother for early-, mid-, and late-stage projects. Northern Light Venture Capital, which focuses on early-stage technology investments, will maintain this core investment logic under the registration-based IPO system for the ChiNext board. “However, we will also make some minor adjustments, appropriately considering investments in growth- and late-stage companies with strong potential to go public or become industry leaders.”

Meanwhile, both Song Gaoguang and Liu Daozhi emphasized that the lowering of listing thresholds for enterprises does not equate to a reduction in investment difficulty for institutional investors. “In the past two years, there was a widespread mindset that once a company went public, it was deemed successful. In reality, an initial public offering (IPO) merely broadens financing channels and is not the sole criterion for judging success.” Under the registration-based IPO system, enterprise value is determined by the market, and market mechanisms will eliminate unqualified companies. Therefore, under this system, institutional investors should “return to value investing” by backing truly valuable enterprises to achieve substantial returns.