National Medical Consumables Volume-Based Procurement Imminent: Industry Restructuring Underway

The curtain has risen on the centralized procurement of medical consumables.

Over the past year, numerous policies on volume-based procurement of medical consumables have been issued.In late July 2019, the General Office of the State Council issued the Reform Plan for the Governance of High-Value Medical Consumables, proposing to improve classified centralized procurement methods. On July 3 this year, relevant departments released a request for comments on the volume-based procurement scheme for coronary stents, making coronary stents the first product category subject to national-level centralized procurement. Nationwide centralized procurement of medical consumables is imminent.

Looking back on more than two decades of healthcare reform in China, establishing reasonable prices for medical consumables and pharmaceuticals has remained a persistent challenge for policymakers.In this process, it is undoubtedly extremely difficult to maximize the interests of all parties—patients, medical insurance, hospitals, pharmaceutical companies, and medical device enterprises—within a single framework and find a balance. It should be noted that every detail in each policy or regulation can have a significant impact on the industry. It is precisely for this reason thatThe tug-of-war over the prices of medical consumables and pharmaceuticals has permeated nearly the entire course of China’s healthcare reform.

Things are taking a turn for the better. In March 2018, a major restructuring of State Council institutions was implemented, introducing top-level design reforms. That May, the National Healthcare Security Administration (NHSA) was officially established and began operations. As is well known, under the previous system, oversight of healthcare insurance funds was fragmented across four different departments: basic medical insurance for urban employees and urban residents was administered by the Ministry of Human Resources and Social Security; the New Rural Cooperative Medical Scheme fell under the National Health and Family Planning Commission; medical assistance programs were managed by the Ministry of Civil Affairs; while pricing for medical services and pharmaceuticals was regulated by the National Development and Reform Commission.The establishment of the National Healthcare Security Administration not only ensures comprehensive management and regulation of the medical insurance fund, but also leverages its position as a super-payer to drive industry-wide transformation and other strategic initiatives.

Holding the “purse strings” of public healthcare and pharmaceutical expenditures, the National Healthcare Security Administration has decided to squeeze the “fat” out of the prices of medical consumables and drugs.Drug prices were the first to be cut. Since 2018, the National Healthcare Security Administration has successively led four rounds of national centralized drug procurement: the “4+7” pilot program, the nationwide expansion of the “4+7” pilot, the second batch of national centralized drug procurement, and the third batch of national centralized drug procurement.

The results are significant. Taking the third round of China’s National Centralized Drug Procurement in August this year as an example, 125 companies were provisionally selected as winners, covering 191 drug specifications. The average price reduction was 53%, with the highest decrease exceeding 95%. Some drugs even dropped to just a few cents per tablet.

With centralized drug procurement already in place, nationwide centralized procurement of medical consumables has also been put on the agenda.. The curtain is slowly rising on a new wave of transformation in China’s healthcare industry.

“For a long time,Fraudulent insurance claims, artificially inflated prices of drugs and consumables draining the medical insurance fund, and “micro-waste” caused by overtreatmentand so forth. These seemingly ordinary, “ant-moving-household”-style behaviors accumulate over time, causing serious erosion to the medical insurance fund.”

In June this year, Hu Jinglin, Director of the National Healthcare Security Administration, delivered a speech titled “Let Reform Be the Most Distinctive Feature of the Healthcare Security Banner” at a training session on deepening healthcare security system reforms. The speech has circulated widely online, sounding another alarm over the issue of artificially inflated prices for pharmaceuticals and medical consumables.

To address this phenomenon, the National Healthcare Security Administration has shouldered significant responsibilities since its inception.Starting with drug prices, centralized procurement has achieved maximum price reductions of over 90% for certain medications., reinforcing the resolve of relevant authorities to advance healthcare reform with volume-based procurement as the primary lever.

After achieving significant results in drug pricing,The advancement of centralized procurement for medical consumables is also accelerating continuously.As of December 31, 2019, volume-based procurement programs for high-value medical consumables had been implemented in 13 provinces and municipalities. Anhui and Jiangsu provinces pioneered the pilot programs, with Jiangsu having conducted three rounds of volume-based procurement. Other regions, including Shanxi, Shandong, Liaoning, Gansu, Hunan, Yunnan, Chongqing, and Hainan, have also successively launched implementation initiatives. The Beijing-Tianjin-Hebei region established a Northern Procurement Alliance based on regional cooperation, creating a new “3+5” joint procurement model...

Similar to the results of centralized drug procurement, local-level centralized procurement of medical consumables has also achieved favorable outcomes.For example, data from the completion of Anhui Province’s volume-based negotiation and price bargaining in July 2019 showed that the average price reduction for orthopedic spinal materials was 53.4%, with the maximum price reduction for a single component reaching 95%; the average price reduction for intraocular lenses was 20.5%. Based on the online procurement volume of orthopedic spinal materials and intraocular lenses across the province in the first half of 2019,The two categories of products achieve annual cost savings of approximately RMB 370 million and RMB 30 million, respectively.

The core of centralized procurement is exchanging volume for price; therefore, the key to securing significant price reductions from medical device manufacturers lies in whether there is sufficient procurement volume.. On this basis, the current volume-based procurement projects for medical consumables can be mainly categorized into three types: provincial-level, alliance-based, and municipal-level.

Provincial-level procurement refers to volume-based procurement organized at the provincial level.Currently, Anhui and Jiangsu provinces have implemented volume-based procurement for medical consumables. The selection results indicate that both provinces prioritized high-value consumable categories characterized by substantial procurement expenditures, extensive clinical utilization, and intense market competition.

City-level procurement refers to volume-based procurement organized at the municipal level.For example, on August 23, the Wuxi Municipal Healthcare Security Administration organized a procurement alliance comprising 40 public hospitals at secondary level and above across the city to negotiate prices with 23 medical consumable manufacturers. As a result, the average price reduction for four product categories ranged from 48% to 61.2%, primarily involving low-value consumables such as dialysate, medical polymer splints, and central venous catheters.

Alliance-based procurement refers to cross-regional group purchasing, including intra-provincial municipal alliances and cross-regional provincial alliances.For example, on July 25, the Joint Procurement Office for Pharmaceuticals and Medical Devices of Qingdao, Zibo, Yantai, Weifang, and Weihai issued the "Qingdao-Zibo-Yantai-Weifang-Weihai Joint Procurement and Price Negotiation Scheme for Pharmaceuticals and Medical Devices in Public Medical Institutions (Trial)," leveraging volume-based procurement to secure price reductions for over 30 million units of low-value consumables, including infusion sets, indwelling needles, and pre-filled catheter flush syringes, ultimately achieving an average price reduction of 60.93%.

In terms of procurement categories,Provincial-level initiatives primarily focus on high-value medical consumables, whereas municipal-level efforts mainly target low-value medical consumables.Undoubtedly, the division of procurement responsibilities between provincial and municipal levels is relatively clear.

Why Were Pharmaceuticals, Rather Than Medical Consumables, the First to Be Included in National Centralized Procurement? This Is Related to the Complexities Facing the Centralized Procurement of Medical Consumables. The “Three Major Obstacles” Looming Ahead Are the Primary Factors.

The first “major hurdle” is the lack of generic names for medical consumables., which is attributable to the wide variety, diverse specifications, and complex models of medical consumables, resulting in the absence of a unified national coding standard for medical consumables at present.The second “major hurdle” is the more fragmented market for medical consumables。The third “major hurdle” is that the vast majority of medical consumables can only be used within healthcare institutions., the proficiency of users directly impacts medical outcomes.

The Three Main Causes Behind the “Three Big Mountains”First, the regulatory framework for medical consumables is complex, with certain products subject to approval by provincial authorities. This has led to a wide variety of specifications and a lack of standardized nomenclature, resulting in instances where different products share the same name or the same product is known by multiple names. Second, medical consumables are characterized by short R&D cycles and rapid iteration, leading to an exceptionally large number of specifications and models listed in current registration approvals. Third, the use of medical consumables, particularly high-value ones, involves a certain learning curve and poses challenges to the competencies of healthcare professionals.

“The key reason why the national centralized procurement of drugs has been able to advance rapidly is that the consistency evaluation for pharmaceuticals is highly mature, whereas the consistency evaluation for medical consumables has not yet been implemented,” an industry insider told VCBeat.

In response to the aforementioned issues, relevant policies are being continuously advanced and refined.In June 2019, the National Healthcare Security Administration issued the Guiding Opinions on Standardization of Medical Security. The document stated that a unified national coding system for high-value medical consumables would be implemented by 2020, putting an end to the era of proliferating and inconsistent product names. In August of the same year, the Response of the National Healthcare Security Administration to Suggestion No. 6395 from the Second Session of the 13th National People’s Congress indicated that the National Health Commission would collaborate with relevant regulatory authorities to establish institutions for the consistency evaluation of medical consumables, thereby introducing a “consistency evaluation” framework for consumables similar to that applied to pharmaceuticals.

The first batch of national centralized procurement for high-value medical consumables will start with coronary stents.

In July this year, the Pharmaceutical Price and Tendering Guidance Center of the National Healthcare Security Administration issued a letter soliciting public comments on the "National Centralized Volume-Based Procurement Plan for Coronary Stents (Draft for Comments)."In the first batch of national volume-based procurement, the target of this centralized volume-based procurement is coronary stent products., the material shall be approved by the drug regulatory authority and obtain a valid medical device registration certificate.

The materials involved in this instance are cobalt-chromium alloy and platinum-chromium alloy, the drug types are rapamycin or its derivatives, and the nature of the drug carrier coating is non-polytetrafluoroethylene for coronary stents. The Joint Procurement Office for High-Value Medical Consumables Organized by the State is responsible for formulating specific technical indicators.

The procurement cycle for this round is two years. Upon expiration of the agreement, each province shall determine the supplying enterprises, agreed procurement volumes, and procurement periods. In the event of significant changes in supply-demand dynamics, technological standards, or market structure, the selected enterprises, selected prices, and agreed procurement volumes may be determined through methods such as competitive bidding, price negotiation, direct negotiation, or request for quotation.

Notably, in terms of procurement scope and volume, this volume-based procurement initiative represents the largest procurement alliance to date.The plan specifies that public medical institutions and military medical institutions with a coronary stent usage volume exceeding 1,000 units in 2019 shall participate. Other public medical institutions, military medical institutions, and privately operated medical institutions designated as basic medical insurance providers may participate voluntarily in accordance with the arrangements of their respective provinces. Provinces that have already implemented centralized volume-based procurement for such products and are still within the contract period may opt out.

Regarding the proportion of agreed procurement volume, medical institutions participating in the alliance-based procurement shall determine the total procurement baseline and the procurement baseline for each product (excluding stainless steel stents) based on their reported procurement volumes from 2019. The agreed procurement volume shall be set at 80% of the total procurement baseline, with the guarantee that the procurement volume for each selected product shall be no less than 80% of its reported procurement baseline.

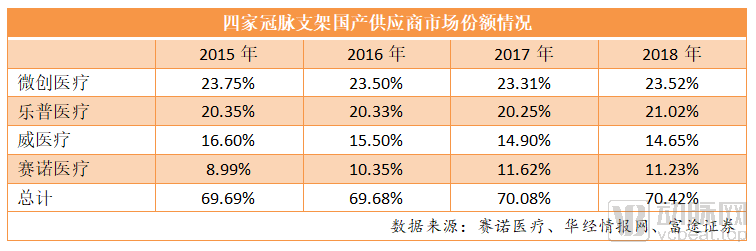

According to data compiled by Futu Securities, the domestic substitution rate for coronary stents has reached 70% to date. Although the technical barriers for coronary stents are relatively lower, the industry scale is substantial. Currently, second- and third-generation coronary stents account for as high as 99% of the market, with the competitive landscape stabilizing and market concentration steadily increasing.

Currently,In the field of coronary stents, there are four major domestic suppliers., namely MicroPort Medical, Lepu Medical, Jiwei Medical, and Sino Medical. Among them, MicroPort Medical holds the largest market share, occupying a leading position in coronary stents. Lepu Medical and Jiwei Medical follow closely with similar market shares. Notably, all of Sino Medical’s products are made of stainless steel and do not meet procurement requirements, whereas the other three companies have flagship products that comply with the criteria and are thus eligible to participate in centralized volume-based procurement.

Judging from the results of China’s national volume-based procurement (VBP) for pharmaceuticals, the “blade” of centralized procurement has clearly taken a significant toll on corporate profits. However, market concerns are emerging that companies failing to win bids will be shut out of the market and unable to secure any share, while even some winning bidders may ultimately collapse due to razor-thin margins resulting from steep price cuts. Therefore, can the price-reduction mechanism established through VBP operate sustainably in the long term and be replicated?

First and foremost, it is essential to clarify thatThe purpose of volume-based procurement is to eliminate inflated sales and promotional costs embedded in the prices of medical consumables., the price reduction ultimately borne by medical device companies comes from the profit margins of distribution channels; if these margins are substantial, the impact on R&D and manufacturing enterprises will be relatively limited.

Among medical consumables, high-value consumables account for 62.50% of the market, with a market size of approximately RMB 106 billion (based on 2018 data). Due to their high prices, high-value consumables impose a heavier financial burden on patients and exert greater pressure on the national medical insurance fund. Consequently, they have long been a focal point of policy initiatives and public attention, which underpins the central government’s intensified efforts in centralized procurement of these products.

Undeniably, in addition to the “genuinely high” prices of high-value medical consumables driven by their high technological content, clinical value, and management costs, there is also an element of “artificially inflated” pricing, primarily attributable to the following three factors.

First, the price formation mechanism is unreasonable.. Compared with pharmaceuticals, the sales of medical devices rely more heavily on distributors, and the competitive landscape of the device distribution market is more fragmented. For instance, in terms of hospital terminal prices, it is difficult to establish a unified tender procurement price due to the wide variety of specifications and types of medical devices. The price differentials between ex-factory prices and terminal prices vary across different device categories. Furthermore, as the “two-invoice system” for medical devices has not been strictly enforced nationwide, significant room for maneuver remains within the distribution channels.

Second, there is a lack of relevant policies on medical insurance payment.Due to the wide variety of medical devices and their diverse raw materials, systematic classification and comparison are challenging. China’s health insurance reimbursement primarily operates on a fee-for-service basis, and the absence of a national reimbursement guideline catalog for high-value medical consumables has contributed to their overuse.

Third, hospitals exhibit weak willingness to implement controls.Hospitals and physicians are inclined to use high-value medical consumables, partly due to their relatively high technological content and quality standards, and partly because the use of such consumables generates revenue for hospitals, compensating for the excessively low prices of medical services. Consequently, hospitals have limited motivation to implement strict controls.

What impact will the comprehensive implementation of volume-based procurement (VBP) for medical consumables have on the industry? Insights may be drawn from the national centralized drug procurement program. Based on the experience of the “4+7” drug VBP pilot, the three winning bidders share 60%–70% of the national market, while non-winning small and medium-sized enterprises are completely marginalized. As a result, over time, smaller firms with limited innovation capabilities risk being eliminated from the market unless they proactively pursue transformation.

Not only that,As volume-based procurement of medical consumables becomes normalized, excess production capacity will be gradually phased out, while leading domestic enterprises with strong innovation capabilities will leverage greater market share to secure more pronounced competitive advantages.. Industry concentration will continue to rise, and the “Matthew effect” within the sector will accelerate.

“The national centralized procurement of medical consumables has imposed new requirements on cost control for device manufacturers, thereby squeezing the profit margins of distributors. To maintain sustainable development,”Distributors should rationally configure their product portfolios to better align with clinical needs, gradually assume responsibilities such as training and after-sales service, and thereby strengthen their stickiness with manufacturers.. In addition,Distributors with deep expertise in specific fields or departments and greater sensitivity to new clinical technologies will have more opportunities..” Tian Feng, Investment Director at Qingtong Capital, told VCBeat.

From a trend perspective, large enterprises with strong innovation capabilities will capture market share exclusively by trading price for volume. Small and medium-sized enterprises (SMEs), constrained by limited profit margins, minimal room for price reductions, and restricted production capacity, are unable to compete with large corporations. As their survival is threatened, industry concentration continues to rise.

Following the industry reshuffle driven by the national centralized procurement of pharmaceuticals, distributors and medical device companies must rethink their positioning and development strategies under cost-containment pressures as the national centralized procurement of medical consumables is set to begin.

First, for distributors, especially small and medium-sized ones, once they lose the consumable products included in volume-based procurement (VBP), they are forced to shift to other consumable categories not yet covered by such policies. This results in increased time and channel costs associated with transitioning to new product lines. In particular, the direction of VBP for high-value medical consumables is likely to involve future sales through the platform of the National Healthcare Security Administration (NHSA). Once this stage is reached, the enterprise rebates and price differentials on consumables that previously existed will no longer be available.For distributors, digitalized logistics and back-end services may be the way forward.

Furthermore, for consumables manufacturers, the current focus of innovation lies in delivering high-quality products at low prices. At this juncture, companies must either capture over 70% of the regional market share across consumables categories or face elimination from those segments. In the long run, however, manufacturers still need to pursue a “qualitative leap” in their products.Strengthen product R&D efforts to seek greater incremental growth in innovation and clinical value.

Finally, for innovative companies specializing in high-value medical consumables,In product R&D, greater consideration should be given to the strengths and weaknesses of competing products to develop innovative and differentiated offerings., to avoid falling into the "approval equals death" trap.

As the nationwide centralized procurement of medical consumables approaches, this new transformation concerning China’s healthcare industry will continue to deepen. Drawing on prior experience with the national centralized procurement of pharmaceuticals, companies in the medical consumables sector are bound to undergo a new round of reshuffling and restructuring. For some enterprises, this may present an opportunity to expand market share and achieve rapid growth; for others, however, it could deliver a devastating blow.

However, regardless of the circumstances,Following the reshaping of the industry landscape, there will be an increasing availability of medical consumables, particularly high-value consumables, that offer better cost-effectiveness and better align with clinical needs, which will serve as a positive driver for the industry.. Just as the phoenix rises from the ashes, reborn through fire, the medical consumables industry is poised to welcome a new spring.

References:

“National Centralized Procurement of Consumables Gains Momentum, Industry Concentration Continues to Rise, and the ‘Matthew Effect’ Accelerates in the Sector” – MedDevice Hub

“Starting Gun for National Centralized Procurement of Medical Consumables Fires: Coronary Stents Lead the Way—Who Can Seize the Momentum to Stage a Comeback?” Futu NiuNiu

“A Single Head of Medical Equipment Department Can Pocket RMB 3.96 Million in Kickbacks: How Much Room Is There for Price Reductions in China’s National Centralized Procurement of Consumables?” – Ba Dian Jian Wen