Tasly Biopharmaceuticals Files for STAR Market IPO, Aiming to Raise Over RMB 2.4 Billion

2019Year6In [Month], Tasly Biopharmaceuticals Submitted Its Listing Application to the Hong Kong Stock Exchange, and on2019Year11Passed the HKEX listing hearing in [Month], but the IPO process was interrupted. According toIPOHaving learned the news, Tasly Biopharmaceutical is considering postponing its listing on the Hong Kong Stock Exchange, due to both the recent poor performance of the Hong Kong market and the current uncertainty in valuations within the pharmaceutical sector.

On September 3, 2020, Tasly Biological submitted an application to the STAR Market, aiming for a listing on the board.

Shanghai Tasly Pharmaceutical Co., Ltd. (formerly known as Shanghai Tasly Pharmaceutical Co., Ltd.) was established in 2001 and is primarily responsible for the research and development of biopharmaceuticals. It is an innovative biopharmaceutical company with a complete integrated platform for research, production, and sales. The core business of Tasly Bio focuses on the full lifecycle of biopharmaceuticals, covering the entire process from drug discovery, product development and clinical research to commercial production and sales.

It is understood that Tasly Biopharmaceuticals has successfully launched and commercialized its national Class I innovative biologic drug, Recombinant Human Pro-urokinase for Injection (brand name: Puyouke). Tasly Biopharmaceuticals is also strategically positioning its R&D efforts in three key therapeutic areas—cardiovascular and cerebrovascular diseases, digestive and metabolic disorders, and oncology and immunology—while rapidly advancing its pipeline of investigational candidates with international competitive advantages.

Tasly Biologics’ core product is recombinant human prourokinase for injection, marketed under the brand name “Puyouke.” To date, Puyouke remains the only commercially available recombinant human prourokinase product in China.

Currently, the indication for Puyouke is acute ST-segment elevation myocardial infarction (STEMI). Acute STEMI is caused by persistent obstruction of blood supply, which may lead to extensive necrosis of cardiomyocytes. Its clinical manifestations primarily include chest pain, as well as ST-segment elevation and dynamic evolution on electrocardiogram. Acute STEMI is a life-threatening, time-sensitive acute condition; patients must seek medical attention promptly and undergo coronary reperfusion therapy as soon as possible, including percutaneous coronary intervention (PCI) or thrombolysis. Puyouke is used for thrombolytic therapy in acute ST-segment elevation myocardial infarction.

China is one of the countries with the highest number of new cases of acute ST-segment elevation myocardial infarction (STEMI) globally. According to a report by Frost & Sullivan, the number of patients with myocardial infarction in China was approximately 928,300 in 2019, among whom about 696,200 had acute STEMI. Driven by factors such as dyslipidemia, hypertension, smoking and other unhealthy lifestyle habits, as well as an increasing rate of reperfusion therapy accessibility for acute STEMI patients, the number of acute STEMI patients in China is projected to rise to approximately 801,700 by 2030.

According to the prospectus, approximately 141,200 patients in China were eligible for thrombolytic therapy in 2019. With the continuous optimization of healthcare resource structures and growing recognition of the benefits of thrombolytic therapy for patients with acute ST-segment elevation myocardial infarction (STEMI), the proportion of reperfusion therapy administered via thrombolysis is expected to further increase. It is projected that by 2024, approximately 219,600 patients in China will be eligible for thrombolytic therapy.

According to a Frost & Sullivan report, based on the results of Phase IV clinical trials of Puyouke involving more than 2,000 patients and the Guidelines for Rational Use of Thrombolytic Therapy in Acute ST-Segment Elevation Myocardial Infarction, Puyouke demonstrates the highest recanalization rate (85%) among approved thrombolytic agents for the treatment of acute ST-segment elevation myocardial infarction (STEMI) in China, indicating significant efficacy. Meanwhile, it has the lowest incidence of intracranial hemorrhage (0.29%), reflecting a favorable safety profile. As a recommended thrombolytic agent for patients with acute STEMI, Puyouke has been included in multiple major academic guidelines and other authoritative medical publications.

In addition to its use in treating acute ST-segment elevation myocardial infarction (STEMI), Tasly Biopharmaceuticals is actively expanding the indications for Puyouke, primarily including acute ischemic stroke, acute pulmonary embolism, and other potential thromboembolic disorders. It is reported that the B1140 project, aimed at expanding Puyouke’s indications to include acute ischemic stroke, received funding from the National Major Science and Technology Special Project for Significant New Drug Development during the 13th Five-Year Plan period.

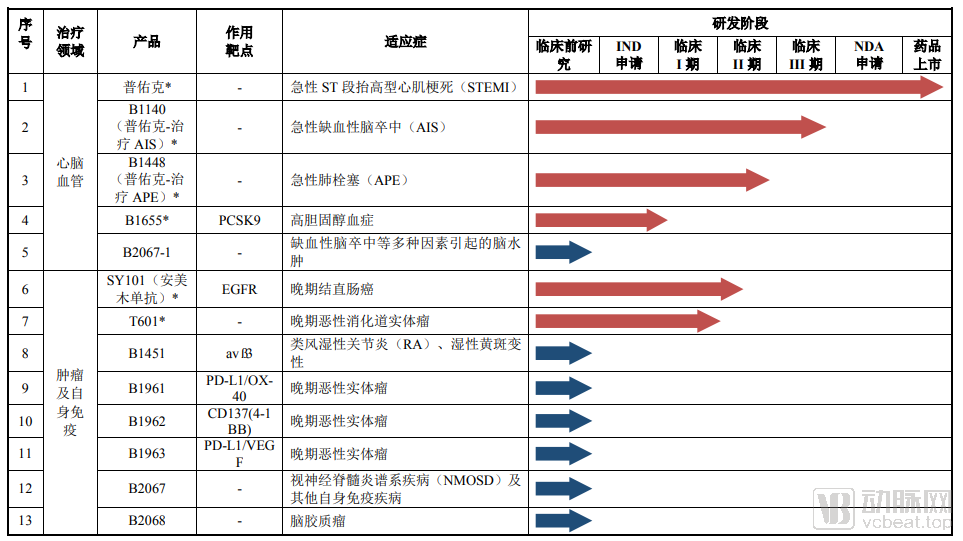

In addition, Tasly Biopharmaceuticals focuses on three major therapeutic areas: cardiovascular and cerebrovascular diseases, oncology, and autoimmune and digestive/metabolic disorders. It enriches its product pipeline through a “four-pronged” strategy encompassing independent R&D, licensed-in acquisitions, collaborative development, and acquisition of commercialization rights. Currently, Tasly Biopharmaceuticals has established a broad portfolio of 19 biologic drug projects, including Puyouke and six other core products in clinical development.

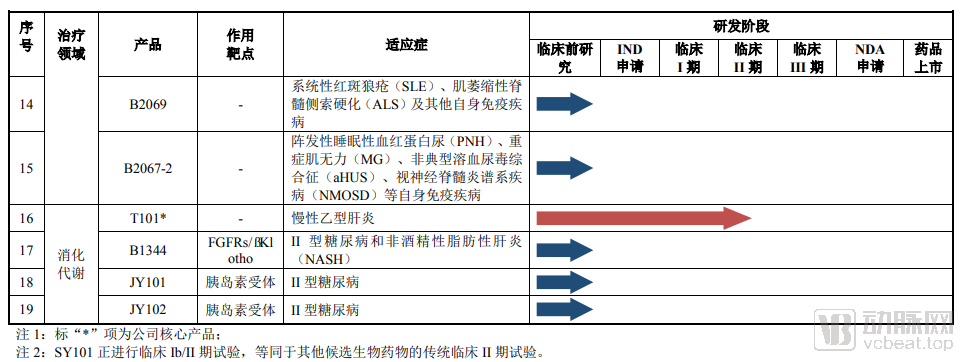

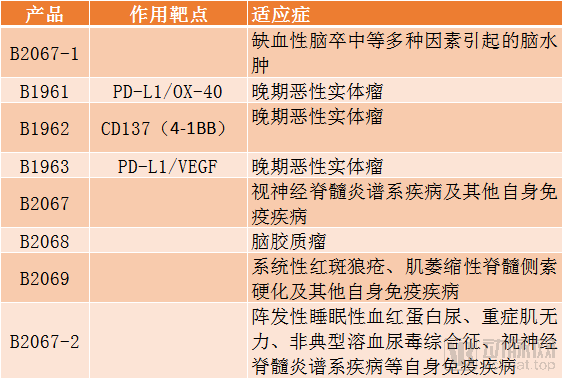

As of now, Tasly Biopharmaceuticals’ core product pipeline comprises 19 products, including the marketed product Puyouke and 18 products under development. Among the investigational projects, the expansion of Puyouke for the indication of acute ischemic stroke (B1140) is in the Phase III clinical trial summary stage, while the expansion for the indication of acute pulmonary embolism (B1448) is in the Phase II clinical trial summary stage. Of the other products under development, SY101 and T101 are in Phase II clinical trials, T601 is in Phase I/IIa clinical trials, and B1655 is in Phase I clinical trials; the remaining candidates are currently in preclinical research stages.

Compared with the prospectus filed in June 2019, this prospectus reflects adjustments to the R&D pipeline: the SY102 program for leukemia and solid tumors, B1452 for non-Hodgkin lymphoma, and B1453 for advanced malignant solid tumors have been discontinued, while eight new R&D pipelines have been added.

(Tasly Bio's newly added R&D pipeline; data source: prospectus; graphic by VCBeat)

Currently, the clinical-stage products include the following six: B1140 (Puyouke for the treatment of AIS), B1448 (Puyouke for the treatment of APE), B1655, SY101 (Anmeimu Monoclonal Antibody), T601, and T101.

B1140 (Puyouke for the Treatment of AIS) and B1448 (Puyouke for the Treatment of APE)

B1140 (Puyouke for the treatment of AIS) is indicated for acute ischemic stroke and is currently in Phase III clinical trials; B1448 (Puyouke for the treatment of APE) is indicated for acute pulmonary embolism and is currently in Phase II clinical trials. The advantages of both products include: they are next-generation specific thrombolytic agents with a unique mechanism of action, low risk of systemic bleeding, and high safety profile; they exhibit a low rate of re-thrombosis after thrombolysis; and they benefit from advanced manufacturing processes. Puyouke has been included in the National Reimbursement Drug List twice, resulting in low out-of-pocket costs for patients. Additionally, B1140 (Puyouke for the treatment of AIS) has received funding from the National Major Science and Technology Project for Significant New Drug Development during the 13th Five-Year Plan period.

B1655

B1655 is indicated for hypercholesterolemia and is currently in Phase I clinical trials. Its advantages include: being a fully human monoclonal antibody with low ADCC and CDC activity and low immunogenicity; positioned as a high-quality, low-cost product with strong patient affordability; addressing a large patient population with broad market prospects; and targeting a highly druggable target.

SY101 (Anmeimu Mab)

SY101 (anmeimumab) is indicated for advanced colorectal cancer and is currently in Phase II clinical trials. Its advantages include: being a fully human monoclonal antibody with low immunogenicity and a long half-life; the product exhibits low skin toxicity, mild diarrhea, and a high safety profile, with noProphylactic administration is required, with high patient compliance; the target exhibits high druggability. Furthermore, this product has received funding from the National Major Science and Technology Special Project for Significant New Drug Development during both the “12th Five-Year Plan” and “13th Five-Year Plan” periods.

T601

T601 is indicated for advanced malignant gastrointestinal solid tumors and is currently in Phase I/IIa clinical trials. Its advantages include: a dual therapeutic mechanism combining oncolysis and targeted chemotherapy, which enables selective oncolysis while converting 5-FC into 5-FU and 5-FUMP to exert targeted chemotherapeutic effects, significantly enhancing treatment efficacy against tumors, particularly refractory cancers such as glioblastoma and pancreatic cancer; compared with conventional chemotherapy, it exhibits high selectivity toward tumor cells, delivering targeted chemotherapy while reducing toxicity to non-tumor tissues; the combination of the oncolytic virus with immune checkpoint inhibitors can enhance existing therapeutic effects and may potentially treat “cold tumors” that respond poorly to immune checkpoint inhibitor monotherapy.

T101

T101 is indicated for chronic hepatitis B and is currently in Phase II clinical trials. Its advantages include being the first virus-vectored therapeutic vaccine for chronic hepatitis B approved to enter clinical trials in China; it possesses specific anti-HBV immune activity, capable of inducing HBV antigen-specific cytotoxic T lymphocytes (CTLs) and promoting cytokine secretion to eliminate HBV from infected hepatocytes; and it has demonstrated favorable efficacy and tolerability results in Phase Ia clinical trials in North America and Europe.

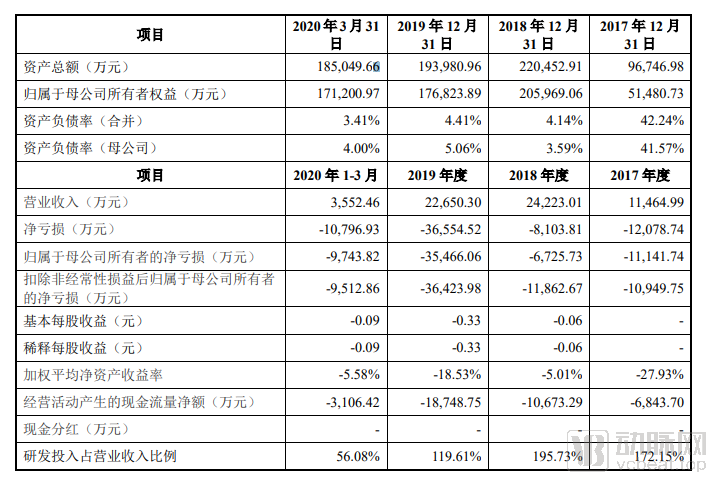

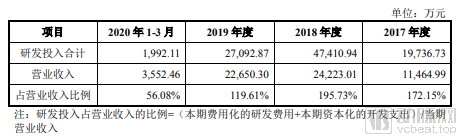

From 2017 to 2019 and during the first three months of 2020, Tasly Biopharmaceutical’s operating revenues were RMB 116 million, RMB 240 million, RMB 227 million, and RMB 35.5246 million, respectively; the company has not yet achieved profitability, with net losses amounting to RMB 121 million, RMB 81.0381 million, RMB 366 million, and RMB 108 million, respectively, for the corresponding periods.

It is evident that Tasly Biopharmaceutical has made substantial investments in research and development (R&D). In 2018, R&D expenditure reached RMB 470 million; however, it decreased to RMB 270 million in 2019, representing a 42% decline. According to the prospectus, the R&D spending of RMB 470 million in 2018 was attributable to Tasly Biopharmaceutical’s intensified R&D efforts on the B1140 and T101 projects, as well as the addition of the T301 and T601 projects.From January to March 2020, as the relevant technical trials for the SY102 project still failed to meet the company’s expectations, and considering that the project would require substantial continued investment in the future, Tasly Biopharmaceutical decided to suspend its R&D efforts on this project, while temporarily halting the B1452 and B1453 projects.Stop.

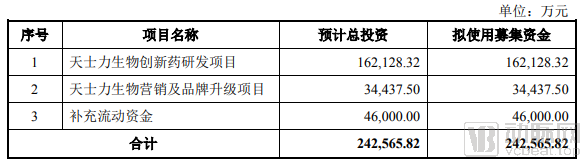

The funds raised in this offering will be primarily allocated to research and development, with a portion designated for marketing and brand upgrading, as well as for supplementing working capital.

According to the prospectus, Tasly Biological Products will expand the new indications for Puyouke. To date, B1140 (Puyouke for the treatment of acute ischemic stroke) is in the phase III clinical trial summary stage, with a new drug application planned for submission in the fourth quarter of 2020; B1448 (Puyouke for the indication of acute pulmonary embolism) is in the phase II clinical trial summary stage, with a pre-new drug application meeting planned for early 2021. Tasly Biological Products is fully promoting related processes to explore new markets such as acute ischemic stroke and acute pulmonary embolism.

Tasly Biopharmaceuticals will enhance its R&D capabilities, accelerate R&D progress, and expand and optimize its product portfolio. By increasing investment in innovative R&D, Tasly Biopharmaceuticals will further strengthen its biologics R&D capabilities, continuously enrich its product pipeline, and expedite product development. Meanwhile, the company will continuously develop and introduce industry professionals to bolster its R&D capabilities.

Tasly Biopharmaceuticals will strengthen its marketing infrastructure to enhance brand competitiveness. The company will accelerate the professionalization of its marketing team, leveraging members’ expertise in pharmaceuticals and marketing to refine a tiered and segmented marketing network for precision marketing. Meanwhile, Tasly Biopharmaceuticals will promote the scientific and systematic management of its overall marketing operations, increase market coverage for existing products, and provide systematic support for the future commercialization of products under development.