How the Pandemic Accelerated the Turning Point for China's Top Five Third-Party Medical Testing Companies: Insights from Their Semi-Annual Reports

Independent clinical laboratories in China emerged in the 1990s. After decades of development, the third-party medical laboratory (ICL) market has cultivated four leading players: KingMed Diagnostics, Dian Diagnostics, Da An Gene, and Adicon. Despite the presence of these four major competitors, the penetration rate of ICLs in China remains low. Approximately 95% of medical tests are conducted by hospitals, resulting in an overall ICL penetration rate of only 5%. In contrast, the ICL market penetration rate in the United States has reached 35%.

But this figure saw an incredible surge during the pandemic. In the first half of 2020, by the end of June, KingMed Diagnostics and Dian Diagnostics each had conducted over 10 million COVID-19 nucleic acid tests, with their combined testing volume accounting for approximately one-tenth of China’s total COVID-19 nucleic acid tests. The combined output of just these two companies represented 20% of the national total.

The market share of third-party medical laboratories has surged from 5% to 20%, a development that may well become a landmark event in the history of the industry’s growth.

Although the COVID-19 pandemic was an isolated event, the exponential surge in testing volume it triggered has brought about significant changes to the third-party medical laboratory market.

In the existing market, the overall landscape is expected to undergo further consolidation, leading to increased market concentration. Leading enterprises have strengthened their overall profitability under the severe test of the pandemic, with multiple independent clinical laboratories turning losses into profits and reaching an operational inflection point ahead of schedule. In terms of market coverage, third-party medical testing has successfully penetrated primary care markets that were previously difficult to access.

From the perspective of incremental market growth, third-party medical testing companies have been permitted to conduct COVID-19 nucleic acid testing directly for end consumers (C-end users). This public health prevention and control measure has spurred new business models such as direct-to-consumer (2C) services and “Internet + Laboratory Testing.” These emerging business models may become a disruptive force reshaping the future industry landscape of the third-party medical testing sector.

VCBeat (WeChat ID: vcbeat) analyzed the short- and long-term impacts of the global COVID-19 pandemic on the third-party clinical laboratory industry, based on the semi-annual reports of five independent clinical laboratory (ICL) companies in China and the United States.

Note: In addition to third-party medical testing services, Dian Diagnostics, Da An Gene, and BGI Genomics also engage in other businesses, such as reagents and instruments.

Analysis of the semi-annual report data reveals that in the first quarter, the third-party medical laboratory testing industry, like other sectors, was severely impacted by the sudden outbreak of the COVID-19 pandemic. As routine medical services were suspended due to the epidemic, the core routine testing services offered by third-party medical laboratory platforms came to a standstill. Furthermore, in the early stages, third-party medical laboratory platforms did not have the qualification to perform SARS-CoV-2 nucleic acid testing, as authorization for such testing had not yet been delegated to them.

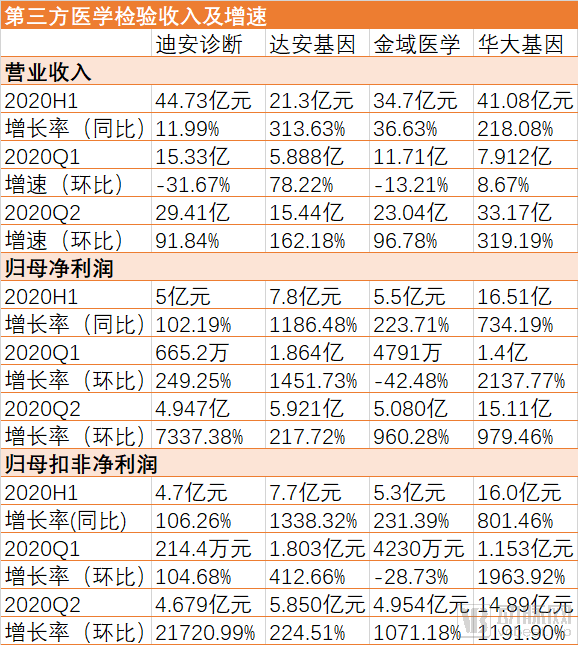

In particular, companies whose core business is diagnostic services, such as KingMed Diagnostics and Dian Diagnostics, suffered significant financial losses in the first quarter. KingMed Diagnostics reported Q1 operating revenue of RMB 1.171 billion, a 13.21% decline quarter-on-quarter; Dian Diagnostics recorded Q1 operating revenue of RMB 1.533 billion, a 31.67% quarter-on-quarter decrease. Meanwhile, Da An Gene and BGI Genomics, which also manufacture COVID-19 nucleic acid diagnostic reagents, were able to partially offset losses in their other business segments during the first quarter.

It was not until February 3 that policies permitted qualified third-party testing institutions to conduct nucleic acid testing, in an effort to strengthen epidemic prevention and control, enhance diagnostic confirmation capabilities, and reduce testing turnaround time. This marked the entry of third-party medical testing providers into the frontline of the anti-epidemic campaign. Following the decentralization of testing authority, these enterprises experienced an initial period of underutilized capacity before gradually reaching peak testing volumes. Leveraging advantages such as large-scale production capacity, strong technical expertise, specialized cold-chain logistics, and efficient, centralized resource allocation, third-party medical testing institutions emerged as the mainstay in nucleic acid testing for epidemic control.

The role played by third-party medical testing laboratories during the pandemic has also been recognized. On August 31, the State Council issued the “Work Plan for Further Advancing the Construction of Nucleic Acid Testing Capacity for COVID-19,” which stated that by the end of 2020, all secondary general hospitals should have nucleic acid sampling and testing capabilities; construction of urban testing bases and public testing laboratories should be completed; the role of independently established medical testing laboratories (hereinafter referred to as “third-party laboratories”) should be fully leveraged; regional mobile nucleic acid testing resources should be rationally allocated to establish a rapid-response deployment mechanism; and the capacity to complete population-wide nucleic acid testing within a relatively short period should be ensured in the event of localized cluster outbreaks.

In the second quarter, third-party medical laboratory enterprises saw strong business growth as nucleic acid testing volumes increased and routine testing services resumed.

Taking KingMed Diagnostics as an example, its revenue bucked the trend in the second quarter, with nucleic acid testing income growing rapidly. Meanwhile, as the domestic epidemic eased, routine testing services also saw an effective recovery. The operating revenue for the second quarter reached RMB 2.304 billion, representing a quarter-on-quarter growth rate of 96.78%. Overall, KingMed Diagnostics achieved an operating revenue of RMB 3.475 billion in the first half of 2020, marking a year-on-year high-speed growth of 36.63%.

The “black swan” event of COVID-19 not only directly impacted the operating revenues of independent clinical laboratory (ICL) companies, but also enabled some enterprises to enhance their overall profitability and achieve leapfrog business development amidst the major test posed by the pandemic.

During the special period of the first half of 2020, Dian Diagnostics reported total diagnostic service revenue of RMB 2.049 billion, a year-on-year increase of 55.51%, with net profit doubling. Notably, in the first half of this year, eight of Dian Diagnostics’ ICL laboratories turned profitable. To date, the company operates 38 ICL laboratories, 29 of which are profitable, signaling an earlier-than-expected operational turnaround.

Generally speaking, from the perspective of operating a single laboratory, the first 3–5 years are typically characterized by investment and patient acquisition, with profitability usually achieved after a 3–5 year ramp-up period. Undoubtedly, the pandemic brought a significant surge in patient volume to individual laboratories, thereby accelerating this process.

Another company that achieved leapfrog development in third-party medical testing services during the pandemic isBGI Genomics.BGI Genomics’ third-party clinical laboratory services are integrated into its comprehensive precision medicine testing solutions. Previously, these comprehensive solutions primarily provided one-stop high-throughput gene sequencing laboratory solutions to healthcare institutions and third-party testing companies.

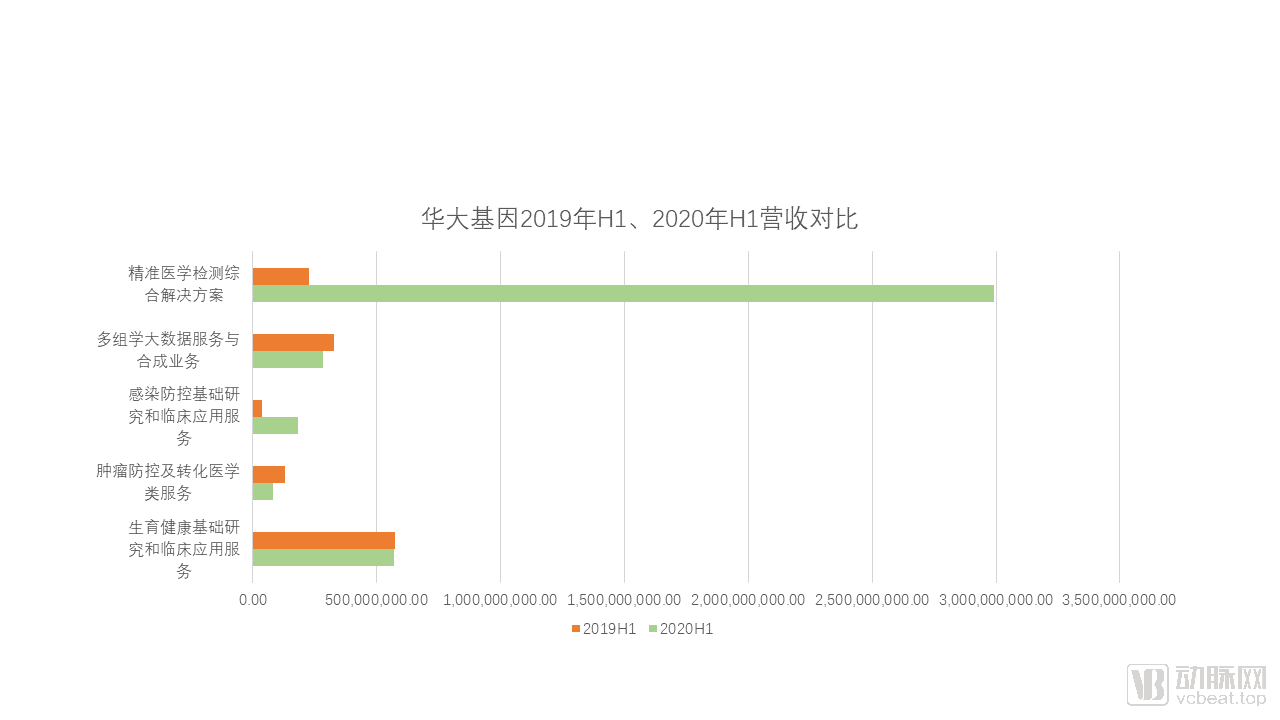

In 2019, the comprehensive solutions for precision medicine testing generated RMB 570 million in revenue for BGI Genomics, accounting for 20% of its total revenue and ranking as its third-largest revenue source.

In the first half of 2020, BGI Genomics' comprehensive solutions for precision medicine testing accounted for 70% of its revenue, with its infectious disease diagnostics business generating RMB 2.99 billion, a year-on-year increase of 1,230.36%.

As can also be seen from the table above, BGI Genomics’ primary revenue previously stemmed from basic research and clinical application services in reproductive health. The robust growth of its third-party medical testing business has now created new opportunities for incremental business expansion.

During the pandemic response, BGI’s “Fire Eye Laboratory” gained widespread public attention and earned broad recognition from all sectors of society. Worldwide, the maximum daily testing throughput of BGI’s “Fire Eye” laboratories exceeded 200,000 samples. To date, BGI has cumulatively operated 58 “Fire Eye” laboratories overseas, across 17 countries and regions.

Previously, BGI Genomics’ primary business model for third-party clinical laboratory services involved providing instruments, reagents, and service solutions to healthcare institutions and third-party clinical testing companies. During the fight against the COVID-19 pandemic, BGI Genomics’ infection prevention and control business and its comprehensive precision medicine solutions established direct collaborative relationships with multiple national governments, multinational corporations, foundations, and non-governmental organizations. Evidently, BGI Genomics’ contributions to combating the pandemic have also inadvertently created opportunities for the future expansion of its third-party clinical laboratory services.

The “black swan” event of COVID-19 has not only the potential to reshape the landscape of the third-party medical testing market and rewrite corporate development trajectories, but post-pandemic market demands and policy directions will also drive the third-party medical testing market toward higher-quality development.

First, under the impact of the COVID-19 pandemic, market concentration in the third-party medical testing sector is expected to increase. In the early stages, the pandemic prevented the delivery of routine medical services, as most healthcare resources across China were redirected toward epidemic prevention and control, severely disrupting routine care. This has intensified competition for smaller third-party medical testing providers with limited technical capabilities and narrow service networks, creating opportunities for market consolidation within the industry.

The core competitiveness of Independent Clinical Laboratories (ICLs) lies in reducing service costs and enhancing service quality through centralized and large-scale operations. The increase in industry concentration is an inevitable trend for the ICL sector, a process that was accelerated by the COVID-19 pandemic. A comparison with the development of the third-party medical testing industry in the United States reveals that the U.S. ICL sector has undergone two major phases: an initial stage characterized by market consolidation and increased concentration, leading to the formation of large-scale groups, followed by a later stage marked by the emergence of specialized enterprises in niche fields and a subsequent decline in concentration.

In the 1990s, the combined market share of Quest and LabCorp, the two giants of third-party medical testing in the United States, reached 60%, but has since declined to 50%. The rise and subsequent fall in market concentration can be attributed to two phases. In the first phase, during the initial wave of market consolidation, many small and medium-sized independent clinical laboratories (ICLs) were absorbed or eliminated. In the second phase, some of the small and medium-sized ICLs that survived the consolidation shifted their focus toward more specialized niche segments, thereby capturing a certain share of the market.

The COVID-19 pandemic will undoubtedly accelerate the consolidation of China’s independent clinical laboratory (ICL) market, driving the industry toward higher-quality development.

Meanwhile, in terms of industry standards and requirements post-pandemic, the National Health Commission issued a directive requiring all regions to further strengthen the development of clinical laboratory services in conjunction with COVID-19 prevention and control efforts. Secondary hospitals and above with adequate capabilities are required to conduct nucleic acid testing. This underscores that rapid, accurate, and comprehensive pathogen detection has become an essential clinical need.

In its prospectus, KingMed Diagnostics also noted that following the COVID-19 pandemic, particularly as epidemic prevention and control measures became normalized, the development of primary healthcare capabilities across China will be strengthened. Consequently, the demand for building disease-assisted diagnostic capabilities, represented by respiratory pathogen diagnosis, will gradually become more prominent. Key factors determining market success will include innovation in clinical testing technologies, clinical service capabilities, and the integration of multidisciplinary technical platforms. Meanwhile, quality safety and biosafety have been elevated to higher priorities. The market demands arising from the impact of the COVID-19 pandemic have imposed higher requirements on the third-party medical laboratory industry, thereby accelerating its transition toward high-quality development.

Whether in terms of reshaping the competitive landscape of the third-party medical testing market or accelerating the industry’s transition toward high-quality development, the shockwaves from the COVID-19 pandemic have primarily impacted the existing market base of third-party medical testing.

Another major impact of the pandemic on third-party medical testing laboratories was to unlock the growth potential of incremental markets. During the pandemic, third-party medical testing institutions were approved to provide COVID-19 nucleic acid testing services directly to individuals and social organizations, thereby opening a consumer-facing (C-end) traffic channel and further integrating “Internet + Laboratory Testing.” Online traffic and the consumer market have introduced new business models for third-party medical testing companies. In the future, consumer-oriented (B2C) businesses and new “Internet + Laboratory Testing” models may become disruptive forces reshaping the industry landscape.

In May this year, VCBeat reported that a total of 270 third-party medical testing institutions entered the market for individual nucleic acid testing for the novel coronavirus, with many companies also partnering with Tmall, JD.com, and WeChat to offer online appointment services.

In its prospectus, Dian Diagnostics disclosed the volume of online appointments for COVID-19 nucleic acid testing. During the pandemic this year, Dian Diagnostics partnered with online platforms such as Tmall, Alipay, Qunar, and WeChat to enable nationwide appointment scheduling. The company established 50 offline sample collection sites across 29 cities in China, completing over 42,000 scheduled tests during the pandemic period.

Although the proportion of online appointment-based tests remains relatively low among Dian Diagnostics’ tens of millions of COVID-19 nucleic acid tests, the breakthrough of 45,000 online appointments represents a significant milestone for the company, which has been continuously exploring its direct-to-consumer (2C) business.

Dian Diagnostics established Dian Health Checkup in 2014 to explore its B2C business starting with health management and physical examinations, making it one of the earliest third-party medical testing companies in the industry to venture into the consumer market. This year, Dian Diagnostics formed a dedicated B2C team and launched “Xiao Fei Jian,” an online B2C brand. Targeting high-frequency, easy-to-sample, and easy-to-store test items, the company has successively developed and launched eight products, including tests for HPV, obesity-related genes, pediatric/adult medication guidance, and gut microbiota.

According to data from the Dian Health Checkup Tmall Flagship Store, the best-selling product is the novel coronavirus nucleic acid test, while other products—such as paternity tests, pre-employment health examinations, and gut microbiota tests—have each recorded fewer than 100 sales.

Unlike the hospital market, where business needs are relatively fixed, the consumer-facing (C-end) market requires tapping into and meeting the substantial demand for mass health testing. This not only demands robust capabilities from third-party medical laboratory enterprises in areas such as quality control systems, cold-chain logistics, service network scale, and testing technology platforms, but also tests their ability to innovate business models. Further exploration and experimentation are needed to develop diverse testing offerings and service models that cater to the personalized and varied health testing needs of the general public.

VCBeat has also analyzed that, in the future, as consumers develop the habit of online consultations and internet hospitals expand rapidly, the integration of third-party medical testing services with internet hospitals to meet the laboratory testing demands generated during online diagnosis and treatment may break through the inherent business model of third-party medical testing.

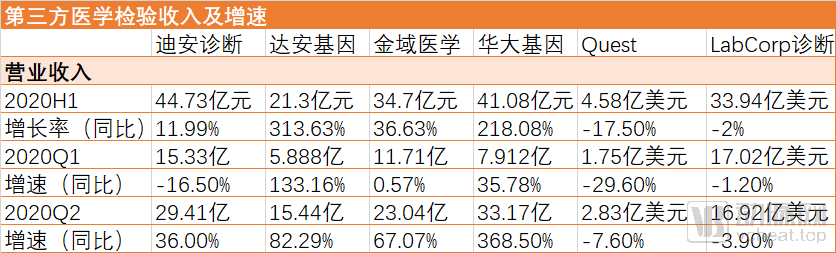

The global spread of the COVID-19 pandemic has impacted not only domestic third-party medical testing companies but also global giants such as Quest Diagnostics and LabCorp. A comparison of the performance of third-party medical testing providers in China and the United States during the pandemic reveals that the impact of COVID-19 on this sector in the U.S. has largely mirrored that seen elsewhere. In the first quarter, U.S. third-party medical testing companies performed normally in January and February. However, by March, the outbreak of COVID-19 significantly disrupted their operations. For instance, at Quest Diagnostics, total test volumes plummeted by 40% in the last two weeks of March, even after accounting for COVID-19 testing.

In terms of COVID-19 testing volume, domestic companies are on par with overseas giants. The main third-party independent laboratories for molecular diagnosis of the novel coronavirus in the United States are LabCorp and Quest Diagnostics. Among them, Quest currently provides up to 150,000 molecular diagnostic tests per day, and by August, the number of COVID-19 molecular diagnostics completed by Quest had reached 11.2 million. In recent weeks, LabCorp has processed approximately 180,000 tests per day, accounting for one-quarter of the 700,000 tests conducted daily in the United States.

In the second quarter, the increase in the volume of nucleic acid testing for the novel coronavirus helped mitigate losses for third-party medical laboratory companies in the United States to some extent. Judging from the revenue growth rates in 2020, it is evident that domestic third-party medical laboratory enterprises in China were less impacted by the pandemic and were able to recover quickly thereafter, a trend closely linked to China’s epidemic prevention and control measures.The United States has the highest cumulative number of confirmed COVID-19 cases globally, with a mortality rate exceeding that of many other countries, significantly impacting the routine testing operations of third-party medical laboratory companies in the U.S.

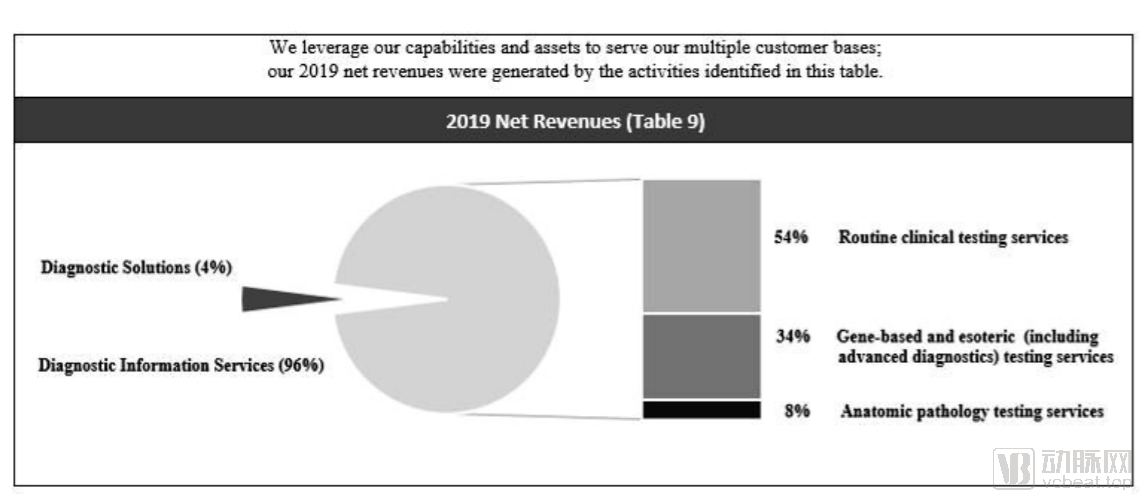

An analysis of Quest’s 2019 profit composition reveals that diagnostic information services constitute its primary revenue source, mainly comprising routine clinical testing and advanced diagnostic services. Due to the COVID-19 pandemic, the core business of U.S. third-party medical laboratory companies has declined significantly. Furthermore, the pandemic has led to higher personnel costs, which have prevented these companies from restoring their normal revenue growth rate in the second quarter.

Quest 2019 Net Profit Composition

Overall, while it may appear that the COVID-19 pandemic has pushed the third-party medical testing industry into a period of unprecedented transformation, in reality, the pandemic merely accelerated the industry’s pre-existing development trends.

A review of the development of independent clinical laboratories (ICLs) in China reveals that market growth has consistently preceded policy support. During the first decade of this century, large chain medical testing groups such as KingMed Diagnostics, Dian Diagnostics, and Adicon had already taken shape in China’s third-party medical testing market. However, at the policy level, it was not until 2009 that the former Ministry of Health issued the Basic Standards for Medical Laboratories (Trial), which formally established the legal status of independent clinical laboratories and provided third-party medical testing institutions with their official “identity.”

Subsequently, the implementation of policies such as healthcare cost containment and tiered diagnosis and treatment has driven rapid growth in China’s third-party medical testing market. KingMed Diagnostics, Dian Diagnostics, Daan Gene, and Adicon have emerged as the four leading players in this sector. Pursuing high-quality development has remained a central theme in the evolution of China’s third-party medical testing industry.

It is foreseeable that, in the wake of this epidemic, the third-party medical testing industry will play a more significant role in China’s healthcare system.

References

KingMed Diagnostics, Dian Diagnostics, BGI Genomics, and Daan Gene Semi-Annual Reports

Deeply Cultivating Medical Laboratory Testing: Entering the Harvest Period After Aggressive Expansion—An In-Depth Analysis of KingMed Diagnostics by Guoyuan Securities