Investment Landscape Behind the IPOs of 103 Chinese Healthcare Companies in the Past Three Years

In 2020, the healthcare sector once again gained favor in the capital markets due to its counter-cyclical nature and risk resilience. During the early stages of the COVID-19 pandemic, while the secondary market was largely stagnant, the healthcare sector bucked the trend by rising rather than falling, offering investors a glimmer of hope.

In recent years, the number of initial public offerings (IPOs) in the healthcare sector has gradually increased, with market capitalizations continually reaching new highs, achieving strong performance in the capital markets. According to the "2020 Hurun China Top 100 Private Health Enterprises," Hengrui Medicine had a market capitalization of RMB 372 billion, Mindray Medical RMB 291 billion, WuXi AppTec RMB 175 billion, and AliHealth RMB 162 billion. The total market capitalization of the listed companies amounted to RMB 4.7 trillion. This demonstrates that domestic healthcare enterprises are continuously breaking through and developing rapidly, supported by key factors such as policy, economic conditions, and growing health awareness.

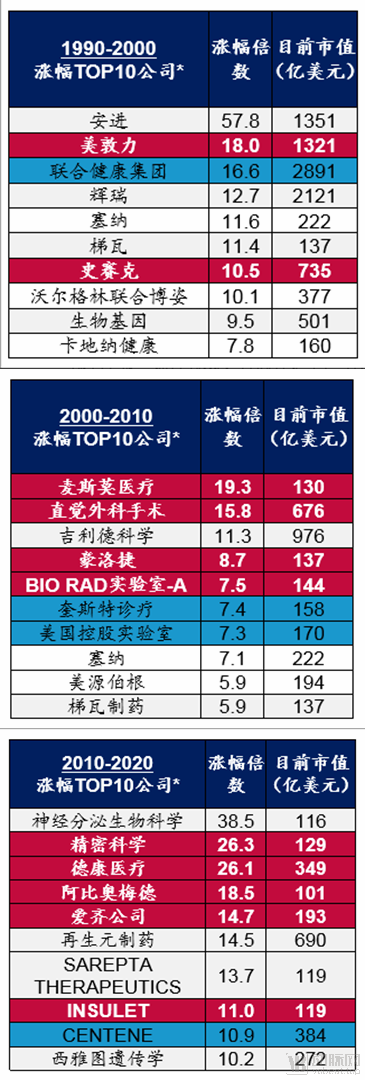

Looking at the relatively mature U.S. stock market, the healthcare sector’s share has been continuously rising, with its growth outpacing other industries. Among the top ten best-performing U.S. stocks, healthcare companies constitute the majority. For example, from 1990 to 2000, Amgen surged 57.8-fold and Medtronic rose 18-fold. Similarly, from 2000 to 2010, Masimo, Intuitive Surgical, and Gilead Sciences each posted gains exceeding 10-fold. From 2010 to 2020, Neurocrine Biosciences jumped 38.5-fold, Exact Sciences climbed 26.3-fold, and DexCom rose 26.1-fold.

(Image source: Haitong Securities)

It is foreseeable that numerous high-growth, large-cap giants will also emerge in China’s healthcare industry in the future.

Which niche sectors are more likely to give rise to industry giants? Among listed companies, which investment firms have secured the most bids? What is the secret behind these investors’ unique and discerning vision?

To address the aforementioned questions, VCBeat has compiled this article for our readers.

Core Views:

l In 2020, the number of listings is expected to break the 2017 record and reach a new peak.

l Policies, talent, capital, health awareness, and other factors are driving the development of China’s healthcare industry.

l The disease areas of cardiovascular and cerebrovascular diseases, cancer, and chronic diseases are more likely to incubate giant enterprises.

l Companies in the fields of innovative drugs, biologics, high-end medical devices, high-value consumables, and IVD will have greater development opportunities.

For a more comprehensive analysis, VCBeat selected all domestic healthcare companies that have listed on the A-share, Hong Kong Stock Exchange, or U.S. stock markets since 2018, totaling 103 firms. It should be noted that for companies with dual A+H share listings, only the date of their most recent listing was used for analysis.

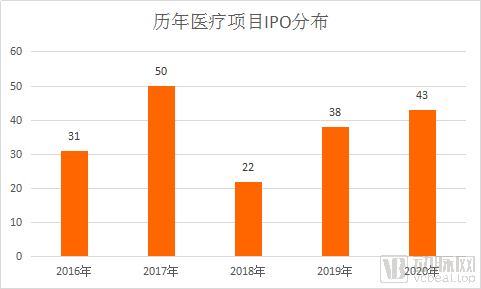

Since 2018, 103 domestic healthcare companies have gone public on the A-share, Hong Kong Stock Exchange, and U.S. stock markets. In contrast to the IPO boom of 2017, which saw 50 companies list, the IPO market cooled in 2018 with only 22 healthcare companies going public. The number rebounded in 2019 to 38 listed companies. In 2020, as of August 20, 43 healthcare companies had already gone public, poised to break the 2017 record and reach a new peak in the number of listings.

(Note: Data as of August 20, 2020)

Below is the specific list of healthcare companies that have conducted initial public offerings (IPOs) since 2018:

(Sorted by time)

In recent years, driven by changes in policy updates, talent development, capital influx, and health awareness, China’s healthcare industry has ushered in significant opportunities for growth.

In terms of policy, measures such as priority review, centralized procurement, innovation incentives, medical insurance reimbursement, and the Marketing Authorization Holder (MAH) system have been continuously strengthened, creating a favorable policy environment for pharmaceutical and medical device innovation. Meanwhile, ongoing updates to domestic policies have spurred the emergence of a wave of innovative enterprises, including internet healthcare companies.

In scientific research, talents who have studied or conducted research abroad have become the main force in technological innovation. With the development of scientific theories and innovative concepts, China’s research strength has significantly improved, leading to continuous iterations of innovative products. Many of these products have gained prominence on the international stage, even outperforming foreign competitors. Furthermore, the emergence of new technologies has facilitated product iteration by integrating them with traditional medical devices, making these products more suitable for clinical applications. For instance, combining monitoring systems with 5G, the Internet, big data, and artificial intelligence helps alleviate physicians’ workload, enhances monitoring efficiency, and promotes the decentralization of medical resources.

In terms of capital, numerous investment institutions are heavily focusing on the healthcare sector, providing substantial financial resources to support corporate development and innovation. In the primary market, financing and investment activities in healthcare have proceeded more smoothly than in other sectors. In the secondary market, investment firms have made significant bets on healthcare companies. The participation of these investors has provided strong financial backing for the growth of healthcare enterprises.

In terms of public awareness, health consciousness among Chinese residents has risen, leading to a gradual increase in healthcare-related spending. Meanwhile, as the global landscape evolves and the strategy of domestic substitution continues to be implemented, Chinese consumers are showing greater support for domestically produced products. Furthermore, driven by factors such as centralized procurement and medical insurance coverage, domestic products have become the preferred choice due to their high quality and competitive pricing.

Driven by multiple factors, China’s healthcare industry is experiencing rapid growth. Hengrui Medicine, with a market capitalization of RMB 486 billion, has become the most valuable company in the Chinese healthcare sector. The industry holds even greater potential for future expansion.

This analysis adopts the Global Industry Classification Standard (GICS) to categorize companies into 17 sub-sectors. When classifying companies by industry, GICS primarily considers revenue and net profit from core business operations, offering a more scientific approach.

According to the Global Industry Classification Standard (GICS), among 103 IPO projects, the pharmaceutical sector accounted for the largest share, followed by healthcare equipment and biotechnology.Based on an analysis of the companies’ core businesses, the aforementioned IPO projects span numerous subsectors, including innovative drugs, active pharmaceutical ingredients (APIs), medical devices, vaccines, health supplements, pharmaceutical distribution, pharmaceutical e-commerce, contract research organizations (CROs), medical education, medical aesthetics, and healthcare institutions.

So, which niche sectors are more likely to give rise to industry giants?

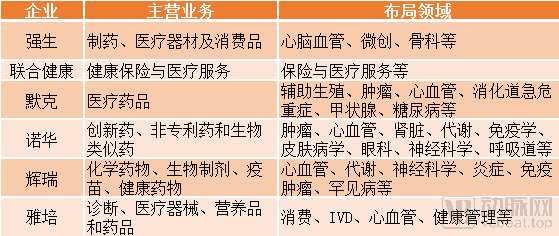

Looking at the more mature U.S. stock market, companies such as Johnson & Johnson, UnitedHealth Group, Merck, Novartis, and Pfizer have all grown into world-class enterprises. These top-market-cap companies have strategically focused their investments in areas such as cardiovascular and cerebrovascular diseases, orthopedics, oncology, and chronic diseases.

(Compiled from public information; graphic by VCBeat)

Therefore, therapeutic areas such as cardiovascular and cerebrovascular diseases, oncology, and chronic diseases are more likely to give rise to industry giants.According to the "Report on Cardiovascular Diseases in China 2018," the number of patients with cardiovascular diseases in China has reached as high as 290 million. The proportion of deaths due to cardiovascular diseases among all causes was 45.50% in rural areas and 43.16% in urban areas. This large patient population has given rise to a vast market, while the high mortality and disability rates underscore the critical need for effective treatment options.

According to the “2018 Pharmaceutical Industry Research Report,” the annual number of new malignant tumor cases in China has exceeded 4 million, with an incremental market value of over RMB 140 billion and an existing market value exceeding RMB 250 billion. There is a need to unlock the potential of the existing market in areas such as early cancer screening, cancer prevention, and cancer treatment, thereby benefiting more patients while enabling enterprises to grow and strengthen.

“Blue Book on Health Management: Report on the Development of China’s Health Management and Health Industry (2018)” points out that the number of chronic disease patients in China exceeds 300 million, with hypertension, fatty liver, dyslipidemia, diabetes, and chronic gastritis or gastric ulcers being the major chronic diseases. Chronic diseases account for a large proportion of medical expenditures; therefore, chronic disease management has been elevated to a national strategy, and companies providing chronic disease solutions will usher in significant growth.

From the perspective of the core businesses of large-cap healthcare companies in the U.S. stock market,Sub-sectors such as medical devices, innovative drugs, high-value consumables, health insurance, and healthcare services all hold the potential to produce world-class enterprises.

Medical devices, innovative drugs, and high-value consumables correspond to treatment plans that meet the rigid demands of patient populations. Health insurance aligns with disease prevention and early intervention, reflecting the growing emphasis on health among the population at this stage. Medical services remain an indispensable force in healthcare throughout history and across cultures, with physicians always serving as the core, irreplaceable role in the medical field.

With economic development and rising living standards, patients and individuals in suboptimal health conditions are placing higher demands on medical services. For instance, cardiac patients increasingly prefer treatment options with fewer side effects and complications, as well as minimally invasive or non-invasive approaches. Where there is unmet need, there lies opportunity for growth. Consequently, the heightened expectations for medical services and care quality will drive rapid advancement in innovative pharmaceuticals, high-end medical devices, and high-value consumables.

Drawing on the U.S. market as a reference, an analysis of domestically listed healthcare companies reveals that enterprises in innovative drugs, biologics, high-end medical devices, high-value consumables, and in vitro diagnostics (IVD) will have greater opportunities for growth.

It is worth noting that the vast majority of world-class companies operate across diverse sectors and place a strong emphasis on innovation. Meanwhile, high-tech enterprises are experiencing rapid growth; for instance, Intuitive Surgical has achieved a market capitalization of $80 billion driven by its single flagship product, the da Vinci Surgical System.

Since 2018, among domestically listed healthcare companies in China, pharmaceutical companies have been the most numerous, with a total of 34; followed by healthcare equipment and biotechnology companies, with 22 and 20 respectively.

Among them, 22 of the 34 pharmaceutical companies are listed on the A-share market; 14 of the 22 healthcare equipment companies are listed on the A-share market; and 11 biotechnology companies are listed on the Hong Kong Stock Exchange.

It can be seen that,Pharmaceutical and healthcare equipment companies prefer to list on the A-share market, while biotechnology firms favor the Hong Kong stock market; only a minority choose to list in the U.S.

Notably, the rise in the number of IPOs for healthcare projects is closely tied to the innovative regulations of the STAR Market. Among healthcare companies listed on China’s A-share market, the majority have chosen to list on the STAR Market.

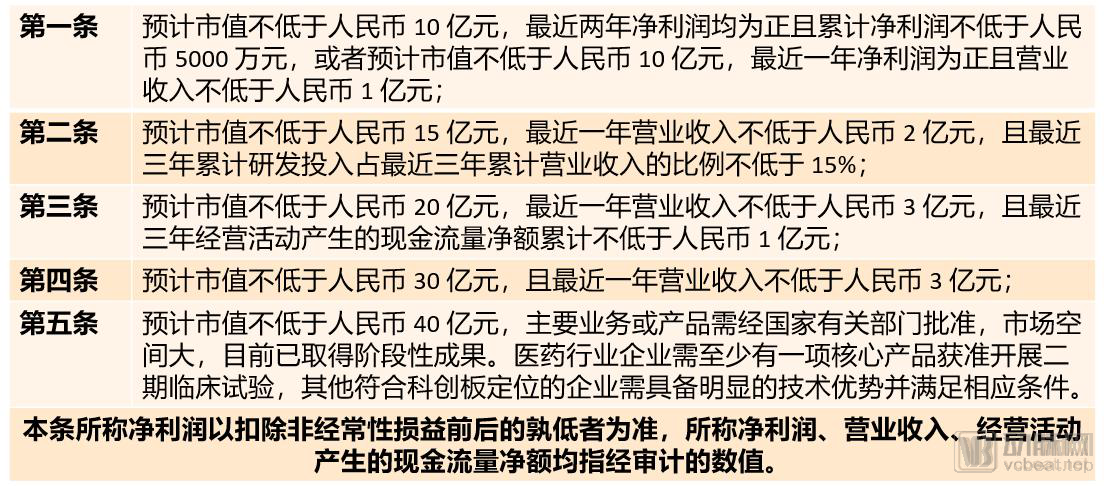

The STAR Market prioritizes support for high-tech and strategic emerging industries, including next-generation information technology, high-end equipment, new materials, new energy, energy conservation and environmental protection, and biopharmaceuticals. Its five sets of listing standards have lowered entry barriers, providing domestic enterprises with new channels for financing.

(Listing Standards for the STAR Market)

(Listing Standards for the STAR Market)

Based on the five listing standards established for the STAR Market, it is evident that these standards center on company market capitalization and form inclusive listing criteria by combining it with metrics such as revenue, cash flow, profitability, and R&D investment. For pharmaceutical companies, an additional requirement regarding R&D progress has been introduced: relevant enterprises must have at least one core product approved to enter Phase II clinical trials.

A key highlight of these five criteria is that "the higher a company's market capitalization, the lower its profitability requirements"; specifically, no profitability requirement is imposed if the company's market capitalization reaches RMB 4 billion.

According to VCBeat’s previous article, “Total Market Cap Exceeds RMB 900 Billion: 41 Companies Break Through—How Does the STAR Market Lead the Healthcare Industry’s Long-Term Growth?”, as of August 15, 2020, more than 150 stocks had been listed on the STAR Market, with none trading below their IPO prices. Focusing on the 41 constituent stocks in the healthcare sector, their total market capitalization reached RMB 929.4 billion, averaging RMB 22.6 billion per company, with the free-float portion accounting for approximately one-tenth of each company’s total value. Among them, Orient Gene achieved a price increase of 854% relative to its IPO price (peaking at 1,060%), while the average gain across the entire sector stood as high as 306.4%. To date, the market capitalizations of some STAR Market-listed companies have approached the average level of A-share companies.

This demonstrates that the STAR Market also exhibits exceptional fundraising capabilities. One contributing factor is the high-tech nature of its listed companies; compared with peers in other market segments, these firms represent high-quality investment targets and are highly favored by investors.

Among the aforementioned 103 healthcare companies, VCBeat collected financing information for 64 of them. The most frequently appearing investors included Hillhouse Capital, OrbiMed, CDH Investments, Sequoia Capital China, Lilly Asia Ventures, Ping An Ventures, Shenzhen Capital Group, Qiming Venture Partners, Honghui Capital, Legend Capital, and STO Capital.

For example, Hillhouse Capital was an early investor in companies such as BeiGene, Innovent Biologics, WuXi AppTec, CStone Pharmaceuticals, Frontage Holdings, Hansoh Pharmaceutical, Venus Medtech, Gan & Lee Pharmaceuticals, Hygeia Healthcare, Kangji Medical, Junshi Biosciences, and Tigermed. To date, Hillhouse Capital has cumulatively invested in more than 160 companies across the fields of biopharmaceuticals, medical devices, healthcare services, and pharmaceutical retail, including over 100 Chinese enterprises. The total investment amount exceeds RMB 120 billion, and the aggregate market capitalization of its portfolio companies surpasses RMB 2.5 trillion.

For example, OrbiMed has invested in companies such as Junshi Biosciences, Akeso, Hygeia Healthcare, Kangji Medical, Ocumension Therapeutics, Burning Rock Biotech, and Peijia Medical. To date, OrbiMed’s portfolio spans biopharmaceuticals, life sciences, medical devices, healthcare services, and diagnostics, with total net assets under management amounting to approximately $13 billion.

CDH Investments participated in early-stage investments in companies such as Venus Medtech, So-Young, I-Mab Biopharma, Nanxin Pharmaceutical, HitGen, SinoCellTech, and BeiGene. Among the more than 200 companies in CDH’s portfolio, over 40 are healthcare enterprises, accounting for approximately 20% of all its investment projects. To date, more than 60 of its portfolio companies have gone public, including as many as 16 healthcare firms, which represent about 27% of all listed companies. CDH Investments spans multiple sectors, including healthcare, retail and consumer goods, industrial manufacturing, financial institutions, high-tech services, and real estate, with healthcare being a key focus area.

In the field of healthcare investment, Hillhouse Capital, OrbiMed, and CDH Investments have made deep inroads and achieved outstanding track records. Among the 103 companies that have gone public since 2018, projects backed by these three firms account for approximately one-third of the total.

So, how do Hillhouse Capital, OrbiMed, and CDH Investments respectively select their investment targets? How do they help enterprises develop?

Hillhouse Capital

Hillhouse Capital is a star investment firm in the healthcare sector.

An analysis of Hillhouse Capital’s existing portfolio reveals a strong focus on the biopharmaceutical sector, with investments in companies such as Gan & Lee Pharmaceuticals, BeiGene, Innovent Biologics, I-Mab Biopharma, and WuXi AppTec. Meanwhile, Hillhouse has established a comprehensive presence across the entire healthcare industry chain. This includes medical device manufacturers such as Shenqi Medical, Biomere Medical, and Nanovision; digital health platforms like WeDoctor and JD Health; ophthalmology providers including Carestream Asia Pacific and Aier Eye Hospital; dental care groups such as Arrail Dental and Tongbu Dental; private hospitals like Beijing Lu Daopei Hospital and Guangzhou Jianfeng Eye Hospital; and pharmaceutical retail chains such as Xi’an Yikang Pharmaceutical Chain.

From a temporal perspective, Hillhouse has long favored biopharmaceutical companies, such as BeiGene, Junshi Biosciences, Innovent Biologics, Genor Biopharma, and CStone Pharmaceuticals. In 2017, Hillhouse expanded its portfolio to include specialized companies in ophthalmology and dentistry. By 2020, Hillhouse further increased its investments in medical devices; for instance, in the first half of the year, it increased its stake in MicroPort Scientific, invested in Kangji Medical and Peijia Medical, and participated in the private placement of Kaili Tai.

It is foreseeable that Hillhouse will gradually expand its presence in the medical device sector.Compared with the biopharmaceutical sector, China’s medical device industry still has significant room for growth. In the United States, the consumption ratio of pharmaceuticals to medical devices is 1:1, whereas in China, spending on medical devices lags far behind that on pharmaceuticals, further underscoring the substantial growth potential of the medical device sector.

As population aging intensifies and residents’ lifestyles change, the incidence of various diseases continues to rise, creating a substantial incremental market for medical devices. Meanwhile, advances in medical technology are facilitating the decentralization of healthcare resources, and improving household economic conditions are enabling medical device companies to gradually tap into the existing stock market. Breakthroughs in both the incremental and stock markets will drive rapid growth in the medical device industry.

On its official website, Hillhouse Capital states: “Hillhouse’s investment and operations teams can assist portfolio companies in making strategic moves at various stages of development, while working closely with entrepreneurs to build growth-oriented solutions from the ground up.”

OrbiMed

The homepage of OrbiMed’s official website states: “Immunotherapy, gene therapy, gene editing… the future of biomedical science is not as distant as one might imagine.” With support from policy and capital, biomedical science is gradually becoming a reality. OrbiMed, which focuses on investing in biomedical and life sciences companies, will gain greater renown for its role in advancing the development of biomedical science.

For example, among the companies invested in by OrbiMed, Burning Rock Biotech is a leading domestic enterprise in tumor next-generation sequencing (NGS), and Akeso Inc. holds a leading position in immunotherapy. Meanwhile, OrbiMed also focuses on medical device companies with strong scientific research capabilities and high technical requirements; for instance, Peijia Medical, an interventional medical device company, and Kangji Medical, a platform for minimally invasive surgical instruments and supporting consumables, have both received investment from OrbiMed. In addition, Ocumension Therapeutics, an ophthalmic drug platform, and Hygeia Healthcare, an oncology healthcare group, are also companies previously invested in by OrbiMed.

It can be observed that OrbiMed’s areas of focus include immunotherapy, precision medicine, gene editing, innovative drugs, hospitals, specialized medical groups, high-end medical devices, and high-value consumables. In terms of the development of its portfolio companies, OrbiMed has delivered the most outstanding investment performance over the past decade, with 53 of its invested companies going public. Meanwhile, six of its portfolio companies completed initial public offerings (IPOs) in the first half of 2020.

From a geographic perspective, Orbimed’s portfolio companies are widely distributed across North America, Asia, Europe, and other regions. As stated on Orbimed’s official website: “Unbound by time zones and undeterred by the cycle of day and night, our footprint spans the globe, all to ensure we can identify exciting medical breakthroughs worldwide at the earliest opportunity.”

From this perspective, OrbiMed places greater emphasis on healthcare innovation—both technological and commercial.Based on the current development of the healthcare industry, it is speculated that innovative drugs and high-end medical device innovations should be the key focus of OrbiMed.

In supporting its portfolio companies, OrbiMed typically invests as a lead investor to help create value. Meanwhile, OrbiMed possesses extensive experience and resources in assisting companies with their initial public offerings (IPOs). Furthermore, having invested in approximately 500 biopharmaceutical companies worldwide, OrbiMed leverages its robust global network and resources to help portfolio companies introduce products and technologies from overseas, identify international strategic partners, or enter global markets.

CDH Capital

Since its investment in Ciming Health Checkup in 2004, CDH Investments has been deeply engaged in the healthcare sector for 16 years.

In the first half of 2020, CDH Investments-backed companies including Fudan-Zhangjiang Bio-Pharm, HitGen, Nanxin Pharmaceutical, I-Mab Biopharma, and SinoCellTech went public one after another, demonstrating CDH Investments’ strength and capabilities in healthcare investing. To date, CDH Investments has invested in more than 40 healthcare companies, with 16 having successfully completed their initial public offerings (IPOs).

A review of CDH Investments’ portfolio reveals that the vast majority of its investments are in innovative drugs, oncology, and healthcare services. In the field of innovative drugs, CDH has invested in companies such as Luye Pharma Group, Kanghong Pharmaceutical, Poly Pharmaceutics, Grand Pharma, Leading Medicine, GenFleet Therapeutics, GemPharmatech, Sinocelltech, I-Mab Biopharma, and Nanxin Pharmaceutical. In oncology, CDH has invested in enterprises including Conlighting Bio, Ascentage Pharma, Sipi Health, Sirtex Medical, Maxin Biotechnology, Huiyi Huiying, and Harbour BioMed. In healthcare services, CDH has established a presence in specialized hospitals and institutions covering high-end obstetrics, pediatrics, health check-ups, orthopedics, ophthalmology, and plastic surgery, with investments in entities such as Ciming Health Checkup, Kangfang Hospital, Yining Hospital, and New Century Healthcare.

From the perspective of portfolio companies, these enterprises span multiple segments of the value chain, including R&D, manufacturing, sales, active pharmaceutical ingredients (APIs), finished dosage forms, and contract research organizations (CROs). They primarily focus on key technologies such as gene therapy and new drug development platforms, with oncology as the main therapeutic area. Thus, it is evident that CDH Investments favors innovative pharmaceutical companies dedicated to addressing oncology and other diseases.

Based on CDH Investments’ recent investment activities, we infer that its current or next-phase focus will primarily be on genes, innovative drugs, immunotherapy, oncology, and related fields.

In supporting its portfolio companies, CDH Investments has built a full-industry-chain healthcare ecosystem grounded in deep collaboration, facilitating mergers and acquisitions (M&A) for growth and internationalization. In assisting companies with M&A, CDH Investments’ cross-border M&A strategy is centered on the Chinese market, leveraging a global perspective and localized mindset to acquire leaders in relevant overseas industry sectors. Subsequently, through in-depth collaboration with portfolio companies, CDH Investments accelerates their development.