GRAIL Files for IPO: Multi-Billion-Dollar Cancer Early Detection Leader Set to Launch Galleri and DAC Tests

GRAIL

Early Cancer Diagnosis Technology Developer

The U.S. stock market in 2020 is destined to feature a significant presence for oncology NGS. Leading Chinese companies, Geneseeq and Burning Rock Biotech, have already listed on the NASDAQ this year. Now, GRAIL, the “funding king” of oncology NGS, has also entered the scene.

Backed by sequencing giant Illumina, with one foot in early cancer screening and the other in liquid biopsy, GRAIL was born with a silver spoon in its mouth. Subsequently raising a total of $1.69 billion across multiple funding rounds, GRAIL has undoubtedly become the “star player” in the field of tumor NGS.

Although GRAIL has announced its latest progress at major conferences such as ASCO and ESMO every year, these fragmented pieces of information have failed to provide a comprehensive overview of the company. Moreover, despite nearly five years of development since 2016, GRAIL has yet to launch its own product. There is widespread curiosity about how this well-funded oncology NGS early screening company is actually performing.

Now that GRAIL has filed for an initial public offering, we finally have the opportunity to gain insight into the true state of this enigmatic company through its prospectus.

In January 2016, Illumina, the world’s largest NGS provider, announced the establishment of GRAIL, with the aim of achieving early cancer screening through simple blood tests. Leveraging Illumina’s sequencing technology, GRAIL will develop a comprehensive cancer screening test based on direct measurement of circulating nucleic acids in the blood.

GRAIL, meaning “Holy Grail,” reflects Illumina’s expectations for the company. Illumina’s senior leadership believes that the Holy Grail of oncology lies in finding solutions capable of early-stage screening, which is precisely the goal Illumina has set for GRAIL.

Throughout GRAIL’s development, Illumina has consistently provided substantial support, participating in and even leading multiple rounds of financing for GRAIL. According to disclosures in GRAIL’s prospectus, Illumina remains its largest shareholder to date, with a stake of 14.6%.

The early cancer screening market targets the general population, and the vast demographic base ensures a highly promising market outlook for GRAIL. Meanwhile, as cancer research continues to deepen, there is growing recognition that intercepting tumors at an early stage of their development can significantly improve patient survival rates, compared with focusing solely on developing treatment regimens. Gene sequencing technology has long been regarded as the final piece of the puzzle in addressing the challenges of early cancer screening.

Consequently, a large number of tumor NGS companies have entered the field of early cancer screening to address this clinical need. GRAIL is both a pioneer and a dedicated specialist in this area.

Many tumor NGS companies choose to develop companion diagnostic products while carrying out early cancer screening, thereby achieving faster commercialization. In contrast, GRAIL has chosen to focus solely on breakthroughs in early cancer screening, continuously collecting data through large-scale clinical studies and refining its products, to the extent that its product has yet to enter the market. This has resulted in GRAIL still being in a state of no revenue, with no product sales and no services provided externally.

GRAIL is patient, but capital appears to be even more patient than GRAIL.

GRAIL's Financing History

Upon its establishment in 2016, GRAIL simultaneously completed a $100 million Series A financing round led by Illumina. In the subsequent years, GRAIL successively closed its Series B, C, and D funding rounds, bringing the total capital raised across these four rounds to $1.69 billion—equivalent to over RMB 10 billion—earning it the reputation as a “capital harvester” in the primary market.

GRAIL’s investors include not only Illumina and institutional investors, but also internet companies such as Tencent and Amazon, as well as pharmaceutical companies like Johnson & Johnson and Bristol Myers Squibb (BMS). These institutions and companies have recognized the potential of the tumor NGS early screening sector in which GRAIL operates, and believe that GRAIL’s business plan will enable it to capture this market.

So, what exactly did GRAIL do after securing the massive funding?

Over the past few years, GRAIL has been primarily focused on conducting clinical studies to continuously refine and upgrade its algorithms.

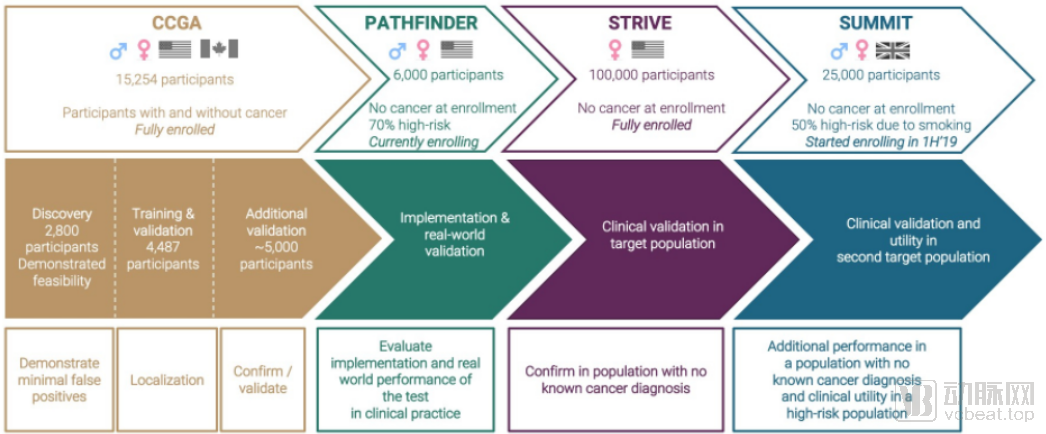

GRAIL's Major Clinical Studies

Specifically, GRAIL’s clinical research is primarily divided into four major programs: CCGA, STRIVE, SUMMIT, and PATHFINDER.

CCGA is GRAIL’s primary clinical study for product development, while the other three are prospective cohorts conducted in collaboration with different institutions.

CCGA Study Main Framework

In late 2016, GRAIL launched the Circulating Cell-free Genome Atlas (CCGA) project, which extracts and sequences cell-free DNA from patients and healthy individuals to compare differences between the two groups, thereby aiding early diagnosis.

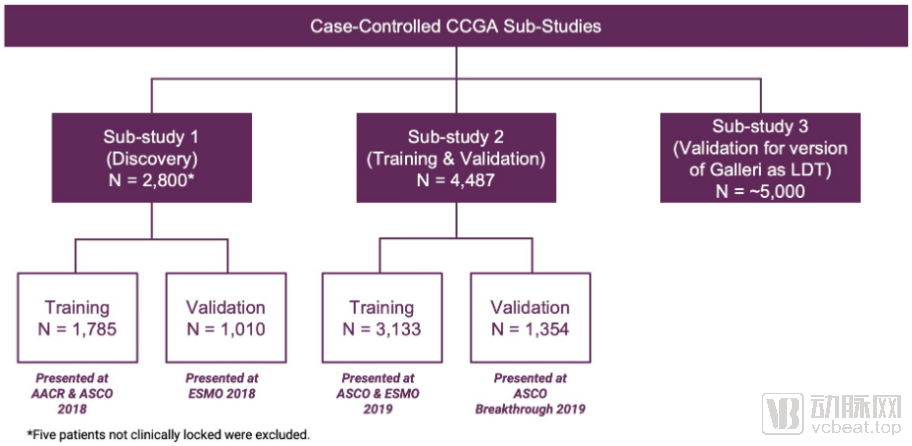

This is the first research initiative officially launched by GRAIL, which is divided into three distinct sub-studies. The three sub-studies are progressive in nature,CCGA-1 primarily focused on discovering detectable targets directly associated with tumors; CCGA-2 expanded the cohort and delved into algorithm training and validation; while the currently ongoing CCGA-3 is conducting further clinical validation of the outcomes from the first two phases, namely the final product.

To date, the first two studies of the CCGA project have been largely completed. The studies incorporated data from nearly 6,700 patients, including 4,487 participants enrolled in the CCGA study and 2,202 participants enrolled in the STRIVE study. These participants included both cancer patients and individuals without cancer.

The latest findings from the CCGA study have achieved a specificity of over 99% and a sensitivity of 55%. For 12 types of high-mortality cancers, the sensitivity can be further increased to 67%. More importantly, in more than 90% of positive tests, GRAIL accurately identified the location of the tumor signal.

In other words, based on current research findings, once this achievement is integrated into clinical diagnosis and treatment, it can not only identify potential tumor patients but also achieve relatively precise tumor localization, thereby enabling targeted clinical testing.

Based on its superior product quality and the urgent need for early cancer screening, the U.S. FDA granted GRAIL’s “multi-cancer early detection product” the Breakthrough Device designation in May 2019.

And now, this product has its own name. This cancer early screening product, operated as an LDT, has been named “Galleri” by GRAIL.According to GRAIL’s plan, it will officially launch as an LDT in 2021(Laboratory Developed Tests)Galleri was launched.

In addition to Galleri, GRAIL has also translated the findings of the CCGA study into another product, DAC (Diagnostic Aid for Cancer test).

Compared with Galleri, DAC enters the diagnostic and treatment pathway at a later stage, primarily to expedite the confirmation of diagnosis for patients with undiagnosed tumors. According to projections in GRAIL’s IPO prospectus, out of more than 12 million patients, 10 million would undergo invasive procedures or time-consuming clinical testing. These examinations can cause physical harm to patients or delay treatment. The launch of the DAC product will help clinicians achieve tumor diagnosis with greater efficiency.GRAIL is expected to launch DAC in the second half of 2021, also under the LDT model.

Overall, the value of the CCGA study has been reflected in GRAIL’s business model. The data collected from the CCGA study has become the foundational dataset for GRAIL’s research framework, and two products have already been developed based on this data, both of which are scheduled to be launched in 2021.

In other words, 2020 is expected to be GRAIL’s last fiscal year without revenue.

Following the CCGA study, GRAIL subsequently launched three prospective clinical trials—STRIVE, SUMMIT, and PATHFINDER—to further validate its product algorithms through long-term follow-up of healthy participants.

In April 2017, GRAIL, in collaboration with Mayo Clinic and Sutter Health, launched its ambitious STRIVE clinical study, which aimed to enroll nearly 120,000 women aged 18 and older and conduct long-term follow-up for each participant. Data from the prospectus indicates that enrollment for the STRIVE study began in February 2017 and was completed by November 2018, with a total of nearly 100,000 female participants enrolled. During the follow-up period of up to 30 months, these participants underwent regular mammograms, and blood samples were collected and stored at the time of each examination.

GRAIL’s initially designed STRIVE study was more ambitious, with an enrollment of 120,000 participants and a follow-up period of up to five years. Although the final scale was slightly reduced, this did not detract from STRIVE being one of the largest cohort studies for early breast cancer screening.

To date, GRAIL has not reported the clinical study results of STRIVE; however, partial data from STRIVE were incorporated into the CCGA study. Based on the aforementioned data, these account for approximately one-third of the current CCGA study dataset.

In early 2019, GRAIL partnered with institutions such as University College London to launch the SUMMIT study. The initiative was originally expected to recruit 50,000 participants aged 50–77 in the United Kingdom who were free of cancer at enrollment. However, according to the research plan disclosed in its prospectus, the projected enrollment for the SUMMIT study was reduced to 25,000 participants. Participants will undergo annual blood sample collection during the first three years, followed by two years of annual follow-up visits, and long-term follow-up through national health registries.

Since the program was officially launched in April 2019, only 11,639 participants have been enrolled over the past 16 months. Notably, half of the participants in the SUMMIT study are required to have a history of smoking, suggesting that this study may focus more specifically on early screening for lung cancer.

In December 2019, GRAIL launched its fourth clinical study, PATHFINDER. This prospective clinical study aims to provide additional clinical evidence for Galleri and is expected to enroll 6,200 participants. As of August 31, the trial had enrolled only 2,585 participants.

GRAIL itself also acknowledged in its prospectus that the slow enrollment in the SUMMIT and PATHFINDER studies was, to some extent, affected by the COVID-19 pandemic.

Large-scale, long-term clinical trials indeed introduce greater uncertainties in patient enrollment and follow-up. Although GRAIL has selected partners to jointly advance this process in order to enhance the stability of its clinical studies, we have indeed observed slight discrepancies between the final outcomes of GRAIL’s studies and their initial designs in practice. For researchers who are also preparing to launch large-cohort clinical trials, this may suggest that expectations for such studies should be appropriately moderated.

However, overall, GRAIL’s several prospective clinical studies have provided more data for research and learning for its products, and will offer additional support in terms of clinical evidence once future studies are completed.

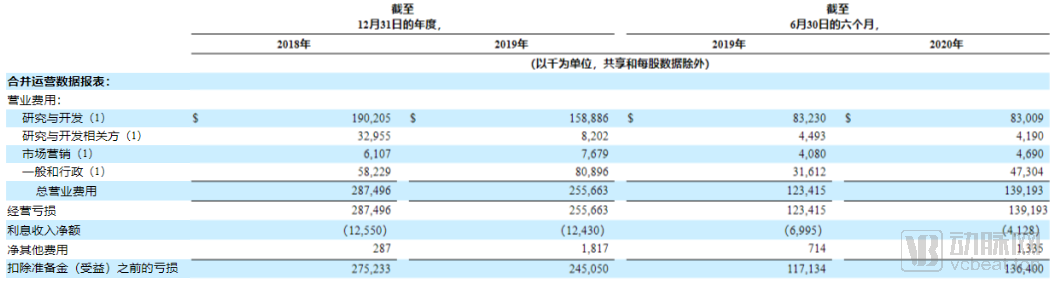

As previously mentioned, GRAIL has yet to generate any revenue to date. The substantial funds raised through financing have been primarily allocated to clinical research.

GRAIL: Selected Financial Data

Due to the absence of revenue, operating expenses are listed as the first line item in GRAIL’s financial statements.

R&D-related expenses primarily consist of two components: direct R&D expenditures and payments to R&D-related parties. In 2018, GRAIL’s total R&D spending reached $223 million. In 2019, with the phased completion of the CCGA project, GRAIL’s R&D expenditures experienced a slight decline, decreasing to $167 million. Overall spending in the first half of 2020 was comparable to that in the first half of 2019. It is therefore reasonable to expect that GRAIL’s full-year loss in 2020 will likely remain on par with that of 2019.

Although there was a certain narrowing in 2019, the R&D expenditure of $167 million remained a substantial sum. This significant spending was primarily driven by GRAIL’s simultaneous conduct of multiple large-cohort clinical studies, along with the corresponding data curation and analysis efforts.

Compared with clinical trials for pharmaceuticals, GRAIL’s follow-up intervals are longer, and there is no need to bear high drug costs, which seems to make it easier to control the costs of clinical research. However, the scale of GRAIL’s clinical studies is excessively large. Clinical trials involving tens of thousands of participants, coupled with the ongoing expenses associated with long-term follow-up, mean that even if GRAIL ceases to initiate new clinical studies in the coming years, the few currently ongoing trials alone have already set the tone for sustained high R&D investment by GRAIL in the short term.

However, from another perspective, we must also analyze whether GRAIL’s substantial R&D investment is justified.

First, from a strategic perspective,GRAIL first developed the algorithm for its early cancer screening product by comparing healthy individuals with cancer patients in the CCGA study, and subsequently further validated the algorithm’s accuracy in larger-scale prospective cohorts. This product development pathway is fundamentally sound.

Secondly, regarding the issue of cohort size. Taking the largest STRIVE clinical study as an example, STRIVE enrolled nearly 100,000 participants, all of whom were healthy individuals. GRAIL needs to conduct long-term follow-up on these subjects and further analyze those who develop incident breast cancer during the follow-up period in order to generate core value for the development of its early screening products. The incidence rate of breast cancer in the healthy population is less than 1%. Even with a research cohort of 100,000 individuals, the number of breast cancer cases captured during long-term follow-up may amount to fewer than 1,000. Such a scale is barely sufficient for algorithm validation.

Therefore, it was not due to GRAIL’s arrogance, but rather because the company chose the challenging path of early cancer screening from the outset, making substantial clinical research expenditures indispensable.

Fortunately, with Illumina as a backstop and consistent recognition from the capital markets, GRAIL has managed to reach its current position despite the immense pressure of substantial R&D investment.

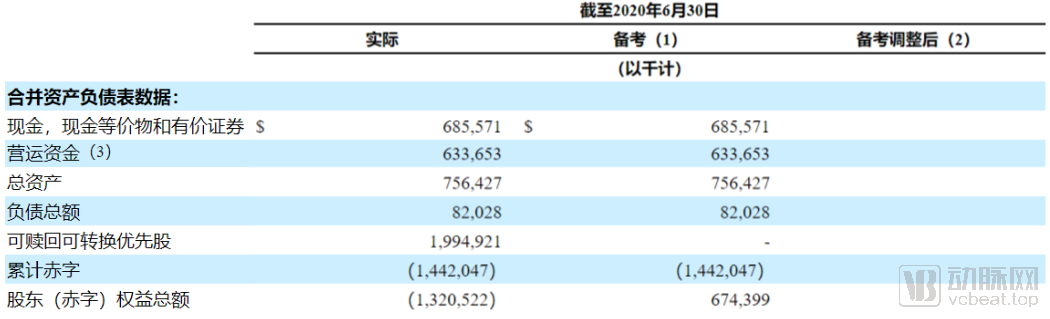

Overview of GRAIL’s Assets

From an asset perspective, GRAIL currently maintains ample cash reserves and a low debt-to-asset ratio. Even if the current IPO attempt proves unsuccessful, the company is unlikely to face any significant short-term liquidity pressures.

Regarding future planning, GRAIL will largely continue to focus on its ongoing business operations. The proceeds from this financing round will primarily be used to advance the commercialization of its two products, Galleri and DAC, and to build out its sales team, while the remaining funds will be directed toward continuing R&D projects.

According to the information disclosed in the prospectus, GRAIL is at a critical stage of commercialization. Core studies have been preliminarily completed, and the product is scheduled for market launch next year; prospective clinical studies are gradually beginning to provide valid data for product development.

When GRAIL was founded, it set off a wave of interest in early cancer screening. Now, with GRAIL’s IPO application, will next-generation sequencing (NGS)-based early cancer screening once again become a hot trend?

With the market launch of GRAIL’s products, we now seek to address another question: Is tumor NGS-based early screening finally poised for commercialization?